As Katie Martin has noted in the FT this morning, there is something exceptionally strange going on in the world's financial markets at the moment, and we should be taking note.

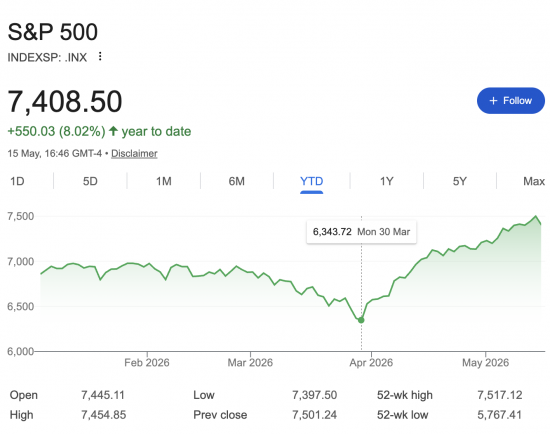

Since 30th March this year, the S&P 500 index in the USA has gone up by approximately 17%:

This, as Katie Martin points out, using not wholly dissimilar language, feels like pre-crash mania. There is a good reason for her concern, which I have also expressed for some time, and that is that this is precisely what we are seeing in this chart.

The long-term chart makes it clear just how absurd the current situation is:

Those engaged in these trades might fear missing out, but what they are actually doing is exposing themselves to enormous risk.

The reality is that, as the realisation dawned that the Strait of Hormuz was closed and unlikely to reopen for some time, with massive economic consequences for the world, stock markets have celebrated as if there is no tomorrow. That might, of course, be one possible reaction to the situation that Donald Trump has created. This particular reaction, however, adds to the economic meltdown I expect this summer and autumn, the risk of a stock market crash. That, I think, is now entirely unavoidable, and to a greater extent than I ever believed before.

Then add to this something important, which is the chart that Katie Martin produced showing what has happened to government bond rates around the world since that stock market euphoria erupted on 30 March. This data is from the FT:

Everywhere, and without exception, traders are, utterly bizarrely, at a time of crisis when they should be heading for safety, selling bonds and buying shares. After all, the money to fund this mania has to come from somewhere, and this chart makes clear its source. When government bonds are sold, the effective interest rate increases. That is because, in practice, the amount of interest paid on bonds is fixed, meaning that if the price falls, as happens in a net selling market, that fixed interest payment appears to be more valuable in terms of the interest rate earned.

I stress, the trend is universal. The UK might have experienced a slightly larger increase in rates than other countries, but it is no exception to the general rule. To therefore pretend that there is a peculiar crisis in the UK, and that this has something to do with whatever Labour might be up to, is total nonsense.

To even pretend that any of this has something to do with a change in the risk profile of gilts, or inflation expectations, or just about anything else, is also utterly absurd.

All that is happening is that market traders are following the herd in pursuit of what they think might be gains, and are ditching government bonds as a result to put all their money into shares, with the risk that they will suffer very large losses as a consequence, at cost to those in whose interests they are meant to act, many of whom will be people saving for their pensions.

This behaviour defies all rationality. Anyone with any sense can perceive that we are facing fuel and food shortages, and the risk of massive supply chain disruptions as a consequence of Trump's war against Iran, with a resulting risk of economic meltdown, substantial falls in corporate profits, the risk of corporate failure, and a banking crisis, both in the mainstream and shadow sectors.

The likelihood that this might be as bad as 1929, with consequences at least as severe if governments do not take action to bail out many of those who will be impacted, is very high indeed. In that case, if you look at what is happening in financial markets, the only reasonable conclusion to reach is that those trading in them are giving themselves a massive dopamine hit at cost to the rest of the world before the crisis arrives.

I am angry because governments are going to have to bail out banks and even major corporations as a result of what is going to happen. We will be doing QE again, but this time we have to get it right.

I am angry because millions, if not billions, of people will suffer the financial consequences of this coming crash, just as they will also suffer the direct economic consequences to their employment prospects and the real physical consequences of supply shortages.

I am angry for all the people whose futures will be destroyed as a consequence of this utter folly.

I am angered by most in the media, who are completely distorting this story to say that markets have lost confidence in governments, when in fact the true story is that we should have lost confidence in markets.

I am angry with the media that says nothing about the idiots trading this way, whilst demanding that governments must serve them.

I am angry that we have ministers who apparently cannot see what is going to happen, or who are doing absolutely nothing about it, meaning they are, as a consequence, contributing to the disaster heading our way.

