Yesterday's stock market turmoil, whatever its long term impact, hints at a much bigger problem than a simple over valuation of Chinese shares needing adjustment.

It is also a bigger issue than our failure to address the issues that 2008 made clear had to be addressed, important as that is.

What it suggests, with its theme of recurrence seemingly beyond the control of governments to address it, is a deeper systemic flaw in the financial markets and their ability to meet the needs of society. This is what I really think we need to address .

The flaw is inevitable in a system where the long term human need for a place to save can seemingly only be matched with a short term savings mechanism, which is all that is readily available to many people at present.

The need to save is innate to many humans (not all, I know: some always assume tomorrow will sort itself out). The reasons for saving vary from simple caution about the proverbial rainy day, to family provision (education, weddings, housing), to retirement. I suspect the variety of motives is remarkably small the world over. And in most cases there is probably strong risk aversion on the part of the saver: those who save are, almost by definition, cautious people.

What the world offers them are essentially three products. The first is cash and its close relations, including gilts (although these have downside risk, especially with present rates) and corporate bonds. These tend to merge risk into the next category for saving, broadly based around shares. Beyond these there is the illiquid market. That's made up of your own business (yes, that can be a savings mechanism if the aim is to realise a lump sum) and property. Go much further into categorisation and you come into a derivative of any of these.

The difficulty in all this is multifold. First, cash saving is essentially a negative act. In times of low inflation it is a safe act and, with deposit guarantees, broadly secure but it yields next to nothing and, as importantly, does nothing for the economy. Saving in cash effectively takes money out of active use. It is a loan to a bank that then forms part of its capital (it no longer remains your money: it does belong to the bank once deposited and all you own is a loan recorded in a bank statement) but what we now know is that banks do not then lend this money on: all the loans they create are made out of new money created for the purpose. They do not therefore, effectively, need deposits to make loans. Unsurprisingly, as this realisation has dawned so too have cash deposit rates fallen, in real terms, to near enough nothing to reflect their near worthless economic status.

Gilts are a surprisingly hard to access savings mechanism for the average person: National Savings is the alternative product for many. What's the plus? The person you're lending the money to is guaranteed to repay. Plus, they use the money for social purposes and there is no intermediary: the government sells the product and it uses the money. It's a surprisingly rational savings mechanism, but one with a dull reputation unless the rates are out of line with expectation.

Then there's the stock market. And we go out of our way to incentivise this arrangement. Once almost all mortgage savings were in it. Now a significant (but falling) part of pension savings are. And ISAs are still used to encourage it. The incentive is even encouraged by subliminal messaging: on the hour almost every hour the news tells you what is happening on the markets and most of the time that induces feelings of good news: markets rise steadily and do down sides rapidly. It's as if there is a conspiracy to lure money in.

But why are we doing that? This stock market trading is almost entirely about redundant money: almost as useless as cash in its economic impact. When you buy a share it is almost invariably a second hand piece of paper you are acquiring: someone else sold a property right in a company to you and (although many people seem to think otherwise) the company that created the share that has been sold gains or loses not a penny in the process. In the case of many companies it is also many years since they created any new shares: the stock market in shares is now rarely used as a mechanism for raising money for investment, which is a process undertaken almost entirely through corporate bonds, which few smaller investors have any knowledge of, and which are almost entirely institutionally owned. So, the truth is that the stock market, and saving in it, does not produce new investment funds. It is almost as hopeless in this regard as saving in cash.

No investment conspiracy is needed to get money into property. For those who can access the market the appeal is obvious: it is in short supply, there is a real demand for it and, just as importantly (if not more so), it's utterly comprehensible. Do not fail to notice this last point: ask most people to explain the economic realities of any of the other savings mechanisms and I expect they may well have real difficulties, even with the reality of cash deposits. Property also has an obvious use as a long term savings mechanism, even if the very process of using it as such means many who want to own property are denied the chance to do so: that's the paradox in this savings market; using it for saving frequently undermines the goal of providing secure housing.

