Two articles in the FT this morning make clear that the issue of climate change and accounting is not going away. This is the headline of the first:

And this the headline of the second:

The articles appear under different headings, but the message is the same. It is well said in the second:

The expected launch this year of a sustainability standards board by the IFRS Foundation, which oversees international accounting standards, should make ESG reporting more consistent. But for now investors are suffering from a shortage of meaningful data by which they can track progress and dissuade executives from fudging the numbers if they miss their targets

The message is simple, and is that accounting is very far behind the needs of society, investors and business on this issue.

But, worse, there is an assumption within these articles that now that the International Financial Reporting Standards Foundation has decided that it will set up a Sustainability Standards Board, despite objections from many readers of this blog (who between them provided sixteen per cent if the comments sent on this issue last December) then this is the way that we must go.

This proposal cannot answer the issue being raised. The IFRS proposal is to create sustainability standards outside the accounting standards framework. That is why they want a new, separate, board. By definition this is wrong. This perpetuates the myth that climate change is peripheral, and an externality as far as business is concerned.

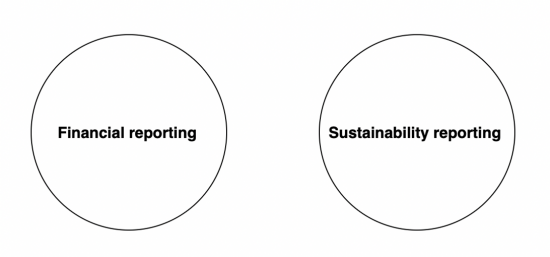

The IFRS view would seem to be that financial reporting and sustainability reporting are unrelated issues:

That is not true. Climate change is at the very core of business concern now. It is all that business should be about because unless a business can now embrace climate concerns it is no longer a going concern, and determining whether a company is a going concern is the core issue within financial reporting. This means that the required view is this:

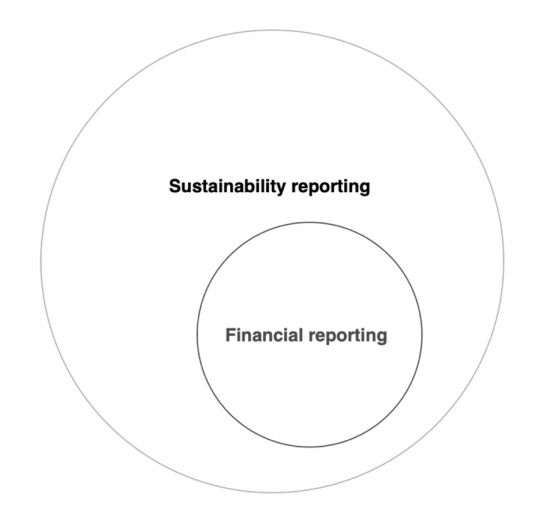

Sustainability reporting should actually encompass financial reporting and not the other way round.

Sustainable cost accounting, which I propose, does that. Only if we put climate change very firmly on the balance sheet will we get the change we really need in accounting.

I am pleased to say that I am reporting this opinion at a seminar at the Institute of Chartered Accountants in England and Wales to discuss this issue next week.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“Reporting Standards Foundation has decided that it will set up a Sustainability Standards Board, despite objections from many readers of this blog (who between them provided sixteen per cent if the comments sent on this issue last December) then this is the way that we must go.”

Because IFRS, a global organization with thousands of experts directly or indirectly involved has to listen to the ramblings of a self-appointed expert and the readers of his blog? Because they spammed the consultation?

My guess is IFRS took one look at what you were proposing, realized it was window-licking crazy and put it in the trash where it belongs.

Which is why the ICAEW is promoting a seminar on it?

Good luck with this – it is the right way forward in my view.

I also posted a link to this blog post on the SBFG Facebook page this morning along with this following commentary……

“In a second post on Tax Research this morning Richard Murphy discusses another vital issue – corporate accounting standards. Richard has been campaigning on this for ages and it really is highly relevant for this group. Allocation of capital to companies has to take into account what environmental and social impacts corporate activities have and their future plans will have. We must avoid allowing public money and public savings being allocated for harmful purposes and this is why this issue is a vital part of what we need to be thinking about and campaigning about.

I was one of the readers of Richard’s blog who submitted a response to the IFRS consultation exercise – and along with many others our views have just been ignore by the powers that be.”

Thanks Jim

I will do some content soon

[…] which companies are likely to be most impacted by the transition to a sustainable economy. From an investor perspective this is vital, and yet this is not what the International Financial Reporting Standard Foundation is proposing to […]

Has to be the right way round to think about sustainability and conventional accounting.

It does beg the question of who are the right people to be conducting the ‘audits’ and sustainability reports. Is it the existing audit firms? Widening their ‘consultancy’ services ever further. Do we need a different kind of organisation to conduct sustainability audits and then how would we pull the financial and sustainability elements together?

We need entirely new. independent, audit firms who do nothing else