The Tax Justice UK to mark the tenth anniversary of the Northern Rock crisis at the Royal Society of Arts last night was fascinating.

Prof Daniela Gabor explained why we have a shortage of some sorts of debts in the UK right now, as I have often said of government debt.

Prof Daniel Mugge (who has the amazing title of Professor of Political Arithmetic at the University of Amsterdam) made clear that financial crises are a first world luxury created by overfed optimism that inflates the quantity and value of debt, which in itself is always a measure of inequality.

Nick Shaxson talked about the need for political change to challenge the neoliberal thinking that competition conquers all that has, however, led to the continuing rise of rent-seeking monopolies.

I offered comments on the theme discussed here yesterday, but strongly supported Daniel's view that some assets are horribly overpriced, and that this is deliberately overfed optimism.

Take two examples. The first is the world wide stock market index, now at an all time high this week:

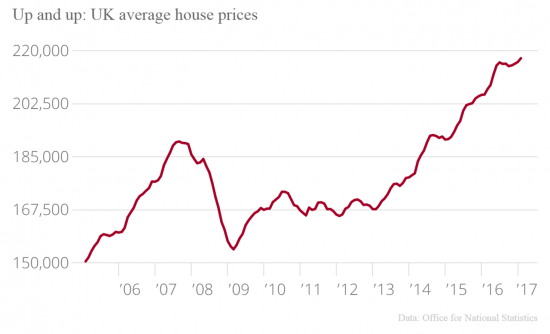

Add in UK property prices:

Add in UK property prices:

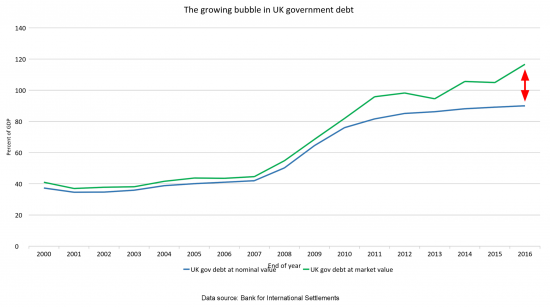

And Daniel had a great slide showing how much greater the market value of UK government debt is than its nominal value. The excess is about £500 billion right now - all of which has, by definition, to unwind before these debts are repaid. This is his chart:

What was my big takeaway of the event? I would say it is that we will have another crisis, and next time it will be different. That, however, will be because it will be much worse than last time simply because the scale of asset over valuation is so much greater this time round.

If and when interest rates rise (and the Bank of England is suggesting it may do just that) and if and when they try (I emphasis the word try) to reverse QE, as they hinted they might only yesterday (although their hints are notoriously unreliable) then I suspect the time to a tipping point will begin to reduce, sharply. And, as the stock index chart shows, whilst it takes quite a while for an over valuation to arrive the down sides tend to happen pretty quickly. There is ample talk of cliff edges when it comes to Brexit but that's a minor hillock to fall off compared to the cliff from which a major asset revaluation will cascade.

It could, of course, be argued that this might be the best way that there is to reduce wealth inequality. I have to say that is not the way I look at this. The stress that a radical asset revaluation will create is enormous. Pension funds will be in massive deficit. Insurance company solvency will be challenged. Households will have negative equity. Banks will have big holes in their balance sheets, and could easily fail. Tax revenues will fall. And there will be a recession as a result. And because there's further to fall than last time, and the range of over valued assets is greater, and the scale of personal indebtedness is higher, let's not beat about the bush, this time it's betting to be uglier than last.

And for the record, there's very little we can do to stop this happening. The overvaluations exist. The supposed robustness of the banking and financial systems about which so many are so smug is dependent upon them and so there is no willingness to address them. And the Bank of England and others are willing to lie to defend the status quo, as are all those politicians still wedded to the failed neoliberal model.

In that case we have three options.

The first is design systems to prevent this happening again, such as better regulation, wealth taxation, international tax cooperation, universal basic incomes, better training in the nature of tax and money, and so on, all of which have to be underpinned by a new political narrative.

Second, we have to ensure there are tools to deal with this crisis when it arrives like the Green New Deal and People's Quantitative Easing, both of which remain pretty much unique in their potential role in any recovery.

Third, we have to be ready. We do not know when this will happen. We are in a Gramscian moment waiting for the new to be born. But it will be. Until then we despair knowing that what will come will be horrible, and base our appraoch on the optimism that there are solutions available for politicians to use when this moment arrives.

In the meantime, hold any savings in cash. That's not financial advice. It's just what I am doing.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“how much greater the market value of UK government debt is than its nominal value. The excess is about £500 billion right now — all of which has, by definition, to unwind before these debts are repaid.”

