Some have suggested I should not have commented on Ken Livingstone's tax affairs over the last couple of weeks. I reflected carefully before doing so, and did so only on the basis that all who took my comments made clear I was actually in favour of systemic reform of small company taxation. In fairness, both the Observer and Telegraph did that. But the issue carries on. Ken has himself now joined the debate saying the comment is just a smear campaign.

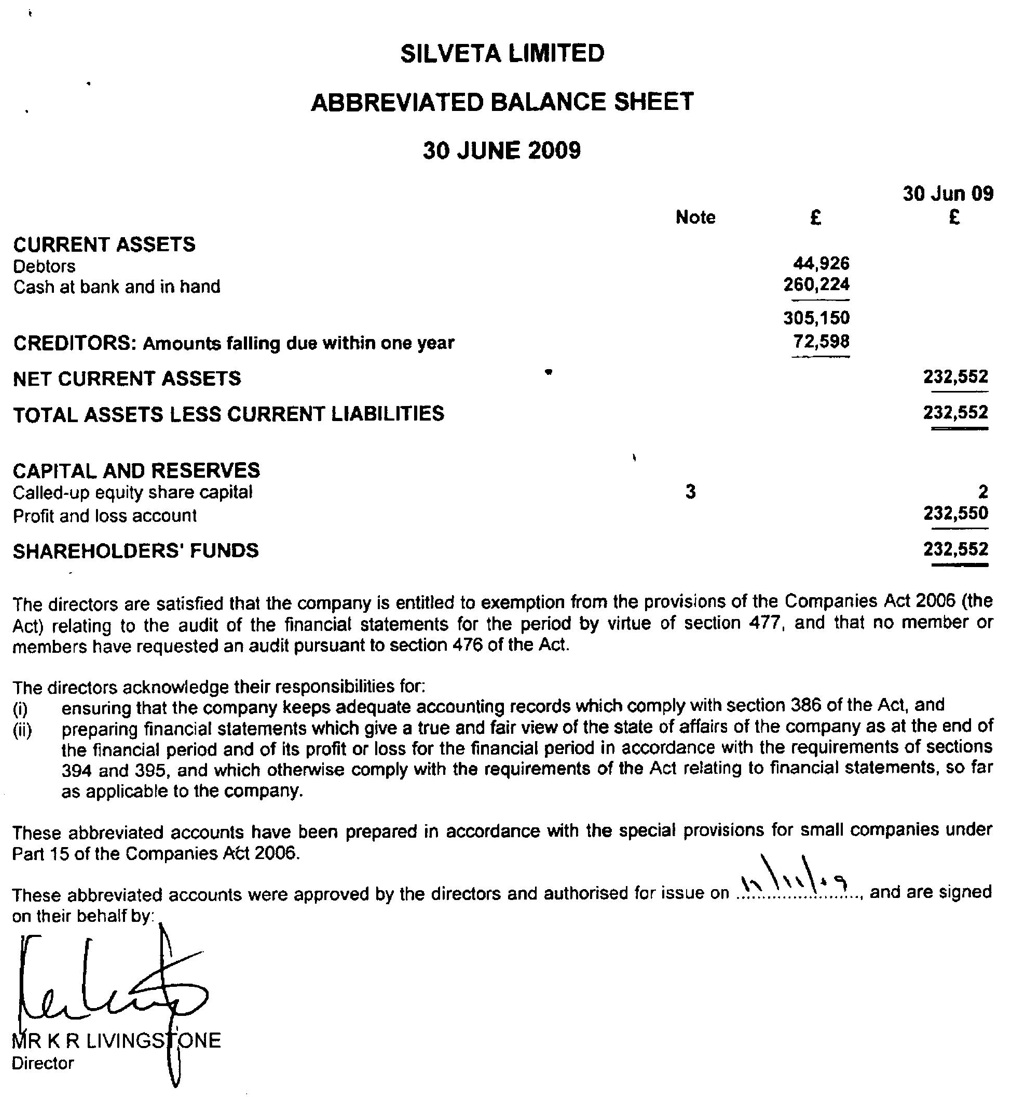

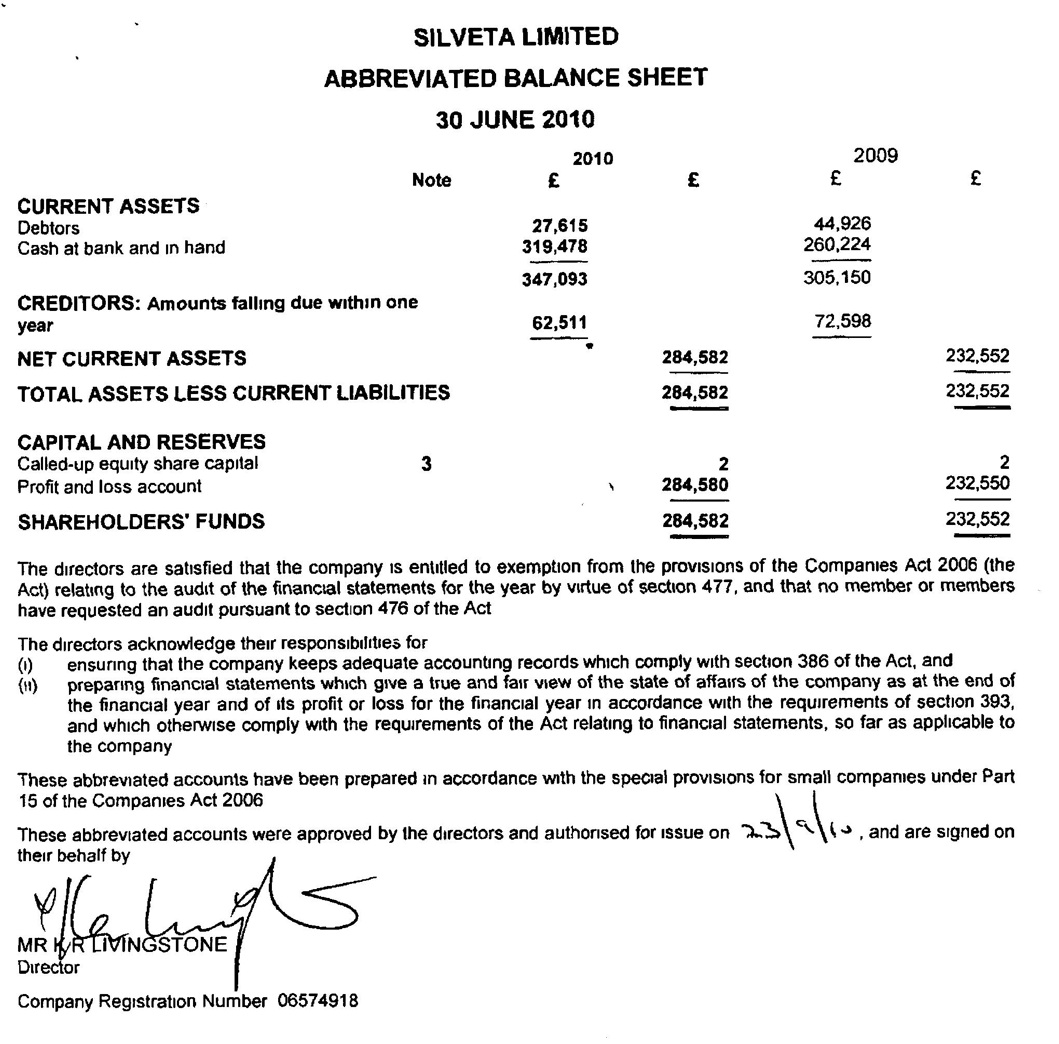

So let's have some facts. These are the published balance sheets of Ken Livingstone's company:

and

In the first year Ken made a lot of money. We have no profit and loss account for the company, quite legitimately. They need not be filed. I always file mine - in the interests of transparency, but Ken Livingstone chose not to do so. That's his right. But whatever happened, he had £232,000 left over after 21% tax in the company. So profit pre tax, and after expenses was likely to exceed £293,000.

Ken says he had expenses. In the Guardian he's quoted as saying:

Livingstone said he employed a researcher, a press officer and his wife who typed his memoirs. "I am in exactly the same position as everybody else who has a small business. I mean, I get loads of money, all from different sources, and I give it to an accountant and they manage it," he said on the Andrew Marr Show on Sunday.

"You pay corporation tax. If you then take out spending yourself, you have to pay more. What I am not doing is paying income tax on the money I use to employ other people."

Livingstone said that he earned £55,000 in the last year and paid the full rate of income tax on that but did not earn enough to pay the top rate of income tax.

"The simple fact is, and the hypocrisy of all this, is Boris Johnson has exactly the same arrangements to handle his earnings from television. Almost everybody in the media, who is not employed directly, has exactly the same arrangements," said Livingstone.

"I am not offshore. I am running a small company, just like hundreds of thousands of people. It's a smear campaign currently being run."

Now let's be clear: what is being done here is commonplace. No one is saying otherwise. It's legal. It's regularly suggested by accountants. I have accounted for people doing it - and have owned companies. And I also have to make clear I've changed my mind on the issue.