Small business saving does, I think, fall into a wholly different category. I am going to ignore it.

But having made these points let me be clear. What they reveal are three things. The first is the difficulty people have with understanding savings. Very few people have any real understanding of the mechanisms they use to save or what the impact of those mechanisms on the real economy is. This leads to serious errors of judgement, mismatched expectation and to exposure to mis-selling, loss and even fraud.

Second, most 'saving' is unrelated to any investment activity, meaning that little economic gain arises from it.

Third, saving in these largely economically useless ways allocates vast amounts of energy to supporting this activity when in many cases little or no return is actually generated as a result of that activity.

Last, and perhaps most important, given that the most important reason for saving is, without doubt, to provide for old age, the fact that many of these savings mechanisms cannot actually generate the returns needed to support people in their old age means that in large part they are unsuited for that purpose. There is massive market failure as a result.

I explained the essence of this in a short publication I wrote in 2010 called ‘Making Pensions Work'. A lot of what I wrote then does, I think, remain completely relevant today. At the heart of my concern was the failure of what I called the ‘fundamental pension contract':

This is that one generation, the older one, will through its own efforts create capital assets and infrastructure in both the state and private sectors which the following younger generation can use in the course of their work. In exchange for their subsequent use of these assets for their own benefit that succeeding younger generation will, in effect, meet the income needs of the older generation when they are in retirement. Unless this fundamental compact that underpins all pensions is honoured any pension system will fail.

As I then argued of private pensions:

This compact is ignored in the existing pension system that does not even recognise that it exists. Our state subsidised saving for pensions makes no link between that activity and the necessary investment in new capital goods, infrastructure, job creation and skills that we need as a country. As a result state subsidy is being given with no return to the state appearing to arise as a consequence, precisely because this is a subsidy for saving which does not generate any new wealth. This is the fundamental economic problem and malaise in our current pension arrangement.

If anything matters are now worse than I envisaged at the time. George Osborne's pension reforms are turning what was meant to be a pension system into a tax subsidised short-term savings arrangement for those already well off: it is staggering that, as the FT has reported this week, two-thirds of customers surveyed by Royal London, the largest mutual life, pension and investment company in the UK, took their entire pension pot as a cash lump sum following the introduction of the pension freedoms in April. Most seem to have no intention of using those funds for pension purposes now, and George Osborne is simply exploiting this financial short termism for the purposes of securing his own short term tax hit.

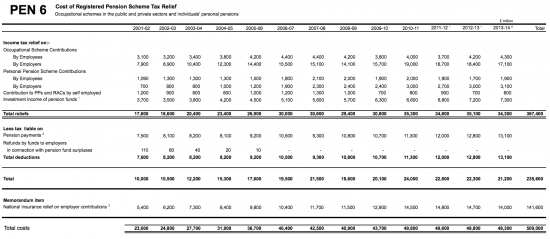

In the face of this effective collapse of the private pension system some radical re-thinking of pensions is needed. This is no small issue either. As this table, adapted from that published by HMRC, shows, the cost of pension tax relief over the last 13 years for which records are published is £509 billion (click for a larger :

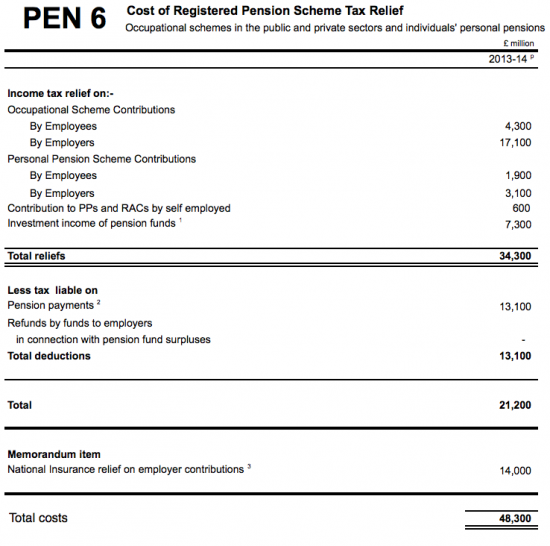

For the sake of clarity the data for 2013/14 alone was:

