The Australian edition of the Guardian (available via the UK website) had an article yesterday that was headlined as follows:

The author is described as 'a financier and author'. His Wikipedia page makes clear he has a fairly conventional finance background.

The article might fairly be described as an attack on modern monetary theory (MMT). He describes MMT in this way:

A state, MMT argues, finances its spending by creating money, not from taxes or borrowing. As nations cannot go bankrupt when they can print their own currency, deficits and debt don't matter. Accordingly, governments should spend to ensure full employment, guaranteeing a job for everyone willing to work. Alternatively, though not formally part of MMT, governments can fund universal basic income (UBI) schemes, providing every individual an unconditional flat-rate payment irrespective of circumstances.

These claims are wrong. They are either not what MMT says or the telling is distorted. For the record, MMT actually says is quite different.

First it is true that MMT argues that all government expenditure is funded by money creation. In the UK it can reasonably be said that this has happened since 1866 when the Exchequer and Audit Departments Act was first passed. This does not, however, mean, as the author implies, that there is no role for taxation or borrowing within modern monetary theory. In fact, the exact opposite is the case. Taxation has a fundamental role, to control inflation and, I would argue, to provide a delivery mechanism for a whole range of government social and economic policy.

Collecting taxes also fulfils the fundamental task of completing the government's promise to pay that is both printed on every banknote and is implicit within the existence of the fiat currency, where all money is simply a debt. Only accepting its own currency in settlement of tax liabilities is what provides a country's currency with its value, and so the naive presentation made by this author is completely false.

In addition, borrowing also has a very clear function, although it is entirely unnecessary for a government to borrow in theory because the government can always create money of its own instead. In practice, a government will want to borrow to provide a safe place of deposit for people within the society for which it is responsible, and it will wish to issue bonds of varying ages because these provide it with the mechanism to control interest rates within their economy.

Secondly, whilst it is technically true that any government that issues its own currency and which, most importantly, only borrows in that currency (conditions the author did not note) cannot go bankrupt it is entirely untrue to say as a consequence that governments are quite indifferent to the level of their deficit or debt. The only reason why a government would wish to run a deficit is if it had the desire to stimulate its economy because it believed that the private sector activity within it was either not delivering full employment, or was alternatively delivering outcomes that were not as socially beneficial as those which the state could deliver instead. Tax basically restricts the role of the private sector to make the more useful or socially desirable activity possible in that case. Running deficits that could, for example, lead to inflation is something that any government following the principles of MMT would wish to avoid. The author's representation is, again, then entirely false.

Third, Das is then right to suggest that a government following the principles of MMT can then pursue a policy of full employment as its primary economic goal. In fact, the only reasonable question to be asked of a government that did not understand this is why it would not wish to pursue that goal on behalf of the people of the country for which it is responsible?

Fourth, the alternative claim that Das makes that MMT says that a universal basic income can be run instead is completely false: he could search long and hard for this to be recommended within MMT literature and not find it, because most MMT academics do not think that the job guarantees that delivers full employment and universal basic income are in any way alternatives to each other. Again, then, his argument is false.

I make these points for one good reason. If you're going to criticise something you have to fairly state what that thing that you are criticising says. Das does not do that. As a consequence all that he says thereafter within his article is bound to be wrong. He is not arguing with MMT. Instead he is arguing with a straw man that he set up in place of MMT. Most of those who take argument with MMT do this, and Das is stereotypical in doing so.

