I am presenting evidence to the EU Parliament's Tax3 Committee this morning on VAT fraud. In advance of the hearing the Committee asked for my written submission on a number of issues. These were the comments I supplied. I will publish my notes for the oral evidence I will submit separately:

TAX 3 Hearing

Vat fraud

Questions

Presentation by Professor Richard Murphy[i]

‘How come that a solution to tackle VAT fraud could not be found?'

1. Can you present the latest development of VAT frauds? Can you shortly present a typology of VAT fraud?

In brief VAT fraud exists in four forms:

- By far the most commonplace type of VAT fraud arises from the suppression of data on the existence of domestic trade. This is, in other words, the consequence of the shadow economy. The data in question relates to real trades, the vast majority of which will be domestic, which are not declared for the purposes of any tax. A note on the scale is attached as an appendix.

- There is taxpayer neglect. This is not criminal. It is tax not paid as a result if taxpayer mistake and omission. It is fraud because the taxpayer is indifferent to the gain that they might make as a consequence of their neglect. Such errors can be in favour of the tax authority as well as at their cost, but the latter appear to be more commonplace when such errors are tested, as they have been by HM Revenue & Customs in the UK[ii]. In the UK it is estimated that 10% of tax losses arise for this reason: a separate figure for VAT is not published.

- There is criminal fraud. This represents, deliberate, organised fraud of which the most common element has been missing trader fraud. In some countries this appears to have been reduced, and in the UK now represents less than 4% of the VAT gap[iii].

- Other fraud. The most common is believed to relate to relate to distance selling. In the UK the estimate of losses ranges from £1bn to £1.5bn per annum, or between 8% and 12% of the VAT gap[iv].

It is estimated in the UK that 13% of the total VAT gap arises from bad debt and less than 1% is due to tax avoidance[v]. Taken together these estimates imply that suppressed data from trade in the domestic shadow economy may, in the UK, contribute 62% of the VAT gap, which is the difference between VAT theoretically due and that actually paid. A word of warning should be added: as the table attached as an appendix to this note shows, the UK has one of the smallest shadow economies in percentage terms in the European Union. It is entirely possible that other countries may suffer higher rates of loss to the shadow economy as a part of their overall VAT gap than the UK does.

2. Have you identified adaptation of the frauds following the implementation of the mini one-stop-shop (MOSS)?

I have not researched this issue.

3. Do you see the one-stop-shop (OSS) as a solution to VAT fraud or do you expect and adaptation of the fraudsters to this new regulatory environment?

I expect that the OSS will reduce VAT fraud and I do not see it as being as easy to combat as other measures have been in the past. There will be a requirement that VAT be charged on all sales at the VAT rate applying in the country of end-user consumption. The option of not paying tax on exports, and imports within the EU, will therefore be eliminated. If a requirement that VAT be enforced on all imports made through online portals, such as Amazon and eBay, then the risk of fraud arising in this way will also be considerably reduced. As Amazon has recently noted on its website as a result of recent changes in the law in Australia to tackle online abuse[vi]:

If you are selling a LVIG item on amazon.com.au and you are dispatching to a customer in Australia from outside Australia, one-eleventh (1/11) of the sales price and delivery cost that you set in Seller Central will be deducted by Amazon and remitted directly to the Australian Tax Office (ATO)

This simple, but effective routine is going to be hard to evade.

4. Can you give an indication of the size of the resources dedicated to the fight against VAT fraud in Member States, generally and in some of them?

I have sought to answer this question by surveying EU tax authorities to ask about their approaches to the tax gap in general and the resources dedicated to the task of closing them. This work has been undertaken as part of the Combating Financial Fraud and Empowering Regulators (COFFERS) Horizon 2020 project. Responses were poor: just six countries replied and most information supplied was too scant to use.

This reflects the fact that by no means all EU member states undertake any work on tax gaps. In 2016 the EU suggested that the following states were doing so [vii]:

| Member state | Taxes covered |

| Czech Republic | VAT |

| Estonia | VAT, income tax and social security |

| Finland | VAT |

| Germany | VAT and corporation tax |

| Italy | VAT, income tax and corporation tax |

| Latvia | VAT, income tax and social security |

| Poland | VAT |

| Portugal | VAT |

| Slovakia | VAT |

| Slovenia | VAT |

| UK | VAT, income tax, corporation tax, social security |

The OECD has suggested others might be doing so as well: there is evidence that Denmark, Sweden and Lithuania are doing so, as well as the European Union itself with regard to VAT. This does however leave only half of members states taking any proactive steps to determine the scale of the tax gap they face, which must be seen as an essential pre-requisite for planning the allocation of resources to tackle this issue.

Evidence from the OECD on tax administration management[viii] published in 2017 and relating to the calendar year 2015 does not indicate the number of staff dedicated to tax abuse. I am currently engaged in undertaking research on tax administration efficiency using this data but am unable to present findings at present. I might be able to do so by early autumn.

5. Is VAT carousel fraud a European problem only or are other countries facing this problem too? If yes, could you present how they address this type of fraud?

