I have asked, often, on this blog whether markets might crash. I have said, as often, that I think they will. I continue to hold that opinion.

Why? I have three reasons for thinking so.

Alienation

First, the degree of alienation people are feeling from the world around them seems to be growing at present.

Many people are asking me how I can continue to write about the issues I address here. They tell me they have deleted their news feeds and social media because they can no longer face stories about UK politics that are so out of touch with reality, and US politics that appears intent on wanton destruction domestically and internationally. It seems they have had enough, and would rather live in ignorance.

I am seeing that reflected in our data, and Owen Jones has recently said the same thing. Our traffic is down by at least a third compared to last year, and if anything, I believe we are producing better material, with a stronger educational focus, quite deliberately.

AI is not delivering

Secondly, AI is not surviving contact with customers. The US stock market boom, which is bigger than that in other markets, is based on the value of just seven AI-related companies. They now represent around 40% of US market value. And now people are really coming to terms with their products; they are realising three things.

One of them is that they are very expensive, and that cost is likely to rise. Even Facebook is reported to be rationing AI use among its employees because costs are so high at current prices, and this can only increase, as no AI company is making money at present.

Another is that when you push these products for anything but very routine tasks, they can break, are surprisingly not good at repetition even when given the same instructions, and can take a lot of time to both learn and use, resulting in considerable frustration. We know this. Many other people I speak to are telling me the same thing. That wheels are already falling off this bus. I cannot see AI spreading at anything like the rate forecast at present. It is just not good enough to justify the hype, as yet. It may get better. But the current affordable models are limited in scope, and affordability is key.

And then there is the issue of kickback. People do not like AI slop. It is deeply unpopular on social media. It is almost as unpopular in other uses. I recently got what initially seemed like very good customer service on a product. I then realised it was a program talking to me; the enquiry went off track, and descended into a formulaic sales pitch. From being surprised and even pleased at the speed of response, I ended up feeling distanced from the company. If this is widespread, AI company earnings are not going to meet expectations.

I would add another worry, that I am not yet hearing elsewhere, to this mix. That is, if AI is to deliver, then people will pay as a result of a major shift in rewards from labour to capital. In a world where grievance politics is already very real and, in many cases, justified by neoliberal excess, this is unlikely to happen without major social unrest. At present, this impact is seen mainly in the new graduate job market. IT is going to get worse.

Share valuation

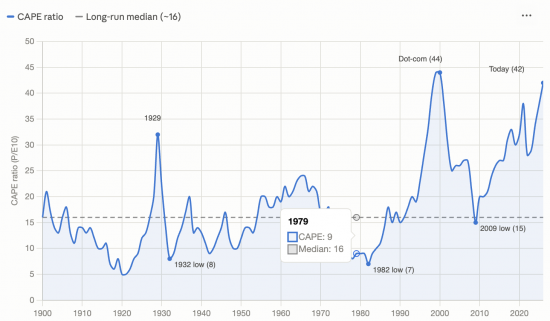

And then, thirdly, there is the issue of excess share valuation. Robert Shiller's CAPE index addresses this issue. This Yale academic's Cyclically Adjusted Price-to-Earnings (CAPE) ratio measures the US S&P 500's aggregate price relative to its average inflation-adjusted earnings over the prior 10 years. The 10-year smoothing dampens the distortion caused by boom-and-bust earnings cycles, providing a more stable read on whether stocks are cheap or expensive. The formula is simply:

Price ÷ Average real earnings per share over the last 10 years.

This is the data for the last 126 years, and, yes, I did ask AI to generate it:

That markets are now highly valued is obvious: even at the 2009 low, they only returned to the long-term mean.

Importantly, there are three peaks: 1929, 2000, and now. They crashed heavily after 1929; they did so again after 2000, and now we are facing another peak.

Does that mean markets will crash again? No; that cannot be said with certainty. But the signs are not good. Just list these factors, some already noted above:

- Economic, social and political confidence is low.

- The US and Israel are out of control, and the full impact of their very obviously ongoing war has yet to hit, but will.

- AI is not going to meet expectations, and to be good enough it will become much more expensive, limiting the scale of its adoption. AI companies are overvalued in that case.

- Climate change is happening, and the costs are growing rapidly, but are being ignored so far.

