The government has, within the last hour, published its statistics on the total tax take for July 2014. I have done a little number crunching.

Taking the first four months of the year take take from 2008-09 to 2014-15 has been as follows:

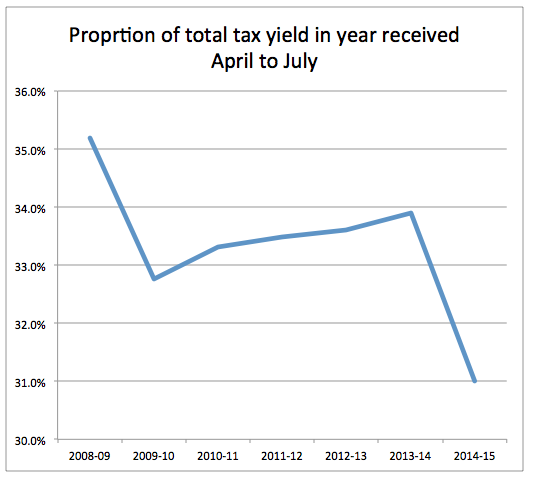

You would think George Osborne should be relieved; there is an upward trend.

That would be a deeply mistaken conclusion. Taking this data as a proportion of the total HMRC tax receipts for each year (using the 2014/15 OBR forecast here, table 2.8) the data looks like this:

On average from 2008-09 to 2013-14 33.7% of receipts were made from April to July. This year just 31% have been: a shortfall of 2.7%.

Total forecast HMRC receipts are £513,600, which I have always considered optimistic. The July shortfall suggests an undershoot of £13.9 billion.

Assuming all other forecasts remain as stated this would increase forecast borrowing this year from £83.9 billion to £97.8 billion - more than last year's £95.7 billion.

George has a very great deal to be worried about.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

One wonders where, if employment is so enormous, the corresponding tax take is. More clear evidence any suggestion of a recovery is illusory. But, I remind readers, we don’t want a recovery, instead we want a completely different economy, one which caters for the needs of the broader population rather than a few landowning and banking parasites.

George Osborne’s plan is to destroy the state by sweet heart deals to weathly individuals and to multinational corporations, less tax revenue and more debt equals less state and services to people, he’s using the shock doctrine tactics.

I agree

The evidence (from the ONS) is that the bulk of the new ’employment’ since 2008 has been self-employment, and low-paid self-employment at that – people like my window cleaner! He would struggle to find employment without his van and ladder, and Mum to help him with PAYE, NI, and other paperwork, as he’s learning disabled, and this wretched Government has closed all the Remploy factories. There are thousands of other disabled people of all ages who can’t get work who are being persecuted – benefit sanctioned on ESA – because there is no work for them, but the Government regards their unemployment as their fault.

The Government has this theory, you see – if a person is long-term unemployed, it isn’t the fault of society or the economy, but of the long-term unemployed individual. There must be something wrong with them: they’re lazy, or they’re alcoholics, or drug addicts, or inadequate or defective in some other way, and in any event content to live on benefits at the expense of the long-suffering taxpayer, and that situation must cease.

Hence the Government’s ‘anti-poverty strategy’, Universal Credit, the benefits sanctions regime, the benefits cap, etc. And hence Iain Duncan Smith’s recent speech where he claimed (on the basis of ‘evidence’ supplied by the Cato Institute in the US) that ‘welfare payments’ constitute a ‘disincentive to work’ and that reducing them will get people back to work. Bear in mind that there are more cuts to come – we have only seen the beginning. The hardship, misery and suffering, the burden on the Food Banks, the real hunger, the homelessness – it is all destined to multiply. THAT is what is going to happen if the Tories are returned to power next May.

Unfortunately, it may well be what will happen if Labour get in, too, given their enthusiasm for ‘balanced budgets’, spending cuts and Trident missiles. I view the future with a perfect dread.

Indeed-the ‘illogic’ that welfare payments are a disincentive to work is egregious (my mot du jour!).

If that were the case why on earth would some of the richest people on the planet keep amassing more wealth?

