The Tax Justice Network has published its 2021 State of Tax Justice Report. Regular readers of this blog will know that I was underwhelmed by the 2020 version of this report, which I found lacking in a post published in July this year. I do not propose to repeat all the methodological flaws that I identified then. Suffice to say that it appears that very few methodological changes have been made in the meantime.

I do, however, wish to highlight one particular issue that I mentioned in my last review and which is well worth referring to again now. This is that the Tax Justice Network is, by combining some deeply simplistic assumptions with some suspect statistical analysis, coming to some profoundly misleading conclusions. I will simply concentrate on one of the headline figures to highlight this issue.

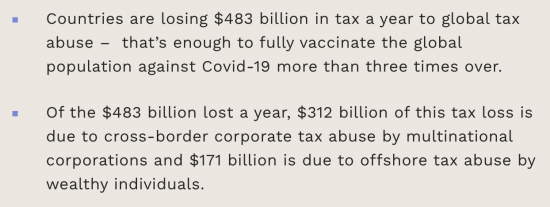

The Tax Justice Network says this on its website page that launches this report:

I will leave aside the figure for the loss of corporation tax. I have already published peer-reviewed research that shows that the basis for this claim is unlikely to be sound. I will instead concentrate upon the claimed loss of $171 billion to tax abuse by high net worth individuals.

The Tax Justice Network says in chapter 3 of their report that the methodology to estimate this sum is as follows:

In the first step, we identify what we call “abnormal deposits”. We start by identifying jurisdictions that (a) attract amounts of bank deposits that are disproportionally large in comparison to the size of their economy and (b) offer strong bank secrecy laws.

Using regression analysis, we then estimate the expected amount of inward bank deposits in these jurisdictions based on the strong relationship between GDP and bank deposits in countries that do not provide opportunities for secrecy arbitrage (ie those countries with lower secrecy scores for banking secrecy and a relatively low ratio of bank deposits to GDP). “Abnormal deposits” are then quantified as the difference between the observed deposits and the expected proportional deposits in each jurisdiction. We argue that these abnormal deposits are located in these jurisdictions precisely due to the fact that these jurisdictions provide financial secrecy. ... We find that 51 per cent of global bank deposits can be considered abnormal as per our definition, meaning that they are located in secrecy jurisdictions in quantities that are higher than would be expected based on the size of these jurisdictions' economies.

In the second step of our approach, we attribute these abnormal deposits to their origin countries. To do so, we broadly follow Alstadsaeter, Johannesen, and Zucman's approach and use the Bank for International Settlements' (BIS) Locational Banking Statistics.

In the third step, we combine existing estimates of total global offshore wealth with our estimated country shares, to derive the value of offshore wealth originating from each individual country. In particular, we use the most recent estimate of global offshore financial wealth of 11.4 per cent of global GDP, or US$9.9 trillion in 2019. It is important to note that this estimate only includes financial assets and not non-financial wealth.

In the fourth and final step, we derive the tax revenue losses resulting from wealth being stored in secrecy jurisdictions. Following Zucman's approach in his 2015 study, we assume a 5 per cent return on offshore investment (which includes a combination of securities, bonds, bank deposits and other financial assets). We then multiply these returns by the personal income tax rates that would have been applied in the assets' origin countries, had these assets not been moved to secrecy jurisdictions.

I have edited the above down to be of manageable length, but all the words are all the Tax Justice Network's own. TJN say as a result that there is a worldwide loss of$171 billion a year.

Now let me suggest why that figure is bound to be wrong as a result of the flawed logic that the Tax Justice Network uses.

The first flaw is to assume that all offshore deposits belong to individuals. They clearly do not.

The second is to assume that none of the sums in tax havens are declared to the tax authorities that need to know about them. That is obviously absurd, and has never been true.

The third is to assume that a 5% rate of return can be earned offshore when it is widely known that most illicit funds held in those places are held in cash, and they will not be paying anything like that sum at present.