- Political turmoil looks likely in many countries.

There are probably a few more issues to throw into the mix, but these will do.

So what does this mean? First, current stock market yields, in real terms, are low, simply because share prices are so high. That is what the Shiller chart reveals. They cannot go much higher before the risk-reward ratio becomes absurd. There is no room for further growth. The reality of this has to be realised. Prices could be maintained, but the chance of the bubble continuing is low.

Second, stable high prices are rare. Once people realise shares are overvalued, prices tend to crash. With so many other trigger points now available to precipitate this, that crash is likely.

Third, the crash will not remain in stock markets. Too many banks have lent too much based on share prices for banking stability to survive a stock market crash. The whole shadow banking sector, most especially, could be at risk, and it is deeply material to financial stability, or rather, risk, now, as the Bank of England has acknowledged.

So, is a crash likely? Yes. That is the unavoidable conclusion. We just cannot say when, precisely.

Factor it in, Andy Burnham. If you don't, it will eat your premiership, and if it does happen, it will be before 2029. The irony of the date cannot be missed.

Unless the government plans for this now, we are in even deeper trouble, and is anyone talking about it? It seems that they are not. All the talk is of growth, but that is just a wild daydream that is not going to happen.

Most importantly, and I stress the point, it is this wilful blindness that is the biggest issue of all. The risk is there, and is being ignored. That is a measure of gross irresponsibility.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

An interesting perspective. I appreciated that the post looks beyond day-to-day market movements and asks readers to think about the underlying economic risks rather than assuming markets will keep rising indefinitely. Whether or not you agree with the conclusions, it’s a useful reminder that confidence can change quickly, and understanding the broader economic picture is just as important as following stock prices

I will start with my usual quote “Markets can remain irrational longer than you can remain solvent” but I do agree with you about the US stock market…. but I am the man that has predicted 5 of the last 2 crashes.

I often ask “Why has it got to the level it is today?” and there are a few reasons.

Market access: Online brokers have allowed anyone to gamble on the stock market.

Self-serving “professional” advice: Stocks are always the best long term investment.

Laziness: They have always gone up…. so they will keep going up.

Corporate profits: The politicians (lobbied by corporate money) have allowed companies to reap ever larger profits without regulation…. share prices reflect expectations of ever rising profitability.

These can change in a heart beat.

There are reasons to be less concerned about the UK market – valuations are not as stretched and there are few AI/Tech related companies….. but we know that “if America sneezes the UK catches a cold”.

I don’t think the UK banking system is at risk of collapse….. unless things get REALLY ugly. The BoE stress tests assume a 30% drop in house prices, 40% in Commercial real estate and 9% unemployment – all of which are possible but could be countered by government policy to some extent as they were in 2008 and 2020.

Once we get into the “shadow banking system” things are more murky and nobody knows the risks and (more importantly) the linkages to the real economy.

Much to agree with – and the accounting is a key issue because it is deeply pro-cyclical – but banking is at risks because of its exposure to shadow banking.

Whilst there maybe fewer UK baser AI businesses, UK based businesses have largely drunk the AI koolaid. They are still expecting AI to reduce wage bills, improve efficiency and create innovative new products (or rejuvinate existing offerings). Once board members and share holders realise the shortcomings of non-corporeal AI, it is going to become apparent that many UK companies cannot deliver on their projections.

The job market, at least from my perspective, has stagnated because of AI. Academics have demonstrated AI screening of job applications is more often than not, leaving the best candidates high and dry.

And personally, I think the biggest threat of our current trajectory is going to be food scarcity. Once consumers start to notice, consumer confidence will nose dive and markets will follow, if the AI bubble has not already burst by then.

The ” language machine” companies have been issuing corporate bonds. One. it is rumoured. is paying 17% interest on one round of bonds. They are also involved in circular funding of each other.

These companies are not producing profits to pay their financial obligations.

The way you pay for the use of their products through “tokenisation” is pushing the price through the roof. Guess what, the user companies are going “stop, stop, stop, we run the risk of wiping ourselves out”.

Musk’s space company is 90% reliant on US government contracts to run/fund the space programme.

It’s amazing the US federal system is wasting money and must be cut. But hold on not the area that my company needs government contracts.

