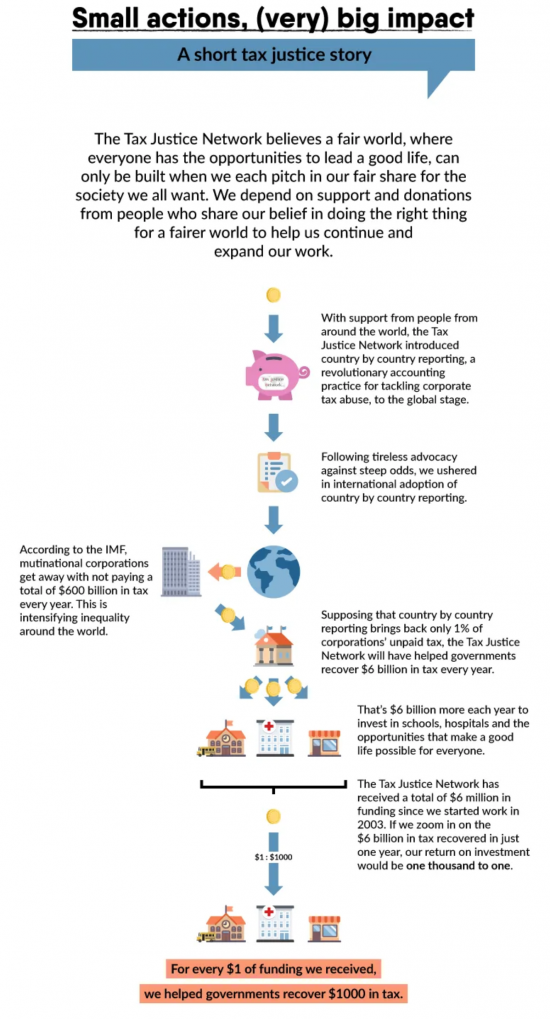

The Tax Justice Network has an infographic on its blog about its work and a new funding scheme it is launching. I wish it well.

One part of the infographic is this:

The story is true. But I was paid nothing as the creator of country-by-country reporting.

I fully admit that I could not have made it happen: it took many others in many organisations, including Tax Justice Network, to make that happen. And I am delighted by the rate of return, however approximate the measures. The couple of days it took in 2003 to get this ball rolling were time well expended.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Just out of interest, how many enforcement actions and what sum of money has been recovered by country by country reporting?

You know that is not the way corporation tax works, I presume?

I am well aware of how corporation tax works.

Just answer the question above. Has country by country reporting been directly used in any tax case, and if so how much money was recovered?

You clearly do not understand how it works

The answer is we will not know until a case goes to court and none have yet

So, very politely, you are making false claims and looking for evidence in the wrong places

The evidence will come from better profit allocations over time

“The answer is we will not know until a case goes to court and none have yet”

Congratulations. You have finally managed to answer the question – correctly. No enforcement actions have been taken on the back of information provided by country by country reporting. I can also inform you than none are pending within the EU at least.

“So, very politely, you are making false claims and looking for evidence in the wrong places ”

I haven’t made any claims. The only people making claims are yourself and the Tax Justice Network. I quote “For every $1 of funding we receive we helped governments recover $1000 in tax”. They work this out by “supposing” country by country reporting brings back tax. There is no evidence for this. By your own admission no cases have gone to court and there have been no enforcement actions.

“The evidence will come from better profit allocations over time”

Is there any hard evidence this has happened to date? Real, quantifiable evidence, not just claims by the TJN.

There is substantial data that shows there were gross profit misallocations

And clear evidence of changed behaviour by some banks

There are now quite a number of studies on this issue – I have one out soon

When we have OECD data over time – and right now we have one – we will know more

But the reality is that you give your own situation as someone who has npt the slightest interest in an objective answer with your last comment

And I will also add that your claims that there are no actions is simply wrong – you cannot know. As a matter of fact you are making a false claim.

I suggest that you stop making false claims and realise that the evidence will always be behavioural

I wonder though, do you know what that means?

“There is substantial data that shows there were gross profit misallocations”

If that were the case, where are the enforcement actions?

“And clear evidence of changed behaviour by some banks”

Could you provide this evidence? I have yet to encounter a bank which has changed anything at all due to CbC.

“There are now quite a number of studies on this issue — I have one out soon”

Again, I’d be interested to see which studies you are referring to. The ones I have seen (and worked on) with BEPS/OECD show nothing of the kind.

“But the reality is that you give your own situation as someone who has npt the slightest interest in an objective answer with your last comment”

I am very interested in being objective. CbC reporting hasn’t achieved anything thus far – objectively. It is also well understood that it does not provide the necessary information to make any pronunciation on the tax paid by a company being correct or not.

“And I will also add that your claims that there are no actions is simply wrong — you cannot know.”

Well, other than you yourself saying there have been no actions, the EU have also said exactly the same thing. As far as I am aware there are no actions pending either. See above for the reasons why.