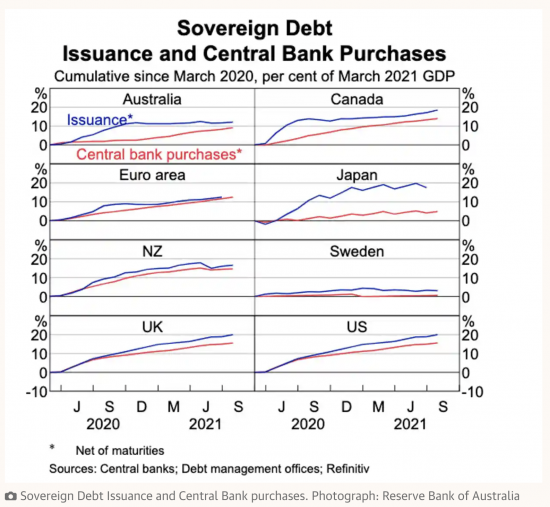

What Das then argues is that it whilst no government, according to him, follows the principles of MMT (about which is also wrong, because every fiat currency government does, as a matter of fact, do so) a great many of them have been increasing their deficit and debt since 2008. He supplies this chart to illustrate the point:

What Das implies is that this means MMT is being followed. He straightforwardly confuses it with QE. I comment further on this below. They are not the same thing.

Das then delivers another trope, suggesting:

MMT is actually a melange of old ideas: Keynesian deficit spending; the post gold standard ability of nations to create money at will; and quantitative easing (central bank financed government spending) pioneered by Japan.

If it was nothing new, what is he worried about? The fact is that MMT is new understanding but like so many others, Das wants to deny the fact. To understand why this is the case we have to look next at the claims that he makes about what he describes as the uses of MMT.

The first such use is, he claims, to direct the creation of new employment. He does however dispute that government is able to direct the private sector in this task, which makes something of a mockery of 70 years of tax-related fiscal policy, which is the actual policy most commonly used for this purpose. As for governments directly employing people to facilitate this, the opinion of Das on this is best summarised in his own words:

The woeful record of postwar centrally planned economies, where people pretended to work and the government pretended to pay them, highlights the issues.

Again using his own words, it would seem that he thinks that a government's role in employment creation is:

Getting one person to dig a hole and another to fill it in creates employment, but it is of doubtful economic and social value.

In that single throwaway casual sentence he dismisses all the value created by teachers, universities, health and social care, the justice system, environmental protection, the regulation and protection of fair competition, and so much more on which society depends, to none of which he apparently attributes are value.

Das then turns to the old trope of inflation, saying:

Second, excess government spending and large deficits financed by money creation risk creating inflation.

Of course that is true. MMT wholly recognises the fact. That is why it discusses so many mechanisms to control inflation. The only reason why he can make this claim is because he denies what MMT actually says.

Next Das claims that MMT may weaken the currency and increase the expense of servicing foreign currency debt. There are many reasons for dismissing this ridiculous claim. The first is that as we know that almost every major economy and currency has been engaged in a similar process of using quantitative easing, which Das falsely equates with MMT, there have been no major currency movements against each other as a consequence, because every government is pursuing a similar policy. To suggest that there is any currency threat is, as a consequence, ridiculous, using his own evidence. But, the fact that worldwide interest rates are now at a record low, and that this only happened during the period when QE has been in prevalent use, which happens to coincide with what he thinks is MMT, completely undermines his argument about the cost of servicing debt: if anything it is very apparent that QE has delivered the means to control the cost of debt into the hands of government, and it has no desire to let go of it. Das is, yet again, completely wrong.

Das then moves into the realms of the surreal when suggesting that whilst it is within the power of nation states to issue their own fiat currencies this is unavailable to state government, private businesses or households as if there is something wrong with that. His inability to spot the difference between macro and microeconomics is quite staggering. He is also wrong. Anyone can issue a currency. The problem is in getting it accepted. He does not understand currencies.

His complaints go on though. His next is that:

Who decides the target employment rate or UBI payment level?

Answering his own question he says:

The theory delegates management of MMT operations to politicians, rather than unelected economic mandarins. But financially challenged elected representatives may be poorly equipped for the task. Political considerations and cronyism may influence decisions.

Das is obviously quite horrified by the idea of democracy and clearly believes that corruption is something only found in the state sector. I think he should go out a little more.

Next, he complains that:

MMT may encourage hoarding of commodities. This exacerbates inequality and increases the cost of essentials such as food, fuel and shelter. Fear of debasement of the value of paper money, in part, is behind unproductive speculation in gold and cryptocurrencies.