Forgive the stupid question, but what’s the significance of the gap opening up between nominal and market value?

The significance is that in pensions funds, insurance companies and banks there is a massive pile of assets valued at vastly more than they can ever actually be worth because they only ever eventually pay back their nominal value

Nonsense, you are looking solely at the redemption value and ignoring the coupon payments!

I am entirely aware of this fact

And I’ll out it to you that this will not protect them from a major change in valuation at some point

But keep believing your spreadsheets if you wish

Maybe I’m missing something but aren’t you forgetting the coupons these bonds pay? Lots of the legacy gilts pay coupons of 5%, whereas the current at-market rate that you can achieve from investing in essentially-riskless investments is closer to 0%

Bond prices are the sum of discounted future cash flows. When at-market rates are 0% then essentially there’s no discounting (as in the absence of a market return then money in the future is worth the same as it is today)

So if you have a 10y bond paying 5% coupon then it’s price in a world of 0% interest rates is 10×5 + 100 = 150.

Over time the price will go down towards 100 as the noteholder receives his/her 5% coupons. But that’s not a concern. After year 1 you go from having a bond worth 150, to having 5 cash and a bond worth 145, so there no loss at all.

What am I missing?

You’re missing the fact that these bonds remain heavily overvalued to realisation

Did youy notice what they guy who did the calculation did? Do you think he (and I) have no awareness of discounting?

Are you aware how badly these CAPMs crashed before?

In my example you’ll realise 150 of cash over the next 10 years, as long as the UK Government doesn’t default, or get into such a precarious position that it has to restructure its debts, and currently the market prices that chance as very close to zero.

What value should market participants be ascribing to 150 of Government-guaranteed cashflows?

You have clearly failed to read my assumptions

But carry on in your own risk free world

Cash? Which currency, Richard?

In the UK sterling

Thanks Richard. What are your thoughts on gold instead of cash?

I have no thoughts on gold

It is a largely useless commodity

But speculate if you wish

‘In the meantime, hold any savings in cash.’

Are you talking under the mattress cash or in a savings account cash?

In a bank

A bit under the mattress could be useful for the period when the ATMs are all down, or withdrawals are limited as they were, I believe, in Cyprus and Greece.

Thanks Richard for your take on this. You have been correct (in the past) and I fear that your prediction will come to pass. My main concern at present though is that I also have savings in cash accounts and wonder if there is any risk of these becoming inaccessible in the future when something ‘bad’ happens?

Ian

Spread them is the best advice….

Banks in the same group (Institution) have a combined limit of £85k per person. If you are fortunate to have more than this then look up if your bank(s) are linked http://www.moneysavingexpert.com/savings/safe-savings#whatcounts

I agree with your general hypothesis that there’s going to be a crash soon (after all it’s 10 years since the last one so it’s time for it), and it may be fairly devastating, mainly because the economy is in a much worse state than it was last time, and, of course, the impact of Brexit.

However I don’t follow your argument re the gap between the market and nominal values of government debt. This arises because we have much lower interest rates now than we did at the time most of this debt was issued. So the gap represents the capital losses that have already been incurred by the holders of the bonds, not as something that has to be repaid in the future. What it does mean is that the government now has relatively expensive debts on which it is paying interest above the current rates.

I am baffled

How have you made a capital loss when the asset has risen in price, because that is what has happened?

And no, the government does not have expensive debt: it has incredibly cheap debt because it only has to repay the nominal sum meaning that future capital losses are guaranteed to those buying at current prices or valuing them at these marked up rates

Your article states regarding the difference between the market and nominal values that “The excess is about £500 billion right now — all of which has, by definition, to unwind before these debts are repaid”, which implies that the current bondholders will suffer a loss on the value of the bond as the nominal value or capital is redeemed at much less than the market value. But this has already been factored into the current value of the bonds which is mad up of both capital and interest payments.

And the government does indeed have an expensive debt as it is paying well above the current interest rate for each £1 of debt issued on these bonds.

With respect, if you believe that you’re one of those who thin k the over-pricing won’t correct

Until it’s too late of course

Read Adair Turner on the shock he suffered post 2008 when he realised that supposed rational pricing models weren’t either rational or realistic at all

If you are saying markets sometimes get it wrong I couldn’t agree more.

But first the gilt market prices have a rather more solid foundation than most in terms of their anticipated cash flows and interest rate assumptions, and second if there is another crash the probable solution will be a move to negative rates which will be positive in terms of bond values

And still leaves them overvalued

“And no, the government does not have expensive debt: it has incredibly cheap debt because it only has to repay the nominal sum meaning that future capital losses are guaranteed to those buying at current prices or valuing them at these marked up rates”

Are you forgetting coupon payments? The government has to pay back the bullet nominal sum, but also ALL the coupons over the life of the bond.