The Great Trump Depression is still on track. If the Houthis block the Bab el-Mandeb Strait (highly probable) and the Straits of Hormuz remain effectively closed the global economy will start to unravel very quickly.

Why? No container ship company will risk sending ships into such unstable environments.

Remember on the 27 February the Straits of Hormuz were fully open. On the 28 February Trump and Netanyahu attacked Iran and the Straits have been “closed” since then.

Who caused the closure? Trump and Netanyahu. Who is still the cause of the closure? Trump and Netanyahu.

Is the UK preparing for this? It appears not. Remember the Colonel commented a little while ago that Labour did not get it.

I understand that the Civil Service’s immediate concern is transferring staff to Manchester. Guess what? No one wants to go.

The UK is about to be blown away by external events and I don’t believe Labour has any idea what may hit the economy.

So batten down the hatches, the ride may be very bumpy.

Much to agree with

Totally agree re AI slop can’t even do basic research

EverythIng I recommend must be free to public sector professionals.

i asked AI to find free developmental checklist up to teens. It came back with one that cost $100. After interrogating the slop, it admitted it wasn’t free. And then didn’t find better UK free developmental checklists, which I knew existed. Not truthful nor thorough, can’t be trusted.

Yes. Really is slop.

Apologies to post twice.

Alienation. Definitely.

FtF is where I go to find analysis, expertise and hope. A rare thing.

I feel great spiritual pain at having psychopathology in charge of the planet and humanity. The news is just rinse and repeat of their depravity, unbearable.

I spend more time with our local anchoress, Juliana of Norwich. Who lived in troubled times, to this day her words and wisdom give comfort.

I have read much about her, some time ago.

Just regarding AI, I’m certain the bubble will burst before not too long. I watched a YT video about AI the other day and author David Gerard explained that a lot of tech companies are quietly rehiring the staff they tried to replace with AI because the work the AI did was so poorly coded. The AI output invariably needs major rework which is incredibly tedious and demanding to rewrite because of the complete lack of structure which you’d never get with even a novice human coder. He described the AI output in software as being the equivalent of cardboard mock-ups that look the part but don’t actually work in the real world.

Another point he made was that the AI products are so heavily subsidised to trap new customers, whereas the real cost could be as much as 40 times higher than the prices on offer currently. When the reality is laid bare, no one is going to be able to afford to use AI. And the funding runs out for a lot of these big companies in 2027. There are going to be some really hard questions asked about delivery and returns.

Anecdotally, AI does not survive contact with customers. I upgraded a VPN product recently and checked with the AI would I be eligible for refund if it didn’t work out. The AI said yes with the caveat that I could use no more than 10GB of data. I only wanted to subscribe to a news site to see if I could access it. Long story short, I was already ineligible for a refund because that limit included prior usage which it hadn’t told me. The AI even refused to connect me to a human but I ended getting a refund, from a person.

The newly released open-weight Kimi K3 language model from Moonshot exceeds even Claude’s Fable 5 on coding benchmarks, and it is about 1/3 the price. This victory is in part because of the hardware restrictions imposed on Chinese companies by the US, forcing them to concentrate on efficiency.

Couple this with the shortfall of power supply in the US while China builds ever more capacity into their grid and it seems clear that the AI battle is already lost and China has won. All of the AI investment has been predicated on the US companies having dominance in the market. This is no longer true.

Alienation – so much to agree with Richard, as noted hitherto, you and you contributors are a daily dose of sanity for which I am deeply grateful, as this is directly opposed to ‘hopium’, if you see what I mean.

Thank you.

I wonder how many AI users ask about the embedded values and attitudes that all AI systems have and how these are reflected in output the users and their customers receive? The insidious influence over time can have a damaging effect. The best way of avoiding this type of issue is perhaps not to use AI in the first place.

Don’t ever search the webh then, using any known search engine.

Or you can run AI locally so that the data never leaves your computer. It’s getting easier and easier to access. I use it for engineering calculations and other work but my clients would not be happy with their propriety data being sucked up by some AI corporation to profit from. You can’t compete with the power of AI run in big data centres but the models available are still quite capable on a modest set up.

Apple now has an LLM built in. I have not tried this as yet…

I only usually let AI summarise my own work – it seems to be reliable for this.