Das is deeply confused because he equates MMT with QE. The above consequences could arise from QE, I agree. However, that is because QE injects money into the financial system without putting any control over how it might be used resulting in it being directed towards wholly unproductive speculative activity rather than into productive use. MMT is entirely different. If MMT were in active rather than passive use the government would not inject funds through the financial system but would instead take directly responsibility for the use of those funds within the economy. Consequently the claims that Das makes would not arise. The money would not be available for speculation.

He still goes on. The seventh claim Das makes is:

MMT might undermine trust in the currency. Instead of spending the payments, citizens may question a world where governments print money and throw it out of helicopters.

Once again, the simple fact is that Das has not done his research. No one associated with MMT suggests that helicopter money should be used. Milton Friedman did. Marton Wolf has done so in the Financial Times. But MMT has not. Yet again, the claim made is completely false

Finally, Das says just because Japan has used QE2 for decades without any apparent risk arising does not prove that MMT will work. I agree, it does not, because what Japan has done is not pure MMT. On the other hand it is pretty persuasive evidence and cannot be ignored, although Das would like to do so.

What does Das conclude from all this? His first conclusion is:

MMT's allure is the irresistible promise of freebies; full employment, unlimited higher education, healthcare and government services, state-of-the-art infrastructure, green energy and “the colonisation of Mars”.

How wrong can he be? MMT offers full employment for sure, because it is possible. The rest is simply made up. There is a full employment constraint, after all. That is what really limits us. MMT consistently says so. It never says anything of the sort that Das claims. I am left wondering if he has ever read anything about MMT.

Then he claims:

But monetary manipulation cannot change the supply of real goods and services or overcome resource constraints, otherwise prosperity and utopia would be guaranteed.

This one is quite fantastic. I think he will find that cutting off money supply can most definitely change resource allocation. So too can inflation; he has already said so. What MMT says as a consequence is that in that case the supply of money must be carefully managed for social purposes. Das would not seem to realise that social purposes exist.

Finally he says:

While the current game can and will continue for a time, the bill will eventually arrive. The borrowings will have to be paid for out of disposable income, higher taxes or through inflation, which reduces purchasing power, especially of the most vulnerable, and destroys savings. Other than nature's free bounty, everything has a cost.

I agree that QE has a cost. That is from the inequality and pointless speculation it induces. That is why I have argued its use is wrong since 2010. That is what led me to what I realised was MMT. That is why I argue for Green QE, which is what might be called applied MMT.

But even with regard to QE he is hopelessly wrong. QE never has to be repaid. QE has not created higher taxes or inflation, despite all the claims. And all that can destroy savings is the cancellation of QE, which literally destroys money. It is he who is the threat to savings.

What do I conclude? It is that Das is a typical underread neoliberal commentator who would appear to be driven by loathing of government, democracy, public goods and social worth, all of which radiates from what he has said. Worse though, the Guardian has given him space to discuss something about which he has little knowledge, and which he totally falsely portrays, whilst offering opinion that would be deeply detrimental to society if acted upon. What I hope is that they will publish a full rebuttal. They have a duty to do so.

_________

For another comment on this see Peter May on Progressive Pulse, who offers another perspective on this.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Das ends a with the ultimate justification for destroying the planet through unbridled growth, which is far worse than getting MMT wrong.

“ Other than nature’s free bounty, everything has a cost.”

It’s exactly this attitude: that nature is something “other” to us, that we are not a part of nature, that it can be “taken” free; that had led us to the construct an economic system, real and financial, that is destroying the planet before our eyes.

MMT is no doubt part of the solution, at least in many countries, but this changing this attitude is more fundamental.

Staggering comment, wasn’t it?

Exploitation is all in this world view

The whole article was drivel but I think that section of nature being a freeby sums up neoliberal economics and you are right, it is that mindset which is driving Global Warming and Ecological Collapse. Shocking statement.