Let me ask you a question?

If the government issues two different 10 year bonds on the same day, both with a nominal face value of 100, but one with a coupon of 2% and one with a coupon of 5%, which one is worth more?

I really do know all about this stuff

And I am also wholly aware that your models work in orderly markets

And fail in disorderly ones

You have clearly forgotten that

No wonder we will have another crisis

Overvalued relative to what, over which time period and in which circumstances? Not under a high-ish inflation, zero or negative interest rate scenario which is fairly likely when there is a crash. After all cash is losing you 3% pa currently with inflation, and if it’s really bad gilts are safer than banks.

I asked you a very elementary question – if you know all about these things as you say you do, why can’t you give me an answer? It’s not like I’m asking you to prove relativity or something – a single sentence would do.

I’m also interested to know which models you are referring to, when discussing bond prices/values? Most models have a name – perhaps you could provide us all with it?

I have answered

Read the quote from Adair Turner

Tell me why it’s wrong

You haven’t answered anything. I’d go as far to say you are dissembling to try and hide your lack of knowledge.

Let me try and ask my question again.

If the government issues two different 10 year bonds on the same day, both with a nominal face value of 100, but one with a coupon of 2% and one with a coupon of 5%, which one is worth more? Let us assume in this case that the markets are functioning fine. Which one is worth more right now?

I’m not dissembling in the slightest

I am saying – as Adair Turner found out – that theory need not hold true

And why is that? Because you think that all that you’re facing is risk

I am saying you’re facing uncertainty

Now if you can tell me from now until a 10 year gilt matures what rates will be and when changes will take place I’ll concede you face risk

Otherwise I am right: uncertainty can create major price changes that can seriously reprice even an asset like gilts

If you deny that, tell me why

What makes you clairvoyant in other words, because unless you are what you’re suggesting is pure poppycock (or words to that effect)

You are dissembling. Of course over the life of a bond, it’s value can change.

That is of course NOT what I am asking. I am asking which bond would you rather have, of the two I described – today.

Given that market conditions for both bonds today are identical, which is worth more?

You entirely miss the point

Your abstraction takes us away from realty

That is my point

I’m not sure which abstraction you are talking about. Both bonds, issued on the same day will face the same risks and uncertainties going forward. The bonds are otherwise identical bar their coupon.

I am not asking you to value them going forward, or to say which will be worth more in the future, I am simply asking you which will be worth more today. This, for anyone with a basic understanding of bonds, should be a simple – even instant – answer.

That you cannot provide it suggests to me that you don’t know what you are talking about, despite your protestations to the contrary.

As you say, that’s basic stuff

But it proves two things

A) You’re asking a stupid question because it is pointless

B) You are not engaging with the point I made

And with respect, this my place and so I decide what I respond to and I have little time for time wasters who want to reveal what little understanding they have.

I think your inability to answer shows only one thing. The point of my question was to see if you had any understanding of how bonds work, given that what you have said above is quite simply nonsense.

Likewise, the points you have made are immaterial to the question I asked.

The two bonds I asked you about will always be worth the same amount. Their yield to maturity will always be the same. Which is of course what we care about when talking about bonds. The 5% coupon bond will have a higher cash price, thanks to it’s higher coupon, but that does not mean it is worth any more than the 2% coupon bond. in terms simple enough for you to understand, you will pay more for the extra 3% coupon, and this extra will exactly cancel the value of those bigger coupons out. So the two bonds are worth the same. Always.

As I say, over the life of the bonds they will give exactly the same risk and return, and cost exactly the same to the government to issue and fund.

They will also be worth the same regardless of market conditions, risks, volatility and all the other factors you went on about. Which suggests to me that you don’t really understand the topic.

All Daniel Mugge’s graph is showing us is that interest rates are low, and the the UK’s debt stock was issued when interest rates were higher – and thus the coupons on the bonds was higher. Which means the face value of the older bonds is above par. You will find the same kind of chart for most of the developed markets, and it tells us exactly nothing – because as we all (well, it seems not in your case) the face value and coupon of a bond are immaterial, and only the yield to maturity tells us anything useful about a bond.

Respectfully, I repeat the points made

I will post a long blog explaining why you are wrong later today

I have real people to meet in the meantime

And please note – being repetitious and rude are reasons to be deleted here

You are both

Would you count premium bonds as cash (or near-cash) or do you consider government bonds as at risk?