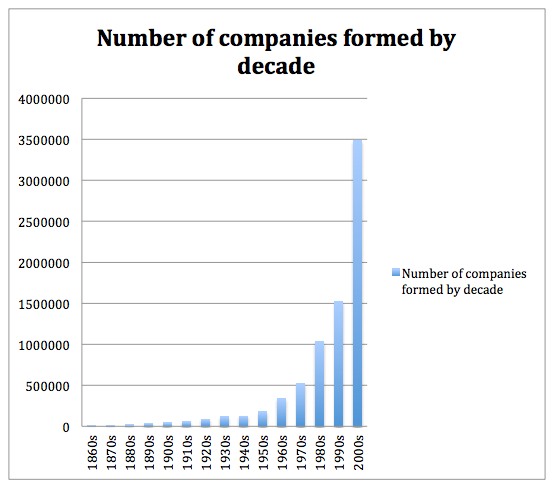

One reason why is that the evidence has demanded that I do so. I've long argued (since the early 1990s) that forming companies unless there was good commercial reason to do so made no sense. Those I've had in the last decade (bar a dormant formed solely for research purposes) have had the sole primary purpose of giving limited liability from risk on publishing data, software and other materials. Tax has always been a secondary (very secondary) consideration. Anyone who has wanted to run a limited company properly has to have a desire for red tape or accountant's fees that makes little sense to me unless commercial motives strongly suggest the need. But it's clear lots of people have wanted to run companies as these tables on incorporation shows (taken from my research on companies, here, data source for this table Companies House):

It is glaringly obvious that behaviour changed completely in the last decade. If you want to know why I changed my mind on this issue, that's why.

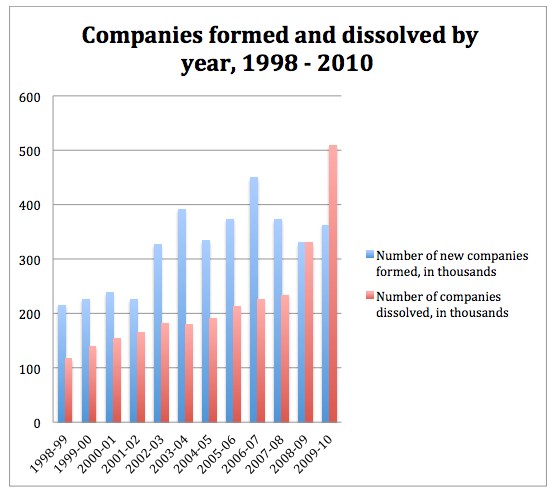

The trend, in more detail, looks like this:

Gordon Brown's absurd 0% corporation tax rate, introduced in 2002, changed behaviour, radically, on small company incorporation. It suddenly became very clear that tax became the driving force for this choice. And the failed IR35 rules (explained here) did not stop this, as is obvious.

As I have shown (here, albeit out of date now but with the principles remaining exactly the same to date) incorporation and paying dividends can save a single person money compared to self employment (my always preferred option for recording my income - and an LLP generates self employed income, for the record). If the income is split in ways that are hard to economically justify based on the apparent contribution of the respective parties to generating it these savings can be significant. HMRC tried to challenge this, and have for all practical purposes failed. I analysed why, here.

That however does not mean that tax avoidance is not going on in scenarios of the type Ken Livingstone has used. His actions are legal - of course. But if tax avoidance involves deferring tax payment or reducing rates at which tax is paid - and it clearly does - then this scenario does potentially do both things, and so avoidance has occurred unless another commercial justification can be shown to exist. So far I've not seen Ken Livingstone offer that - but candidly, this is not about Ken as far as I'm concerned. His numbers just create a case study.

In his case if there are profits in a year after expenses (all of which could just as easily be offset against the income as a self employed person - the rules are the same, after all) of £293,000 then it would of course have been the case that tax at 40% would have been paid on much of this income by Ken Livingstone and his partner if earned in their names. But by paying a few pounds to buy a company and subscribing for £2 worth of shares the tax bill was near enough halved at the time, with the benefit of paying tax in later years and smoothing income over time being secured. I have no idea whether any income splitting took place in Ken Livingstone's case: I'm ignoring it if it did, or not. The simple fact is that tax at maybe 19% on £293,000 was deferred. That's over £55,000.

I'm not saying that won't be paid: it may be in full at some time. But it wasn't in 2009. And given that no other explanation for the company has been given, bar the fact everyone's doing it, and the reason everyone's doing it seems to be very largely tax driven, then this looks like a tax motivated act, even if recommended by an accountant (presumably for that reason).

Candidly, the state could have done with £55,000 in 2009.

So, in the face of the evidence that this practice is now so commonplace it can reasonably be said to be distorting behaviour to an unacceptable degree and is likewise distorting tax receipts what can be done about it? The cost of these structures continuing to be used in this way is now too high for the practie to be allowed to continue, in my opinion. That's why I commented on this case.