Thank you for this superb exposition. It must be repeated many times. I celebrate the need for it, since this demonstrates unequivocally the impact of MMT. I have commented on previous occasions that you are subversive and that is indeed the way MMT and its advocates are seen. Expect to be vilified like Marxists. Game on, Richard, but it’s deadly serious.

I can take the shit

Behind the scenes I have taken a great deal this week

I only wish to comment on the preliminary remarks about the fundamental relationship between money issue and taxation, not about the whole Das discussion. I think your comments on taxation are trenchant and well made: “Taxation has a fundamental role, to control inflation and, I would argue, to provide a delivery mechanism for a whole range of government social and economic policy. Collecting taxes also fulfils the fundamental task of completing the government’s promise to pay that is both printed on every banknote and is implicit within the existence of the fiat currency, where all money is simply a debt. Only accepting its own currency in settlement of tax liabilities is what provides a country’s currency with its value, and so the naive presentation made by this author is completely false.” The last sentence provides the essence of the authority that provides the currency issuer uniquely with the capacity to demonstrate that it alone possesses the sovereign power to ensure the effective monopoly of its currency within the community.

The reason I wish to focus solely on that issue, is that neoliberalism attempts to falsify this fact; a fact that I may term the equivalent of the Second Law of Thermodynamics in physics; not a theory, but a brute fact. A sovereign power that cannot exercise that authority over its currency is simply not a sovereign power. Neoliberalism has attempted (implicitly and without formal acknowledgement); to argue that money is just a another form of private property; and failed badly, but simply refuses to accept the proof: the reliance of neoliberal markets on the operation of sovereign power to save the limited ability to survive real economic crises thay have no capacity to survive.

I am waiting for a neoliberal economist to explain 3% War Loan (issued 1914); but so far have not found anyone able to explain how Britain funded its War Effort in 1914, when Capital demonstrably failed to support the War, when it failed to buy the issue, and the issue failed. The Government continued to fund the War – technically funded by the leading “purchaser” of the Stock: the Bank of England Chief Cashier (1902-1918), Sir John Gordon Nairne. Who knew he must have been the richest man in the world? Any direction to a good neoliberal explanation for this ‘anomaly’ would be appreciated.

Thanks John

That sounds very interesting, John. Where can I find out more about the funding of WW1?

Start here

https://bankunderground.co.uk/2017/08/08/your-country-needs-funds-the-extraordinary-story-of-britains-early-efforts-to-finance-the-first-world-war/

Thanks!

That information about British war financing during WWI is fascinating. I hope to incorporate it when I next teach Modern Money Theory.

Thanks from me too, as had lost reference. The comments are worth reading; and I am puzzled that, accordingl to the maps, Ireland and Scotland seem to have contributed enormously to such purchases as were made but are not mentioned in the article

Great rebuttal btw Richard.

I too was shocked to see this – unchallenged – in the Guardian. Have you written to them?

No….

Now that my ‘business’ is more moral theology than my past in the City’s financial markets, I feel less qualified to dissect Mr Das’s argument on the grounds of economic theory. However, I would want to hear from him an explanation of how he arrives at his conclusions applying his moral philosphy, if that be a consideration at all, in arriving at his conclusions. This is a reasonable question because he has removed himself from a morally neutral position. Meanwhile, Richard, don’t let the whatsits grind you down!

Peter

I like your question

I was thankfully born fairly resilient or I could not do what I do

But it’s tedious to be engaged with by those wielding tropes that they think represent arguments

Richard

Thanks for tackling this one Richard.

There was another recent piece in the Guardian that I rather expected a comment from you about, though in this case they were broadly on side. An editorial about green finance: https://www.theguardian.com/commentisfree/2021/dec/08/the-guardian-view-on-green-finance-doing-business-as-if-the-planet-mattered

Their observation that Shell have issued a “sustainability report” claiming an ambition to become net-zero by 2050, but their accounts are constructed on the basis of business as usual, hit the nail on the head – and should be the trigger for proper discussion about how future green ambitions should impact accounting. The Guardian noticed that the company’s auditors supported them ignoring the accounting implications of planning to change their business model.

