This comes from page 182 of the Kindle edition* of the new Bank of England book on economics, which is in the chapter explaining the virtue of banking:

The implications are:

a) Money is tangible when it is not;

b) Banks lend other people's money when they don't; they always create loans out of thin air;

c) Banks are intermediaries when they are not, which the Bank of England has acknowledged since 2014.

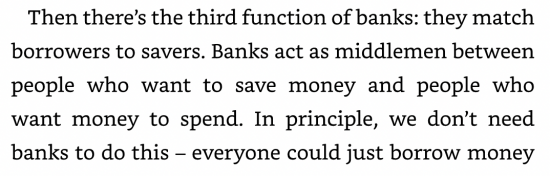

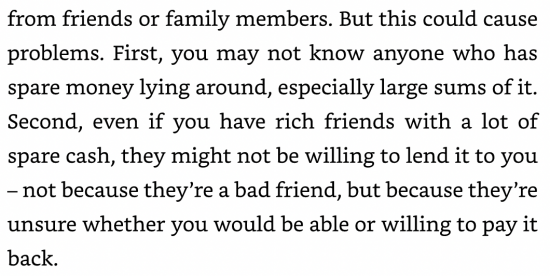

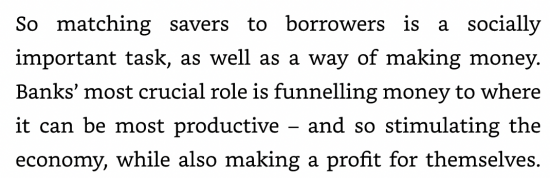

I admit that in the previous chapter it was explained that banks could and do create money out of thin air. But then we get his nonsense - which heads straight back to the old textbook teaching about banks as intermediaries. Not only does this contradict the previous chapter (never a good idea in a book) it is also wrong. Banks in the UK - the target audience for this book - do not act as intermediaries. They never match savers and borrowers. The suggestion that they do so is just wrong and is deeply misleading.

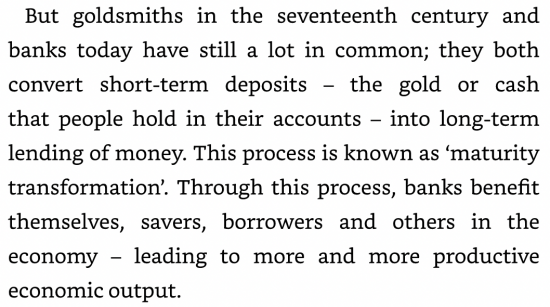

And this is not a one-off mistake. On page 190 they say:

And on page 191 they say:

This is just drivel, to be polite. If banks do not need deposits to lend - and they do not - then this is total nonsense.

The Bank of England really should understand banking before they publish a book about it.

And for the record, they should follow their own advice. In 2014 they said in an article:

This article explains how, rather than banks lending out deposits that are placed with them, the act of lending creates deposits — the reverse of the sequence typically described in textbooks.

Now they have published their own textbook and then have done so using the out of date model of banking that they condemned as wrong in 2014. It's very hard to make incompetence on this scale up.

And, for the record, they also don't understand money. They never once note that it is a record of debt.

This is really grim stuff.

* Bought so that I could screenshot it.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

….or done deliberately to confuse matters?

A rearguard action against growing MMT/QE theory and practice?

Obfuscate?

To make sure that TINA?

To rob us of hope?

So that they can use the tax bonanza to bribe people in 2024 with tax giveaways?

They are all in on it – the BoE, Treasury and the Government.

As the saying (from various commentators over the years) goes, “It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

The authors of the BoE tract were perhaps directed in their writing by seniors at the bank? This would be dishonest, but the alternative is more worrying because it would mean that two experienced economists had somehow worked their way through academia and into relatively important roles at the BoE despite their thorough incompetence in the field.

I mean, they can’t really have got everything so wrong without deliberation being involved? Surely not?

