HMRC published its tax gap data for 2018/19 yesterday. I have long criticised this annual debacle which has always published a number between £29bn and £38bn or so over the last decade. It's so predictable that I now wonder why they do it, as this data shows:

And the methodology remains as flawed as ever. In essence, tax evaders pretty much fall outside the scope of much of the tax gap because HMRC refuse to believe they can exist, even when the evidence is so obviously there to see - not least in the 3 million companies that exist in the UK and do not declare any tax liabilities and who are not chased by HMRC to do so and who instead turn a willing blind eye. In addition, the definition of tax avoidance is so narrow that much of what everyone agrees to be tax avoidance - like the widely condemned abuse by multinational companies - does not get into the tax gap definition that HMRC use, which is absurd.

Rather than reiterate all my arguments try this from last year, except please note it now looks like they have also changed the way of doing VAT and I suspect that I now have reservations about that too.

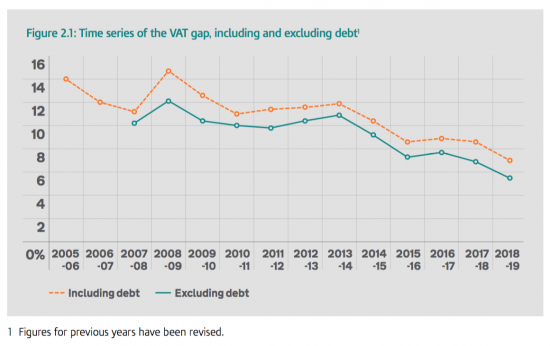

But there is a dimension to this that makes the report this year even more absurd than usual. To keep the number in the required and seemingly pre-determined range (four years in a row with an almost identical number is utterly implausible) that suits HMRC's management HMRC has to make the most staggering claims about their increases in productivity to counter the impact of inflation and growth. In other words, the tax gap as a proportion of tax take has to keep falling to hit the required number range, as is very apparent from the above chart, and also this one on the VAT gap:

We are apparently almost twice as honest now as we were only a decade ago.

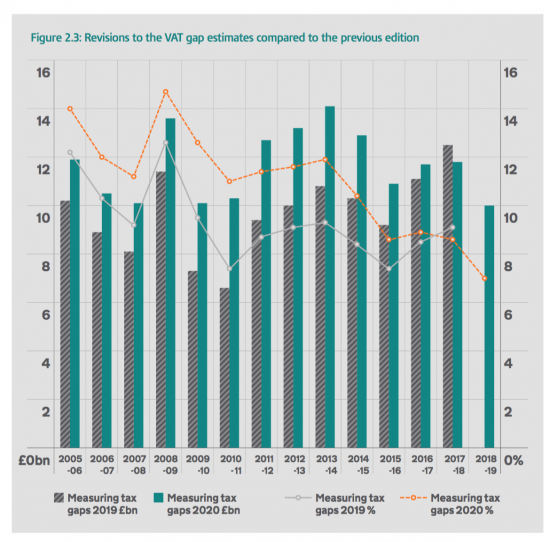

Or rather, HMRC assume we are. This chart shows the revisions to the data as a result of their own changes in methodology:

Last year the VAT gap was deteriorating as the grey line shows. The trend was markedly upwards.

Now, apparently, HMRC realise we were much worse in the past, but suddenly are getting so much better after all. That's what the orange line shows. And apparently, instead of getting worse, were all reformed and complaint people.

There are, then, some simple questions to ask of this data. The most obvious by far is how likely is it that attitudes to tax abuse changed so radically in such a short period of time without there being a great many obvious reasons for them to do so?

On international issues I think there is a chance that this happened. I have no doubt that multinational companies have changed their behaviour since Margaret Hodge savaged Google, Amazon and Starbucks in 2012. Knowing that country-by-country reporting was coming will also have hastened change, although abuse remains, as I note elsewhere this morning.

And for individuals using tax havens I am sure that automatic information exchange of data will have had a significant impact on compliance.

That's two gains for tax campaigners then and not much for HMRC. There is also a third. We know that the crackdown on VAT abuse through Amazon and eBay had begun by 2018/19. But I stress, it had only begun. And then only due to the relentless pressure from Richard Allen on this issue. Another win for campaigners and not for HMRC then.

But only the Amazon / eBay case impacted VAT: offshore did not. And yet HMRC claim that compliance rates on VAT have improved staggeringly over a very short period of time, when during that period they were closing as many tax offices as possible, pushing their staff's morale through the floor, and were losing their most experience people who did not want to move to the new regional hubs that HMRC has insisted on creating. Inspection of trader's records had almost entirely ceased as well. All my feedback from HMRC is that compliance got worse in this period.

