The Tax After Coronavirus (TACs) project suggests that the most important role of tax in a jurisdiction is to shape its society and economy in the fashion that its government, and those who elect it in a democracy, might desire. This post introduces that issue within the context of the UK's capacity to increase the taxation of wealth to create greater equality in society as well as to raise additional tax revenue if that was ever considered desirable.

The Tax After Coronavirus (TACs) project suggests that the most important role of tax in a jurisdiction is to shape its society and economy in the fashion that its government, and those who elect it in a democracy, might desire. This post introduces that issue within the context of the UK's capacity to increase the taxation of wealth to create greater equality in society as well as to raise additional tax revenue if that was ever considered desirable.

Introduction

In the aftermath of the coronavirus crisis there appears to be a widely held opinion that taxes on wealth should increase. Both the Pope and Archbishop of Canterbury appear to share this view, for example. They do so with the objective of reducing inequality in society.

They are not alone. There have been many demands that this be an objective for the After Coronavirus era. For example, the Financial Times has said:

Radical reforms – reversing the prevailing policy direction of the last four decades – will need to be put on the table. …. Policies until recently considered eccentric, such as basic income and wealth taxes, will have to be in the mix.

In this context it is appropriate to test data on the existing tax system that operates in the UK to see whether this demand for increased taxation of wealth is reasonable at this time.

Summary

To achieve this goal a report has been prepared to appraise data on whether or not there is the capacity for those with wealth to pay more tax in the UK, or not. Having appraised data from the Office for National Statistics, HM Treasury and HM Revenue & Customs four main conclusions are reached.

The first is that in the period 2011 — 18 the national income of the UK was £13.1 trillion, and in that same period the increase in net wealth was £5.1 trillion. It is stressed, that this figure is not for total wealth, but the increase in the value of that net wealth in that period.

Second, the overall effective tax rates on income during this period were unlikely to have averaged more than 29.4%, but those on wealth increases did not exceed 3.4%.

Third, if these rates had been equalised it would, at least in principle, have been possible to raise an additional £174 billion in tax revenue per annum from the owners of wealth.

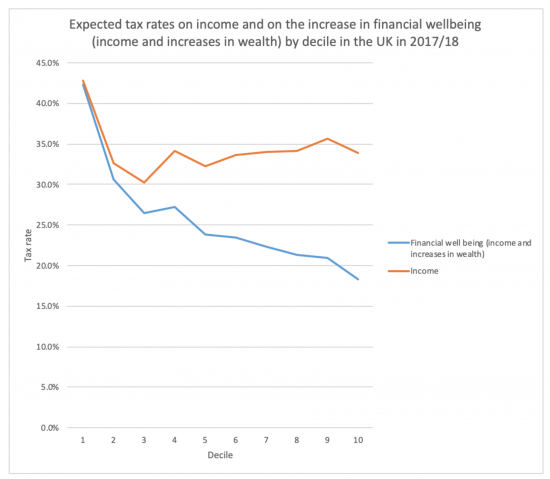

Fourth, because there has been no attempt at equalisation and because the distribution of the ownership of wealth varies substantially across the UK, which variation is reinforced by factors such as age and gender where substantial inequalities exist, the effective tax rate of the 10% of those in the UK who are in the lowest earning group of taxpayers exceeds 42% of their combined income and wealth gains in a year, but the equivalent effective tax rate for those in the highest ten per cent of UK taxpayers ranked by earnings is less than half that at just over 18 per cent. This is summarised in this chart:

It is, as a result, suggested that there is considerable additional capacity for tax to be raised from those who own most of the wealth in the UK, many of whom are in that top ten per cent of income earners.

Whether or not it would be desirable, or even technically feasible, to raise £174 billion of additional tax from additional tax charges on wealth is not the primary issue addressed by the paper. Nor does it concern itself with the issue of whether that sum should be redistributed simply to redress wealth inequality. A value judgement is not being offered on the matter of wealth holding, as such. Instead the issue of concern being addressed is that those most vulnerable to precarity within the UK are also those paying the highest overall effective rates of tax.

Whether that is appropriate is the first question raised as a consequence, with the second being whether, if that is the case, any tax increases that might arise in future should have any impact upon those with lower income or earnings. In the context of the coronavirus crisis and the debates that will, inevitably, occur at some point on whether and if taxes should be raised to contribute towards its cost, these appear to be issues of considerable significance.

This evidence in the paper suggests that those with substantially higher income and wealth should bear the majority or all of that cost if it was thought appropriate that anyone should.

That does, however, then suggest that it might also be important that the disparity in the relative tax payments made by those on high and low earnings in the UK should be addressed whether or not overall net additional tax revenue is required, or not. That is because there is now ample evidence that inequality creates significant social costs within any society, and it is apparent that the UK tax system is contributing to this problem.