Government bonds (gilts) are clearly at risk

Premium bonds are not

http://nsandi-corporate.com/about-nsi/

Premium bonds are just another way of lending money to the Government.

You’ve criticised me for “living in a risk-free world”, and talked about “universal credit crises”. How is that consistent with equating Premium Bonds to cash?

Because there is no overvaluation

I have not disputed that the government will return the notional capital in gilts

This is all there is in a Premium bond that is guaranteed to be returned so overvaluation cannot happen

That is what I was referring to. Please keep up

“I have not disputed that the government will return the notional capital in gilts”

“they only ever eventually pay back their nominal value”

“the government … only has to repay the nominal sum”

It’s these statements that have raised the ire of a lot of people I think; to the reader you’re either saying that the bonds don’t pay coupons, or you’re saying that all the coupons should be valued at 0 (while the principal should for some reason be valued as risk-free). And then you say bond-market participants should listen to Turner because they’ve got their valuation models wrong!

Now it’s totally fair to lament the lack of risk premium in markets after the global wave of QE has lead people further out along the risk spectrum in search of a return, and of course to express a concern about how unwinding QE will be managed when that time comes (in my view it’ll be done over a period of decades simply by Central Banks not using the proceeds of maturing Government Bonds to buy new bonds, but that’s by the by).

It’s also fair to say, OK, are we sure that regulators have done everything they can on bank solvency, capital ratios etc, given asset prices are currently high in the wake of QE. I’m sure they’re far from your favourite organisation, but the ASI are doing good investigative work on this for example: https://www.adamsmith.org/research/no-stress-iii-the-flaws-in-the-bank-of-englands-2016-stress-tests

But it is a bit odd to say that Pension funds will be in massive deficit when rates rise as analysis has been done that shows a 0.1% increase in gilt yields decreases aggregate scheme liabilities by 2.0 per cent while only decreasing aggregate scheme assets by 0.5 per cent http://www.pensionprotectionfund.org.uk/Documents/purple_book_2015_chapter5.pdf

This, while making and defending odd declarations about the structure of Government Bonds like I quoted above, I fear has lost the message you were trying to convey.

Nonetheless, I appreciate you taking your time to reply to everyone’s comments.

Of course they pay a coupon: don’t be daft. Do I really have to state the bleeding obvious for you Worstallites?

The point is that you cannot say that has certain value in current terms and to capitalise it on the basis that there is no uncertainty attached to it is just wrong.

And as for the ASI – please don’t make yourself look really stupid. Most of you have tried to do that hard enough already.

“The excess is about £500 billion right now — ” as Card said forgive the stupid question…

This seems significantly close to £435 billion QE. Are the two things directly correlated? I.e. is QE causing 90% of the bubble or is it just a coincidence?

They’re not directly related

But they are indirectly related

QE kept interest rates low

The result is inflated prices

‘base our appraoch on the optimism that there are solutions available for politicians to use when this moment arrives.’

I have to say that I am not convinced that many in our government have either the necessary intellect or the imagination to do anything other than follow dogma. What we seem to have is a group of people, prepared and trained by PR types, often exclusively educated, whose primary goal is to preserve the nation, and their position within it, in the way they want it and have been brought up to expect. Admittedly that approach is not exclusive to the Tory party.

You’ve got your logic, as far as insurance companies and pension funds are concerned, entirely wrong.

Pension schemes are net exposed to rates falling (further) – hence the depressed yields have worsened their solvency position despite equity market growth. Increasing interest rates will reduce the value of some of their assets but will reduce the value of their liabilities by much more, thereby beenfitting their solvency positions.

Insurance companies tend to be much better matched between assets and liabilities, but in the main would marginally benefit from rising interest rates.

This really is basic financial maths 101 – how are you getting this wrong?

I’m not

Nor is the professor of political arithmetic

You’re assuming interest rates can rise without consequence

I am saying they won’t rise but the consequence of the attempt will be a financial crash

Maybe you need to do economics 101

Richard Murphy says:

“… the professor of political arithmetic”

It is always good to learn new things. Arithmetic is the study of actions of the four basic

operations between numbers –addition, subtraction, multiplication and division.

This much I know.

So in what way is political adding up different from run of the mill adding up?

No wonder you have to be a professor to see the difference.

Thank you.

The politics of arithmetic are, as I understand it, about how maths is used to present a reality that isn’t

As is happening on here today from many commentators

Good assessment. Don’t entirely agree with the remedy but appreciate someone is taking this into account..!

an equal argument can apply to other jurisdictions…including Europe which is in a much worse state (recent positive figures notwithstanding).

