As the FT has noted this morning:

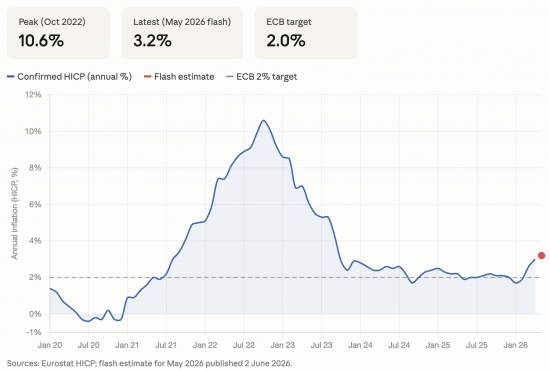

Eurozone inflation rose to 3.2 per cent in May, bolstering the case for the European Central Bank to raise interest rates for the first time in nearly three years as it seeks to contain price pressures unleashed by the conflict in the Middle East.

Tuesday's estimate, which was in line with economists' forecasts in a Reuters poll, was up from 3 per cent in April and marked the highest annual inflation rate since September 2023.

Let's be clear. It does appear, as a matter of fact, and using measures that are commonplace worldwide, that European inflation is rising, but only to very modest levels. No one, with any kind of sense, thinks that 3.2% is a high rate of inflation that should cause anyone concern.

That said, I also accept that the trajectory is upward. This is the chart, which does emphasise that the latest information is an estimate:

Now, I accept that, using the conventional logic of central bankers, an upward trend in inflation suggests that there is action to be taken to stamp out the trend and return the inflation rate to what is either considered normal, for which there is a clear baseline in this data, or that which is considered desirable, which is stated to be 2%.

However, the question missing from this report and from the proposed action that the European Central Bank is thought to be planning is why?

Why take action now?

Why do so when there is already a shortage of demand inside European economies, and when it is known that raising interest rates can only work as a tool to tackle inflation when there is excess demand?

And why raise interest rates when this inflation is clearly being caused by a shortage of oil, gas, fertiliser, food, and other materials, none of which will in any way be made more available by increasing interest rates?

Has no journalist worked this out?

Has no member of the ECB worked this out?

Has no member of the Financial Times editorial team worked this out?

Have none of them realised that if you increase the price of money at a time when inflation is being stoked by an absolute shortage in the supply of essential commodities, all you can do is increase the rate of inflation?

I have posted here recently about the failures of our education system and the fact that it does not teach any form of critical thinking. I am, of course, aware that some people develop that ability for themselves, but it appears that in economics and related journalism, it is almost entirely absent.

Are we really going to have to suffer absurd policy decisions on top of the economic crisis that is already coming our way?

If so, everything will be much worse than it needs to be.

Educational failures have consequences, and this will be a massive one.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Beyond the direct cost of debt, given many large companies have relatively large debts and structures to limit liability, there may also be a risk of seeing companies essentially designed to pay out high debt repayments to connected companies which might then fail, along with others with long payment timescales who will also struggle more with higher interest rates.

More companies going under due to dropping demand, higher debt costs, etc, creates a risk of contagion where other companies unexpected don’t get paid. This then suggests increasing margins to compensate for risk or non payment, and further adds to inflation.

In affordable housing development, the Treasury would expect developing Councils like the one I am working for to raise the internal interest rate we use on loans from the Housing Revenue Accounts (yes, even though HRAs are now stand alone capital for Councils, our over centralised country still likes to interfere ‘ localism’, ‘devolution’ my arse). Although this would create reserves from which to invest in the future, it may also make some schemes unviable at a time of rising costs anyway for the stuff you build the houses with. So a double whammy, rising cost of stuff, rising cost of your own loans to get stuff done. We know the best loan rate for us, not the bloody Treasury.

And there you have sovereign governments sitting there with the latent power of printing money. Yes – I know there is more to it than that, you need the infrastructure to spend it, agreed, but it is the money – the investment – that gets the whole ball rolling and creates the infrastructure.

What we have now I can only call ‘catatonic economics’ – the government is there, the power is there but nothing moves. And now the people are salty to the point that a rich immigrant called Zia Yusuf can wind up white people and say that they are the ones being discriminated against. I feel as though I am in Samuel Beckett play – don’t you? Absurdism is everywhere.

Thank you.

Beckett, yes, or even a Python sketch, in a strange topsy-turvy world where all is upside down.

Despair. Its propaganda.<p>

R4 Today wheeled out Howard Davies to ‘explain’ that the government is like a household, and that foreign holders of gilts (‘far more here than in Japan for example’) had to be placated.<p>

As soon as there is any sign this might be ‘debated’ – by consulting some of the many heterodox economists who might begin to provide enlightenment , the discussion is closed.<p>

Nothing can be allowed ot blur the message that ‘there is no money for anything’.

I despair too

There is another new book ‘The Money Sham’ by Stephen Laughton, of whom I have never heard <p>

https://www.amazon.co.uk/Money-Sham-Breaking-Economic-Orthodoxy/dp/3982879906<p>

There are so many books, including the George Monbiot The secret doctrine’ about neo liberalism – and others more or less MMT – related – all of which challenge the ‘there is no money’ myth. <p>

They are all out there – but BBC sees no reason to refer to them.

That one gives me no reason for confidence.

Howard Davies, another archetypal central banker. From that deeply mainstream school of economics that dominates in central bankers. Who seem incapable of understanding that supply shortages lead pretty inevitably to price increases and that increasing interest rates will make no difference to them. ‘It’s the supply stupid’ as Clinton might have said. Except to make things worse by adding costs and further suppressing demand.

Just feeds my view that whatever your views on BofE independence and its remit, a good start would be to change the make up of the Monetary Policy Committee who make these decisions. Shift from all geek economists with a few City folk, to a mix of economists, business types – large and small, and people from regions, local government and civil society.

That would be better

But even then, they must advise the Treasury, not set the rate.

My sceptical view is that the Treasury is just as bad! The nexus of BofE, Treasury and City with shared beliefs and interests. Hence introducing some potentially very different views into the MPC itself.

Having once had the job of understanding how the MPC worked, interviewing a number of them and finding out where they got their information from. The doubts started back then…

Might it be that recent and current formal/state education is designed to deliver managed ignorance, unquestioning acceptance/obedience and general passivity because those with power seek to enforce compliance on the regular populace?

Might this possiblity be supported by the facts that the National Curriculum does not include socio-economics as a stand-alone subject and that tertiary education avoids theories and practices which question Neoliberalism?

It might be

As a secondary educator – yes. The current curriculum and government strictures (no criticising capitalism for example) leave students even more uneducated than they are now. Of course the independents and grammars pump out neoliberal economics and conservative politics in their add-on lessons.

Very good, Richard – the comment, too.

Commodity Markets Are Living on Borrowed Time | naked capitalism

Good, but still avoids the punchline of what happens then?

In a word, “Problems”. Let’s hope not “Predicament”.