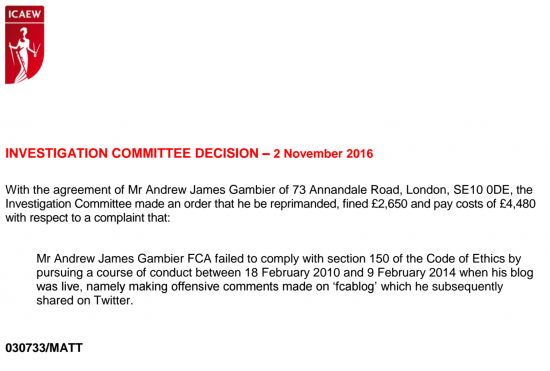

On 6 December this year the Investigations Committee of the Institute of Chartered Accountants in England and Wales published the following statement:

Why share this? There are a number of good reasons.

First, the consent order does not reveal what was really going on here, or the appropriate dates. The FCAblog was run by Andrew Gambier until 3 September 2015. Its demise was noted in a blog I posted on that day. The ICAEW did not get their facts right.

Second, the blog was not just offensive, it was crude and deeply personal. I was one of its principle targets. This was apparent even in comments on the farewell posting. Tim Bush at Pensions and Investment Research Consultants (PIRC) was another. I won't reproduce the types of language used: I would not tolerate it near this blog.

Third, more importantly, this blog appeared to have a particular gripe against those not following the line of accounting orthodoxy, which both Tim and I have questioned. It did so from an indisputably knowledgeable viewpoint. The way it did it was profoundly inappropriate.

Fourth, what the ICAEW announcement did not make clear was that Andrew Gambier was throughout the period during which the offences took place the ICAEW Technical Strategy Manager; effectively its number two in its technical department. In fact, because many if the blog's were posted during the working say I find it impossible to believe that the ICAEW paid for many of them.

Fifth, I find it nigh on impossible to believe that some in the ICAEW could have been unaware of this, although I know Michael Izza, its chief executive, did not. Presuming he did I informed him of my awareness of Gambier's authorship of the FCAblog in mid September 2015 and his reaction was clearly of genuine shock. Gambier's employment ended a few days later: I have no idea of the circumstances. I did not ask. I did not want to know. I made no complaint. I was unaware that a professional disciplinary action was taking place until told in the last few days. I have no issue with Andrew Gambier personally and professionally he has been sanctioned.

But I do have a remaining issue of concern. Gambier went from the ICAEW in September 2015 and by November 2015 was appointed Head of Audit and Assurance at another UK accounting institute, the Association of Chartered Certified Accountants. This is a fully authorised UK accounting body, self regulating its members in this area of work.

I said nothing at the time of Gambier's appointment as he had not been found guilty of professional misconduct at the time, but I will now. I think it impossible for a UK professional body of accountants to employ a person as Head of Audit and Assurance who has been disciplined by another such body for serious professional misconduct of the type I have noted (which he admitted in this closing comment on his blog was only possible from behind a veil of secrecy that he had carefully created to prevent his employers knowing if his actions over a number of years) and still retain a shred of credibility on this issue.

For the avoidance of doubt let me make it clear why I say that. To be credible a professional body must be fair, open, reasonable, transparent and accountable. By implication it must avoid prejudice, bias, offence and opacity. And since a professional body can only work through its employees they must be seen to embrace and uphold these standards. That cannot now be said of Andrew Gambier, who wrote deeply prejudicial and offensive material, sufficient to justify professional sanction, from behind a veil of secrecy designed to veil his identity from his own professional institute who also happened to be his employer.

I have no desire to see anyone out of work. But professional standards exist for a reason and all professional institutes have a duty to uphold them. The ACCA is known to be deeply antagonistic to any issue relating to tax justice, improved accounting disclosure and country-by-county reporting. Gambier might well fit into its ethos, but his conduct cannot. I will watch what the ACCA does now with interest.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I’ve just read his final blog and the comments that follow. Several mention you in person and one wishes you dead. How anyone can think it acceptable to allow such a comment – and then publish it – is beyond me.

Nice, wasn’t it?

This is also illuminating for the insight it shows from a certain Oxford tax academic https://twitter.com/Callies895/status/639524766781718528/photo/1

I noticed her hashtag in one of the comments. Not surprised.

Having read that more than ever before I believe that a really relevant job-creation scheme for the on-line world of today would be employing people to look at stuff like this and then ban the offender and in some extreme cases send the police around to tell people to behave themselves.

This Gambier fellow and his followers are entitled to their opinion (which to me of course just sounds hypocritical and self justifying – they might as well be on a different planet) but there is no excuse to troll or flame people in response to different opinions.

It seems to me though that as far as professional standards are concerned, there is only one standard in certain spheres to adhere to and this is simply the one of making money and nothing else.

Don’t like the sound of that. Sounds like something China/May would be keen on.

