The McKinsey Global Institute has produced a new report on wealth. I have not read all the detail as yet - but strongly suspect I will be. Instead, I highlight the headlines because I am not sure that the authors are not as shocked by them as I am.

Take this summary paragraph:

Net worth has tripled since 2000, but the increase mainly reflects valuation gains in real assets, especially real estate, rather than investment in productive assets that drive our economies.

Take too this summary of their takeaways from the work:

- The market value of the global balance sheet tripled in the first two decades of this century

- Real estate makes up two-thirds of global real assets or net worth

- Asset values are now nearly 50 percent higher than the long-run average relative to income

- Financial assets and liabilities also grew faster than GDP, vastly exceeding net investment

- Several scenarios are possible, with an imperative to deploy wealth more productively for critical investment needs

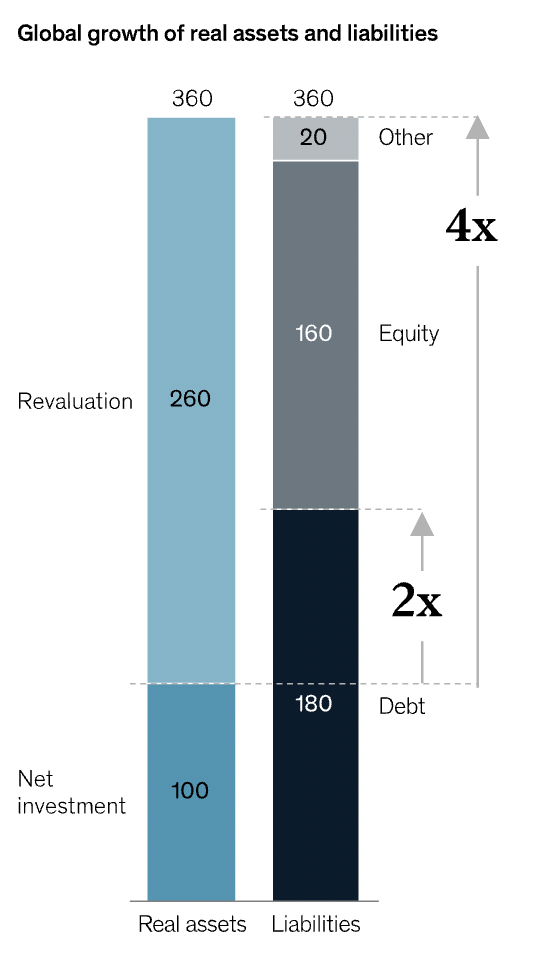

This chart is, for me, the most telling of those I have looked at, so far:

The message is simple. It is that we live in a world where supposed wealth does not come from value creation any more. It does, instead come from financial engineering. Revaluing existing assets - aided enormously by the introduction of International Financial Reporting Standards in 2005 - has permitted a boom in the notional value of wealth from which only those who already owned that wealth and those who advised them have really benefitted. In particular, the increase in debt that does nothing more than pay returns to existing asset holders has been staggering.

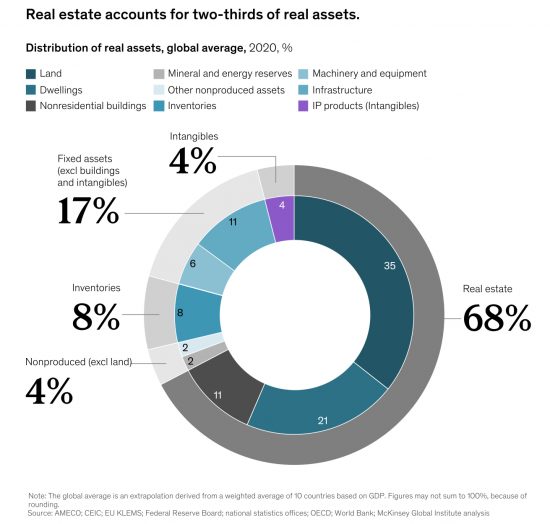

This is unsurprising when what makes up wealth is considered:

It is as if feudalism had not ended: this is a world where land backs wealth. And older generations are using that as the opportunity to leverage returns, whether from sale prices or rents, from younger generations. The evidence is that they still have ample opportunities to exploit, except for one thing.

It is as if feudalism had not ended: this is a world where land backs wealth. And older generations are using that as the opportunity to leverage returns, whether from sale prices or rents, from younger generations. The evidence is that they still have ample opportunities to exploit, except for one thing.

The question as to how much debt can be created has to be asked. This is also from the report:

From 2000 to 2020, financial assets such as equities, bonds, and derivatives grew from 8.5 to 12 times GDP. As asset prices rose, almost $2 in debt and about $4 in total liabilities including debt was created for every $1 in net new investment.

The country variations were wide, with the amount of debt created for each $1 in net new investment ranging from just over $1 in China to nearly $5 in the United Kingdom.

Leverage has gone through the roof, especially in the UK.

What to say to add to McKinsey's:

Several scenarios are possible, with an imperative to deploy wealth more productively for critical investment needs?

First, we need to appreciate this.

Second, the case for wealth taxation is overwhelming.

Third, the need for land value taxation within that wealth taxation portfolio also seems high.

Fourth, in the face of this the need for social investment is high.

Fifth, instability is built into this.

Sixth, in a world of so much need the distortion of values that the global banking boom launched by Thatcher and Reagan is horribly apparent.

Seventh, subsidies for most savings are no longer needed: we very clearly have far too many conventional savings.

Eighth, if tax and subsidised savings built this edifice so too can it build something better.

