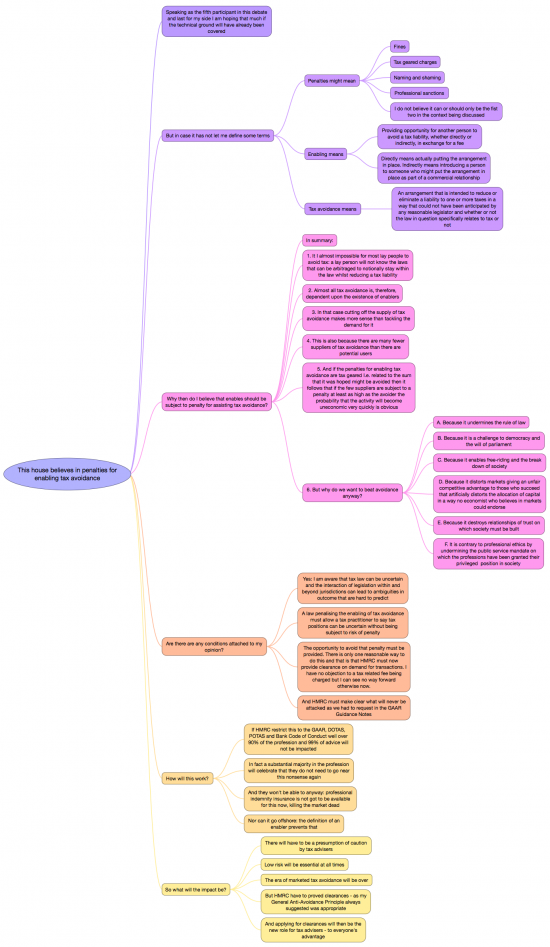

I took part in the first ever Revenue Bar Association debate last evening. The Revenue Bar is, of course, the organisation for tax barristers. The motion discussed was originally ‘This house believes in penalties for tax avoidance'. This, however, got amended so that two votes were taken, one on penalising tax avoiders and the second on whether the the enablers of tax avoidance (otherwise called the tax profession) should be penalised.

I regret to advise the Alexi Moustrous of The Times, Graham Aaranson QC and I, who spoke for the imposition of penalties, lost both motions, the second more heavily than the first. I also have to say I regretted having to listen to some of the quite outrageous comments made by one of those opposing us: some lawyers really do need to make it into the twentieth century sometime (that was not a typo).

These were my speaking notes, although I ended up pretty much ad-libbing what I actually said:

For a larger image click here.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Who spoke against you?

Lord Gold (David Gold & Associates)

Steve Edge (Partner, Slaughter & May)

David Goldberg QC

Goldberg made the comments I referred to

I’d love to hear what they had to say on the second motion.

No doubt your Quaker principles were severley tested. To your credit you seem to have passed. A lesser man such as myself would probably have been detained at her majesty’s pleasure for an indefinate period afterwards.

I went for a drinks and nibbles afterwards

As I said, you are a much better man………………

What is a “reasonable legislator”?

The test is already in the GAAR

I attended the debate last night, although I am a solicitor not a barrister. I thought a number of good points were made by both sides, and there was a (perhaps surprising) degree of agreement between both sets of speakers.

Little of the “against” discussion related to the motion – I think most people agree that people who try to avoid tax, and fail, should on the whole be penalised – but some strong points were made about the fundamental right to seek legal advice, and the conflict that can arise between a lawyer’s fundamental obligation to give their client the best possible advice on the law, and the possibility of heavy personal liability for advising in a situation where the client fails to achieve the expected tax result (perhaps due to faulty implementation by someone else).

Yet there was broad agreement that something needs to be done to discourage the inventors and sellers of egregious tax avoidance schemes, which on the whole do not work anyway (look the stream of cases lost by NT Advisors). I think you agreed that the proposals in HMRC recent consultation document go too far.

Unfortunately the motions were too black-and-white. Yes, some (perhaps most) tax avoiders should be penalised, and yes, some (but probably only a few) enablers should be penalised too. But both must be done in a way that is fair, proportionate and targeted.

I do think the proposal is unbalanced without clearances

I am not surprised the profession does not like the idea of clearances

I think their clients would, a lot

A matter of self interest, I think

Is there any equivalent in legal circles to the accounting concept of “substance over form”?

Individuals must, of course, be able to take legal advice on their tax affairs but where such advice promotes conspiratorial webs of Byzantine complexity it is surely immediately evident that a fiction is being constructed.

Lawyers have no appreciation of that concept

Much too sophisticated for their literal minds

Hey now, that may be true of tax lawyers but I think you’ll find that lawyers in many other areas are perfectly capable of totally ignoring the letter of the law!

S114 TMA 1970 would suggest, at least in its limited circumstances, that lawyers are well able to grasp substance over form.

Limited may be the operative word

Hi Richard, I’m a lawyer, but didn’t attend. From reading your speaking notes I don’t think there is much there for anyone (sensible) to disagree with. However, the main concern I hear amongst the very many lawyers I speak to about this proposal is that the definition of tax avoidance proposed by HMRC goes much much wider than the one you have proposed. If your proposal were used I suspect lawyers would be far more relaxed about this, but I am certain HMRC would not accept it because of your requirement that the tax benefit is something not anticipated by a reasonable legislator.

The answer, as I said at the meeting, is to make a submission

The other aspect is the professional conduct rules points. I must say I don’t have too much sympathy with this – lawyers have always been prevented from enabling their clients to commit a crime, so it’s not going that much further to extend the same principles to tax avoidance (but importantly this is subject to avoidance being properly defined).