I posted this Twitter thread yesterday. As it was actually written on Twitter I do not have a text version to share:

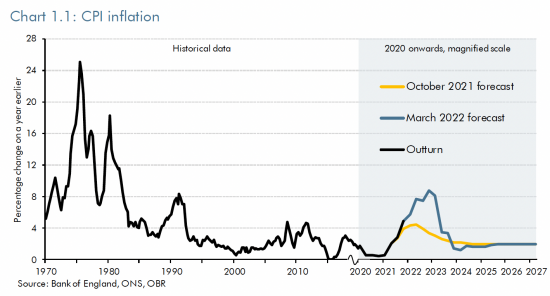

The OBR forecast for inflation I refer to is here:

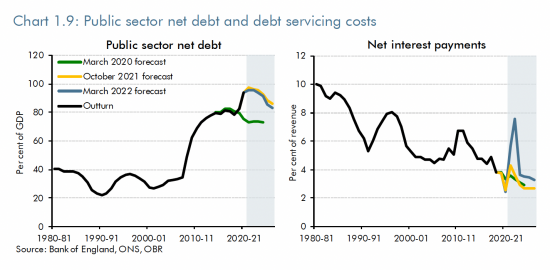

And this is their forecast of interest costs, on the right:

As is apparent, they know that the current claimed cost is a spike that will reverse when the ridiculous accounting assumptions used to underpin it are reversed - as they say they will be.

So why is Sunak using this as an excuse to withhold billions from those facing poverty? It can only be deliberate. And that is unforgivable because even if he had to include the figure in the accounts he could also ignore it - simply dismissing it as the accounting stupidity it is. But he is not. He's using it to punish people instead.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Again, yet again we have ideology trumping reality. I was however interested in Sunak’s evidence before the Treasury Committee, where he admitted that Brexit was having a negative impact on finances and productivity. Small steps…

For those coming to this topic afresh, I refer to the couple of previous posts on this topic in recent days, particularly Clive’s explanation in the second, as to why this “interest” is illusory.

* https://www.taxresearch.org.uk/Blog/2022/03/25/the-government-is-forecasting-a-big-fall-in-its-interests-costs-just-as-it-wants-to-give-tax-cuts-in-2024/

* https://www.taxresearch.org.uk/Blog/2022/03/23/the-chancellor-may-overstate-necessary-government-interest-costs-by-up-to-30-billion-today/

I like your simplification of discussing what happens with a nominal £100 of gilts.

The OBR may be wrong, of course. They often are. That is the nature of forecasts, but they stopped publishing those graphs showing how consistently wrong their previous forecasts were (that is, consistent wrong in the same direction, reflecting an underlying bias).

Such as productivity. https://www.taxresearch.org.uk/Blog/2021/10/28/the-office-for-budget-responsibility-is-a-really-terrible-economic-forecaster/

Or GDP. https://fullfact.org/economy/budget-forecasts/

And if this sort of basic number goes wrong, so does everything else.

Agreed, and thanks

A very good thread to explain an obscure, technical but IMPORTANT issue. Thanks.

To people who don’t get it I tend to just ask the question. “So, who received all this interest?”. When they can’t identify anyone then I say that “nobody received it because it was never paid”.

The next question is “why does the ONS print this number?” to which I answer “because they get confused between principal and interest. I accept that principal owed has gone up due to inflation but interest costs have remained broadly unchanged.”

The reply is then “well, we will all pay in the end”…. but I respond “yes, but timing, orders of magnitude and future revenues matter

(1) Why austerity/suffering now for something that, if it is a problem at all, is a problem 20 years down the road.

(2) Rishi Sunak may say Interest costs have doubled. I say they the level of debt has risen by 1% of GDP due to a 4% rise of inflation. 100% sounds alarming, 1% does not.

(3) Also, higher inflation means higher tax receipts. If we want to get really clever we could argue that higher inflation is reducing the national debt (but that is another story).”

