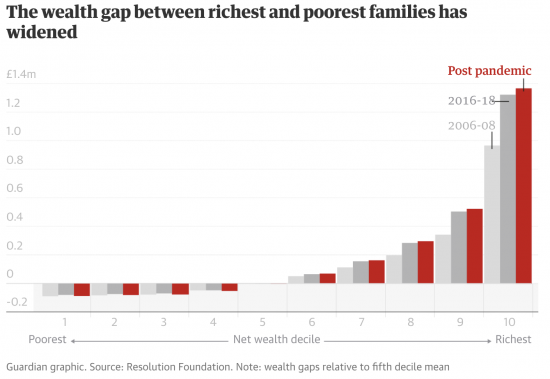

The Resolution Foundation has published a report this morning in the massive increase in wealth that the wealthiest in the UK have enjoyed during the Covid crisis.

The Guardian report makes clear, albeit inadvertently, that the Resolution Foundation does not understand the reasons for this. As they note a Foundation spokesperson saying:

The Covid-19 crisis has seen a highly unusual combination of a sharp reduction in economic activity, and a sharp increase in household wealth. Many families have been forced to save rather than spend during lockdowns, while house prices have continued to soar even while working hours have plummeted.

But this is not the reason for the increase in wealth. Savings have happened, of course. But the real reason why that has happened is not because of savings in season ticket costs, or on nights out. Nor has house price inflation happened by chance. Instead these things are the direct result of the government running substantial deficits whilst simultaneously denying people the chance to save with the government. This has forced money into cash accounts (which have grown in value, enormously) and private sector, speculatively based investment, including housing.

It is a shame that the Resolution Foundation do not understand this. It is one of the many left of centre think tanks in denial on modern monetary theory (MMT). If it wasn't it would understand the simple fact that government deficits always increase private wealth. What they are documenting is not in that case a surprise. It is an inevitability. Government created money has either to be reclaimed by it through borrowing in the short term or tax in the long term, or it stays in the economy where the impact of multipliers means it inevitably ends up in the hands of the already wealthy, even if not paid to them the first instance. This is what has happened here.

Those gains they have secured have, because some have been saved speculatively, increased in apparent value over and above the sum injected into the economy by the government. The multiplier effect appears to be something like threefold.

As the Resolution Foundation has noted, those at the lower end of the income spectrum have not gained, at all. On average they have dissaved:

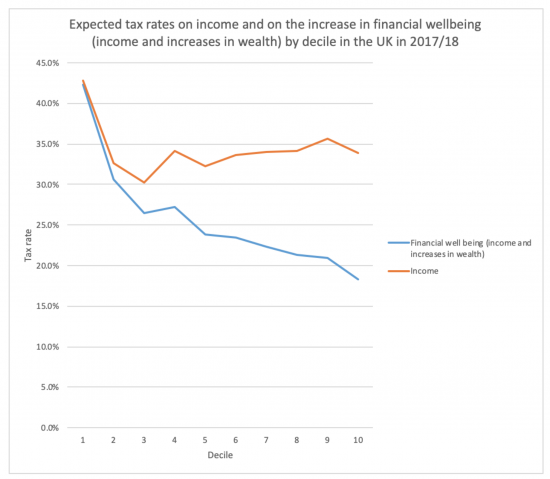

I predicted this last year. Doing research then on data for the years 2011 - 2018 I showed that if the increase in capital value was considered to be income (as it is) then the overall tax rate was deeply regressive:

The wealthiest not only gain the most, they pay least tax.

The answer is obvious. We need to tax wealth more. But since we have no effective wealth tax and it would take time to create one what we instead need to do is tax the income from wealth a lot more. As it us, almost every firm of income from wealth is taxed less and enjoys more reliefs and allowances than income from work does. That is, straightforwardly, wrong.

I explain what needs to be done in this series of blogs:

- There is significant room for wealth taxation in the UK

- The UK could tax wealth more

- The relationship between income, wealth and tax

- The TACS approach to wealth taxation

- Reforming taxes on wealth by equalising capital gains and income tax rates

- The need for an investment income surcharge

- Capping total ISA contributions

- Abolishing the personal savings tax allowance

- Restricting pension tax relief

- Abolishing higher rate tax relief on gifts to charity

- Reforming council tax

The advantage of MMT is that as pure theory it explains this. The Resolution Foundation miss out by not comprehending what is actually happening. I hope that they will, soon. It is essential that this inequality is tackled, but that requires that its cause be properly understood as well.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Maybe it doesnt have to be labelled ‘MMT’ – as that seems to frighten the horses. You describe the process in terms of dynamic accounting identities which identify where the vast money creation/ govt deficit has to end up – ie in asset price inflation etc. Surely they have to accept that?

