George Turner of Tax Watch UK published a paper and made a claim at an event yesterday that tax evasion is the same as tax avoidance, and both should be considered to be illegal. I regret to say that this is decidedly unhelpful. The reality is that behaviourally the difference between tax avoidance and tax evasion are very different.

As I wrote this about tax evasion in a recent, as yet unpublished paper:

Tax evasion arises in a number of situations. One way in which it occurs is when the misrepresentation that a tax relief is being appropriately used becomes so extreme that actual misrepresentation takes place. That misrepresentation of the truth is as much tax evasion as other forms of that activity are.

More generally though, tax evasion involves the deliberate falsification of a declaration relating to a source of income to escape claims arising that the tax due on it should be settled. This suppression of data might include:

- Deliberately understating the value of a source of income on a tax return;

- Omitting a source of income from a tax return;

- Omitting to make a tax return at all;

- Making sure that the income or other tax base that might give rise to a liability is recorded in an entity whose existence can itself either be hidden from view (e.g. it is in a tax haven and ownership data concerning it is suppressed) or it can be dispensed with before tax is due (e.g. a limited company that can be deliberately dissolved without the means to settle its tax liabilities, or even the records to show that they might exist);

- Over claiming a tax relief, allowance or expense on a tax return when the conditions to claim that relief have not been met e.g. the expense has not actually been incurred.

Evidence suggests that tax evasion is considerably more commonplace than tax avoidance in countries, whether so-called developed or developing economies are considered.

In other words, there is falsification here. In contrast, I said of tax avoidance:

If a taxpayer arranges their affairs in a way specifically allowed or encouraged by tax law (for example, they pay part of their income into a pension fund and save income tax) they are not avoiding tax, even though they may pay less tax as a result. If the law permits this activity and the taxpayer reduces their income by paying it into a pension (which is very likely to mean that they defer their right to enjoy the income in question,) then this would not qualify as tax avoidance. In such a case, presuming all rules had been complied with and all required evidence is supplied, a tax authority would be obliged to provide the relief the law encourages.

This does not necessarily mean that the outcome of this activity is desirable or socially useful, but thje critical point is that tax avoidance is not about the use of tax reliefs, allowances and exemptions in the way that a government prescribes. The cost of that activity belongs in the tax spend/ expenditure gap. Tax avoidance is more complex than straight forward use of reliefs.

The UK's HM Revenue & Customs notes[2]:

"Tax avoidance involves bending the rules of the tax system to gain a tax advantage that Parliament never intended.

It often involves contrived, artificial transactions that serve little or no purpose other than to produce this advantage. It involves operating within the letter, but not the spirit, of the law."

In that case much of tax avoidance is about the abuse, or manipulation of tax expenditures. Doing so remains strictly within the law, meaning that the taxpayers undertaking this activity are likely to avoid a penalty for their actions, and yet they are falling within the realm of tax avoidance. Examples of tax avoidance might include:

- Incorporating a company simply to take advantage of lower corporate income tax rates than they would pay on personal income, subject to income tax rates;

- Seeking to recategorise income as capital gains to take advantage of lower tax rates that are often charged on capital gains, if they are subject to tax at all;

- Seeking to recategorise income arising from work as income derived from investment to avoid higher rates of personal income tax often due on earnings from labour as a result of social security charges and payroll taxes;

- Seeking to represent income arising within a country as income arising from outside it to defer or cancel tax arising on that income;

- Suggesting a trade exists to claim an expense deduction that could not be offset against employment income;

- Shifting income and assets into tax havens and charging for their use to related operations in higher tax jurisdictions to reduce the overall level of corporate income tax due within a group of companies;

- Changing the nature of a sales transaction to apply a more favourable sales tax rate or exemption to that transaction.

I then offered an explanation of what avoidance is using the work of tax barrister and tax justice campaigner Claire Questin, saying:

The mechanism to differentiate these behaviours has been defined by UK based tax barrister David (now Claire) Quentin[3]. If there is no risk of the transaction being challenged by a tax authority - because it is tax compliant - then even if it reduces the amount of tax to be paid by a taxpayer it cannot be tax avoidance because it is wholly within the spirit of the law. In these circumstances the tax saved would be a consequence of a permitted tax expenditure.