That’s for next week….

Seriously

Well, I’m really disappointed in this.

I’m actually a fan of Das. He’s extremely intelligent, engaging and well read.

His books ‘Traders, Guns & Money’ (2006) and ‘Extreme Money’ (2011) are essential reads about the culture of big finance that led up to the 2008 crash – even better in my view than anything written by Michael Lewis who just skimmed the surface. I would still recommend those books to anyone on this blog.

Das’ s account took you right inside the meeting rooms and presentations of the bankers that led to the financial crash. What marks him out for me is his obvious moral outrage at what he saw happening. He obviously thought that the sector was out of control and not really an ‘investment’ sector anymore because it was driven by short term get rich quick gains.

I think he wrote a text book on derivatives that you could buy on Amazon for a hefty fee. Das maintains (as he makes in a refreshingly honest appearance in the film ‘Inside Job’) that derivatives were never ever meant to be nothing other than ancillary functions for investment banking. With the help of people like ‘fat’ Larry Summers however, derivatives – shorn of any regulation by the U.S. SEC thanks to him personally (and this is now a matter of record BTW) – became the main banking activity which as Das points out, amplified risk in the global financial world. This led to 2008 and all that.

I had picked up however that Das was not to keen on things like state pensions and the like (his attitude was to me that they were ‘barmy’). I bought his book ‘The Age of Stagnation’ (2015) hoping for some ideas.

However, even though his analysis of the issues was as strong as ever, and that some of his prognoses would not be out of place on this blog (his notion of consuming less for the sake of the planet and all concerned) the glaring issue with the book for me was that it ended on a rather hopeless note with no acknowledgement at all for a role for the State which left me completely dumbfounded – even though they’d just bailed everyone out!!

I’m not sure whether he is neo-liberal though. I see him as an out and out liberal of the old kind – morally rigorous, intelligent and with a self imposed standard of ethics but with the rather idealist view that all people are rational and apply the same code of ethics to themselves – a major failing in my view of liberal thought (I am being consistent with myself here) with those in modern finance, economics and politics not capable of thinking like that at all. He is thus disappointed with his kind in the private sector, and rather wishes that they would behave like proper investment bankers thinking long term and offering pensions etc.

What I’d like to see happen is for progressives to engage with him on MMT; to do what the Neo-libs do and talk and influence. If Das was ‘turned’ he’d be a hell of an asset in my view.

As for the Guardian.

Well, as long as they pull stunts like this – do not allow an opposing view – I will decline to pay them as I trawl through their website for free. Tough. Let your income drop for all I care. You’re done.

They are as craven as the Labour party itself. I’d rather have nothing than some half-arsed excuse for a ‘progressive paper’. People like Carole Cadwalldr are so strong that they could survive elsewhere easily.

Sorry.

PSR, the revised edition was I believe 2010. But there was also a 2012 edition. I don’t know what is going on with this book. On a different note, no one criticizes his knowledge of micro; it is his understanding of macro, that is, nation state economics and national currency systems, that is in question. And this apperas to be problematic.

Macro befuddles macroeconomists

It’s like most accountants who have never been near a bank think that bank loans are liabilities when of course for a bank they are assets, so macroeconomists do not realise that macro is the other way round from micro

I wondered about writing to The Grauniad but didnt.

What the article highlighted is the extent to which people are making money from money and I suggest that it would help if MMT addressed Usury. As a ‘for example’ the total turnover on global foreign exchange markets is about 100 times the amount needed to cover the foreign exchange needs for actual global trade.

Not only that of course but when it goes wrong its the taxpayer that bails out the participants.

Thanks for “grasping this nettle” Richard. The article is a in prime example of obfuscation, misdirection and plain nonsense.

My imagination was gripped by his fourth concern. Is he implying that regional government, private businesses and ain citizens are unfairly left out by MMT because they are denied the ability or “right” to create their own money?