Now, I accept that if totals are considered some offset of tax collected is appropriate, (although of course much of the tax collected would have related to contributions from before this period, so the direct offset of tax against cost is not appropriate), but however looked at the cost of these reliefs in proportion to total government spending is enormous. In 2013/14 total government spending was £720 billion. And let me be clear, the taxes on past pensions would have been received in that year in almost exactly the same amount if no new tax relief had been given. So, the next effect was that a subsidy of £48.3 billion was given to the pension sector, equivalent to 6.7% of all public spending. To put this on context, defence spending in the year was £40 billion, housing and environment spending was £21 billion and public order and safety cost £31 billion.

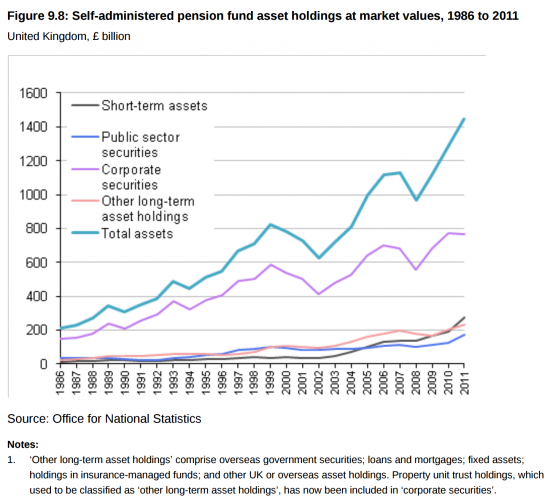

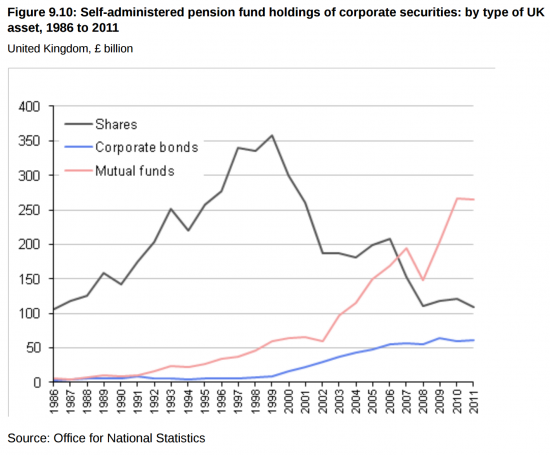

The latest reliable data I can find on allocation of these sums comes from the ONS in Pension Trends — Chapter 9: Pension Scheme Funding and Investment, 2013 Edition. There the mix of assets invested in the largest category of pension funds is shown to be as follows:

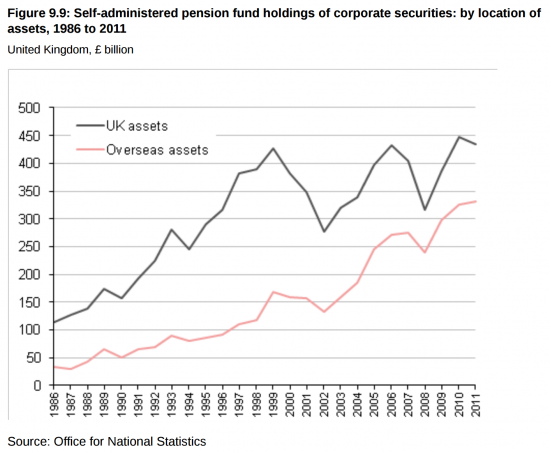

There was a flattening in corporate exposure post 2009, and this figure includes bonds and equity with overseas holdings growing significantly over time:

This is a trend seemingly associated with a growing use of mutual fund investment:

Now I stress that I know that this is not the whole picture on pension fund investment, but what seems to be fairly obvious is that the trends that are occurring are broadly towards increasing financialisation, less direct engagement with UK corporates and an increasing international diversification to the point that the obvious question has to be asked, which is what is in this for the UK government and what now justifies its massive spending on pension subsidies?