A worthwile point you make (as an aside) suggest some aspects including Euro related carnage could well overshadow Brexit in the longer term…

‘You’re missing the fact that these bonds remain heavily overvalued to realisation

Did youy notice what they guy who did the calculation did? Do you think he (and I) have no awareness of discounting?”

‘Heavily overvalued to realisation’???

This is just meaningless drivel.

Insurers and pension funds that hold these assets to maturity will get the returns they expect, a combination of income (at elevated levels) offset by a capital loss.

And any change in interest rates will equally (or greater) offset the liabilities.

Oh dear….

Such is the blindness that costs others money

Your just making statements with zero supporting evidence which fly in the face of everything we know anout the assets and lisbilities of insurers and pension funds.

Please explain what will happen to interest rates (gilt yields) that will cause pension fund deficits to increase and insurers to go insolvent?

From the Turner Review, 2009:

At the core of these assumptions has been the theory of efficient and rational markets. Five

propositions with implications for regulatory approach have followed:

(i) Market prices are good indicators of rationally evaluated economic value.

(ii) The development of securitised credit, since based on the creation of new and more liquid

markets, has improved both allocative efficiency and financial stability.

(iii) The risk characteristics of financial markets can be inferred from mathematical analysis,

delivering robust quantitative measures of trading risk.

(iv) Market discipline can be used as an effective tool in constraining harmful risk taking.

(v) Financial innovation can be assumed to be beneficial since market competition would

winnow out any innovations which did not deliver value added.

Each of these assumptions is now subject to extensive challenge on both theoretical and empirical

grounds, with potential implications for the appropriate design of regulation and for the role of

regulatory authorities.

Read and inwardly digest, I suggest

If you buy at 150 and write off 5 points per year to a 10 year maturity the yearly diminution of the capital value of the fund via revaluation will equal the earned income over that period. In cash terms a present outlay of 150 will generate a future (10 year) inflow of 50 plus the maturity payment of 100. What am I missing? Are you not simply exchanging capital for income?

What can be done about pension savings, if anything? There is some scope for choosing investments.

Cash

Don’t think cash is an option in my pension scheme investment options. I don’t know if I’m allowed to take the money out. I think the nearest is an inflation-linked option.

Most funds have a cash option

Mine does

Ask

Richard,

You mentioned spreadsheets in one of your earlier replies so I thought it would be enlightening and helpful to try something out.

Assume the following:

Current interest rate is 0.5%

Gilt has a nominal value of £100 and redemption is in ten years

Coupon is 5% payable annually.

Question:

What is the value today of this bond?

Method:

enter the following into cell A1

=NPV(0.005,5,5,5,5,5,5,5,5,5,105)

This gives a present or market value of £143.79 or more than 40% above nominal value.

Would you agree with my workings?

But you’re assuming a shock free world and it does not exist

It’s true that I’m assuming that the UK government will be good for its outstanding commitments to holders of its securities over a ten year horizon but then so is the market for gilts, which is why gilts can be issued at par in London but their equivalent in Athens, say, are heavily discounted at issue.

But you’ve side-stepped my point which concerned the basis of calculation. I’m trying to grasp the perceived problem with market versus nominal price differentials so some further guidance would be helpful.

I am not disputing your theory

See what Turner said

I am saying there can be discontinuities in practice

Even in gilt markets

And especially when there are universal credit crises

But you and others commenting keep your head in the sands of micro theory and ignore macro practice

I was right last time

And I will be this time too

Sad to say, I am afraid

So difficult to hold on to cash with these new slippery notes……..

Richard,

Could you please explain, for the uninitiated such as yours truly, the circumstances in which the Gilt holder would lose (some of) their money?

Would this occur only if/when they all suddenly attempted to sell the Gilts on the secondary market *before* maturity, then?

(Because assuming they held them to maturity, is it not the case that UK Treasury would redeem them at the full price initially paid for them?)

Clearly you are angered by those posting above who insist you are wrong, but I’m not doing that, I’m just curious as to at which point, and the mechanism by which, the holders of Gilts would lose some of their money?

Thanks!

The loss is if there is a sudden movement in price for external factors which requires, for example, accounting revaluation across a whole portfolio indicating significant financial stress vene if the plan is to hold ot redemption

In those situations, ignored by those commenting, real stress arises irrespective of theoretical pricing models

And it does happen

Richard

If gilts default we’re all fucked. The cash stashed under your mattress will probably be worthless too

I didn’t say they’d default

They won’t

I said their could be disruption in valuation in the market with significant consequences

I’m afraid I think you’ve really lost the plot on this one. Which is a shame a lot of what you say seems pretty sensible

You might ay so

And I am entirely confident in all that I have said

“The loss is if there is a sudden movement in price for external factors which requires, for example, accounting revaluation across a whole portfolio indicating significant financial stress vene if the plan is to hold to redemption”

OK, as a non-accountant/economist/banker I am struggling to get this, but, I’ll try: So, would, say, interest rates increasing suddenly and dramatically to e.g. 5%, (making mid-term 10Yr 0.5% Gilts worth bugger all) be the sort of thing you refer to as likely to decrease the value of those Gilt holdings below current market prices?