I tend to agree with you

Use of the goldsmith is especially egregious. They are using the notion of a commodity money. But this is not the system we use, which is a fiat currency system with flexible exchange rates. We haven’t used a gold standard system since 1971 when Nixon unilaterally and without took the world off Bretton Woods. The Bank should be aware of this. This is incompetence of a very high order.

Sorry: commodity money system.

People who want and need money to spend, and may have little of it, includes those who do not have bank accounts, do not trust banks or are not considered good credit risks by banks. They rely on the free circulation of notes and coin to survive or thrive; notes and coin offer a much better way than banks, indeed in some cases the only way, for the poor to access money to spend – and support businesses in their community, and support the general economy.

* Bought so that I could screenshot it: and read as a public service so that your readers did not have to. It certainly is awful. As you contend, it is very hard to make incompetence on this scale up. I would have hoped it would be nigh on impossible, but not so with Johnson in office.

I’m assuming from the style and form of writing in the quotes you provide that this is a textbook for school children (e.g. GCSE), Richard? Certainly your excerpts are not degree level material – or not in my experience, at least.

And given that you say that the text in one chapter contradicts points made in another I wonder whether that’s because some sections have been cut and pasted from previous (in this case pre 2014) material and then not picked up by a decent copy editor (or maybe they didn’t bother with one).

But whatever the reason, what an absolute shambles of a job from people working for an organisation like the BoE.

It is meant for the ‘lay person’

As I noted yesterday, it is deeply patronising

The problem with the money system we currently have is that it is not so straightforward to the outside observer, so it gives this kind of room for such tortuous interpretations.

It is true that banks create new money when they lend and they certainly do not need deposits to do that. The obvious question then is why do they seek deposits if they don’t need them to lend? The real reason is that deposits made with them are the cheap form of borrowing, it keeps them topped with reserves they need to pay other banks,(or lend out on the interbank markets if they have a surplus) or satisfy customer cash withdrawals. Deposits in effect are just a cheaper form of borrowing, cheaper than from the central bank or other banks.

For the BoE to keep muddying the waters is not at all helpful. But its what they have done for the past 400 years and they don’t like us knowing their big secret. Even when that secret it is out of the bag they still try to obfuscate.

You are right: deposits are cheap capital that put the account holder at risk, excepting the government’s guarantee for which the banks do not pay

Isn’t the FSCS funded by levy on the banks etc? Thats what their website says.

It is underwritten by the government

Richard

is there any chance of opening a dialogue with the authors ?

perhaps through the Daily Mirror ?

I m considering this

This is a good idea.

Someone from the bank must tell us which set of statements is true: their new book or the Money Creation bulletin from 2014. Because they are in absolute contradiction to each other.

Don’t forget The Bundesbank in 2017 also published this:

“when a bank grants a loan, it posts the associated credit entry for the customer as a sight deposit by the latter and therefore as a liability on the liability side of its own balance sheet. This refutes a popular misconception that banks act simply as intermediaries at the time of lending – ie that banks can only grant loans using funds placed with them previously as deposits by other customers.”

https://www.bundesbank.de/resource/blob/654284/df66c4444d065a7f519e2ab0c476df58/mL/2017-04-money-creation-process-data.pdf

Really quite an embarrassing moment for the BoE to have proudly published contradictory statements, both still available to view.

I will ask them for a statement…

Amusingly the BofE themselves in their 2014 PDF say this: “”… Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks.”.” a tradition they seem keen to continue 🙂

Further, The BofE’s very own Michael Kumhof has been researching the subject of money creation, and in this video on the subject he makes the significant observation, “Banks are not intermediaries of loanable funds” https://www.youtube.com/watch?v=OgsEyM82oCE

From the Norges Bank, “When you borrow from a bank, the bank credits your bank account. The deposit – the money – is created by the bank the moment it issues the loan. The bank does not transfer the money from someone else’s bank account or from a vault full of money. The money lent to you by the bank has been created by the bank itself – out of nothing: fiat – let it become. The money created by the bank does not disappear when it leaves your account. If you use it to make a payment, it is just transferred to the recipient’s account. The money is only removed from circulation when someone uses their deposits to repay a bank, as when we make a loan repayment… To sum up: banks create money out of nothing and withdraw it when loans are repaid.”