Maybe they see themselves as merely measuring the increasing wealth inequality, and dont want to stray tOo deeply into causes, or to look at the implications – in terms of taxing income from wealth etc.

After all, this was funded by Standard Life!

You may be right

And the Standard Life foundation is not Standard Life

I know it is confusing….

Always good to know who these people are.

The Standard Life Foundation is a charity largely funded, it seems, from “unclaimed assets” from the demutualisation of Standard Life in 2006 – something like 10% of the former policyholders did not claim their share entitlement straight away, so their shares valued at around £300m of went into a trust from whence they could be claimed. After 10 years, there was £81m left that was donated to the Foundation – https://www.standardlifefoundation.org.uk/en/about and https://unclaimedassets.co.uk/standard-life-unclaimed-shares/ That is quite some endowment. In the year to 31 December 2019, it had £608k of investment income, and £7.5m of investment gains, and spent £1.1m. It trustees include Alistair Darling, James Daunt and Naomi Eisenstadt, and its chief executive is Mubin Haq.

Whereas the Resolution Foundation was set up by Clive Cowdery in 2005 and is largely funded by his Resolution Trust (in the year to 30 September 2019, that was £1.6m of its £1.8m income, and it spent about three times its reserves, so it is pretty hand to mouth). Cowdery’s insurance run-off company Resolution plc was acquired by Pearl in 2008. Since 2015 the Foundation has been directed by Torsten Bell and David Willetts, who are presently its chief executive and the president of its advisory council. Cowdery remains the chair of its trustees.

Oh, should have given a link for the Resolution Foundation: https://www.resolutionfoundation.org/about-us/team/

I don’t know about the Resolution Foundation specifically, but it seems strange that often it is the same think-tanks who complain that government creating (“printing”) money to enable spending would cause excessive retail inflation that then don’t understand that creating money in the asset markets (through bond buy-back under QE) will analogously cause asset inflation.

Now the MMT logic is to use tax to control inflation caused by money creation, which in this case means taxing assets (wealth) or as you recommend pragmatically the realising of asset gains. But going back to the cause of the problem, is it essential to use QE as the way of protecting the economy at times it is threatened (whether by Covid or failure of the banking sector) or could it be done differently without that unwanted side-effect?

The problem is that QE money is injected via banks

It could be spent in directly – which was my Green QE or Corbyn’s Peoples’ QE plan

I am not sure it matters much as to how it gets from the BoE to the Treasury. At the moment the government sells a bond which is bought by the BoE via a market intermediary. The effect is a credit to the Treasury DMO account at the BoE, which then gets used to fund spending. At the moment this money is being spent into the economy on covid support, extra Universal Credit, track and trace, PPE, bungs to mates, etc. So that will have a direct effect on the economy which pre-2020 QE did not. Whichever way it is initiated, though, the new money will simply circulate around BoE accounts and gravitate to the reserve accounts of the clearing banks. The only way it could actually leave the BoE would be as cash bank notes. As you have noted a state deficit enables private savings. Those savings will gravitate to the wealthy simply because wealth always trickles up unless some steps are taken to counter that. £20 extra per week on Universal Credit will improve life for those at the bottom, but they will spend it so it will not increase their wealth. The profits and revenues of the companies flow upwards to the owners. I think if the government simply ran an overdraft and dispensed with the bond the effect would be the same. The new money will still all end up in the commercial bank reserve accounts and the spending still generates savings largely for the wealthy. The wealthy will try to invest their extra savings somewhere which is where the asset price inflation is coming from. Pre-2020 the QE wasn’t being directly spent by the state but was forcing investors out of gilts and making them invest their savings somewhere else. That wasn’t increasing private savings, but switching them out of a term deposit account at the BoE (as a gilt really is) into a current account (both for the former owner of the gilt and into the reserve account of his/her bank). In this case the QE would not directly increase savings (thus wealth), but asset price inflation would occur as people had to purchase something other than gilts.

The pre-2020 QE was completely misguided as it would never have much real impact on the economy. The present QE is better as it is real spending and thus having a real impact on the economy. However that means it is vital as to what the state buys (Universal Credit – good, £40 billion to Serco for an ineffective track & trace – bad), and as you have pointed out the tax system needs to collect the excess wealth and recycle it back into state spending. To keep the capitalist system going is always going to need a constant process of removing excessive concentrations of income and wealth and re-distributing them. Otherwise Marx would turn out to have been correct about the inevitability of a revolution.