To put it another way, why are we willing to spend £48 billion a year subsidising the financial services sector in the UK and abroad when doing so is not resulting in funds being used to, in almost any way, fulfil that fundamental pension contract that I outline above?

And why, at the same time, are we tolerating the use of those funds to a) support the increasing financialisation of our society b) support activity largely based in the south east of England c) increase wealth divides in society, which is what this process, inevitably, does?

I can no longer find reasonable answers to those questions. I stress, I am not alone in doing so: George Osborne is floating the idea of an ISA based pension with substantially less tax relief given. There does, however, remain a problem with that: the fundamental pension contract that requires we pass on real assets - houses, infrastructure, functioning businesses, knowledge, intellectual knowledge and the mechanisms that support all these things - is likely to be even more ignored in a personal ISA based pension than it is at present.

And so let's go back to the China problem. China's boom was caused by people seeking to save in mechanisms of which they had little understanding with outcomes that were uncertain, risks hard to calculate and a likely mismatch with their real need. I am sure there will be many suffering significant losses as a result. But they are in much the same position as a result as the many in the UK who bought endowment mortgages and who now look at their pension savings and wonder 'why did I bother?' Those products have also failed to meet need for almost exactly the same reasons, and one of them has been subject to considerable tax inducement. No wonder economies are going wrong. Fundamentally a massive game of deception has been played on millions, and probably billions, of people and the consequences are becoming clear: the pretence that we were providing for anything with our savings was just that, a pretence. And it all happened to ensure that the financial services sector got rich in real time.

It was for this reason that I suggested People's Pensions along with Colin Hines and Alan Simpson (then an MP) in 2003. The idea was simple. The government would create a pension fund, or funds, in which people could invest. This fund would then fund the creation of the assets that the nation needs to ensure that the fundamental pension contract was fulfilled. So it would finance the building of hospitals, schools, broadband for rural locations, insulated properties and invest in small business and high tech and so much more. The fund would attract tax reliefs: an ISA wrapper may work for investments in it. Alternatively, capital gains and income received from it, to a limit, could be considered tax free. And the fund would then work in partnership with (let's call it) a National Investment Bank, whose bonds it would buy and who would actually deliver the projects. The same National Investment Bank would also issue those bonds into the broader market for those who wanted to buy them: they would also be available for the purposes of People's Quantitative Easing when the government, via the Bank of England, believed it needed to stimulate the economy by increasing investment in these assets.

How would returns be paid? Three ways. First, by way of interest payment: that's hardly surprising. The government is used to paying interest on its borrowing.

Second, there would be a real current return on the investment: I think it would be entirely appropriate to designate local funds or sector funds so people could see that the money they were investing was linked to a real economic output. Nothing could make investment more comprehensible than that.

Third, there is, of course, in the long term a return to be paid as a state backed pension based on contributions. The mechanisms would need refinement, but given that government bonds have for decades underpinned the annuities used by private pension funds such an arrangement is completely normal. The important point to make though is that this pension could be economically justified precisely because the assets underpinning it would still be in use: this is a pension contract that reflects the inter-generational agreement that must underpin such arrangements with real assets.

How much could be spent a year on new investments? Well, let's start with most of that £48 billion, shall we? Its proximity to the amount I have suggested be spent on People's Quantitative Easing is just fortuitous.

The gains are obvious. First the fundamental pension contract would be recognised and be the basis for pension provision, for maybe the first time ever.

Second, the savings mechanism would be readily comprehensible, have low risk and be secure.

Third, a mechanism for increasing the flow of funds into the productive economy and away from the financial services sector - an essential part of rebalancing the economy - would have been created.

What's not to like? Ask the City. But for the rest of us this is all gain.

First this is a programme to deliver real investment.

Second, it redirects pension subsidy to public gain.

Third, it rebalances the economy.

Fourth it creates jobs in every constituency in the UK.