I am angry at the pretence that life is carrying on as normal when it is doing anything but that.

I am angry that we do not have financial transaction taxes that could kick in to prevent speculative trading of this sort.

I am angry that we still have a bias within our tax system towards wealth and against ordinary people, which means folly of this sort is supported by the state.

I am angry that we have banking regulations and financial market regulations that do nothing to prevent all of this.

I am angry that neoliberal politicians still think, despite all the evidence to the contrary, that markets are rational when they are anything but, as this situation shows.

And one day, I know I will come back to this post. I am going to say, “I told you so”, and I will be sorry to say that, but I know it is going to happen. In the face of this type of madness, nothing else is possible. In the history of stock market investment, no other resolution to madness of this sort has ever been found.

My advice is then, to batten down the hatches, expect the worst, and, if you have any control over your own financial affairs, and I am well aware that not everybody has, look for safety. Do not worry about missing out now. Take the long-term view. Markest may be abandoning caution. There is no reason for you to do the same.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Very good Prof. M, if somewhat frightening.

May I ask – how is a regular bloke to batten down the hatches? Can an individual buy govt bonds with his (cash) savings?

Yes.

Some platforms sell them.

And then you read articles like this, and wonder what the heck is going on with all the ‘behind the doors’ negotiations?

https://economymiddleeast.com/news/uaes-sheikh-abdullah-bin-zayed-meets-british-mp-in-london-as-bilateral-trade-exceeds-33-7-billion/

Where is the money going? Not where it should be.

Corruption under another name basically.

If, as is here hypothesised, we have not one but three economies, as listed below, might it be that a considerable proportion of politicans and writing and speaking main stream journalists function for the support and encouragement of the group 1 economy?

1) The wealthy/powerful/influential

2) Regular citizens and their children

3) The significantly disadvantaged and so weakest socio-economic group

Might it be that group 1 chooses to further disadvantage group 3 because they are the easiest target?

Yes

Ans 2 is shrinking towards 3

The billionaires and multimillionaires are safe in their bunkers and gated housing, so don’t give a damn. Funding the extreme right and living under the illusion that AI is going to produce even more profit and abundance. Blind to the fact that massive unemployment will follow, let alone the ecological consequences. What to do? That is the question. Certainly no clues from our present rulers.

So what we are actually seeing is a repositioning of asset holding in anticipation of a crash – betting in other words? A last gasp of transactions that will of course mean that the survivors will still get their bonuses when the inevitable happens? And who will be left holding the bag this time? Well, OK, maybe one private banking institution or two will just run out of time but inevitably it is ordinary working people who will be left holding the bag won’t it?

This is no way to run a global economy, that is for sure.

But I’m afraid something else occurs…………until such a time as ordinary citizens – ‘main street’ – acquaint themselves with the facts of money – ask where their consumption of cars, housing, everything actually comes from, they will be nothing but ‘things’ swept along by unreason into unfreedom. The citizen I’m afraid must free themselves. This blog and its offshoots hopefully can get them started.

But fundamentally, I think what enables the Neo-liberal airship from crashing to the ground (it is already on fire, with no engines) is the citizen’s deference to wealth that keeps it in the air. You see, how can you question what you worship, when the worship is a statement of belief? We are asking citizens to question something they believe to be perfect state – to aspire to (wealth/stuff). Doing so is at act of personal sovereignty, rebellion even. But that is why it is so difficult. But you need the resources to start to do that, and these blogs/substacks etc will help people on that journey.

Much to agree with.

I was churning similar thoughts this morning driving down the M1.

I have learned a lot through the discussions on these blogs and on the YouTube videos, especially when having no specific politics/economics background apart from being affected by the consequences of the socioeconomic effects having worked for the NHS in the community, living with a chronic disability, having things going on in the community around me linked to crime and justice/mental health/social housing; and finding that my thought processes are coming into conflict with other members in the extended family and past friends to the where I feel isolated not wanting to be in the same bubblesphere that they are in, and when I do speak out – I am the one that gets criticised for my behaviour being out of control!!

What has become more apparent with my self-learning, and please correct me if I am wrong, is how much of this so-called “wealth” is just electronic numbers being passed from broker to broker, gambling upon how high a margin they can get on a ‘deal’, but with nothing actual physical being traded or a service provided. So if the servers went down with a huge virus or lack of power for the cooling required for the mega data centres, then what?! A person living with a small patch of land, with some cattle, vegetable patch and having things to take to market and able to keep themselves and community sustained would then be content and wealthier than the City broker who wouldn’t be able to access anything that is electronic and haven’t the basic skills for daily living as have been to eager to run to the summit before walking around the base and setting camps gradually on the way up.