Then, if so, I get it now… but if not, then perhaps you could provide a couple of clear examples of what sort of event/s would need to happen for this devaluation in Gilts to occur?

(I have never quite recovered from the time when my oldest friend, a Maths and Philosophy graduate, told me that I obviously found it hard to think in abstract terms – although painful to hear, clearly this is one of those occasions!)

Might I suggest the blog I will publish soon

Sorry – been in a meeting for the last couple of hours or so

That’s the campaigner’s life

If it’s not default I’m not clear what else could disrupt valuations.

Gilts are defined by nominal, coupon and redemption date. Valuation is determined by discounted cash flow against the yield curve alongside the perceived certainty that the payments will be received i.e. they will not default.

The only unknown variables are the expected shape of the yield curve and of course the market demand. Yield curve expectations may vary over time but this has always been the case. Demand for gilts will almost certainly increase in a crash as investors seek safe havens.

You have no clue what the uncertainties are

Because you can’t know my assertion is the only one that can be said to be based on fact

The fact is, you don’t know

And because you don’t know volatility is likely

The talk was very interesting, and the discussion afterwards. I was surprised there were so many empty seats in the room.

Richard, I can’t find a source for the research behind Daniel’s gilt graph. Is it (or the data) available somewhere?

Can you confirm: is it showing that the current market price of gilts is much higher than the nominal principal amount? (Which is what you might expect, if the interest on the gilt is significantly greater than the current rate of interest.) Or is it showing that the current market price of gilts is much higher than the sum of the nominal amount of the principal *plus* the nominal amount of the future coupon payments? And if the coupons are taken into account, at what discount rate? Thanks.

The differential is market price to nominal

I was a little disappointed with attendance : NGOs really need to learn to overbook

“The differential is market price to nominal”

OK – fair enough. But why would a Gilt have a different price to it’s nominal 100 value? If as you say is true, and governments only have to pay back the nominal value, why aren’t all gilts exactly the same price?

Notice the graph

You tell me why

I know the answer

And I can see the disruption

Why can’t you?

I am a little more nuanced about holding cash: hold investments in small companies with robust cashflows and managers you trust.

I’m not sure you do know the answer – given you haven’t managed to answer a simple question earlier, and so far have got everything wrong when it comes to bond valuations.

Of course, the answer is pretty simple. Bond valuations aren’t fixed – they move with interest rates. Bonds rarely trade at par in the secondary market. They might redeem at par, but that redemption value is only part of of what a bond is worth.

Did you nite I discussed interest rate changes as the precursor for disruption?

Why do you think I did that?

Richard You responded earlier:

But the discontinuities (and to be candid I’m not sure what precisely you mean by “discontinuities” unless it’s another word for crisis or code for a coup d’état) represent a risk which the market can accommodate and price.

So if you accept that the UK Government is likely to meet its obligations for the life of a gilt, then what can disturb the relationshp between the market value today of a gilt and its future redemption value.

It grieves me to say so but I’m beginning to wonder if this isn’t a premature April Fool’s joke you’re playing on your followers.

Go back to Turner

The market did not price such things correctly

I had always thought it incapable of doing so

Turner thought pre 2008 that it worked as the models said

Then like Greensoan I realised the models did not work

But what commentators here are proving is that the lesson has not been learned so we will have another crash

I will comment on the reasoning in a blog this morning

You really will need to take note

These “models that failed” that you talk about were in a completely different space to any considerations for valuations for the Gilt market.

Individual sub-prime mortgage borrowers can be thought of as individual bond issuers. The products that were created that were mis-priced were those that combined, say, 100 of these mortgages I nto one entity, which then itself issued tranches of bonds whose risk-exposures were marketed as being very different to each other. That is to say, the first few defaults of the underlying mortgages would hit only Bond Tranche A, only the defaults following those would hit Tranche B etc etc, with the apparently-least-risky Tranche requiring a default of a huge number of the underlying mortgages before they saw any capital loss at all.

The models you (and Adair Turner) talk about assumed the mortgage borrowers weren’t correlated. This was indeed wrong, they were highly correlated, i.e. when a few defaulted then they essentially all defaulted in sequence, so the risk of each Tranche was a lot more equal than initially thought, so people holding what they thought was a riskless Tranche ended up losing money.