… and if it is all too complicated EVERYONE can see that the “rabbit out the hat” that will be produced for Tory voters next year is at the expense of the poorest today. Shockingly cynical.

Thanks Clive

““yes, but timing, orders of magnitude and future revenues matter”

Not only ‘matter’ but but the essence. This is the key point I believe most people simply do not understand about ‘money’, and the whole money system. This issue and its significance is perhaps the least understood by the public of all monetary matters.

Oh yes….

The promise to pay might not be right now.

tis, presumably , is the reason he was rubbishing the OBR in media interviews.

There is very little to add – this has also been pointed out at the recent select committee.

‘Do you think people are stupid?’ Sunak was asked.

Well, evidently enough of us are it seems.

No, we’re not all stupid in much the same way that we’re not all accountants. I for example am a mechanical engineer who has spent most of his life working in manufacturing. If you want chapter and verse on the failures of parts of British manufacturing primary amongst them myopic, narrow-minded and frankly incompetent management I have a wealth of experience.

To assume that we’re all stupid is to assume we’ll never understand and once you assume that, you stop trying to get the point across. For me at least, that would be a pity as I come on here to try and understand some of the mechanics behind what I intuitively know, which is that the current manifestation of the Tory Party is a moral and ethical vacuum quite content to deliberately inflict hardship and poverty on millions of my fellows in order to bribe the gullible, credulous and feeble-minded to return them to office in order that they may continue to drive the accelerated decline of this country.

The Chancellor’s performance at the Treasury Select Committee revealed what a glib, gauche, product of the corporate, apparatchik world. He attempts to show his mastery of detail that quickly breaks down under any close questioning; Alison Thewliss MP on pre-paid meters. Sunak passed off one solution for 60% of this population, only to require to change that to 40% under scrutiny. A solution he proposed to accomplish for people with direct debits and pre-paid meters; said completely without irony.

In the middle of a world crisis on multiple fronts (Covid, Brexit, war in Ukraine and a watershed in modern history); and he is so lost in the detail of his budget he thinks the problem can be reduced to an issue of the nuances of a ‘taper’.

Ludicrously he made a comparison with WWII, and the need to ‘pay the bill’ for the support through the Covid pandemic. There is the problem. He has declared a victory, but a victory over what? There was no ‘unconditional surrender’. There is no measure of what counts as ‘victory’, save the opportunism of a chancer. This is rather like the Conservative declaration of the end of ‘austerity’. Remember that one? Their goal was the elimination of the deficit and the reduction of the national debt. They failed to eliminate the deficit, and the national debt sharply increased. They declared a victory anyway. They didn’t understand economics then, and they do not understand economics now.

The Covid pandemic is not over, and we do not know the scale of the danger it still carries. Worse, the economic impact of Brexit is still working through. Worst, the world has been changed forever by Putin and Russia in Ukraine. Sunak has gratuitously declared a victory in the middle of the war. Chancellors do not tell Prime Ministers to surrender because he doesn’t have the budget to pay for the war. You fight the war and win it; then you pay for it. You declare a victory when the Pandemic is over, when the Brexit economic problem is (somehow) fixed, and European crisis is over, and a new order has secured Britain’s future. You do not allow a box-ticker to declare a victory, and make it far less likely; just because he is out of his depth.

I can see what you’ve done here. You’ve looked at two charts, assumed correlation equals causality and done no other research. You haven’t even read the chart properly – which would have helped you.

In doing so you’ve got your first thing wrong.

The chart showing Net interest payments shows them against percentage of revenue. This is rather important. As guess what – revenue fell between 2020 and 2022 because of the pandemic. Which accounts for the spike you are seeing. NOT some accounting due to inflation linked bonds – which is a story you’ve had to make up to suit your own version of events.

Which takes me on to the second thing you get wrong.

You are correct in saying there is a premium paid over the nominal face value for these bonds, but you go wrong from there on after. I quote “the Treasury is assuming in it’s budgeting is that the current inflation rate is going to continue until all these bonds mature” and “There is instead just what’s called an accounting provision for those possible costs”

This is incorrect. Treasury make no provision for future inflation and account for inflation linked bonds at current market prices.