I think you are identifying two related issues.

The first is personal, and very real. Once people begin questioning the assumptions that dominate modern economics and politics, they often do feel isolated. Many of the ideas we are taught to regard as “common sense” — government running out of money, markets always knowing best, wealth reflecting merit — are repeated so constantly that challenging them can create friction with friends, colleagues and family.

The second issue concerns the nature of modern wealth itself.

A very large part of what now passes for wealth is indeed financial claim-making: assets being traded, repriced and leveraged without necessarily creating much new productive activity. Vast sums move around financial markets every day with little connection to producing food, housing, care, energy or other essentials.

That does not mean all finance is useless. Productive investment matters enormously.

But your instinct is right that resilience and real wealth ultimately depend upon the capacity to meet human needs in the real economy:

* food,

* housing,

* healthcare,

* energy,

* skills,

* functioning communities,

* and ecological stability.

In that sense, someone with practical skills, community ties and access to productive resources may indeed possess a form of security and resilience that highly financialised wealth does not provide.

I would not romanticise collapse scenarios. Modern societies are deeply interconnected, and most people depend on those systems functioning.

But I do think recent crises have exposed how fragile a heavily financialised economy can become when detached from the underlying realities upon which all prosperity ultimately depends.

Thanks Richard for your reply to my comment, and I was taking a rather ‘extreme’ analogy of having a subsistence model of something physically real, compared to something more ethereal especially when there was all the hype over non-fungible tokens, and I still can’t get my head around cryptocurrency especially meme coins.

In the same way, looking at the graphs and the interselling of bonds, that initially would have had a fixed yield set by the national issuing bank, seems to me like money is being made out from nowhere. Left to go spinning out of control, because people are gambling on how high they can go before somebody says no, and things fall just makes me scared. Whilst realising the need of these different methods of wealth creation, I am more annoyed about where the source of those funds have come from and where the returns should go. People can gamble their own private money away if they so chose to do so. And if they go bust, then that may have to be their responsibility and choice, unless voices of reason over greed can prevail otherwise.

I think you are being rather Aristotelean, and there is no harm in that. Aristotle argued that we should treat objects in a manner befitting their fundamental nature, and since money is not meant to be a good in itself but only a medium of exchange, he concluded that it is unnatural to desire money as an end in itself. We have long forgitten that.

Good morning Richard.

To have my thinking related to that of Aristotle, I have never had that commented on before, so I’ll take that! Thank-you.

My core values though go much back before the Greek philosophers and further East to Indian subcontinent. I continue to practice my Jain faith which very much has three main tenets of having right beliefs/moral codes; right knowledge; right conduct – all three to be utilised at all times in daily life to minimise harm to all life.

Parasparopagraho Jīvānām • परस्परोपग्रहो जीवानाम् : Souls render service to one another. All life is bound together by mutual support and interdependence. – Tattvārtha Sūtra [5.21]

Do you know Atul Shah and his work?

I don’t know Atul Shah, and had to do an Internet search and saw that he has published articles and written books based upon his Jain faith:

https://theconversation.com/ive-studied-faiths-and-cultures-around-the-world-heres-how-finance-can-be-made-more-inclusive-and-sustainable-258254

Was talking with my Dad, and when in Uganda their accountant was a different Atul Shah who had an accountancy firm AM Shah & Co. with his brother.

AK Shah who you refer to, is Kenyan born, and of the Oshwal Jain community.

I was born here in the UK, and as my grandparents adapted things from India to life in East Africa when migrating in 1930 (before partition), and my family having to leave Uganda in exile in 1972 to the UK; having to constantly adapt and bridge differences across generations and cultures with being a “second generation British Ugandan Asian immigrant of Gujarati Indian Origin”, should I choose to label myself as such, together with all the other flags, and labels I could attach and bind to me rather than just being myself and getting on with living life and assisting others in doing the same when able in whatever capacity I can. This then links to your other topics regarding the current political climate in the UK, and all the joys of ‘identity politics’.

My friend Atul is a good guy.

It is very odd that there is no word, no preparation from politicians, media or markets about the supply crunch that is going to hit. Do they really believe the aggression against Iran is going to be over tomorrow?