He is clearly on a mission to stoke fear in positive possibilities.

I believe Bill Mitchell’s default position is to give Das short shrift.

Bill and I agree on that

Excellent rebuttal Richard.

I have a question as I am about to start an article for rebootgb.today on UBI.

Hopefully, you don’t think it too simplistic.

My understanding is QE was started as a mechanism to stimulate the economy via Bank lending but instead the banks just (mainly) rebuilt their balance sheets with it.

Would that money have not been better spent starting UBI version 1 (since any UBI schemes will no doubt need iterations) which would have stimulated the economy directly? As well as, concurrently helping cure some fundamental ills like homelessness and child poverty?

Which would have in turn taken pressure off the demands on Social Services and the NHS?

Where have I gone wrong, please?

Better to have delivered jobs by a long way via the Green New Deal

UBI cannot save the planet

Work to deliver carbon reduction can

UBI is a mechanism for ensuring demand is maintained in the economy. We have seen a crude version of it in the job retention scheme although not universal. Where an economy creates inequality and marginalises groups into poverty then there need to be safety nets. It doesn’t have to be a universal payment but by being so it avoids the negativity and social stigmatisation of claiming benefits. It could be that a UBI scheme reduces the aggregate hours worked and pushing up demand for workers and consequently costs leaving the economy in the same place as it started or that businesses factor in the payments when agreeing wages and leaving overall income the same. The JRS didn’t have this issue because workers were forced to be idle and the scheme maintained the demand in those areas where businesses could still function without driving them out of business as overall demand fell. There would need to serious research into the potential effects of a UBI scheme.

A job creation scheme designed to reduce carbon is a good plan but also needs the ability of everyone to pay for that green energy, electric vehicles, better food produced by a greener agricultural sector, paying rent for energy efficient homes etc etc. There is no guarantee that a work programme would create the jobs for those marginalised groups and so a mix of options is required to avoid switching existing workers to a new job rather than creating new ones.

What is important is that we as a society start to do something as opposed to carrying on in the same old Neoliberal way supported by Das and others. Energy, food and climate need to be addressed on a global scale

Of citrus’s we can afford green goods

If we don’t we die

I promise you, in that case we can afford them

What we cannot afford are rents

Richard,

I agree a “Green New Deal” is the obvious way forwards. I’m not arguing that UBI is a panacea.

UBI is only one part of a package of measures to get society fixed and a jobs guarantee is part of that “package” too.

But both a Green New Deal and a Jobs Guarantee will take time to work (and get right).

A suitable safety net is needed now and could be implemented now? Plus if we start now at a lower level we can then see what is working, what is not working and iterate to get to the optimum solution quicker than if we leave it until later.

I accept testing is needed

But so too is well paid work

There is no doubt that Satyajit needs to be pulled over on this and given a ticket.

In the words of Brian’s mother (Monty Python’s ‘Brian’) – ‘He’s been a very naughty boy’ and I’m not impressed.

That, and a few books to read for Christmas – Kelton’s ‘The Deficit Myth’ and I think Christine Desan’s ‘Making Money’ for a start.

Maybe Das’ fear is that old one of being supposedly squeezed out by sovereign Government cash?

But has the financial sector he has been so fiercely critical of actually reformed? I don’t think it has.

Anyone with any common sense would that see that, and that the State has to take a lead. I remain grateful for his insights on the inside of criminal high finance but he’s blotted his copy book for me.

I hope he listens to what is coming his way.

Me too

I read reversion to type into this based on what you have said

Thanks for this Richard. Such discursions are very helpful to us amateurs like myself battling the bar-room know alls!

Thanks for saying so

i read that article in the Guardian and hoped that you would address it . Excellent article that even i can understand to a degree and well worth keeping for future references , thanks Richard.

Thanks

I am a bit in awe of this blog which often takes me to edge of despair then by patient and clear analysis prevents me falling and provides glimpses of hope. Deep gratitude for your (hopefully) indefatigable work.