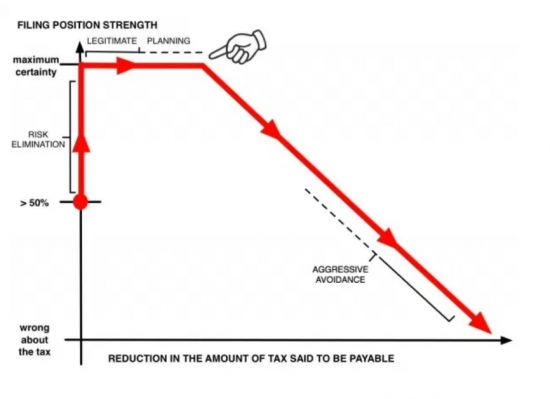

This is explained in this chart from Quentin:

A person who is uncertain of the law is represented by the red circle on the vertical axis. If they take advice from their tax authority or a professional tax advisor they might considerably reduce their tax risk by increasing the certainty that their affairs are legally compliant: this explains the red line up the Y, vertical, axis. They might then make certain other choices that reduce the amount of tax that they might pay that are also legally certain e.g. they might pay into a pension or claim permissible tax reliefs for expenses that they have actually incurred. Both are permitted if relevant rules are complied with, and less tax is paid as a result. This explains the horizontal red line across the top of the chart.

However, a point is then reached where further reduction in tax paid is not possible without uncertain tax positions being adopted of the types noted previously: e.g., a transaction is represented as something that it might not be, or which is at least open to either legal or factual challenge. This is where the line begins to slope downwards.

Thereafter, uses are made of the law which are clearly open to doubt as to their legal validity: many marketed tax avoidance schemes are of this type.

The inflection point where tax expenditure becomes tax avoidance is clearly marked by the pointing finger on the chart. As a person descends down the slope on the right-hand side of the chart the uncertainty in the position that they have adopted increases until what is described as aggressive tax avoidance is being undertaken.

It is thus risk that differentiates claims that are part of the tax expenditure gap from tax avoidance. If there is a risk that the transaction might be challenged by a tax authority because the use made of the law is not obviously compliant with the spirit of that legislation, or because risks in the interpretation of that law have been knowingly taken with the aim of securing a tax advantage, or because the facts that supposedly underpin a claim do not truly represent the economic substance of the transactions that have actually been undertaken, then the behaviour in question is tax avoidance.

So, tax advantage involves risk-taking in three ways. One is with regard to the law. The second is with regard to being found out. The third is that the chance taken with the facts is so great that the issue tips into tax evasion.

Both evasion and avoidance do of course result in tax loss. But are they the same as George Turner claims and that, as he suggests, avoidance should result in a criminal investigation and prosecution? I think not. I am afraid George Turner is carried away by his own premise that:

Much of the focus of investigative journalism over the last ten years has focused on tax avoidance.

And it is held as an article of faith by many journalists, politicians and society more widely that there is a clear dividing line. Tax avoidance is legal, while tax evasion is illegal.

As Claire Quentin, and anyone who has worked in tax (which George Turner has not) knows, such clean-cut divides do not exist. Many things in tax are grey, unless one exercises so much caution that no claims are made - and that is clearly not what the law intends. So judgement has to be exercised. Of course some will abuse that. But is to criminalise judgement right? Of course it is not.

George Turne makes a category error, largely with regard to motivation. What he is assuming is that because tax may not be paid in both cases the activities are the same. That is akin to saying manslaughter and murder are the same because someone dies in both cases. Clearly they are not the same. And the distinction is essential, both to ensure a prosecution and to ensure that the sentence is right.