The last is my focus. Thus report makes for grim, and deeply worrying reading given the obvious instability and inappropriate focus within financing that it reveals. And yet it shows incentives work. So, we need to change the incentives.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Yes – I agree with all 8 points you conclude with.

Increased wealth (by revaluation rather than production) has blinded the elite to our real problems. It is depressing to hear “but stocks are up, and house prices are up” as a response to the problems we face… but I DO hear it!

Will your money hold back the flood? Will it make the ambulance get to you quicker?

Precisely

I found Who Owns England (Guy Shrubsole) a very enlightening read about land assets and the failed attempts over the years to catalog it.

I think wealth taxes would be very hard to enact and enforce given the powerful interests against it.

All tax is hard to enforce….

Well, all perhaps other than PAYE and NIC.

It’s the workers with little choice and power in the matter who cannot avoid their dues.

Some are easier to collect than others.

Some are fairer than others.

Peace, easy taxes and a tolerable administration of justice.

More on this please, Richard. This puts shocking numbers to a more general perception, but the key point must surely be the concession that asset values are real but useless. It’s that vital truth again that only money that circulates benefits society. Look forward to your further analyses.

Does this wealth really exist? Surely it only appears to be there because it is not realised? A bit like climate change, there will be a tipping point and it will vanish.

Banks have been allowed to create government-backed £s and $s to help buy these assets, but like Schrodinger’s unlucky cat, the money is real and not real at the same time.

When the tipping point comes the £s and $s will disappear as if they had never been created. (I see that Bitcoin is currently £48,000. A set of 0s and 1s that you can’t use for food or shelter)

The assets may exist

The values are simply current estimates

The problem is the liabilities: they remain due

“The problem is the liabilities: they remain due”

What liabilities do you refer to?

The debt shown in the graph used to pay for the assets

Having worked with and around the finance sector for a fair bit of my career and watched how its changed I have no doubt that the UK’s bloated and dysfunctional City-based financial institutions are at the root of many of the UK’s problems. Financialisation of so many areas of life, in particular in business where I’d argue that many of the problems of business – under investment in people, plant technology, R&D – reflect how they are run and directors are rewarded, driven entirely by the big City institutions. Our massively over valued property sector, driven by the flood of bank created money. Consumer debt driven by low pay, easy bank created money and a consumption culture.

Time and time again the trail leads back to the City. Efforts at regulation fail because they invariably just game the system, and probably had their people writing the regulations. Its going to need something much more profound to change. Maybe reversing the whole deregulation that happened in the 80’s. Breaking up banks into their component parts. Recreating mutuals. Ring fencing the speculative activities of investments banks from everything else. Clamping down hard on speculative trading, hedge funds and the debt models used by private equity.

Might hit the tax that the City pays into the economy but off-set by the tax that the City helps others to avoid, and the increased heath of every other sector.

Can Singapore on Thames be any clearer?

Are we going full tilt corporate fascist?

https://www.reuters.com/world/uk/shell-proposes-single-share-structure-tax-residence-uk-2021-11-15/

‘The Dutch government said on Monday it was “unpleasantly surprised” by Shell’s plans to move to London from The Hague.’

‘Consumer products giant Unilever (ULVR.L)abandoned its dual Anglo-Dutch structure last year in favour of a single London-based entity. Miner BHP Group (BHP.AX) has also called time on such a structure. read more

If BHP and Shell complete their shifts to single share structures, Rio Tinto (RIO.L), Carnival (CCL.L) and Investec (INVP.L) will be the few remaining dual-listed companies on London’s main market.’

“Among other benefits, the proposed changes will increase Shell’s ability to buy back shares,”

———-

Steve Bells take

https://www.belltoons.co.uk/bellworks/var/albums/leaders/2021/4656_161121_BIGOILSCOMINGHOME.jpg

On tv I saw over last few weeks the CEO’s of Shell & Blackrock being jolly at COPS.

I read the Washington Post is suggesting that Elites should have greater choice on who should be the political Leaders.

The feudal world are busy changing the rules themselves!

Why are you always saying that older generations exploit the young, particularly with regards to property?

My children’s houses are worth far more than mine. Yours, in Ely, is probably worth twice as much.

Where do you put yourself on the scale? Are you older or younger? Do you exploit your children?

You really cannot extrapolate from personal situations to the general

As you must be aware, relative to earnings House prices are vastly higher now than when you were young, and the likelihood of buying lower, the duration of the mortgage longer and the chance that inflation will repay the debt lower still

Of course we exploit the young

Great post.

And look at the debt?!!

I think that we are looking at the biggest mis-allocation of resources in world history since Thatcher and Reagan.

The first flat we bought cost £2750 and my husband earned £520 a year. That was because the company he worked for lent us the money for a deposit and gave him a payrise so he could pay them back.

If you had said many older people exploit the young, I wouldn’t have argued, but you imply that everybody does. Lots of the elderly in the North East are exploited themselves. They can’t exploit the young because there is no value in their houses.

You say I can’t extrapolate from the personal to the general, but you are generalising about older generations. What I am saying is that we are not all exploiting the young because we don’t all have the financial clout to do so. I can’t help taking it personally.

Perhaps people like me shouldn’t read your blog as then we wouldn’t get upset at being lumped in with millionnaires. But then I wouldn’t be able to try and convince people about universal basic income or different monetary theories.

If you wish to play semantics say so, because we do them at least know what you are doing

Not playing semantics at all. I am genuinely upset at the idea that I might be thought to be exploiting the young, along with all the other pensioners I know.

I’ll just leave it at that.

OK

Accepted, but I did not read that into your original comment

Sorry

[…] I noted very recently, two-thirds of the world’s national financial wealth is invested in land. Since 2000 that […]