Many thanks

I appreciated that comment and might share it on the blog

Perfect summary of what MMT is and what MMT is not. Thanks to Satyajit Das for making you write this, even if not his intention. Some people are obsessed with money as though it had value in itself rather than as a means to various ends.

I saw that farrago of an article and thought of you Richard. You speared it well.

He is also wrong about families. To young children on pocket money adults are currency issuers. To a 4yo 50p or £1 is a fortune. Money decreases in value as you age. Your first teenage job seems to deliver riches but you wouldn’t want to live on it.

I have to wonder who is worried about MMT since there’s been a rash of these strawman MMT articles of late. Which rich man is worried by it I wonder.

I’m not convinced that full employment obviates the need for a UBI. A UBI can do a lot of jobs and besides with full employment the cost of a UBI will be much smaller than at present. Having a right to a basic income vs our punitive benefit system has its attractions if you have ever been in receipt of benefits.

Much to agree with – including the use of ubi with a jg for full employment

That is when it really delivers

Thank you Richard for this rebuttal. I was gobsmacked when I read Das’s article in the Grauniad. It is the drivel I would expect from the Telegraph or Mail, yet a bit too high-brow for the latter. I am cancelling my subscription to the Guardian and will be telling them why. Any newspaper which does not fact check such copy joins the red tops in their egregious support for the policies which are driving us to extinction.

May I quote you in my letter of outrage and cancellation?

Of course….

Why don’t you get yourself published on this then, either in a self-published book, a proper book, a chapter in a scholarly edited book, or even better, a peer reviewed paper? Or is the whole world against MMT?

I have done peer reviewed papers on MMT

https://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwj2pb3IkuD0AhXREcAKHb8CBKwQFnoECBkQAQ&url=https%3A%2F%2Fwww.cambridge.org%2Fcore%2Fservices%2Faop-cambridge-core%2Fcontent%2Fview%2FB7A8B0C7C80C8F7E38D20BE4F5099C83%2FS1474746420000056a.pdf%2Fmodern_monetary_theory_and_the_changing_role_of_tax_in_society.pdf&usg=AOvVaw0H6sxlntqJ-OqjDvLB-RVh

That one won a prize

[…] had a number of appreciative comments for my deconstruction of an article on modern monetary theory in The Guardian, which I published in Saturday, but I admit I was especially pleased by the comment from someone […]

[…] Cross-posted from Tax Research UK […]

Das’s background as a banker perhaps explains his perspectives and prejudices. Money creation is fine as long as it is either done by the banks directly (creation money to fuel house price inflation) or distributed through the banks as in UK. Both forms feed into asset inflation which overwhelmingly benefits the wealthy who hold most of those assets, not to mention the bankers themselves. The same people who are adept at minimising their tax contributions

For Das and his kind, the idea that money creation might be used to benefit the wider economy and society is an anathema.

“The theory delegates management of MMT operations to politicians, rather than unelected economic mandarins. But financially challenged elected representatives may be poorly equipped for the task. Political considerations and cronyism may influence decisions.”

Your observation – “Das is obviously quite horrified by the idea of democracy and clearly believes that corruption is something only found in the state sector”

You pulled a sneaky move there – Das is pointing out that putting the UK’s monetary policy in the hands of elected “idiots” (as you call our politicians in another recent piece) is riskier than leaving it in the hands of unelected economists working for the State.

To claim that he is overlooking the corruption that exists in the private sector is the reddest of herrings – no-one is proposing that monetary policy be handed to private bankers? Unless you are making an oblique reference to the opaque ownership structures of some central banks?

The trouble with insisting that monetary policy be made “democratic” and rested with politicians, is that one day those powers end up being wielded by someone like Donald Trump, yes?

P.S – From what I understand, MMT proposes controlling inflation by taxing more so consumers can no longer afford to buy as many things. The low propensity to consume amongst the wealthy makes that sound very regressive?

So you are an opponent of democracy as well

Now you are on the blocked list