That's exactly the same in the case of avoidance. Avoidance does not necessarily mean a person goes free of liability. They can be made to pay the tax. They can be made to pay interest. They can pick up penalties for a lack of care. Those can be significant. And rightly so in some cases. But if criminality was required to be proved I strongly suspect none of that would happen: the case would very often not be proven to that standard and tax would not be paid, even if it would be as non-criminal avoidance. I presume that is not what George Turner wants. Nor would I. And so I do want a variety of definitions and means of redress to ensure that tax compliance can be assured, where tax compliance is seeking to pay the right amount of tax (but no more) in the right place at the right time where right means that the economic substance of the transactions undertaken coincides with the place and form in which they are reported for taxation purposes.

I would suggest that George Turner's crude attempt to lump these issues together for legal purposes will not help. this. By all means call both tax abuse. Both are that. But don't, please, suggest, that the chance of making redress be hampered by setting the wrong criterion for remedy to be effective, which is what is being suggested.

------

[1] https://www.cambridge.org/core/journals/social-policy-and-society/article/modern-monetary-theory-and-the-changing-role-of-tax-in-society/B7A8B0C7C80C8F7E38D20BE4F5099C83/core-reader

[2] https://www.gov.uk/guidance/tax-avoidance-an-introduction

[3] http://jota.website/article/view/142

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Dear Richard,

As I explained in my email earlier, I don’t believe that George argues “that tax evasion is the same as tax avoidance”. His position, which I agree with, is that tax evasion and tax avoidance are different forms of tax fraud or cheating the public revenue and should be treated as such. So, that does not detract from your proposition “that behaviourally the difference between tax avoidance and tax evasion are very different” and is therefore not “decidedly unhelpful”. To the contrary, the most effective way to counter tax avoidance is to treat it as the fraud it is, which is precisely what George is arguing.

I agree with George because, as you know, my doctoral research was on ‘Cheating the Public Revenue: The Nature and Meaning of ‘Tax Avoidance’ and ‘Tax Evasion’ in English Law’.

The basic starting point is to understand that the terms ‘tax evasion’ and particularly ‘tax avoidance’ are not legal concepts but classic examples of what are called ‘legal nonsense’ in jurisprudence. The three legal concepts which cover every tax behaviour are: (a) cheating or fraud or dishonesty; (b) negligence or carelessness or failure to take reasonable care; and (c) honesty, which can be honest compliance or honest non-compliance because of ignorance or error. Every tax behaviour must fall within the fraud-negligence-honesty trichotomy, depending on the knowledge, abilities and circumstances of the taxpayer and any professional adviser involved. The legal question raised by the terms ‘tax evasion’ and ‘tax avoidance’ is, therefore, where they fall under the fraud-negligence-honesty trichotomy.

The next important point of law is the recognition that cheating the public revenue or tax fraud, like general fraud, is both a criminal offence and a civil wrong. So, there is the crime of cheating the public revenue (which corresponds for tax purposes to the crime of fraud under the Fraud Act 2006) and the tort of cheating the public revenue (which corresponds for tax purposes to the tort of deceit). Like general fraud also, cheating the public revenue can be used as a defence in civil proceedings, which is essentially what the Ramsay principle does. Just as a general fraudster can be prosecuted by the authorities using the criminal law and be sued in a civil case by the victim using the civil law, the Revenue have always had the discretion to apply the criminal and civil law to all forms of tax fraud including tax evasion and tax avoidance.

TAX EVASION is cheating the public revenue or tax fraud by a taxpayer who deliberately or fraudulently fails to make a return of the relevant liability or who deliberately or fraudulently makes a false return of the return without using a tax scheme. This type of fraud is fraudulent concealment. Tax evasion has been used in legislation to describe this type of cheating the public revenue or tax fraud but this does not make it a legal concept because a legal concept like fraud is one that applies to all forms of fraud, not just one form.