VAT carousel fraud has, as I understand it, largely exploited the peculiarities of the EU VAT system and its commonality between members states and the opportunities it has provided for exploitation of cross-border VAT trade without VAT being charged at the point of export (to date). I have not seen much evidence of it being a problem elsewhere, but nor have I spent much time looking at the issue.

6. Innovation can play a role in the fight against VAT fraud. It is said that the blockchain technology could help reducing VAT fraud. Do you agree with that? Can you explain why and how it would help putting an end to VAT fraud?

This is not an issue I have looked at and on which I am not expert enough to comment.

7. Taking the different national VAT systems and enforcement rules in place, do you see that there is a risk of cross-border shopping and arbitrage by criminals? Could you comment on the concerns of some Member States in this regard?

All tax law is subject to abuse and arbitrage. That is because arbitrage, by its nature, depends upon differences between tax systems to exist and it is a matter of fact that there are, and will remain, differences between the VAT systems of differing EU states as a result of different tax rates; different translation of EU directives into local law, different administrative procedures, different enforcement regimes, and weaknesses in border controls. The ways to reduce this risk are by:

- Reducing tax rate and exemption differentials;

- Reducing differences in procedure;

- Enhancing cross-border cooperation and enforcement;

- Better tracking of consignments.

That said, this has a cost, and at present with too few states seeking to appraise their losses to the tax gap what that cost is cannot be appraised by at least half the EU member states, including many with the largest tax gaps. In the circumstances their chance of directing resources towards closing that gap in a cost-effective manner are low. This is an issue I will address in the presentation I make.

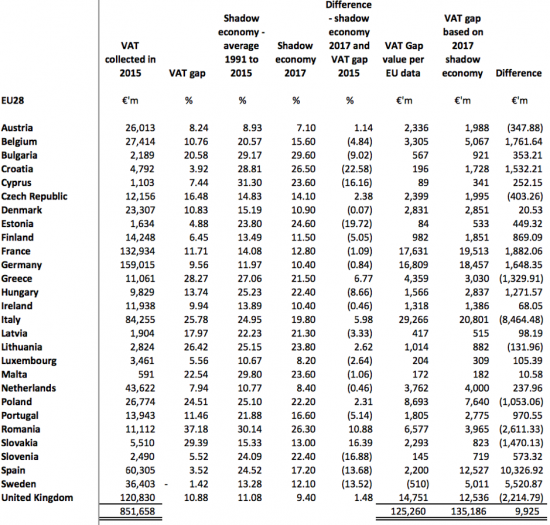

8. Appendix: data on the EU tax gap

The following data may be of use in appraising the losses likely to arise to VAT fraud in the EU:

VAT collection data is from OECD sources[ix]. The VAT gap data is the EU estimate for 2015[x]. Shadow economy data is from the IMF[xi] and is a long-term average and 2017 data, which is generally lower. The estimates of the monetary value of the VAT gap are my calculations and assume that the sum lost is on theoretically due liabilities assuming the VAT gap for the EU or 2017 shadow economy data were to be true.

As will be noted, depending upon the basis of calculation, the VAT gap is estimated to be between 125 billion and €135 billion a year. It is stressed that these figures should be considered approximate and estimates. It should not be implied that this sum could be recovered in full by action to tackle the issues discussed in this note. It does, however, indicate the significance of the issue to which, it is suggested, far too little attention is being given.

9. Endnotes

[i] Professor Richard Murphy FCA FAIA(Hon), Professor of Practice in International Political Economy and Director, Tax Research UK, Rm D503, Department of International Politics, School of Social Sciences City, University of London Northampton Square, London EC1V OHB. richard.murphy@city.ac.uk

[ii] See https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/715742/HMRC-measuring-tax-gaps-2018.pdf

[iii] ibid and author's calculation.

[iv] https://www.nao.org.uk/report/investigation-into-overseas-sellers-failing-to-charge-vat-on-online-sales/

[v] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/715742/HMRC-measuring-tax-gaps-2018.pdf

[vi] https://sellercentral.amazon.co.uk/gp/help/external/4BBHW7XBNS2GMWU

[vii] Tax Policies in the European Union 2016 Survey, Brussels: European Commission, https://ec.europa.eu/taxation_customs/business/company-tax/tax-good-governance/eu-semester/tax-policies-european-union-2016-survey_en

[viii] https://0-www-oecd--ilibrary-org.wam.city.ac.uk/taxation/tax-administration-2017_tax_admin-2017-en

[ix] OECD (2017), Tax Administration 2017: Comparative Information on OECD and Other Advanced and Emerging Economies, OECD Publishing, Paris, https://doi.org/10.1787/tax_admin-2017-en.

[x] Source: European Commission https://ec.europa.eu/taxation_customs/sites/taxation/files/study_and_reports_on_the_vat_gap_2017.pdf

[xi] https://www.imf.org/~/media/Files/Publications/WP/2018/wp1817.ashx

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

[…] have already noted the information I supplied on VAT fraud in advance of the hearing of the Tax3 Committee of the EU […]

[…] Source:Â Taxresearch.org.uk […]