https://www.norges-bank.no/en/news-events/news-publications/Speeches/2017/2017-04-25-dnva/

Here it’s the ECB’s [European Central Bank] turn to describe how money is created as debt by the privately-owned commercial banks, when they explain: “Commercial banks can also create so-called “inside” money, i.e. bank deposits – this happens every time they issue a new loan. The difference between outside and inside money is that the former is an asset for the economy as a whole, but it is nobody’s liability. Inside money, on the other hand, is named this way because it is backed by private credit: if all the claims held by banks on private debtors were to be settled, the inside money created would be reversed to zero. So, it is one form of currency that is created – and can be reversed – within the private economy.”

https://www.ecb.europa.eu/explainers/tell-me-more/html/what_is_money.en.html

Here’s the German Bundesbank explaining where money comes from, and that banks aren’t intermediaries as popularly imagined, “In terms of volume, the majority of the money supply is made up of book money, which is created through transactions between banks and domestic customers. Sight deposits are an example of book money: sight deposits are created when a bank settles transactions with a customer, ie it grants a credit, say, or purchases an asset and credits the corresponding amount to the customer’s bank account in return. This means that banks can create book money just by making an accounting entry: according to the Bundesbank’s economists, “this refutes a popular misconception that banks act simply as intermediaries at the time of lending – ie that banks can only grant credit using funds placed with them previously as deposits by other customers”. By the same token, excess central bank reserves are not a necessary precondition for a bank to grant credit (and thus create money)”

https://www.bundesbank.de/en/tasks/topics/how-money-is-created-667392

Here’s the Bank of Canada describing not only how money is created for the Canadian govt to spend into the economy but also how the private banks create money from nowhere, both as ‘loans’:

“Private commercial banks also create money – when they purchase newly issued government securities as primary dealers at auctions – by making digital accounting entries on their own balance sheets. The asset side is augmented to reflect the purchase of new securities, and the liability side is augmented to reflect a new deposit in the federal government’s account with the bank.”

“However, it is important to note that money is also created within the private banking system every time the banks extend a new loan, such as a home mortgage or a business loan. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money (see Appendix B). Most of the money in the economy is, in fact, created within the private banking system.”

“A key similarity between money creation in the private banking system and money creation by the Bank of Canada is that both are realized through loans to the Government of Canada and, in the case of private banks, loans to the general public.”

https://lop.parl.ca/sites/PublicWebsite/default/en_CA/ResearchPublications/201551E

The IMF step up: “To support the understanding that banks’ debt issuance means money creation, while centralized nonbank financial institutions’ and decentralized bond market intermediary lending does not, the paper aims to convey two related points: First, the notion of money creation as a result of banks’ loan creation is compatible with the notion of liquid funding needs in a multi-bank system, in which liquid fund (reserve) transfers across banks happen naturally. Second, interest rate-based monetary policy has a bearing on macroeconomic dynamics precisely due to that multi-bank structure. It would lose its impact in the hypothetical case that only one (“singular”) commercial bank would exist. We link our discussion to the emergence and design of central bank digital currencies (CBDC), with a special focus on how loans would be granted in a CBDC world.”

https://www.imf.org/en/Publications/WP/Issues/2019/12/20/Money-Creation-in-Fiat-and-Digital-Currency-Systems-48843

I had all this stuff just lying around 🙂 incidentally your link to the book in question is broken, it leads to an old Telegraph article.

Thanks…good stuff

I will look at the link

I actually did something I never normally do by reading Chapter 10 first, because it appeared to purport to answer the question posed by the title of the whole book. Indeed it does, but completely wrongly.

It really is very hard to understand why the Bank is putting out this nonsense that completly contradicts, as you rightly say, Richard, their own Q1 2014 bulletin that describes how banks really operate. I’ve put sticky tabs against 14 things that are totally incorrect and I’m not sure I am going to be bothered to read the rest. Maybe I’ll return it to Amazon.