On the stock market, there is the argument of the ‘passive bid’ – that c.50% of the stock market is accounted for by passive index funds, and that a large proportion of retirees still maintain money in the market, rather than switching to annuities.

The rise in bond yields is more difficult to explain. Perhaps it is as you say that FOMO is shifting money from bonds to equities. Or it might be Gulf states and others liquidating bonds to raise cash?

In a previous post you suggested that if one is near retirement, to get an annuity sorted. Given yields are going up, and we may be in for a period of stagflation before a deflationary recession hits, is it worth waiting until bond yields go higher? Or do you think the BofE will do yield curve control to manage the long rates?

I cannot offer what feels like investment advice.

It’s quite obvious to anyone with basic knowledge of markets and economics, that if inflation is your concern, buying bonds isn’t your path to safety.

its quite obvious from the graphs posted, that although the direction of bond yields is similar across markets, yields in the UK have increased much more – that’s because the fear of inflation is much great in the UK, directly as a result of Labour policy (and fear of a shift leftward in Labour policy).

And in the face of a global economic meltdown, shares obviously are.

Stupidity has to appear here sometimes. You just provided it.

Richard thanks for highlighting that the bonds sales are worldwide, with the proceeds being put into share purchases

I get it that if I own government bonds and want a quick sale then I can expect to sell at a loss compared with my purchase price.

I have probably got this wrong but.

I buy a £1bn UK government that redeems in five years for £900mn, fixed interest of 5%.

I keep the bond, the government redeems it in five years. I get £1bn, a profit of £100mn.

The government has paid me 5%. interest. It is not interested in me buying the £1bn bond at a discount. And it is certainly not going to pay me more interest because I book a higher rate of return on my investment than 5%.

What I don’t get is how me striking lucky pushes up the interest the government must pay for future bond issues.

Surely as the safest investment vehicle in the UK the UK government can tell the market to take it or leave it.

As you have previously written why can’t the ordinary person put their money into government bonds? The only current argument against is the neoliberal “you must invest in the market” and “only the market knows best”.

Utter garbage of course.

John,

I’m not the most knowledgeable contributor here, but my understanding is that if you can buy a 5% bond on the secondary market for less than face value then why would the primary market buy a shiny new bond for face value unless the interest rate was higher?

One option is for the government to call their bluff and say that the security of a government bond is available at 5% plus nothing. Take it or leave it.

The graphs in Richard’s article are very, very telling. Notice that somebody is very clearly willing to buy Japanese bonds even though the returns are way below everyone else’s. Though that might just be The Bank Of Japan itself!

And we should remain angry at declines in living standards, healthcare, mental health, healthy lifespan, all while we continue to produce more and more per capita.

That’s all the fault of the neo liberal ‘experiment’, too

And meanwhile we have an ineffective prime minister in office but not in power and a Labour Party imploding inwards. I hear your frustration, like a biblical prophet who can see clearly the inevitable, but knowing no one wants to hear. I really hope when the inevitable happens a war time spirit is initiated and people help each other, rather than the Tory bungs and those in deprivation being the hardest hit.

Given the choice I might study form…………

(Gee Gees)

The thing is it took more than decade in the 30s depression and then WWII to cure the powers that be and see sense, tax the rich, set interest rates low and introduce rationing thanks to John Maynard Keynes.

The similarities now are striking. So will the realisation dawn sooner? Your piece on the cost of war and the stalemates around the world due to asymmetric adversaries suggests that war is not the answer. I think you are right that the crunch will come later this year. That seems inevitable now. Sadly Central Banks will likely hike interest rates, which will make it worse.

The war on extreme inequality is the one we need to win, just as Keynes and the pre and postwar consensus realised. Will that take more than a decade? I hope not for the sake of those suffering now.

My belief, bolstered by your incisive analysis, is that the poor can also wage asymmetric war on the rich at great cost to the rich as they have little to lose. The state just needs to realise whose side they should be on.

Excellent post and analysis as always Richard. However, I struggle to agree that inflation expectations are not a factor for all bond rates, and potential changes in leadership and economic policy in the UK are not factors. I do agree with the core of your argument that the driver of the crazy stock levels, and this pulling money out of the bond market, can only be explained by FOMO (and AI powered stock software), I just can’t totally dismiss inflation, and individual economic policies also being contributory factors.

What is the risk? And why? And why do you think it will not ne mitigated, which would be easy?

The risk is inflation. And everything you support would exacerbate that – perhaps you just don’t understand economics?