As the father of 13 year old who has been bullied over social media I totally disagree with you.

Sounds like what we’ve been through the last year at the hands of Labour’s Compliance Unit:o(

Good news. I remember reading some of the commentary at the time and it was nasty stuff. Saying you couldn’t do basic accountancy like calculating dividends, calling you a union shill and suffering from some Dunning-Kruger disease.

More power to you Richard.

I agree. You would think that somebody operating under the obligations of membership of a professional body would able to comply with just the basic requirements for treating others with courtesy and consideration, being honest and truthful, and avoiding making disparaging references to the work of others. Only a blithering idiot would struggle with what is essentially just being a decent human being.

You are right, and the fact that these people can’t see it in themselves means they are beyond help and should be ignored, or at least ridiculed.

I’m not sure the idiot in question would realise that he was being ridiculed.

The way to raise professional standards is to increase competition. Set corporation and inheritance tax at the compliance optimising level and there will be many accountants chasing fewer clients.

Tell me what that rate is

And how you find it?

To compensate the pension tax free deferral rate should be 20% across all incomes. Higher rate payers already pay 2% rather than 12% no, so permitting 40% deferral of income tax means we have regressive taxation above 43k. To answer your question though zero is the compliance optimising rate of ct a iht and would cause panic in the accounting industry as they would have no tricks to sell their customers.

Absolute nonsense that zero is the right rate fir those taxes. How do you get to that! And don’t say double taxation because there isn’t any

CT is paid for by workers and owners in a corporation ( and to a tiny extent by customers ). We’ve already got income taxation ( and consumption taxation ) to collect income paid out in dividends and wages. Applying a corporation tax is not so much double taxation but a duplication of taxation.

The world gets richer by doing things more productively at the governmental level too. Adding extra burdens onto government revenues agencies and perverse incentives to accountants to thwart them reduces the productivity of society in general.

Inheritance tax is of course double taxation, as you’ve previously acknowledged.

Ah, the usual old arguments

So tell me, if labour pays why haven’t wage rates risen a lot as UK CT rates have fallen so heavily? They have not, of course

And if income tax works how do you collect fax from the invetsment diverted into an offshore trust and accumulated there when the profit clearly arises in the UK?

Your evidenced answers are requested – and don’t quote Devereux on wages – he only studied CT increases

And for the record, I have never agreed IHT is double tax: it is an essntial single tax when one otherwise applies on most gains

Edward Kleinbard cites US Congressional bodies and committees which work on the presumption that capital bears between 75% and 95% of the economic burden of taxation. These are bodies which make policy on the strength of their assumptions, not academics having a bunfight in a conference.

The problem is that the optimum tax rate always seems to be ‘less’. for years, 20% corporation tax was the Holy Grail, but as soon as we got there, there was pressure to lower it still. Despite a 12.5% rate in Ireland, Apple reduced the rate to an effective rate of around 22% through its tax avoidance activities. The optimum rate for compliance therefore appears to be zero but, to paraphrase The Jungle Book ‘I reached the bottom and I had to stop, and that’s what’s bothering me!’

Apple’s effective rate should be around 2%, not 22%.

Sorry Richard but something doesn’t ring true here. You said in the comments of your original blog post that you had never contacted his employers? One of your comments stated “I have over the years contacted his employer many times, and met the author of the fcablog in his capacity of working for them, but I have never mentioned his authorship of fcablog to them, ever, for the record. If someone has spoken to his employer it was not me, nor, I am assured, the person who advised me of his identity.”

However, in this post above you say “Fifth, I find it nigh on impossible to believe that some in the ICAEW could have been unaware of this, although I know Michael Izza, its chief executive, did not. Presuming he did I informed him of my awareness of Gambier’s authorship of the FCAblog in mid September 2015 and his reaction was clearly of genuine shock.”

So, did you or did you not inform his employer that he was the author of the blog?

When I wrote the blog post on 3/9 I had not revealed his identity to his employer. Bug he implied someone had. I was making clear that was not me.

About 10 days later, believing his employer knew, I raised it in conversation to discover his chief executive, at least, did not, much to my surprise.

I was well aware they had been trying to find out for a long time

My statements are wholly consistent

Thanks for the clarification.

Richard – some chap in Palestine about 2000 years ago advised us to love our enemies and to turn the other cheek.

I did

I did not complain about his conduct

I am not now

I am saying that the ACCA have got this wrong

That is something very different

I’ve worked in banks, and I’ve worked on building sites: some would tolerate the language, but none would tolerate the deliberate intent to attack and to offend.

Consequences follow from such actions, and from such speech.

It is, of course, free speech. He has a right to say it, in a free society: but not to compel others to hear it. Nor to support it, subsidise it, or accept being associated with it: free speech is not a complete freedom from consequences.

There is a bright side to that, if you look from a particular direction: I do not doubt that there’s a place for him today where both his arguments and his urge to be offensive are appreciated. He might even consider himself respectable, in such company.