I wrote about the changes needed, here, back in 2008. I haven't changed my mind since. The summary is that there should be:

1. A change in company law to allow the re-registration of small limited companies as limited liability partnerships. An LLP is tax transparent: its income is taxed as if it belongs to its members even though it is a legal entity that is separate from them for contractual purposes. Tax deferral cannot occur as a result of using an LLP as a result. Income is taxed in the year it is earned;

2. New capital requirements for the incorporation of limited companies undertaking trades, and over time forced re-registration of those that do not meet that standard as LLPs. That might be to require capital as high as £50,000 in due course. This might be necessary consumer protection inb any event;

3. The introduction of a new investment income surcharge chargeable on dividend income at rates broadly equivalent to national insurance charges that would have the benefit of reducing the incentive to split income through dividend payments, would restore the taxation balance between income earned from all sources and allow a reduction in the base rate of income tax without adding substantially to the burden of administration for taxpayers since those liable will, in the vast majority of cases, already be submitting tax returns;

4. Create new, economically justifiable and verifiable standards for splitting income in LLPs so that the risk of legal challenge to such arrangements will be substantially reduced whilst recognising the significant role that the spouses and partners of those who supply their services through owner managed corporate entities play in the undertaking of that activity.

If this were done then:

a. The administrative burdens for many small businesses would be reduced;

b. The certainty of the arrangements under which they can operate would be increased;

c. The rewards that they rightly seek to pay to those who contribute to the management of these companies from within domestic relationships will be rewarded, but within appropriate constraints;

d. The attraction of freelance status in tax terms would be retained;

e. The current injustice that sees income from labour more heavily taxed in the UK than income from capital would be eliminated in large part without prejudicing the required favoured status of pensioners;

f. The incentives for tax planning would be reduced, so simplifying tax administration;

g. The tax yield might either rise, or a reduction in the tax rate might result.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Umm, Richard – I agree with the principle, but don’t LLPs need two members?

Yes

But the income attributable to the second can be small

So effectively you’d be forcing people to enter into partnership with each other.

I’m not forcing anything

I am asking for reform

And if we can accept single member companies we can accept single member LLPs

Richard

I’m with you in spirit but frankly if a government says if you run a genuine business (you know with clients and suppliers and employees, rather than just a front for your own employment) you can either arrange your affairs as sole trader X or as Y LLP or as Z Limited then why point the finger at those who choose Z Limited? Point it only at the government.

Another point which gets me is the widley repeated ill-informed comparisons between corporation tax and income tax such as this in the Guardian article:

“Critics claim that by directing earnings into a limited company, Livingstone is liable for corporation tax of 20% rather than paying income tax of up to 50%.”

No, Livingstone is not liable for corporation tax at 20%; his company is liable for the CT at 20%; he then takes dividends and if they take him over the higher rate threshold, he pays another 22.5% (32.5% higher rate dividends tax – 10% tax credit), so that’s 42.5% in sum; and if over the additional rate, 52.5% in sum. there’s no saving in income tax there. The real saving is of course avoiding both the employers and employee’s NI. But of course that’s too complicated to grab the headlines.

I am asking the government to change

Your understanding of tax law is wrong. Of the tax payable by a recipient of a dividend 20% is covered by the corporation tax

And in practice they always, for technical reasons, end paying 40% or 50% – not the 2.5% ending rates

So there can be a tax saving if there is deferral and more so of there is income sloitting and your argument does not stack

“Of the tax payable by a recipient of a dividend 20% is covered by the corporation tax”

As well as being unclear, this is simply wrong. When a shareholder takes a dividend the tax payable by him is calculated without any reference to the corporation tax paid by the company.

The basic rate tax is deemed to be paid

That’s because it is assumed to be covered by the CT

That’s the logic – and your comment is just wrong

Please try to understand some tax

I understood that CT is deemed to cover basic rate tax liability but perhaps my comment which related to higher and additional rate liability wasn’t clearly expressed. What is clear is that there’s lots of room for confusion. Another reason for reform.

I agree with that

Ed note: This comment has been deleted as it failed to pass the moderation policy on many counts

Ed: This comment failed moderation.

I have made clear this is not a discussion of Ken Livingstone.

RM- There would be some unfortunate side effects to your proposals. Starting from the Tax and NI viewpoint, existing struggling companies with very small profits where the director/shareholders means the effective tax rate would move immediately from 20% to 29% with Class 4 NI (plus Class 2 NI) and they just could not afford to live.

Small companies often have varying profits, in extremis it would be rather unfair to be taxed at higher rate, one year, and then barely cover one’s personal allowance the next.

And in economic terms small companies need tax breaks, the proprietors don’t get holiday pay, enhanced sick pay, security of income, need to employ savings as capital etc.

It’s’ tough in the real world, I think you have well heeled companies in mind, what you are suggesting will hit everyone. I do the maths every day.

Try self employment

Or an LLP

You’re fabricating a case that does not exist

And the reason you do the maths everyday is for your own gain, not for your client’s

If you acted in your client’s interests you would not incorporate them. But you’d be paid less. And therein lies the rub