Each of these needs to be corrected for. I am helped in doing so by having attended an open seminar organised by the World Bank yesterday at which Niels Johannsen of the University of Copenhagen, who has done a lot of work in this area happened to speak about new research he is doing. He is using the actual data supplied under automatic information exchange arrangements from other countries to Denmark under Organisation for Economic Cooperation and Development arrangements. I am not going to steal the thunder of his research but will focus on some key elements he raised, and then note that all the extrapolations are mine.

First, he noted that the most recent round of automatic information exchange reported a worldwide total of £10 trillion of funds held in one country by a person resident in another. This is remarkably close to the figure of $9.9 trillion used by the Tax Justice Network.

Of this sum, it transpired that 80% was corporate money, and the vast majority could be matched to large quoted companies. In other words, these are corporate treasury accounts.

Of the remaining 20% of balances held by individuals about 80% were found to be likely to be tax compliant.

That leaves 20% of 20%, or 4%, that may not be personally compliant, and as TJN notes, only 51% of balances are in secrecy jurisdictions.

So, to extrapolate:

At most $5.1 trillion is in secrecy jurisdictions ($10 trillion (as per the OECD which is almost identical to $9.9 trillion as per TJN) x 51% (as per TJN))

Of this $5.1 trillion 80% is corporate funds. That leaves $1.02 (call it $1 trillion) of personal funds that may be in tax havens.

Of this $1 trillion 80% of owners are compliant with their tax disclosure, which is hardly surprising when they now know about automatic information exchange arrangements that have now been in place since 2017. That leaves £200 billion of non-compliant funds, at most, worldwide.

If we assume that 5% could have been earned on these funds - which I think unlikely - the income return would have been $10 billion per annum on that sum. I will accept this figure for now, but it could be much smaller.

Nothing that I can see in the Tax Justice Network report tells me what the average personal tax rate that they used might be. Let's assume 40% in that case. That results in a loss from personal tax abuse of $4 billion a year as a consequence.

Note that Tax Justice Network says the loss is $171 billion. Assuming a 5% rate of return and a similar 40% tax rate would require (by working from the loss backwards) that more than $8.55 trillion be held illicitly offshore to generate this sum ($8.55 trillion at 5% = $427 billion, which at 40% loss of tax = $171 billion). Even this simple 'sanity check' of the Tax Justice Network claim shows how implausible it is when they start by saying there is only $9.9 trillion of offshore wealth of which 49% is not in questionable locations. However looked at, the Tax Justice Network figures cannot stack.

Let me draw some conclusions in that case. Firstly, it is very obvious that no one at the Tax Justice Network sanity checked this claim before publication. If they had, then using the simple extrapolation that I have undertaken in the previous paragraph it would have been obvious that the claim made was wrong. The evidence is abundantly clear in that case that the Tax Justice Network is not checking the quality of its own work, which is something that John Christensen had to painfully point out when he resigned from the organisation in August this year.

Second, I am the first to say that neither of these figures are right. Both are based upon estimates, but given what we now know about offshore holdings, and given what we also know about behavioural changes in response to tax reforms I believe that the data supplied by Niels Johannsen is both likely to be right, and likely to be replicated in a great many other countries. Therefore, of the two estimates I think that mine is vastly more likely to be correct in its indication of magnitude than that supplied by the Tax Justice Network.

Third, as someone who worked very hard to secure automatic information exchange, having written about it since 2005, I am delighted to see that it is working, and that much higher tax compliance rates then we might ever have thought likely at the time that the Tax Justice Network was created are now being secured. I am pleased to note this success and even to claim a very small part of the credit for it. What, I admit, deeply annoys me is that this achievement is being entirely overlooked by the current researchers at the Tax Justice Network, who I think are irresponsible for doing so.

Fourth, I seriously suggest that no one should put any weight upon the findings now published in this report by the Tax Justice Network. I happen to think that the corporate findings are also likely to be overstated, although not by such a dramatic degree as is the case for the personal abuse findings, but such is the magnitude of error that I have just noted that no one should think that this report is any indication of the scale of the offshore tax problem that now exists.