Mendacity and bovine scatalogy.

The REAL disincentive: A LIFE OF DEBT PEONAGE!!

@ProfSteveKeen Moment UK stopped reducing borrowing was point at which recovery began https://t.co/BU5IMgqqZk

It’s certainly still borrowing

But what about the deficit, the deficit?

Or is that concern an example of old fashioned 2010 thinking, like ‘no top down reorganisation of the NHS’?

In practice Osborne is on Plan B by default – he has just never said so

It’s just embarrassing that it now provides no cover for his attacks on the vulnerable

The question I pose is this: with overall tax take forecast to reduce as a proportion of expenditure (tax cuts, tax dodging, a low income economy producing less overall tax income) and with economies around the world borrowing money to meet the shortfall, what is going to happen when private investment and priveq is allowed to run riot when all public services are privatised because government say there isn’t enough public money to maintain them? With a decreasing amount of public money going to meet profit targets, shareholder demands, executive pay and bonuses and private equity debt, even less money will be spent on delivering actual services (for the most recent example see the Swissport fiasco at Gatport Airwick). With austerity hobbling the ability of people to move their money into the economy beyond their non-discretionary costs, how will private equity backed enterprises pay back their debts when they are receiving less money? When the creditors of nations want their money back and it isn’t there because tax money is being used to support other private wealth, what happens when they realise they’re never going to get the money back? Because there will never be enough public money to meet the voracious demands of the market? One could predict an apocalyptic outcome.

You are predicting an apocalyptic outcome

And you may be right to do so

The deficit and the National Debt have never mattered a tuppenny-ha’penny damn. The idea that the Government is like a private individual or a firm or Mr Micawber and if it spends more than it receives in income it’s in trouble was, is and remains nonsense. Unlike the private individual, the firm or Mr Micawber, the Government can do something quite legally that none of them can do: print money, lots of it, as much of it as it likes.

It can also legislate, and repeal the Bank of England Act, 1998, and take back full control of the Bank of England, which should never have been surrendered in the first place (one of Gordon Brown’s dafter ideas, like selling off all our gold reserves at the bottom of the market).

It can then, if it controls the Bank, decide what to spend the money on, and when to spend it, so not only can it repay its debts and debt interest, it can do so strategically, and pay off PFI debt (which would be a very good thing, as that shouldn’t have been incurred in the first place!) and boost demand in the economy, thus reducing cyclical (Keynesian) unemployment, which would, in turn, lead to increased tax revenues and reduced social security expenditure. Furthermore, if it boosts demand by infrastructure spending, then this has to be a good thing as it is long-term investment for the benefit, not merely of the economy, but of society as a whole.

Agreed

All possible

And desirable

I will keep reposting this from FT 2011 – on Gordon Brown’s gold sale.

Britain was right to sell off its pile of gold

By Alan Beattie

The Treasury made the right decision not selling, says Alan Beattie

The continued run of the gold price is a global investment sensation. Recently it broke the $1,500 an ounce barrier for the first time, 30 per cent higher than a year ago. Surely this lays bare the extraordinary foolishness of Gordon Brown’s announcement, 12 years ago this week, that the UK Treasury would sell off some of Britain’s gold holdings?

Actually, no. On this one occasion, Mr Brown’s decision was the right one. Let speculators go gambling on a shiny metal, if they want to. For most governments in rich countries, holding gold remains a largely pointless activity.

With hindsight, of course, Mr Brown could have gained a better price by waiting. At current rates, the $3.5bn the UK received selling bullion between 1999 and 2002 would have been closer to $19bn. The difference at current exchange rates, by the way, would be enough to cover a little over three weeks of the UK’s expected public deficit for the fiscal year 2010-2011 — not negligible, but hardly pivotal.

Mr Brown, his critics say, must be kicking himself. Similarly, the French no doubt still suffer sleepless nights for prematurely taking profit on their Louisiana claim by offloading it to Thomas Jefferson in 1803. And had I put my life savings on Ballabriggs at 20-1 before last month’s Grand National, I’d be writing this on a solid platinum laptop while being sprayed with pink champagne in my new beachfront villa in Barbados.