What we need urgently, Richard, is your forthcoming book to act as an antedote to this poison. And it really does need to be very loudly exposed as a fraud.

The book is in progress, but a month late at present….

If banks don’t need deposits to lend, why did Northern Rock go bust? Will I loose marks in my essay next month if I don’t understand this?

Because they lent 125% of value of properties and ran out of regulatory capital

Correct me if I am wrong but was it not the Tories/Thatcher who lowered the ceiling for bank reserves held for a rainy day, and instead let this money be used for loans etc?

Not only did that have a deleterious effect on risk management but it was surely something bound to cause inflation?

Labour, I think…

Northern Rock in essence ran out of money. They loaned way too much. More than the other banks for the amount of reserves they actually held. This was in an age when bank reserves were relatively in short supply. It was a risky and aggressive position.HBOS had a similar businesses model. Then came RBS which was so huge it basically broke the British banking system as it was then. What we now have is a semi nationalised banking sector. Kept alive by a massive injection of state backed central bank reserves that has had the effect of making sure no bank now struggles to survive. Quite unlike any other sector. This is a highly protected and subsidised sector,one that still likes to pretend it is a real private sector business, laughable really. As Martin Wolf once said, bankers are in effect very highly paid civil servants. They are in effect implementing government monetary policy and should only be rewarded so.

Because Northern Rock’s banking licence would not allow them to lend and lend and lend forever without limit. They funded their long-term mortgage lending (often on assets that were not worth as much as the loan) by short term borrowing, and repaid the short term borrowing by selling chunks of their mortgage receivables, aggregating them together in chunks and selling them to a securitisation vehicle that issued bonds backed by the mortgage debts.

When the money markets stopped lending in the wake of the subprime crisis in late 2007, Northern Rock could not repay the short term borrowing because no one wanted to buy the mortgage backed bonds that would be issued by the next securitisation vehicle. The bank sought liquidity support from the government, which caused a crisis of confidence and led to a bank run when depositors withdrew their savings, but that did not kill the bank as such. It was the lack of liquidity. The government in effect nationalised the bank when they guaranteed its debts (about £30 billion of guarantees, on top of £25 billion of liquidity loans), and then actually nationalised it.

As I understand it, all the government loans were paid off in the end – it really was a problem with cash flow and liquidity, not the balance sheet – and the bank was sold to Virgin Money.

Just to add, Richard, as you’ve purchased the book, you’re quite entitled to leave a review of it on Amazon…

I should…

I have submitted this review to Amazon:

This book is written in a deeply patronising style, as if that is necessary when speaking to non-bankers.

It also fails to understand money. At no point does it say it is debt, which is the only short-hand explanation for what it is, and which permits it to be recorded in accounting systems. The claim is made that it is trust. You cannot do debits and credits for trust. You can for debt.

QE is incredibly poorly described, and its use to directly fund government – which is exactly what it did during Covid – is not mentioned.

Perhaps worst, the book actually says banks are intermediaries between savers and lenders – which in 2014 the Bank of England says is wrong and should not be in a textbook, but they have now issued one saying just that.

The whole book reads like propaganda for a failing economic system. It is deeply unreliable.

Is the book “Can’t We Just Print More Money?: Economics in Ten Simple Questions”

by Rupal Patel, The Bank of England, et al. | 19 May 2022? I ask as nowhere on this page does it say and the link I mention above still goes to an irrelevant Telegraph article.

Sorry – I am human and busy

It’s pulished by Cornerstone Press which is where I ordered it. Search their website. It actually came from Amazon, but a search on their site didn’t find it. It might do now.

It’s there with Richard’s published comment.

Well, Richard’s review is showing.

Alongside 3 other ‘5 star’ reviews from, erm, anonymous folk who have never previously left a review on the Amazon system. Not at all dodgy or suspicious. No, of course not.

I should mention that I don’t think I’ve ever left a review on Amazon, despite many purchases there over many years. I suppose that these reviews could be ‘legit’, but I am willing to eat my full selection of headwear if they are.