Fifth it creates an understandable savings mechanism.

Sixth, that mechanism reflects the fundamental pension contract that must exist in the macro economy.

Seventh, this provides a mechanism for enduring quantitative easing (call it PQE or otherwise; as I have now shown they're really the same thing) when it is needed.

Eighth, this is clear economic narrative that is straightforward to explain both as to the reason for its creation and as to its long term benefit.

And it's open to any political party to use.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

It’s the secondary sale of tokens that funds the pension scheme.

If I hold Token X as a pension saving, when I retire I sell a Token X to somebody who is currently saving for a pension, and then I spend the money the other person has saved. The income from all the Token X’s I stlll hold plus the ones I’ve just effectively sold to somebody else is what forms a pension in payment.

In other words the money I spend as retirement income comes from somebody else who thinks they are saving for a pension. In reality Token X is just held by a pension company and they change the notional ownership in a database somewhere, depending how nominalised the investment pool is.

Essentially the person saving is ‘taxed’ (increasingly so since we now have ‘compulsory pension savings’) so that the retiree can receive an income. All the Token X holding bit is a charade to make the private sector think they’re doing something useful.

You’d get exactly the same effect if you just put up income tax, scrapped all the pension saving and increased the retirement pension (and made it graduated to reflect earnings).

Then all the pension middlemen can be let go and go off to relieve the skills shortage the CBI is always moaning about.

Pensions are always a current production issue. How much of current production should be reserved for people who have not been involved in creating it today, but have bequeathed a public investment pool by which the current production can occur.

But savings are a real and appropriate issue to address

They are, but you have to drop down a level and ask why are we saving, what is the purpose? Can it be done a different way (a better state earnings related pension – possibly with a capitalisation account at National Savings if people feel happier seeing a ‘fund’).

The problem we have is that we are saving too much and don’t really know what to do with it all. One approach is to come up with new savings vehicles. The other is to make people feel more secure so that they don’t feel the urge to save so much – which also then helps with the Paradox of Thrift problem on the spending/income side.

A fund is the next step

I’m getting increasing hysterical comments from people across the Internet when I explain how PQE works. What about risk free investments they cry. How will pension funds maintain their regulatory profile.

But their protests just indicate that the private pension industry *cannot* provide the required retirement risk profile on its own. It depend entirely upon government support and bailouts to provide appropriate pensions.

So what is the point of them being in the middle?

I am not saying they are in the middle

Where’s the pension industry in this plan?

I can’t see them in it

What do they add? Why are they there?

I can’t see them in the future either. They serve no operational purpose once they leave the primary markets for the financialised casino world. Liquidity provider for maturing executive share options isn’t appropriate or enough.

Just as the job of banks is to allocate debt to appropriate projects, the job of private pension funds should be to allocate equity to appropriate projects – possibly as liquidator of successful venture capital investment if such a route can be trusted to work properly.

But if the risk profile can’t be matched by that process then they just end up being overpaid tax collectors, and you lose nothing operationally by striking them right out of the middle and boosting the state retirement provision instead.

People’s Pensions was always designed as a new state second pension

It is the right direction of travel

Sorry liquidator is the wrong word. I’m not suggesting winding up. ‘Liquidity Provider’ is a better term.

This explains for me why the ‘boomer’ generation did not ‘eat’ our childrens future but it does indicate that the Thatcher generation could be accused of that.

“all the loans they create are made out of new money created for the purpose. They do not therefore, effectively, need deposits to make loans.”

You’ve lost me here, Richard. If this is true, why did Northern Rock go bust?

Because no one trusted their promise to pay any more

I have always said there is a limit to this possibility: everyone does

But it was not because it needed more deposits that it failed: it was simply insolvent because the trusty that is the basis of this process had gone

Forgive me if I’m being a little simple-minded here, but I don’t understand.

Why didn’t Northern Rock simply create as much money as was necessary to pay all those who wished to withdraw their savings? Thereby restoring confidence and trust.