By contrast, TAX AVOIDANCE is a conspiracy to cheat or defraud the public revenue by the professional advisers that devise, market, implement and otherwise facilitate the use of tax schemes (‘the professional enablers’) in which the taxpayer using a particular scheme to misrepresent his tax liability in a return submitted to the Revenue (“the participating taxpayer”) may or may not be complicit. The liability or complicity of the participating taxpayer is not a requirement for cheating the public revenue or tax fraud in criminal and civil law. The general principle is that if a taxpayer relies on professional advice in relation to his tax affairs he will not be liable for negligence or fraud if the advice proves to be wrong. Therefore, a participating taxpayer using a tax scheme (which is invariably devised, marketed and implemented by professional advisers usually with the benefit of the ‘blessing’ or legal option of leading counsel) to misrepresent his tax liability in a tax return submitted to the Revenue is more likely to do so innocently rather than negligently or fraudulently. This type of fraud is fraudulent misrepresentation but it is caused by the professional enablers rather than the taxpayer who may have misrepresented his tax liability honestly by relying on professional advice.

Much of the confusion in understanding the meaning of tax avoidance in law is the tendency to focus solely on the intent of the participating taxpayer rather than the professional enablers. I’m afraid that this misconception is evident in your analysis.

As I stated above, the Revenue have always had the discretion to apply both the criminal and civil law to all forms of tax fraud. According to HMRC Criminal Investigation Policy (https://www.gov.uk/government/publications/criminal-investigation/hmrc-criminal-investigation-policy): “It’s HMRC’s policy to deal with fraud by use of the cost effective civil fraud investigation procedures under Code of Practice 9 wherever appropriate. Criminal investigation will be reserved for cases where HMRC needs to send a strong deterrent message or where the conduct involved is such that only a criminal sanction is appropriate.”

HMRC does not acknowledge it but this policy applies to both tax evasion and tax avoidance because they are both tax fraud. Like the former Inland Revenue, HMRC often applies the criminal law to taxpayers engaged in tax evasion and the civil law to taxpayers involved in tax avoidance hence Dennis Healey’s comment that the difference between tax evasion and tax avoidance is the thickness of a prison wall. In other words, the criminal law punishes the fraudster (by imprisonment) while the civil law unravels the fraud (which is essentially what the Ramsay principle does in tax avoidance cases). This administrative approach is also a consequence of the way the tax system works in the sense that in tax avoidance the taxpayer buys the tax scheme from the professional enablers, misrepresents his true tax liability on the basis of the scheme, the Revenue rejects the misrepresentation and demands the true tax liability, the taxpayer then appeals to the civil courts or Tribunal. The missing link in the civil side are the professional enablers that masterminded the fraud. So, the only way to implicate the professional advisers in tax avoidance is by applying the criminal law.

George’s argument is simply that HMRC has the discretion to apply the criminal law to the professional enablers of tax avoidance and should be doing so in order to deal decisively with the source of the problem and he is absolutely right about that both as a matter of law and as a matter of HMRC’s policy.

Osita

I gather George’s argument is your argument.

And I rather think I have answered the pints in my second blog on this issue – which expands my theme.

But as I said in a mail to you, two pahreses jumped out when reading your argument. Thet are ‘Serious Fraud Office’ and ‘Faukure to secure a prosectution’, which is where all this would lead. Cheating is immensely hard to prove, even with recent legal changes.

I set out a simpler, more effective way of addressing this that is objective.

And it also has massive =behaviuoural benefits whereas cheats who know securing prosecution for fraud is very hard will run their hands in glee at the approach you and Turner propose.

We will have to disagree on this.

I have not got time to discuss it further, but I am quite certain tax justice would make a big mistake folllw9ing George Turner down this dead end.

Richard

My view on this is that tax evasion does exist, but we should immediately stop using the term tax avoidance and replace it with tax abuse as that is what avoidance essentially is, finding ways to abuse the law and harm people as a result. The UK is committed in human rights Institutions and structures, let us solve the threshold there on acceptable tax abuse, I suspect the threshold is very low (some informal sector Issues of abuses done due to very poor lawmaking or practice).

Tax avoidance is too neutral as a term, too nice for what it is, tax abuse says what it is i.e. ways that were never intended by lawmakers, that benefit the taxpayer but hurt others especially those with less power or more reliant on public services. Abuse is a rights based term, used by UN human rights rapporteurs, Treaty bodies, and so it has a better grounding than avoidance – a term invented by the marketing departments of enablers of tax abuse and also then adopted by OECD BEPS as a way to describe the phenomenon.