That is the way of things with speculative assets. The truth is that no one has a good explanation why the gold price is currently where it is. The familiar story — a hedge against inflation or government insolvency — is flatly contradicted by the low yields and inflation expectations in US Treasury bonds. The volatility of gold (and other precious metals — witness the huge drop in silver prices this week) merely underlines the risk of holding it. The $1,500 landmark is a nominal price: had governments listened to the bullion fanatics and loaded up on gold in the last big bull market in the early 1980s, they would still be waiting to earn their money back in real terms.

More substantively, criticism of Mr Brown’s sale also betrays a misunderstanding of why a country such as the UK has gold at all.

In common with most rich nations, the function of British foreign exchange reserves is not for the government to manage wealth on behalf of the country. British citizens do that themselves. The UK does not have a sovereign wealth fund that aims to maximise returns, and nor should it. It is not a big net oil and gas exporter such as Norway — UK net foreign exchange reserves are about $40bn, equivalent to 2 per cent of nominal gross domestic product, while Norway’s sovereign fund has $525bn, equivalent to almost 140 per cent of its GDP.

Nor does the UK pile up foreign assets by persistently selling its own currency to manipulate the exchange rate, as does China. It is notable that the much-vaunted official purchases of gold over the past year are mainly by countries such as China and Russia — and, to a lesser extent, Mexico — with big excess reserves.

UK reserves are there mainly for precautionary reasons — to intervene in currency markets to stop a run on sterling or to pursue monetary policy objectives. Yet gold is badly suited for this task because, despite recent interest from private investors, a large proportion of global above-ground stocks — 18 per cent in 2010 — is still held by governments.

Any attempt to sell off large amounts quickly risks driving down the world price, which is what happened after Mr Brown’s announcement in 1999, leading to an international agreement between central banks to restrict further sales.

A precautionary reserve asset held for intervention purposes whose price is likely to fall the instant it is used to intervene is singularly pointless. Of course, central banks selling into a rising market like today’s may not have the same impact as in 1999, but who knows what demand for gold will be like if and when the intervention is needed?

There remains only one other main reason for governments to hold gold — to set monetary policy by linking the national currency to the gold price. This remains as bad an idea as ever. It would have meant sharply tightening monetary policy since the fall of 2008. This would have been madness.

Private investors, and sovereign wealth funds out to make returns, can punt their money on what they like. If they choose to plonk it down on the blackjack table of the commodity markets, that is their decision. But there is no good reason that governments that hold reserves for purely precautionary purposes should feel the need to follow them.

I agree with you Carol

We nee a Modern Money approach:

“the sovereign {government with a sovereign currency} can no more run out of “money” than it can run out of “acres” or “inches” or “pounds”. We can run out of land, but we cannot run out of acres. We can run out of trees but we cannot run out of the linear feet we use to measure them.”

I believe, and think we can all agree, that the problem is not with the borrowing. In fact, in this environment of 0p interest rates, government should be borrowing even more. No, the problem is this government is not spending enough/more in areas deemed necessary!

Precisely

On R5 they have a way of measuring achievement which I think is rather good. They say “if you’d offered x that at start of play would he/they have taken it?”

I think I can say quite safely that if you’d offered Pretty Boy George this 2014 GDP in 2010 he would’ve been appalled & horrified. The Tory Press are trumpeting that the GDP has risen, & there came a point where it had to, & that unemployment keeps falling (which, as I’ve written elsewhere, is fictitious) but not that PBG is nowhere near where he’d have wanted to be. This is most obvious in the total failure to reduce Govt debt which has brought out Tory critics although, unsurprisingly, they have drawn the wrong conclusions. “Austerity? Many people in Rotherham can still afford Sky TV”.

It does annoy me when on AQ/AA or whatever Govt ministers keep saying “we’ve been proved right on the economy” not, so much, because I’m a Lefty, but because it really is the equivalent of Sir Alex saying “yeah, I’m delighted, we were always expecting a 4-0 thrashing in Istanbul”.