There’s a world of difference between deciding a fair discounting rate for a tranche of a complex basket product, and deciding it for a single high-quality sovereign issuer though. There’s no funky maths or obscure models required for the latter.

If you’re saying that market participants aren’t valuing future uncertainty of U.K. sovereign credit risk then I would disagree; for partially this reason, longer-dated discount rates (“yields”) are higher than shorter-dated ones, ie bond-holders want to be compensated for holding longer-dated debt, so they discount it by a higher rate, which means the price is lower than were it discounted at a lower rate.

https://www.bloomberg.com/markets/rates-bonds/government-bonds/uk

Given we’re in a low-interest rate environment, and bonds issued 20yrs ago pay high coupons, then by definition their prices will look optically high. But (and I know you’ll probably comment only on this sentence) there really isn’t anything to worry about. In fact we should all welcome the day when U.K. Gilt prices go down due to the low-interest rate environment no longer being in effect; all those pension deficits that have appeared since rates lowered so drastically post-crisis will disappear, and finally perhaps those of us retiring in the future on Defined Contribution pensions will be able to buy an Annuity that brings us closer to those with their Defined Benefit golden tickets.

All so true

And all so wrong for reasons I will note soon

I can’t be,eve I’m reading this from a supposed professor of economics!

Because the complex models used to value tranches debts (which require numerous assumptions on the timing of repayments and default risk, most importantly the correlation between the different underlying) failed during 2008, you think that we can’t accurately model gilt prices as interest rates change?

That really is priceless.

With known future cash flows, valuing a gilt is trivial. And, for gilts issued some time an with high coupons, prices above par are exactly what would be expected. Everyone knows that they will redeem at par maturity and that causes no problems whatsoever, as they will have also received the high coupons in the interim.

Yoiu’re reading it because I was right then

And I know I am now

You see, there aren’t known future cash flows

Your model works because you are excluding everything inconvenient from it

@Marco Fante

No, the risk free rate is not negative. It is just low. It is negative at some tenors in Europe, for example.

As anyone in the market understands.

Are you always rude?

Aswell as usually wrong?

If (as you claim) there is a massive re-price of gilts (presumably you mean down), but they will still be expected to pay their mandated coupons and redemption payments, what will happen to the value of liabilities in that scenario?

Why do you think this increases a pension scheme deficit or threatens an insurers solvency?

Just saying ‘I can see it, you can’t’ doesn’t explain why you are making those claims (which contradict all known facts about insurance and pension ALM and valuation.

Let me write another blog to explain

The commenters here that have cited formulaic, CAPM type explanations for the aberration in bond prices would appear to have been paying insufficient attention to the relevant chart.

There is no surprise in the fact that there is a gap between the nominal and market value of Govt. debt, and the standard explanation for that applies quite neatly to the period before 2009 where the gap between the two values is relatively narrow, steady, consistent and (as formulae would have it) predictable.

What the standard explanations obviously do not account for is the sudden, erratic and increasing gap that has appeared since 2009. I’m quite shocked by the chart actually. I had no idea that divergance had become so extreme. It has a lot to do with the value people place on security of course. The ‘risk-free rate’ has become effectively negative. More so than I imagined.

Thank you

A rational comment

Try my excel formula above:

=NPV(0.005,5,5,5,5,5,5,5,5,5,105) where the interest rate was assumed to be 0.5% which produced a market/present value of £143.79

Now, switch the interest rate to 4% and we have

=NPV(0.04,5,5,5,5,5,5,5,5,5,105) which gives you a market/ present value of £108.11

Pretty standard stuff, really…

I agree

And so misunderstood

Seriously? You’re struggling to understand what happened since 2008/9 to cause gilt yields to fall?

How about interest rates falling from 5% to 0.5% over that period!!!

Steve

I find you deeply offensive

Any further comment in similar tone will be deleted

Richard

There is a clear lack of understanding of the fundamentals here. Replying to contributors simply saying “I am right” simply doesn’t cut it. I’d suggest not posting on valuations further to retain credibility!

I assure you I will be posting again

Jimmy H

As ever proponents of market wisdom (like yourself perhaps?) are following the herd mentality (micro environment) too closely without looking at the bigger picture (the macro environment). This is what a mixture of a culture of short term gains and bonuses does to markets to make them inflate too much. There is no room to pause and take stock.

In the film ‘The Big Short’ (based on Michael Lewis’ book) those that knew what was going to happen (and profited from it) did something the others didn’t – they went and looked deeper.

Richard’s statements are plausible in my view.