“I suggest that you stop making false claims and realise that the evidence will always be behavioural”

Again, evidence please. You and the TJN just saying it is a massive success doesn’t mean anything – especially given your hardly unbiased position and track record on the matter.

You can use Google as well as me

And if you want to look at changed behaviour look at Barclays – there the allocation change hass been dramatic

Or Vodafone (yes, Vodafone)

And no one ever said there would be actions – they’re not needed – the behaviour is changing

And very clearly you’re looking in the wrong places

But no, I won’t do your Google research for you – wait until my paper comes out and you can work your way through the literature if you like

In the meantime – if you think we’ve failed you have a weird view of failure. I call changing the law in 70 countries and having the EU Parliament and Commission wanting this a success. But you clearly use a different criteria

And I am not debating this with you again

Jeremy won’t believe you until he sees the blood of billionaires running in the gutters. 🙂

Let’s hope it doesn’t come to that.

I can indeed use Google.

Having looked at Barclays CbC reports (which the publish annually and are available on their website or via a google search) it doesn’t look like any behavior has changed at all. If anything the trend is that the amount of Corporation tax they pay has gone DOWN.

Likewise Vodafone (who voluntarily publish CbC reports) don’t seem too bothered by it either – according to UNCTAD at least. It hasn’t changed any behavior or alleged profit shifting at all.

So it very much looks to be that the behavior isn’t changing, and there are no enforcement actions because CbC is not enough on it’s own to challenge a company’s tax on a legal basis.

You may well have got the EU to change the law, but it hasn’t achieved anything in and of itself. as the EU and OECD have acknowledged, because it doesn’t give information viable for successful action.

Which rather begs the question: why bother?

I eagerly await your forthcoming paper. Where will it be published and who will be reviewing it?

The Nordic Tax Journal

Are you not aware that peer review is anonymous?

I despair….

You really do not have a clue what you are talking about – as is also evidenced by the fact you have clearly not looked at the behaviour of eother company

Putting aside the success or otherwise of country by country reporting..

I query your assertion that it is your work and tour brainchild…if it was down to you it would indeed be a magnificent achievement as the UN’s commissioned ‘Group of Eminent Persons’ drafted far reaching proposals which would have required large companies to publish data similar to country by country reporting in 1973. I presume when you were at school Mr Murphy as you were 15!!

Later the UN convened a Group of Experts on International Standards of Accounting and Reporting (GEISAR) published recommendations which contained the requirement to publish financial reports for each company that a multinational corporation operated, not dissimilar to the ‘concept’ of CBCR and these recommendations were made in 1977.

And the International Accounting Standards Commission published a draft International Accounting Standard (IAS14) which was a standard aimed at financial segment reporting by geographical area, again very similar to the ‘concept’ of CBCR. That was in 1980.

If you, Mr Murphy, did create the “entirely new concept”, it’s a shame that you waited until 2003 to first publish your proposals! How do you account for that?

If you had read those proposals you would know that they are not in the form that CBCR took from 2003 onwards

And you would also know that they had been well and truly forgotten by 2003

I was also, like everyone else, wholly unaware of them

And as everyone involved in actually delivering CBCR acknowledges, the form in which is happened was that which I suggeted and the reason why it happened was because I suggetsed it, which was then picked up by others

Your suggestion is akin to saying da Vinci actually invented the helicopter. No, he didn’t. That he sketched something like it did not alter the fact that someone else had to actually invent the real thing, and they would have done so without his sketch

So my response? You’re reproducing data you only know because tax justice researchers found it and they do not agree with your false interpretation of it

And I suggest you get a life doing something better than negatively nitpicking for no gain to anyone

Goodness me Richard, you don’t half have to put up with some shite!

Keep up the good work.

Your detractors I’m afraid do not know the difference between self-aggrandisement and the effective campaigning you do – more’s the pity.

Shite happens!

Forgive me, but I’m a bit confused

Assuming the 1% recovery of the unpaid tax…”That’s $6bn more each year to invest in schools, hospitals….”

How does this square with the statement that “the reality is that tax does not fund government spending” (Reasons to Tax 3/1/18 https://www.taxresearch.org.uk/Blog/2018/01/03/the-reasons-to-tax/) and the six functions of tax?

I’m not trying to be awkward here; I genuinely want to understand, especially as I’ll be leading a discussion on six functions of tax in a couple of weeks!

Most of Tax Justice Network does not agree with me on modern monetary theory

Simple answer

I keep reminding them but they ignore it

I think the six functions is right

They only do the last 4

BF says:

“Forgive me, but I’m a bit confused”

Well you’re not alone there 🙂

“the reality is that tax does not fund government spending”

I might be missing the point here, but the reality is that government policy doesn’t work on reality, it works on the convention of imperfectly matching government spending with tax receipts because that is how it has always been done.

Since e’en as we speak we are still teaching classical (non MMT) economics in universities it will take a while before this fantasy world gets real. In the meantime we put up with trying to make tax and spend doctrine do the best it can.