As the Guardian has noted:

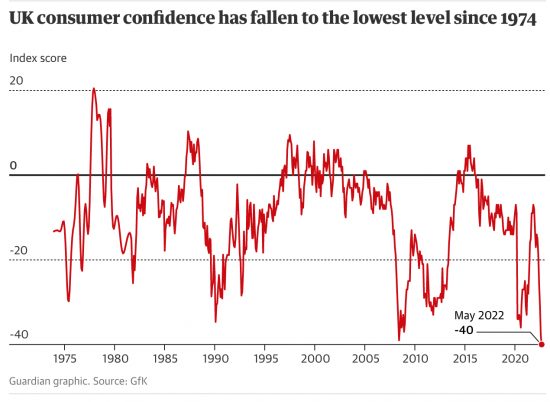

Consumer confidence in the UK has fallen to the lowest level since records began in 1974 amid growing concern over the cost of living crisis.

Stoking fears that Britain is heading for a recession caused by the squeeze on family budgets, the latest monthly snapshot showed consumers are now gloomier about their prospects than they were during the 2008 financial crisis.

- to keep people in their homes, whether rented or mortgaged:

- in their jobs;

- out of debt;

- with employers who can survive the shocks to come; and

- to ensure that they are fed appropriately and are warm.

When at this moment none of those things can be taken for granted, and the government is doing nothing to help, this is a massive challenge which I fear the government will fail. The human cost of that will be high, and I will regret and mourn all the suffering that will occur because all of this is avoidable.

Third, whatever the political significance of Partygate, and it is huge because of the rapidly creeping corruption of fascism that it makes clear exists in this country, this issue is bigger. But, and that is a massive but, if I am right in saying so then it requires the main opposition parties to stop aligning with the bankrupt thinking of the Bank of England and to instead have the courage to go their own way. Direct intervention to help people, requiring government spending of £50 billion or maybe more, is required now.

That funding is readily available, whether through new money creation or by increasing the size of government deposit taking if the funds are to be used for investment purposes (and some should be). Public sector debt paranoia at this moment in time is no excuse for the government imposing private poverty on the UK's population.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Not simply because of the poverty of economic thinking, but also because they don’t seem to give a damn. It is scandalous. How this lot were ever voted in is a mystery to me.

The Government is actually compounding the problem by obliging people to accept a compulsory loan, with a non-negotiable repayment schedule (as supposed ‘help’ with energy bills): a compulsory loan. I cannot think of anyone, outside of loan-sharks and gangsters, who would visit compulsory loans on a vulnerable population. I remain astonished that nobody seems interested in this scandal of misgovernment, and the shocking abuse of power represented by Sunak’s decision to implement it.

Notice that a Conservative Government has now delivered the precedent for future policy use, of ‘the compulsory loan’. Governments will now feel liberated to use this new, convenient, and powerful policy tool, at Government will. It is a population carrot, with the biggest stick built-in and ready to use with lethal effect on the powerless loanee. This is tyranny. God help us.

What we need is for the Good Law Project to take up the case, and a public-spirited organisation who could launch a crowdfund to finance a court case against the Government in the Courts. I doubt if the Courts would look kindly on this, under common law at least.

….. at least that is my hope.

Second the motion concerning the Good Law Project. Let’s juat hope they take up the cause.

On the issue of compulsory debt : there is nothing new about this.

I only bought a house with a mortgage because of landlords kicking me out on the street for trying to fix a fair rent; young people are forced to get into debt to pay for their education and soon old people will have to get into debt to pay for their hips, eyes and heart operations (or die on the waiting list). Universal credit also puts people automatically on repayment programmes as I understand it.

What is new is that the idea that interest rate increases solve inflation is now proved to be wrong as Richard explains.

It would be good to hear Starmer and Rachel Reeves say the same.

Its not that difficult to understand…

The silence you speak of is nothing more than a conspiracy.

I know we don’t like to talk about them here but that is how I see it.

There is and has been an information war on these issues for some time.