The only move HMRC can claim might have helped is Making Tax Digital and very small amounts of extra data exchange from credit card suppliers and trading platforms. I don't dismiss the impact of the latter, but I very much doubt that these were widely known or understood amongst the tax evading community. If they were then that community would have made even greater use of anonymous ‘throwaway' companies that are so easy to create and get rid of in the UK - and which represent the biggest threat to the tax take in this country, and which HMRC persistently ignore.

So, we're down to Making Tax Digital, which HMRC has to say is a success. No one else does. I get no feedback through accounting web sites, for example, that anyone thinks that this has helped productivity, error rates, compliance of anything else. The feedback there is that it has been embraced as a new way of working by those already compliant, but it has not changed compliance rates. Indeed, in many ways it will have helped force the non-compliant out of the system altogether.

But I very strongly suspect that this tax gap data reflects assumptions that Making Tax Digital works and has produced massive savings.

I stress when saying so that I accept that the tax gap is improving. I think it is. But by the amount HMRC claim? I have to say that this change of behaviour is implausible.From 2007 to 2013 the compliance rate hardly changed. But now it's tumbling. I simply cannot believe that. It strikes me that this makes the tax gap data as dodgy as the tax return of the proverbial ‘man down the pub' who has a new BMW each year and says he never pays a penny in tax.

HMRC has a duty to be credible. It has a duty to publish information that can be believed. And I am a long way from believing what they are producing. Put bluntly, the UK is not the most tax compliant country on earth, which it would have to be if these numbers were true. And it does HMRC no good to claim that we are.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“much of what everyone agrees to be tax avoidance”

Isn’t it for the law to decide what is and isn’t allowable with regards to tax planning?

You seem to be saying that the tax gap should include tax which isn’t due under the law but would be if the law were changed and that HMRC should be criticised for basing their tax gap figures on tax due under the law. That’s absurd.

This is so tedious

This issue was settled a long time ago by all except those who want to abuse the law

I guess you’re one of them

How bizarre.

I say that the law decides what is and isn’t allowed.

You say it should be “what everyone agrees”.

You say I am abusing the law.

Your line is a call for mob rule.

The issue on what is and is not allowed has not been settled at all. The law changes. Constantly. But any legal code worthy of the name restricts the enforcers of the law as well as its subjects.

You may find it tedious that the law has to be followed, you may call for mob rule if you wish. But don’t complain if one day the mob turns on you.

If you don’t understand Rac avoidance I suggest very strongly that you go nowhere near it

“not least in the 3 million companies that exist in the UK and do not declare any tax liabilities and who are not chased by HMRC ”

That is obviously not correct.

There are currently 3.1 million companies registered at Companies House, 300,000 of which are listed as dormant.

Are you claiming that not one single active company in the UK is declaring tax liabilities?

You speak of credibility and then use a number which is obviously nonsense.

Can you cite a source for your claim?

There were 4.8 million companies the last time I looked

And registering as dormant indicates nothing at all

I think the problem is all yours

Search ‘In the shade tax’ and you will find my last research

Like many government departments, HMRC has lost any sense of ‘savvy’ and ‘nous’ – and is not going to have any meaningful effect on the tax dodgers.

On thought for the day this morning, the bishop of Leeds recounted his attempts to draw a chair – he wasn’t very good at it. He was then told to draw the space around the chair – I think artists call it the negative space. Having tried this, he found that although the drawing still wasn’t that good, the chair looked more realistic.

There is a general absence of curiousity in HMRC – no one seems to ask ‘what are we missing’, the response would of course be ‘it’s behind you!’ Or more accurately ‘hidden in full sight’.

On companies coming and going, there would seem to be a data matching exercise for company bank accounts (and the lack thereof), compared with those companies showing as active/inactive at HMRC.

It is probably beyond them – just as it is to get a self assessment tax return calculation to work just once in a while.

I suggested legislation to deliver this marching in 2014

It never made it to the statute book

Jacob Rees Mogg talked it out of the House

[…] thought about that when reflecting on HMRC’s tax gap data that I commented upon yesterday. In it HMRC are literally rewriting their past to make their present claims look […]

When even the HRMC are “fiddling” reality then from a democracy viewpoint voters are forced to live in a fantasy “live in hope” electoral world and not an analytical one. Such a world can only ultimately end in tears because it’s masking duplicitous government for the few!

One of the principal reasons that these figures look the way they do is that they are required to justify the continual downsizing of HMRC. The slogan used is “more with less.” There has been something of a pause on this recently, as there is obviously some realisation that excise and customs arrangements simply won’t function with the level of resource [meaning, basically, bodies] presently allocated to them, post-Brexit.

Precisely

It is typical management distortion of data to suit its purposes

Galbraith wrote about it in the 60s