I’m going to bring another type of gut instinct along here – one that sides with the now well known inability of markets to price assets reasonably based on the last crash and the other crashes that happened before 2008 (can the detractors remember how many times there were crashes before 2008?).

All of these crashes were caused or made worse by over evaluations of some sort were they not? The history is there is it not?

All I can see in these comments is denial (because of fear or is it that those with money to invest are just full of hubris?). But also ignorance of just how little has been done since 2008 to stop it happening again.

In my view the reasons why the market has not learnt to price assets and other stuff properly is because on the evidence of the 2008 crash the institutions know that they will be bailed out by the now established practice of financial sector welfare (or orthodox QE).

In other words as a result of QE, the markets have been perversely incentivised to be stupid yet again. Surely people can see that?

And tell me – has anyone heard of any politician saying that they will not bail out a future crash? I’m unaware that this has been said by anyone.

I think Richard is right to raise this – not because I am an expert in investment finance but because well – I just think that finance sector is still driven by short termism based on the behaviour I have seen all these years.

Spot on PSR

Pilgrim,

I’m not arguing with your position, but I think you’ve missed something.

“And tell me — has anyone heard of any politician saying that they will not bail out a future crash? I’m unaware that this has been said by anyone.”

Er…well yes actually. EU rules have been re-written (I’m afraid I can’t give you chapter and verse) to allow for the next banking crisis to to ‘bail-in’ customers and or shareholders rather there be government/central bank ‘bail-out’.

So far I understand this was trialled in Cyprus. However recently the Italians bailed out two of their failing banks (just shy of £5 billion) in defiance of this new edict.

So, yes the option is there, but I guess as ever its implementation will be at the whim of political expediency.

How the EU edict affects UK banks and it’s customers will depend on whether it is to apply to Eurozone or EU banking. Can’t help you there. I simply don’t know. Brexit may or may not have an influence on the BoE position.

If you are in the position of trusting the £85 K guarantee (lucky you if you are) I wouldn’t put too much faith in it.

Richard,

if you agree with me, it’s hard to fathom how you can think Marco Fante’s no doubt well-intentioned contribution is rational.

Did I say I agreed with you?

I don’t recall that

You may have read it that way but I think I was quite careful

Ah, my mistake then. I was looking at your reply to me at 10:20 where you said: “I agree” which I took to mean that you agreed with me but it turns out you were just pulling my leg or something.

Richard Murphy said:

As well as usually wrong?

What is wrong about identifying that UK interest rates are not negative but in Europe they are?

I said usually

You find me ‘deeply offensive’, and yet throughout this thread you’ve patronised those who appear to have much more knowledge on this topic than you.

You seemingly agreed with someone has made a blatantly false statement and you’ve refused yo justify why you are right (and the whole of the financial world is wromg).

Read the blog that’s coming

Richard Murphy claimed:

‘You see, there aren’t known future cash flows. Your model works because you are excluding everything inconvenient from it”

Please explain what is unknown about the future cash flows on a government bond held to maturity…

Just go and read what I have written

PS Are you also a member of the Flat Earth Society?

[…] wrote what I thought to be an entirely reasonable blog yesterday on why I think the next financial crisis will be more serious than the last, and a host of […]

For those who are wondering about “political arithmetic”, dhr. prof. dr. D.K. (Daniel) Mügge explains it on his website. He refers to the 17th century economist William Petty – see https://en.wikipedia.org/wiki/William_Petty – who attempted an empirical quantitative study of economic life. Adam Smith did not like it.

I think I’ll just buy some bitcoin. It could prove to be a lot safer than any conventional asset class.

Or failing that perhaps some tulip bulbs; at least that way I may have some pretty flowers to look at in the Spring.

Most of the gist of this correspondence is concentrated on the one asset class of treasury bonds.

Assumptions about the future value of bonds assumes a conventionally functioning market which we don’t have currently. Many of the major bond buyers are a captive market ‘managing’ funds which are obliged to hold bonds in their portfolios and the bond issuers know this so the market is skewed. Why else would anyone rational buy negative yielding bonds?

I agree wholeheartedly with the headline proposition of Richard’s piece in which the quirks in bond pricing are just one element.

It’s interesting to note that the temporary crash in equity markets was not echoed in property price correction after 2008. Free market my foot!

Economic policy is never neutral or objective it is always skewed in the interests of the powerful.

The only point at which I diverge from your opinion, Richard, is that if I had wealth to protect I would not trust it all to cash. In such unstable times Gold is eerily cheap and I’d have some and I would take a punt on some cryptocurrency, but with less confidence. I don’t trust the 85K savings guarantee given the EU bail-in rules (which the Italians defied just the other week).