There is also legal use of tax incentives and credits as intended by law, like those pensions and ISA relief you mention, they are democratically established and can also be reversed if opinion shifts. Tax abuse, however, was never intended (or maybe it is in some places, but not officially so), and measures to fight it often require international co-operation, at times sanctions.

Call it abuse if you wish

But don’t conflate it with evasion, which is different

That’s my point

Tax avoidance is cheating. Nor is it legal

Tax avoidance involves taking steps to secure a tax advantage never intended by parliament. This means avoiding the intention of the law – hence the name ‘tax avoidance’. And if getting round the law (because to avoid something is to get round it) is not cheating then I am not sure what is.

There is a problem that tax avoidance is not necessarily legal, and no one can claim it is. It may not be illegal, but that’s a long way from being legal.

There is no simple black and white dividing line between legal and illegal. There is a massive grey area between the two where no one can be sure whether things are right or wrong, legal or illegal, permitted or unacceptable.

The uncertainty means no one can be sure that tax avoidance is legal, because by definition it has not been permitted by law, so that claim cannot be made.

And the decision to work in this grey area of uncertainty is a deliberate one that reflects a decision to free-ride the system knowing that this may create an outcome never intended by law and of uncertain legality.

Hence a variety of definitions, and means of redress should be made available.

See my next blog to develop this

[…] would seem that I walked into another minor hornet's nest when tweeting, and then blogging, about Tax Watch UK director George Turner's suggestion that the distinction between tax evasion […]

I heard an interview on the radio a few years back with a top business accountant on this subject. He said his job was to find a way to “legally” reduce his clients tax burden. He illustrated the task by comparing the job to finding the best road route from say Liverpool to London. Occasionally HMRC would set up a new road block on one particular road, which to him just meant having to find a new alternative route.

I quiet liked the analogy and it maybe helps explain how tax avoidance is.

For me this all boils down to having better regulation – the possible evening up of tax rates on e.g. CGT will assist, as perhaps a reduction in employment taxes.

I have also, in the light of Grenfell revelations regarding the fraudulent fire safety claims of cladding suppliers, been wondering about the possibility of suing such companies for compensation. My ‘non thought through’ idea includes, if a company diverts profits to tax havens, there exists a nexus between what might be a limited liability company (the end supplier who could go bust) and head/group/holding companies – opening up the prospect of being able to obtain redress right into where profits may be stashed.

The core of tax evasion is fraud and dishonesty – typically involving someone lying or fraudulently misrepresenting the facts. But in most cases HMRC is much more interested in threatening prosecution to secure a favourable financial settlement, shaking the tree very hard to see what falls out rather than sending a message by sending someone to prison.

Tax avoidance is a much more slippery beast, and a bit of an etymological chamaeleon. Either the tax planning works or it doesn’t. And the plain fact of it is that people will take reasonable steps to rearrange their affairs to reduce the tax they pay if they can do so, from taking dividends rather than salary, to holding investments that produce capital gains rather than income, or making larger pension contributions to investing through ISAs or SIPPs rather than directly in the underlying assets.

In the quote often attributed to Denis Healey, “The difference between tax avoidance and tax evasion is the thickness of a prison wall.”

On a side note, the earliest I can find someone saying this is Joel Barnett – later the inventor of the Barnett formula – in his maiden speech in 1964 – https://api.parliament.uk/historic-hansard/commons/1964/nov/11/5-tax-rebates-for-exports – engagingly talking about the “shocking waste of human resources” of accountants “dealing with taxation problems instead of being engaged on the more fruitful task of helping companies to increase their productivity and efficiency”. But those were in the days before Ramsay and later cases which relegated the Duke of Westminster case to insignificance save as a footnote on legal history. Since BMBF and SPI, the courts have all the tools they need to view facts “realistically” and legislation “purposively” to achieve the result they want.

As I said, HMRC have had impressive rates of success. Tax avoidance is now a mug’s game. But it is very different from tax evasion.

[…] saying that the characterisation I have made of George Turner's comments to a meeting yesterday, on which I have commented, is unfair. He has objected to the underlined words […]