The TUC published a report called 'The Missing Billions: The UK Tax Gap' this morning. I'll declare an interest now: I wrote this report.

It's message is simple, but based upon a mass of research in HM Revenue & Customs data with regard to individuals and in the accounts of the 50 largest companies in the UK with regard to corporate tax. The simple fact is that tax avoidance is commonplace and is costing, in my estimate, not less than £25 billion a year.

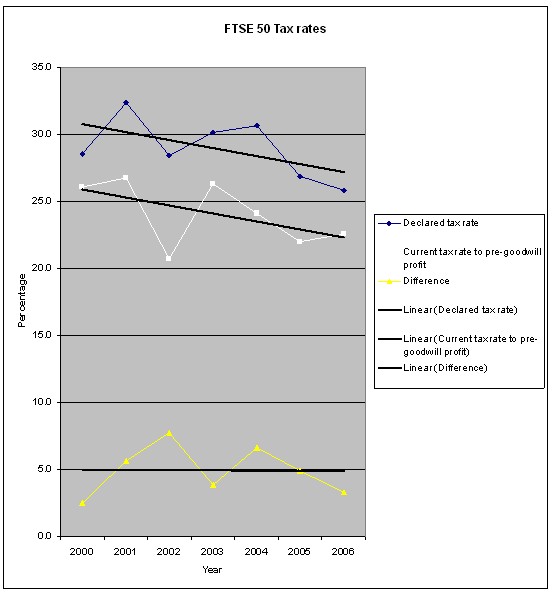

I'll stress now: people will nit-pick that number, and they're very welcome to do so. I'll write more on them later. What I will say is we intended that number to be cautious, and despite that it is big: very big. And it comes in two parts. The first bit is corporate tax avoidance. This graph tells a lot of that story:

Based on detailed analysis of the accounts of the fifty largest companies in the UK I show that their effective tax rates fell from 26% in 2000 to to 22.5% in 2006 - a fall of 0.5% a year. And, they always pay 5% on average less than they declare on the face of their accounts. That's not just tax planning: this is systematic avoidance on a grand scale. Amazingly, when their headline rate of tax is cut by 2% this year many large companies will begin to pay tax at lower rates than small companies in the UK - whose tax rate is on the way to 22%. That's a big issue to resolve, and one that even the CBI can't dismiss as being simplistic: it's a fact. Extrapolate the loss over just the biggest companies in the UK (and to be cautious, that's all I did) and the loss is now £12 billion a year.

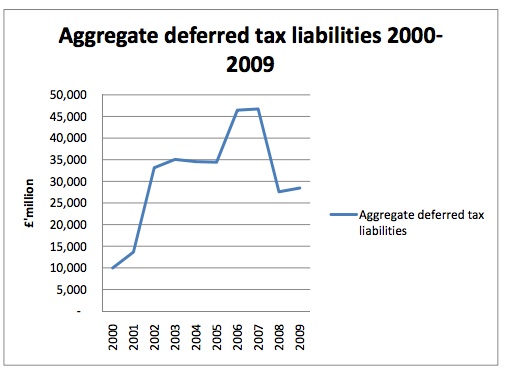

The evidence is available in these companies own accounts. Over the period I surveyed the deferred tax in the accounts of these jumped enormously:

To put this in context, that figure for 2006 means there was more deferred tax on the balance sheets of just 50 UK companies in that year than was paid in total corporation tax in 2006. There's nothing illegal in this pattern, and of course changes in accounting have had some role to play, but let's also be clear: deferred tax should reverse. It is not. It is rising, continually and whilst that is the case there is tax avoidance and not tax planning going on. A permanent deferral is tax not paid by any name one can use. All of which suggests that far from the largest companies in this country being overtaxed as they claim, they are perhaps the only sector to have seen a steady and substantial cut in their effective tax rate this century.

The rest of the report deals with personal taxation avoidance. The biggest part is domicile, where I continue to believe that the amount of tax lost because the government will not really close this loophole creates a tax loss of more than £3 billion. And the next biggest part is income shifting. I spent lot of time studying HM Revenue & Customs statistics to prepare some of the estimates in this report. And I found some extraordinary facts. Over 30% of all UK capital gains are, for example, paid by people with no income tax liability or who pay income tax at 10%. I found that the lowest half of the income scale in the UK have almost as much investment income as the top half, when we know the vast majority of wealth is owned by the top 10% of all households. And so on, and on. To put it simply, the statistics told me one thing: income shifting in private limited companies is just the tip of this issue. The Revenue say that's worth £250 million. I estimate (and again - I stress, estimate) the total cost of income shifting of all sorts to be £3.2 billion. It's more when you calculate NIC lost. And to be cautious I excluded all income shifting within partnerships and by the self employed not using companies.

This gives rise to a question: why in that case is the government only tackling income shifting in a small number of private companies when the evidence is that this is a small part of the problem and it is allowing most income shifting to continue unimpeded? Put another way, why is there such a bias against earned income in our tax system when the rules on investment income and capital gains tax are so readily open to abuse, and are abused as a matter of fact, apparently without concern arising?

Just as the corporate tax loss poses big questions, so too does this personal tax loss. We know the government is going to be short of cash. We know there is pressure for fiscal measures. We know there will be pressure on public services. We know there is pressure on public sector pay. We know that to tackle these issues involves choice. The report is there to show that there is choice available in the tax system. Not tackling tax avoidance is a choice. It is in no small part a decision to allocate resources to the wealthiest in society. And I have offered a range of options on how to tackle that issue, some of which I will refer to over the next day or so.

You can argue about the detail of this report if you wish: I won't be much inclined to do so. I am interested in the policy options it presents because right now they are by far the most interesting dimension. But most of all this report asks one big question, which is do we have the desire to collect tax from those with the capacity to pay it? I'd love to think the answer was 'yes'.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

[…] Toynbee has written about tax today for the Guardian, no doubt inspired by the new TUC report on the subject that I wrote for them. As she […]

[…] was on the BBC’s Today programme this morning and addressed the policy issues that my report for the TUC raises. Mike Warburton was the respondent. You could summarise his argument as ‘there’s […]

[…] it would help stop further deterioration in the effective rate of tax paid by these […]

[…] of the most unexpected spin offs from my work for the TUC has been its use in a study of reactions to the report amongst younger people, now reported on the […]

[…] just one problem with their argument: as I have shown their tax rate over the last seven years looks like […]

[…] contempt for small business: the CBI call for the same rate for large and small business when, as my research has shown, large companies pay an average rate 7.5% less than the nominal rate imposed upon them. […]

[…] billion form anti avoidance measures, most aimed at companies. This, of course, is welcome, but we’ve a long way to go in thta […]

[…] estimate that tax avoidance has reached £41bn – even more than the TUC’s estimate of a missing £25bn. That money is syphoned off by the same very clever accountants who pump out press statements […]

The logical conclusion to everything you are saying is that the government’s should rely on land value taxation as its primary source of revenue ie an annual ad valorem tax on land based on its assessed rental value.

[…] They point out that those seeking to get round the government’s proposed new rules for taxing the foreign income of companies by moving to Ireland are tax avoiders, increasing the Missing Billions. […]

[…] CGT allowance. This might easily raise £1 billion: I suspect rather more since I have shown in the Missing Billions that 17% of all capital disposals are of assets held for less than a […]

[…] Never say it isn’t worth campaigning. […]

[…] in the New Year we’ll also be doing work on post offices and housing, but we could also be campaigning on tax evasion or rip off credit or making climate change history. So this is a call for your help to ensure we […]

[…] Annual cost of Tax avoidance to UK Economy? £25 billion […]