You only have to look at the burgeoning far right in America to see what is coming our way.

A new version of Friedman’s Pinochet era.

I hope you and Danny Blanchflower continue to champion Economics by walking about.

In the real world, somethings really shout at you.

In the world of Horse racing, beyond the major race meetings such as Ascot and Cheltenham, there are a whole range of secondary race meetings that are very accessible and popular with members of the ordinary public.

Recently, we have had Chester and the York Dante meeting. Both were shockingly empty.

Elderly bookies with very long memories were saying they had seen nothing like it.

Interesting….

The government is “blaming” overseas factors for the inflation and so can wash their hands of any responsibilities despite widespread publicity of extreme poverty that is or will affect at least the bottom two deciles of the population’s income distribution. They think they can ride the tide of public anger and wash their hands of it like their attitude to the Irish famine of the 1840s or the starvation in Bengal under the British Empire.

AS far as the personal impact of recession is concerned isnt it time to revisit the idea of National Insurance and look at the ‘perils’ it should cover, in particular unemployment?

I see Mervyn King (quoted on Sky News) has now waded in. The inflation is all the result of excessive money printing by central banks, thus the BoE is very largely responsible, apparently. So now we all have to don sackcloth and ashes and ‘pay the price’ of very high interest rates.

I take it that being entirely delusional is an essential qualification to be a central bank governor?

It would seem so

Having never had a UK student loan (I had a small one in South Africa from Barclays), then this isn’t something I keep an eye on. So just completely shocked to read in The i that Sunak has changed the way the interest rate is to be set back in March. So it will now be the July RPI + 3%. So that could make it 12 or 13% for next year. Talk about not ‘burdening the next generation with the National Debt’!!!

So the Government borrowed it at the current less than 2% cost of a UK gilt, lent it to the students, securitised the loans and sold them off mostly to private equity type persons, who no doubt bought them predicting rates would be quite low and based what they paid on that, now suddenly to get 12% pa or more? A killing or what!! Though it might well kill the students.

So are the Tories intent on a national depopulation? The next generation are in debt bondage for life (isn’t that Modern Slavery?), never leave home, marry or start a family, and by 2100 there will be nobody left except Rees Mogg type folk and some robots?

BTW, the January train fares are also based on the July RPI + X%.

It isn’t often I am genuinely shocked!

Legislation could change this, of course, but the student debts have been sold

Nice to see that I’m not the only one considering a depopulation theory in explaining Tory behaviour.

But the student loan book – that is nothing but criminality – it’s loan sharking at the highest level to me that is. And I too have heard with my own ears about the crocodile tears over the next generation being saddled with debt.

Ha – the Loan Shark State – wow – rentierism gone mad.

There is something evil at work here underpinning all this and it is established wealth pulling the levers of power – believe you me.

They could indeed be going for depopulation. I live near Hampton Court and when the deer start getting too numerous and the herds start threatening to spill out of their area into ours they get culled. Given our Establishment’s lofty opinion of themselves it’s entirely credible to suggest they feel the same should happen to the rest of us as we get, in their eyes, too numerous.

On public debt ‘paranoia’, the increase in interest rates is used to terrify the public with the inevitable increase in the cost of servicing public Government debt. Oddly, however in the case of around £117Bn of NS&I Premium Bond debt (? – I may not have an accurate fix on the current debt level), the Treaury has blithely ignore raising the ‘prize rate’ (which sets the interest rate paid); thus the causal relationship between base rate and actual rate paid is neither direct nor immediate, in all cases. This is not a mere matter of timing, because in all matters of debt, timing is everything: timing defines the existence, and survival of all financial institutions. It is the very essence of debt (and the core of the distinction between credit and money).

The answer is to not raise interest rates…

Or have a 100% tax on banks from the benefit arising to them from doing so

Richard, I was not making a case for raising interest rates, but a case about causation in monetary policy, and on ‘timing’; which is the core of all financial transactions, transferring betweem ‘credit’ and ‘money’.

Accepted