A manifesto for change that could result from this understanding might include suggestion that:

- The considerable scope for increasing the effective tax rates on wealth and income derived from it should now be very firmly on the UK policy agenda;

- Any such increase must be targeted at those with the greatest capacity to pay, which would be those in the top deciles of income earners and wealth owners in the UK;

- Tax increases impacting the income of those in other deciles would be very hard to justify if measures to increase tax on wealth and income derived from it did not also happen;

- Inequality in the UK could be considerably reduced by taking the taxation of wealth into greater account. Which taxes should be cut for those on lower income levels to help achieve this goal also needs extensive consideration especially given the stresses that have emerged as a result of the coronavirus crisis.

These issues will be addressed in further posts on how this matter should be tackled in practice.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

The tory govt rejections Universal basic income. Ian Blackford asked the question about it, Starmer seem to apologetic about questioning the govt.

Banks are going to increase 40% interest rates on using overdraft in july according to Peter Bone a tory. Straight after Ian Blackford

https://www.bbc.co.uk/iplayer/episode/m000hm0g/prime-ministers-questions-22042020 See 20:18

How can you raise revenue from tax collected if that tax once collected is destroyed? I have often on here all taxes collect cannot be used by the government to spend as it does the above. So raising tax for revenue is impossible and in any event the government does not need the tax as revenue. It just seems a contrdiction in terms, I get it you want to tax the rich, but pretending the tax is used as form of revenue is just plain false.

You are completely wrong

The government needs revenues to control inflation – and absolutely so under MMT

And I have explained time and again why we need to tax wealth

What I wrote is wholly MMT compliant

How so? You said yourself on your blog, when taxes are paid they are destroyed. So the question needs to be answered how can you tax the rich to pay for inequality? There your words not mine. I am not against taxing the rich, but i am trying to understand the contradiction because there is a big one. Meaning you cannot raise revenue by taxes. Not unless you call it another name. I am not trying to pick a fight i am trying to understand the role of taxes and money creation. I know taxes are needed for other reasons but your not talking about collecting taxes to control inflation – but your want to tax the rich to generate revenue so it can remove the growing inequalities within british society. Controlling inflation and raising revenue for particular purpose are two different things.

Try this

https://www.taxresearch.org.uk/Blog/2020/04/11/tax-abuse-tax-havens-and-modern-monetary-theory/

We need tax revenue! It just does not pay for the spend

But it serves the purpose of cancelling it

And it has massive social and economic functions

I’m not asking to tax the rich to fund spending

I am saying that if (and I stress the if in all I have written) we need more revenue to cancel the exceptional spends then the rich must pay it

Hi Darren, I think I see what you are getting at. You are quite correct tax doesn’t pay for anything , but when the government creates money at will ( which is what it is doing now in plain sight ) in order to give our currency ( the pound ) value in our minds ( we have to believe in the value of our pounds ) and thus prevent it becoming worthless . It follows that those who have the most to lose by the currency becoming worthless should pay the most in tax to prevent this happening. That has always seemed to me to be the primary argument for the richest to pay the most ; they have the most to lose. That of course is not how our tax system is set up largely because our politicians have been seduced by wealth and wish to become part of it . So we have a conflict, but it’s a political conflict not an economic one. And any political conflict is about power.

Thanks

Interesting twist

Tax as a wealth preservation mechanism

I like that because it is true

[…] have already posted the introductory research on tax and wealth for the Tax After Coronavirus (TACs) project on this blog this afternoon. One person I tested that […]

As a semi-retired person living off accumulated savings this one comes pretty close to home. Nevertheless, I support it (noting that this is NOT a revenue raising exercise but a redistribution/inflation control exercise). That I pay a lower tax rate than my son (who works for a living) is absurd.

The details of how a wealth tax is applied is for others to propose (and your modest proposals sound eminently reasonable and practical) but I think from a macro perspective its inflation control aspect is most interesting. Interest rates have completely failed as a tool – they have allowed CPI to stay too low while asset prices shoot up. A wealth tax would put this into reverse and, I think have some real benefits for the economy overall.

In general, we MUST get away from the absurd idea that monetary policy (or even more narrowly – interest rates) are the only tool in the box. We can do better with a more imaginative interplay between interest rates, money creation, credit controls, income/capital/indirect/inheritance tax.

I have 14 follow up blogs sketched right now….

[…] Cross-posted from Tax Research UK […]

[…] and those who elect it in a democracy, might desire. I have already demonstrated that there is scope for a considerable increase in taxes on wealth in the UK without any economic or social injustice arising. in this post I argue that taxing increases in […]

[…] on the blogs that will comprise the recommendations for reforming the taxation of wealth because, as I have shown, if there is a need for more revenue the owners of wealth have most to […]

[…] a paper published this week, I showed that the effective tax rates on those enjoying increases in their financial well being […]