Fifth, because that offshore tax problem is very likely to be substantially less than the Tax Justice Network now claims precisely because of the success that John Christensen, I and others had when creating change in the international tax system by working through the Organisation for Economic Cooperation and Development other than by opposing it, which is the current modus operandi of the present TJN leadership, I very strongly suggest that it is time to move on from this issue, particularly with regard to personal tax abuse and to focus upon other matters of concern. Of these, by far the most important with regard to offshore is in providing sufficient resources to domestic tax authorities around the world so that they can use the information supplied by the OECD automatic information exchange process to identify the relatively small number of high net worth individuals who are very likely to undertake the vast majority of offshore tax abuse in any tax jurisdiction.

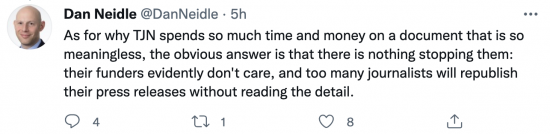

Sixth, if tax justice campaigns are to remain relevant then they have a duty to present data prudently, professionally and even cautiously to ensure that the claims that they make are not overstated. I cannot identify any of those qualities in the Tax Justice Network's State of Tax Justice report, which I think to be careless in the assumptions that it makes and in the claims that it publishes. I noted London tax lawyer Dan Neidle making a comment on this report on Twitter as follows:

Dan Neidle and I have a history of disagreeing with each other. On this occasion, I think that he is right. It disappoints me to say so, and that I have to do so is some indication of the depths to which the Tax Justice Network has fallen.

The State of Tax Justice report is not credible and it most certainly does not represent the state of tax justice. I sincerely hope the sponsors of this report take note.

Footnote: Without having heard Niels Johannsens's comment I would have made slightly different assumptions. I would have presumed maybe 60% of deposits were corporate. I would have guessed the 80% compliance rate though, simply using the 80:20 rule. This would have resulted in a slightly higher loss estimate, of $8bn. The difference would still have been of the same overall order as that noted above.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

It’s interesting to go back and see this claim from 2013

https://www.taxresearch.org.uk/Blog/2013/02/06/new-study-offshore-tax-dodging-blows-40-billion-hole-in-u-s-state-budgets/

when the figure was $40bn, and just for the state governments of the USA.

TJN have long term form for reproducing astonishingly large numbers.

And matters have changed since.

FATCA and automatic information exchange plus country-by-country reporting have all changed matters

I had a role in some of that

I have noticed the win

Tax Justice Network has not

And you miss the point

FATCA – 2010

Automatic Information Exchange – 2014

I can’t see a date for country by country reporting that would change matters since 2013 though.

2-15 mandated

2017 data reported

[…] Substantial revenue is being lost – and certainly much more than offshore abuse is costing the UK now. […]

My thought is that if we didnt have tax havens what might that mean for tax rates if there isnt anywhere the wealthy could hide their money?

Tax havens no longer provide a means for the wealthy to hide their money

That’s why the sums involved are tumbling

Tax havens are being beaten

[…] noted the concerns I have with the credibility of the calculations within the Tax Justice Network's State of Tax Justice report for 2021 […]

Hi Richard,

I saw the SOTJ 2021 report and I was a bit confused when they said that they relied on CbCR data to extrapolate the corporate tax profits being shifted to tax havens. If these numbers are reported in CbCR and taxed accordingly via corporate/ withholding / CFC regimes etc, why are they being regarded as profits that were shifted and therefore not taxed or taxed at the wrong jurisdiction? Am I missing something here? Because the number of £312 bn is pretty mindblowing after taking into consideration multiple regimes such as BEPS Action Plan/ domestic CFC/ DOTAS/ DPT/ DAC6 that are engineered to defeat corporate profits shifting. Just want to get your insights on this.

Thanks,

Zhan

I am as confused as you as to what they are doing

[…] make no apology for sharing one of those videos again today, because as my criticism of new work from the Tax Justice Network this week shows, it is apparent that they and many tax justice campaigners do not seem to appreciate just how […]