In the context of the new Scottish currency, I have been looking at central bank base money and I don’t see any way that it can ever leave the central bank other than as notes issued by that bank. As soon as anyone deposits one of those notes into a bank then it just reverts to the reserve account of that bank at the central bank. In the Scottish context when we sell the S£ into existence and the Scottish Reserve Bank acquires the sterling, what it ends up with will be the contents of the reserve accounts that banks in Scotland currently hold at the BoE. That just moves £60 billion or so out of their reserve accounts and into the SRB account at the BoE. As with other central banks the SRB would have an account at the BoE for holding the sterling reserves of Scotland, as it would have an account at the ECB to hold Euro and the US Fed to hold dollars. So even in this situation Scotland’s sterling reserves still don’t actually leave the BoE.

Much it agree with

Especially this:

“ I think if the government simply ran an overdraft and dispensed with the bond the effect would be the same. The new money will still all end up in the commercial bank reserve accounts and the spending still generates savings largely for the wealthy. “

Spot on

That is the flaw in MMT that does lot prove t wrong, but which has to be addressed

@Steve, wouldn’t reversing QE essentially mean selling the government bonds that have been bought back? Which would look a lot like increasing government borrowing, with political implications.

From Richard’s other writings, reversing money creation that went on government spending presumably could be done by incentivising private saving (not usually politically contentious) or increasing taxation (more problematic, though if the spending had successfully expanded the economy the change in tax balance might not need to be particularly high).

I am sure Richard will put me right if I have misunderstood that aspect of MMT.

My para:

Para 1, correct

Para 2, correct. The result is demand will be sucked out of the economy. We face a major downturn. Reversing qE would make it worse.

Para 3: you have it right

@Jonathan

The point is that QE money injected by banks can easily be unwound as and when the time is right.

If it’s so easy tell me why it has never happened?

And tell me what would be the consequence of it?

How would you make it work?

Another cause of inequality is low wages and low benefit rates such as the £20 a week reduction in Universal Credit for millions of claimants. True the asset/wealth bubble is a major problem but the bottom end of income distribution needs attention as well.

It’s not been unwound as the time hasn’t been right. The BoE has made that clear.

It would be very easy to unwind, just reversing the process that created the money in the first place.

You never talk about the (negative) consequences of your MMT proposals!

I did not ask how it might be do9ne

Why should it be done?

What would be the consequence be?

Could the economy survive it?

What would the interest rate consequence be?

Come on – show you know what you are talking about

One question I might ask in all this is the role of Credit Unions & Building Societies, which, as far as I can see dont ‘create, money in the way the clearing banks do.

If there role were to be expanded and that of conventional banks curtailed what would the impact be on monetary policy and the economy?

Credit unions and conventional building societies that did not act as banks do not create money the way banks do

I think their role is different to banks

I am not sure they would or would need to curtail banking

I also can’t see them as being material to the economy, even though they could have useful microeconomic significance

So I am not sure that I can answer your question: I do not see a zero sum, which you imply

[…] The increase in wealth inequality during Covid is not an accident: it is a design fault that needs t… Richard Murphy […]

May I add this about the consequences of a failure to fairly distribute wealth, income and power?

t is unlikely that an economy of any country will be healthy if the people in it are not healthy. Health inequalities are measurements of life expectancy and periods of life free from disability. These measurements enable comparisons of health inequalities to be made among countries and within regions of a country. There is a gradient to health inequalities. At the bottom are those of lowest socioeconomic status. At the top of the gradient, those of highest socioeconomic status. On average,the richest will live longer than those below and will have lives free from disability for longer than those below.

Health inequalities are avoidable and do not occur randomly or by chance.They are socially determined and are largely beyond individual control. They are unfair, disadvantaging the poorest, damaging their health and shortening their lives. They are enormously costly economically and in terms of lost potential for society as a whole.

Although it was not always so, Scotland has a bad record of health inequalities. Worse indeed than English regions with similar levels of deprivation such as Liverpool and Manchester. These are “deaths of despair”.

http://eprints.gla.ac.uk/226403/

It was not always so.

David Walsh’s Talk 1

Thanks

This link should work.

Here’s the link for David Walsh’s talk – https://www.youtube.com/watch?v=i7igJmiuleE