What makes your logic even crazier is that the OBR inflation forecast shows inflation falling in 2024. If the OBR has this forecast, and the Treasury uses this forecast, then your claim that the Treasury is assuming current high inflation rates going forward is clearly nonsense.

You’ve made up a story to suit your own agenda and argument. It’s a shame that you get basic things so tragically wrong making your argument moot and your article nothing more than propaganda.

There would be a shred of credibility to your claim if they weren’t forecasting a massive provision for costs that will unwind, which they are

In other words, you are wrong

Try reading the chart and understanding what it means

You say – “The chart showing Net interest payments shows them against percentage of revenue”. Correct, you have read the label on the axis.

However, if you care to go to the DMO and ONS websites (and I have and I am a Government Bond trader by profession so have a clear understanding of these issues) you will see that the spike is there in nominal money terms. Moreover, that spike in money terms is identically equal to the inflation uplift on Index-linked bonds… because the ONS says it does.

Therefore, your assertion “Which accounts for the spike you are seeing. NOT some accounting due to inflation linked bonds” is just plain wrong.

So, unless the uplift due to inflation (which the ONS bizarrely includes as interest) continues at 6% per annum then the ONS version of interest paid will fall…. and remember, for inflation to fall it is not required that prices fall – merely that they stop rising so quickly.

Agreed

Thought experiment: let’s say we have say 8% inflation this year, so the principal repayment – due in 50 years time – is inflated from £100 at issue to £108, but then zero inflation until redemption of these bonds. What would the redemption price be then? And then remember, the issue price was £356 per £100 nominal.

None of the increase in the premium is paid today, of course – nor indeed for 50 years – but the Treasury is booking the whole of the increase today and calling it “interest”. If you do want to provide something each year for the inflated principal, perhaps each year’s increase (or decrease) should be spread over the remaining life of the bond. This is a bit like a weighted average over time, to compare to the implicit yield on issue. So that would be 8/50 = £0.16 (and the same next year, and so on for 50 years).

You’d also need to take account of the 0.125% interest, and the nominal yield at issue of -2.39% each year, Until the bond is yielding 2.39% for each and every year it exists, the ultimate payout is less than the premium on issue. If inflation really does drop below 2% for a long time, the bump today will disappear.

I have so many articles (and a book) to write I can’t do this….

Anyone got the time?

@ Clive

Inflation linked bonds are indexed. So for your claim to be right the index would need to fall by ~6% for the uplift to drop out of the ONS accounting.

Which means deflation. Not lower inflation. Positive inflation would mean the index would still be increasing.

It’s also pretty obvious that the ONS have never been accounting for linkers in the way you and Murphy suggest. If they had interest payments as a percent of revenues would be much higher thanks to the continual uplift.

Not sure you are (or more likely were) a very good bond trader if you don’t know the basics.

The numbers don’t help you either. There is no massive inflation related uplift in the monthly debt interest payments – which you would expect if what you and Murphy are saying were true.

https://tradingeconomics.com/united-kingdom/interest-payments-on-government-debt

Gautam is right. All that has happened here is that government revenues have fallen thanks to the pandemic, which is what is creating the spike in the chart which you people don’t seem to understand. Basic maths is all there is at play here – you have a smaller denominator for a brief period.

With respect (but not a lot) the ONS explanation for increased interest costs reported month in month out (that you appear not to have noticed) make clear that this is down to the provisions we are discussing

And since government revenues are rising in 2021/22 when the spike is on the chart your claims there are also just wrong

In other words, everything you are saying is just wrong, to be kind. Why not check your facts before making a stupid claim? I mean – do you realise by how much the denominator would have needed to fall to achieve this impact with a constant spend?

Sorry, that was meant to be a simple exercise for the reader! If inflation is zero for the next 50 years then the bond repays the current principal. 108. Which is very much below the issue price. So why do we currently recognise all 8 of that “interest” in year one and then nothing for 50 years until redemption?