I have written on this extensively. MMT is obsessed with inflation. See the MMT Source Book https://www.taxresearch.org.uk/Blog/downloads/

Perhaps your problem is you do nou understand the first thing about what you are claiming. See

https://www.google.com/search?q=site%3Ataxresearch.org.uk+inflation&sca_esv=96c9b401009ab525&biw=1425&bih=807&sxsrf=ANbL-n44KctAQXpy8cMSoqJoVKrbJZ0ttw%3A1778996807022&ei=R1YJasyNAdmkhbIPzpyAgQg&ved=0ahUKEwiMzfTFz7-UAxVZUkEAHU4OIIAQ4dUDCBI&uact=5&oq=site%3Ataxresearch.org.uk+inflation&gs_lp=Egxnd3Mtd2l6LXNlcnAiIXNpdGU6dGF4cmVzZWFyY2gub3JnLnVrIGluZmxhdGlvbkikKVChAlj2GnABeACQAQCYAW-gAdsEqgEDOS4yuAEDyAEA-AEBmAIAoAIAmAMAiAYBkgcAoAeEAbIHALgHAMIHAMgHAIAIAQ&sclient=gws-wiz-serp

Its a bull market and everyone is piling into the secondhand share market hoping to make lots.

We are in the stage of “the euphoric economy” though this time the future is not assured at all (financial collapse from energy shortage, environmental collapse from climate warming) but the consequences of a recession or depression will be.

Minsky combined insights from Schumpeter, Fisher and Keynes to develop a theory of financially-driven business cycles which can lead to an eventual debt-deflationary crisis. Steve Keen uses this in his economic model Minsky / Ravel.

Steve Keen Monetary Minsky Model of the Great Moderation and Great Recession

https://www.aeaweb.org/conference/2011/retrieve.php?pdfid=185

Steve Keen Minsky At 100. Deriving and validating the “Financial Instability Hypothesis”

https://www.youtube.com/watch?v=qu0WwkZF4FI

Stevce and I are as one on this issue.

Bonds are being sold so what’s happening with the proceeds? Cash, land, gold? It has to be equities as the market going up. I’ve shifted some of our ISA’s to the most cautious fund. I agree with Richard (and the guy at the BofE btw, that equities are overvalued.

If you are right we could soon find ourselves echoing the words of John the Seer (Rev.18:2 – though the whole of the chapter, for those who can interpret its cultural context and sometimes startling imagery, offers an analysis that is highly relevant to the present situation – and I never thought I would find myself saying that in a public forum).

This will keep happening until our governments tax unrealised gains from assets. It would only need to be a small % of the annual gains on equity, bonds and property to rebalance the broken system. The argument that it’s hard to do holds no water given the outcome from not doing it. Wouldn’t it be great to tax assets rather than work?

How would you manage losses?

No charge for losses. If everything is losing, the government will need to borrow more anyway. Also we could Reframe the argument: if you want access to 66 million people with infrastructure & legal protection, this is the cost of doing business. The focus is on the asset, not the owner. Property can’t go anywhere. Equities and bonds are managed by a broker, who (for a fee) would be responsible for sending the tax in. Derivatives would be a challenge though! Given we have put a man on the moon, sequenced the genome and have calculated the age of the universe – not attempting to fix a taxation system feels like an embarrassing lack of ambition. Btw – Thanks for the YouTube channel – really valuable content!

Thank you, but if gains are charged losses have to be accounted for, if olny by being carried forward for offset.

Why? We’re only interested in asset appreciation.

I am also interested in tax justice.

I do not ignore that.

Absolutely. To be sustainable, it must be seen as fair. I don’t see where this wouldn’t be – but am happy to be educated

What do you make of the news that Swatch have had to close stores because of the size of crowds gathering for the launch of a new watch that will cost at least £335 and are allegedly on sale on line second hand (excuse the pun) for up to £16000?

I have not seen that news

https://www.bbc.co.uk/news/articles/c1d2qldr0yko

I had to look it up .. a watch that you don’t wear on your wrist for starters! And you have to wind it up!! Trying to be “disruptive”, by having it swinging from your pocket.

Even on the swatch website they said that the pocket watch would be available for months and not to overcrowd stores…

https://www.swatch.com/en-gb/royal-pop.html

Those that queued up must have too much time on their hands!!

What does the watch do to justify that price value?

Plus ça change, plus c’est la même chose…

We know the price of everything…but the value of nothing.

Tik-tok hypermania!!

I am going to start wearing a monocle and walk around in spats and a cane.

Though can you get varifocal monocles?