The FT reported yesterday that:

The leaders of the Big Four accounting firms have come together in an unusual joint initiative to unveil a reporting framework for environmental, social and governance standards.

The move – spearheaded by the International Business Council, run by Brian Moynihan, chief executive of Bank of America – aims to encourage the 130-odd large global companies in the IBC to adopt the standards for their 2021 accounts.

The FT did not, as usual, provide a link to the document about which they were reporting, so I hunted it out. This is it:

So what we have is the Big 4 firms of accountants, all of whom have been persistently found to have failed in their most basic of professional duties, co-operating with the high priests of the capitalist system that has destroyed the world's environment and driven wealth ever more upward to a few in society, telling us all what we need to know as stakeholders of the companies that they operate. You really could not have a more bizarre scenario for suggesting stakeholder accounting standards.

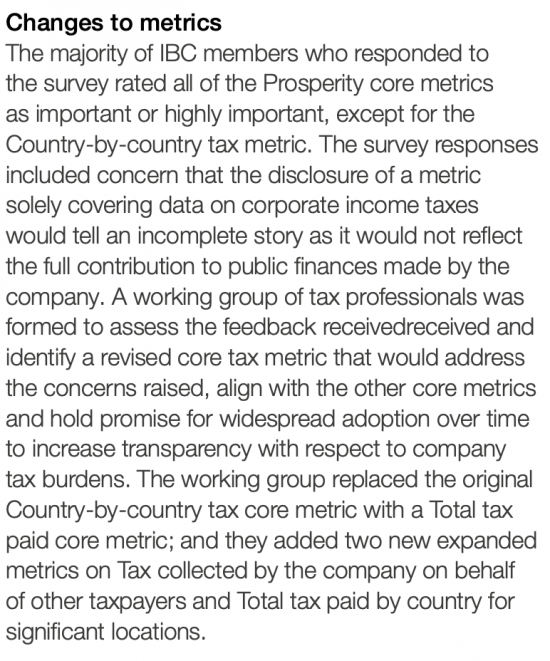

I do not pretend to have read every word of the document as yet (although I suspect that I will). But I do already know they ignored stakeholders in its preparation. I can safely say this because there was apparently an earlier draft that suggested that multinational corporations be required to report on a country-by-country reporting basis so that their tax affairs could be properly understood. This really is a very basic stakeholder demand right across the board now. But as the report notes:

So it wasn't stakeholders who decided that country-by-country reporting was not required: it was the reporting entities that did so.

And it was not stakeholders who made the detailed decision, it was tax professionals, presumably from the Big 4, who have every reason for wishing to hide their tax avoidance activities using tax havens from view: after all, these places only exist because the Big 4 support their existence.

And by doing this the whole process has been discredited, in its entirety, because it cannot be trusted.

Which is a shame because there are some useful things in this report, but not on tax, average wage reporting. or the environment.

Frankly, what this really suggests is that we have a very long way to go, and it really is time these companies talked to their stakeholders and dropped their arrogant view that they know what stakleholders want.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

It looks like the big 4 accountancy firms and the multinationals are making token gestures towards transparency to avoid further scrutiny and exposure during the current multiple crises.

This just sounds like sour grapes from you. Only Richard Murphy has the right motivations and method (dreamt up on his own, with no research, development or testing) for ESG reporting and transparency.

Or it could be that the GRI are about 20 years ahead of you and your woeful Sustainable accounting on ESG, and the OECD, EU and others have all noted that country by Country reporting is essentially useless as things stand, because it assumes production, labour, turnover and profit are all equally distributed. Which of course in the real world, they aren’t.

Which makes it no surprise that companies, accountants, auditors and most importantly, the regulators, all think CbC is not very important.

You are aware GRI have adopted CBCT?

Everyone wants it but the producers

Methinks you are talking BS

GRI adopted CbC to fall into line with OECD BEPS.

But both of them (GRI and BEPS) state that CbC data can ONLY be used as a “high level risk assessment” and CANNOT be used for detailed tax analysis, because I quote, “CbCr may lead to arbitrary taxation. A system that relies solely on CbCr is unsound”.

Neither the GRI or OECD put much any in CbC as it stands, with both moving swiftly away from it to a more comprehensive view of what taxes are paid.

In short, it is pretty useless. Must be hard to see people take your life’s work and basically throw it in the bin.

The way you impugne the motives of anyone but yourself and your fellow travelers tells us all we need to know about you really, doesn’t it?

CBCR has never been a tax assessment tool

It is accounting data

But what you say about GRI is wrong: I was heavily involved in the process of developing that standard and GRI most certainly do not think it useless

And the EU is moving towards it

And you are, I suspect a paid troll

I’ll happily impugn your motives

Richard,

I am confused about country by country reporting and how much meaning you get from the data. Maybe it would help if we could use an example, so you could clarify for us?

Below is the real data from a real company’s country by country accounts.

Country Employees Total Revenue (k) Profit Before Tax (k) Tax on Profits (k) Effective Tax Rate

UK 3191 283,086 8,790 4,545 51.7%

Japan 1502 68,074 -8,192 34 -0.4%

Australia 493 37,136 2,054 -1,439 -70.1%

France 371 25,813 957 173 18.1%

Germany 448 22,798 -1,706 181 -10.6%

Middle East 192 11,492 927 28 3.1%

Holland 87 7,229 2,199 -275 -12.5%

Spain 153 7,210 -808 0 0

Austria 59 4,340 411 15 3.6%

Ireland 34 3,004 595 -117 -19.7%

New Zealand 88 4,918 1,068 -469 -72.2%

Total 7,498 394,947 15,031 2,800 18.6%

I’ve left out many of the smaller countries for brevity, so the above won’t sum to the total – but the total is also from the accounts.