Impossible to say

Sunak pretending he knows what to do in a supermarket and not able to say what the price of bread is or how to pay by debit card says it all.

… in answer to Andrew.

Investors paid £356,000 for bonds with “face value” of £100,000 and real coupon of 0.125%.

If inflation is 10% this year and zero there after the bond will repay £110,000 at maturity and interest of £137.50 per annum (ie. £125 x 110%).

To me, the accounting is simple – the interest is £137.50 a year. Full stop. Now, I accept that this is not the full story becuase the redemption amount will rise with inflation – but that is not interest and if you try to treat it as such you get that absurd spike on the ONS chart. The increase in principal outstanding due to inflation needs to be recorded as just that – an increase in the debt outstanding.

If I may head off into the long grass, here……

In round numbers our GDP in GBP 2trn, size on conventional gilt market is £1trn, size of Index linked gilt market is £0.5 trn. Govt debt as % of GDP = 75%

Assume GDP growth of zero, inflation of 10% and no budget deficit.

New GDP will be £2.2trn (remember, zero GDP growth means zero REAL GDP growth)

Size of conventional gilt market is unchanged at £1trn. Size of I/L market rises by 10% to £0.55trn.

Government debt as % of GDP is now 70% (DOWN from 75%)

So, inflation is REDUCING the debt burden!!

I suppose my real point here is that this is a complicated area and the data requires careful handling.

For info, you can recover the thread as text. Just reply to the last tweet in the thread with “@threadreaderapp unroll please”.

@threadreaderapp will then reply to you with all the text, which you can copy to here.

Someone already did that – https://twitter.com/threadreaderapp/status/1508511016052838404?s=20&t=h1nAYn0pWv9evR687eYr8w

You can – but it’s harder if you write it

Sorry Richard, I thought I’d done it with my own thread, but too long ago to check!

Maybe it works if you paste a link (say to the first tweet in your thread) into the box at https://threadreaderapp.com. It doesn’t know who you are.

Ah! Thanks

@Mike

You are right. After 30 years a Government Bond Trader I have now retired.

I think the “Trading Economics” website you reference merely relays the ONS data…. which is misleading. You need to delve into the “Gilts in Issue” data from which you can calculate conventional gilt interest, I/L gilt interest and I/L uplift. The number that ONS publishes as “interest” is the sum of these three.

The ONS erroneously (in my view) includes the inflation uplift as “interest”. They explicitly say this in their publication. So, if inflation next year were zero then there would be no uplift and the ONS measure of interest would fall. That is just simple arithmetic.

The real underlying position is that interest costs are stable due to a long period of low rates and that it will remain so due to the long duration of gilts in issue.

Of course, the uplift on principal amount is not unwound… but unless you think annual inflation will stay at 6% for several years then the ONS Interest figure will fall.

Your point about “denominators changing” is correct. It does exaggerate the spike to some extent but the spike is there in cash terms not just % terms.

Over at Progressive Pulse, they’ve linked to a similar analysis by (don’t laugh) Julian Jessop, former chief economist of the IEA.

* http://www.progressivepulse.org/uncategorized/is-sunak-losing-friends/

* https://julianhjessop.com/2022/03/29/is-the-uk-government-really-about-to-spend-83-billion-on-debt-interest/

He refers to an OBR table which sets out the one-off peak in accruals for index linked gilts in black and white: table 3.19 here: https://obr.uk/docs/dlm_uploads/Fiscal_Supplementary_Tables_Expenditure_March_2022.xlsx

Thanks

Tweeted now

Just to say, as Euan Monaghan on Twitter pointed out, you can copy and paste the thread text from Thread Reader:

https://twitter.com/euanwhosearmy/status/1508793142501326853

https://threadreaderapp.com/thread/1508461110944534538.html

Thanks for the posts, a lot of it over my head but it’s good to get the gist of it