You now seem to be saying that there is a limit to the process whereby banks can create money. But if the process was no use to Northern Rock — or any other bank in difficulty — then surely the utility of this money creation process is very limited indeed. What am I missing?

See exchange with Frances Coppola

There is ‘a limit to this possibility’ because banks have (regulatory) capital and liquidity requirements that need to be funded.

Northern Rock had got to a level where only 23% of their funding came from deposits and they had actually failed before the run by depositors.

Here’s a long but informative article on why (or more particularly, how) Northern Rock went bust.

http://www.princeton.edu/~hsshin/www/nr.pdf

And – to be genuinely helpful, here’s another one where the B of E “explains how the majority of money in the modern economy is created by commercial

banks making loans”

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q102.pdf

That should cover it.

I cannot see why there has to be any connection between a pension and saving or investment. SERPS was the perfect vehicle: working people paid in to fund payments to those no longer working – simple.

People will understand savings better if they see a link

This is about a new narrative on this issue

Simple if there are equal numbers of retired and working people. An expanding aged group being supported by a diminishing working group (who struggle more than the retired did due to a failed economy) is a problem.

Brilliant article and idea! I have just been looking into pensions and could not believe the tax breaks available for them, especially for higher band tax payers.

I do have one question though, with relation to bank lending you say this:

“all the loans they create are made out of new money created for the purpose. They do not therefore, effectively, need deposits to make loans”

I’ve heard this a few times but I thought with the introduction of Basel III that banks are now required to have a capital requirement of at least 4.5%, which I presume will at least partly come from saving deposits?

See exchnage with Frances Coppola which clarifies this

Richard, I’m afraid there is an error here, or maybe a difference of opinion about terminology. Deposits do not form part of bank “capital”. They are liabilities of the bank. Indeed, one of the principal reasons for increasing bank capital ratios is to protect depositors from losses, or rather (since most deposits are guaranteed) taxpayers.

It’s technically correct to say that banks can lend without pre-existing deposits. And it’s also true that banks create deposits when they lend. But the drawdown of deposits, including those created through lending, has to be funded. If a deposit is withdrawn something must replace it on the liability side of the balance sheet. That something can be another customer deposit (not created by the bank through lending, obviously), bond issuance, wholesale funding, central bank borrowing and of course equity (capital).

Usually when we start talking about banks not needing deposits in order to lend, someone mentions Northern Rock. NR actually didn’t rely on deposits for funding. Its principal funding method was bond issuance – the proceeds from securitisation of its mortgage loans. When the securitisation engine started to falter in 2006, NR became increasingly reliant on wholesale funding as securitisations took longer and longer to reach the market. NR’s rising liquidity risk didn’t go unnoticed by markets, which raised the price of wholesale borrowing significantly over the last 6 months before its failure, adding to its problems. The proximate cause of its failure was the ABCP market freeze in August 2007, but the underlying issue was the balance sheet fragility caused by over-reliance on securitisation for funding. This is why banks need deposits. They are stable funding.

Technically I agree with you

If I did imply a deposit was capital that is an error

But it is also true money ceases to belong to the customer when deposited: it is not protected in a client account

So they are funding: that is what I meant using the term capital in its broader sense

PS I hope you note all I have put up on the lack of BoE independence and trust that debate is over now

Yes, you are correct. Money deposited in banks is lent to them: depositors are creditors of banks, rather than banks being “custodians” of their money. It’s just that when we talk about bank “capital” we usually mean the various forms of equity and subordinated debt that protect depositors from loss. I was concerned about confusion.

I shall catch up with your pieces on BoE independence. You post a lot!

Both fair comments

I’m so glad that I worded my previous (Northern Rock)comment carefully – and, for those who may have missed it, this scholarly article comes well recommended:

http://www.princeton.edu/~hsshin/www/nr.pdf

“Seventh, this provides a mechanism for enduring quantitative easing (call it PQE or otherwise; as I have now shown they’re really the same thing) when it is needed.” This is a really excellent idea and gets round the problem that has always worried me, that PQE would be disastrous when it stops!