From this data, can you tell if they are paying the right amount of tax? And the right amount of tax in each country?

Read this

http://www.taxresearch.org.uk/Blog/2014/06/30/barclays-the-bank-that-just-loves-luxembourg-and-jersey/

No one says CBCR is a panacea

No accounting data is

But it is a risk warning tool

What does it say:

A) That companies are in risky locations

B) There is a high volume of intra-group transactions

C) These appear to reallocate profit

D) There may be less tax paid as a result

E) This income stream may not be sustainable as a result

And I isn’t that exactly what shareholders want to know?

That is a lot of maybes. That doesn’t make for any real information or evidence though. Just guesswork and insinuation. That might be fine for tax campaigners, giving them ammunition for their stories and newspaper headlines, but it isn’t good enough for tax authorities and the law.

I read the article you link to above , and that is more of the same. Maybes and guesses – but then you make statements about Barclay’s behavior as if it were fact.

Which is even more surprising as their overall tax rate is 28.9%, which is higher than the UK corporation tax rate. So if they were avoiding tax, it doesn’t seem like they were doing a very good job of it.

Anyway. Going back to the example I gave you above, can you tell us anything about that particular company and it’s tax? Have they paid the right amount in the right places? I am interested to know, as you are the creator of this and I want to truly understand what it is supposed to do.

CBCR is a risk assessment system

All accounts are

If you don’t realise that then you don’t get anything to do with accounting

And I have a busy life and will not be doing your exercise when I have better things to do

Why not publish the answers instead of playing games?

I’m actually quite taken aback. if you are an accountant and expert, as you claim, then you would know what you say is simply not factually correct.

Accounts are not simply “risk assessments”. Financial and Tax accounts, as well as audits are legal documents and have to be carefully prepared with a high level of detail. Accounting is heavily regulated with numerous international bodies and professional qualifications necessary before a person may be an accountant.

Country by country reporting has almost no detail, as far as I can tell. Your method (which I looked at in your other post) seems to simply apportion profits on the basis of an average between the number of employees and the total profit.

Which means that should a company make an overall profit in a period, by your logic it should have made a profit in every country it operates in, and should it have made a loss, a loss in every country.

Which is quite simply nonsense. It is ludicrous to suggest that such a basic methodology could encapsulate the true and fair amount of tax a company should or should not be paying.

This of course is my take on it, which is why I asked you to explain how you could use the data to gauge if a company is paying the right amount of tax – even as a “risk assessment”. From one of the other posters above, it seems that both the OECD and GRI share this concern.

Looking at that data again, you simply can’t say anything about that company’s tax position. In some countries, where it made a profit it paid a much higher tax amount than expected. In some, it actually paid no tax or even a negative amount of tax. Likewise, in some areas where it made a loss it paid tax. So as far as I can tell this data on it’s own is totally useless.

Which makes me wonder why you think that any real information can be gleaned from it, and why you take such data and treat it as if it were accurate and factual – for example when you claimed that Barclays were avoiding tax.

If Barclays were avoiding tax with an overall rate of 28.9%, then surely this company is also avoiding tax, given their overall tax rate is much lower at 18.6%? Surely you can answer me that at least?

With respect, you clearly think accounting is a science that can provide an answer

And that’s absolutely not true. The very smallest set of accounts apart all accounts involve the use of considerable judgement, and substantial estimation, and many apportionments

There are no rules that say precisely how this is to be done, just guidance

That guidance is usually rather less direct than CBCR is

I suggest you come back when you have learned what accoubn9ing is

I have been a chartered accountant for 38 years now, and I suggest to you that I do know what I am talking about

Accounting is not an exact science – but none are. But what you say is utterly, utterly wrong.

There are various accounting principles (IFRS, GAAP, IAS, etc) which give detailed rules regarding the treatment of almost everything in a company’s accounts. The idea being to minimise judgement and estimation. These rules are legally enforceable in many cases, nit just guidlnes as you claim.

Country by country reporting however is literally nothing more than a simplistic formula, which obviously going to come out with answers that are totally meaningless – as the examples here have shown. You are simply unable to tell us if the example data I gave you means the company is paying too little or too much tax, and in the right places or not. You just don’t have the information necessary to make any judgement.

That seems not to bother you in the slightest though. I assume Country by country reporting was really designed to give people like yourself another stick to beat the corporate world with – truth be damned – beacuse it doesn’t actually tell us anything about tax.

As for you being a chartered accountant? You haven’t practiced for many of them, by the look of it, and then mostly at very small firms. Maybe you are just bitter that your career didn’t go as you felt it ought to. Either way, an “accountant” who doesn’t understand that thinks that accounts are just “risk assessments” and are estimated based on judgement with the use of guidelines rather than regulations is not an accountant I would use. Or, given your accounting career, anyone else it would seem. Worse still, you think simple maths can replace proper analysis and pass that off as a new reporting standard.

I think it is obvious that your inability to answer my question about the example I gave, even in the most basic terms, suggests that country by country reporting is useless and you don’t really know what you are talking about. But that is just using my “judgement”.

For the record, I am an FCA

I have had a practising certificate since 1984

I am an honorary fellow of another institute for outstanding contribution to the profession

And the ICAEW has also given me more than the odd nod of recognition

I am also a visiting Professor of Accounting

And I can say with absolute conscience that you really do not understand accounting

And that you are no longer welcome here