Oil prices are under threat. Food supplies are becoming more fragile. Critical raw materials are under strain. The risk of a major economic shock is growing by the day.

Yet stock markets remain close to record highs.

Why?

In this video, I explore the strange disconnect between financial markets and economic reality. The FTSE 100 and S&P 500 continue to rise despite mounting geopolitical risks, growing pressure on energy supplies, concerns about fertiliser production, and warnings that supply chains could be seriously disrupted.

I suggest there are three reasons why this is happening.

First, pension funds and life assurance companies continue to pour money into stock markets because that is what they have been trained to do. Institutional habits create a constant flow of money into shares, regardless of whether those shares are realistically valued. There will be a heavy price to pay for this.

Second, markets are behaving irrationally. We have seen this before. The dotcom bubble and the financial crisis of 2008 both followed periods when investors convinced themselves that prices could only ever rise. Today, AI speculation appears to be creating a similar mood of market exuberance.

Third, the ultra-wealthy live in a world detached from everyday experience. Rising food prices, energy bills and housing costs do not affect them in the same way that they affect most people. As long as asset prices keep rising, they have little reason to question what is happening.

I also discuss the growing risks hidden within the shadow banking system, the lessons we should have learned from 2008, and why governments should already be preparing for the possibility of another financial crisis.

Most importantly, I ask what should happen if another bailout becomes necessary. Should taxpayers once again rescue private institutions with nothing in return? Or should public support come with public ownership?

The wealthy may still be celebrating, but every financial party eventually ends. The real question is who controls what happens when it does.

This is the audio version:

The Debate Ammunition for this video is available here.

This is the transcript:

The wealthy are still partying while the world heads for economic crisis, and that is worrying me.

Oil, gas, fertiliser, and food shortages are all pointing towards an economic meltdown, and critical raw material supplies are under severe strain, yet stock markets are still close to their record highs. The rich seem unconcerned. So what do they know that we don't? That is what this video is all about.

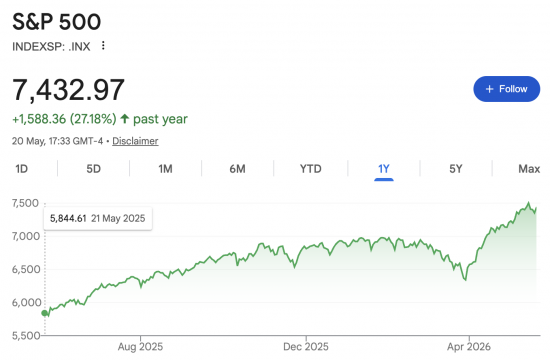

Stock markets are telling us a striking story that deserves closer examination. The FTSE 100 is up by almost 20% over the last year.

That is an extraordinary gain until you compare it with the S&P 500 in the USA, which has risen by around 25% over the same period, and since most of the shares on those indices are not AI companies, there is no rational explanation for these increases.

That is an extraordinary gain until you compare it with the S&P 500 in the USA, which has risen by around 25% over the same period, and since most of the shares on those indices are not AI companies, there is no rational explanation for these increases.

Something else is driving what is happening, and that's something is not good news.

The war on Iran is already transmitting into the real economy. Oil and gas supplies are under direct threat from the conflict. Fertiliser production depends on energy as well as raw material supplies, so food supply is also at risk. And critical raw material supply chains run through or near the affected region, and that is going to have a consequence for many listed companies. Their future profitability must be impaired at this moment, and their customer's lives and their ability to pay their debts are increasingly fragile. Markets are pricing in none of this, and that is what makes them dangerous at this moment.

Distinct reasons why the wealthy are still partying though.

The first is institutional habit; pension funds and life assurers are still, as a result of their inbuilt habits, buying shares.

The second is irrational market exuberance, as seen before every major crash, and I've seen a few in my lifetime.

And the third is that the ultra-wealthy are simply detached from everyday reality.

Each of these reasons operates independently, but together they fuel the bubble we are seeing, and all three have serious consequences for the rest of us.

So let's look at these. Institutional habit is the first of these main drivers of this stock market bubble. Pension fund and life assurance company managers are trained to put their money into stock markets. These managers are taught that the stock market is where value is created. They have no imagination to do anything else. That means that every month, a wall of money flows in from contributions into these funds and goes straight out again into the purchase of shares, and since there's a fairly fixed supply of shares, the demand from these pension funds and life assurance companies means that the price of shares goes inexorably upwards, until it doesn't, that is.

These managers have no idea how to otherwise deploy savings for the broader social benefit. They are simply not trained to think that way. And we all pay a price for this when institutional blindness does eventually meet reality, as it will in a crash, and we are going to see a collapse in pension values very soon, and that's going to hurt a lot of real people.

Secondly, markets are deeply irrational, and history tells us so repeatedly. The Dotcom Bubble of 1999 and the mortgage securities fever of 2007 both ended in crashes. We are now seeing the same pattern of trading again, with AI hysteria driving valuations. Even the Bank of England has warned about the dangers of this kind of exuberance. AI may eventually transform our economy, although there must be serious doubts about that because of the demands it will make upon electricity, water, and other raw material supplies, which remain unresolved at present because they are all going to create shortages elsewhere. But anyway, AI has not transformed our economy as yet, and because we don't know it will, the exuberance we are seeing now is fairly described as ‘deeply irrational', but it's happening nonetheless.

And thirdly, and this is perhaps the most important point I have to make, the ultra-wealthy are detached from reality in a way that compounds all of these problems, and they are major owners of shares. Let's be clear, that is true. They don't invest indirectly through things like pension funds and life insurance funds. They invest through what are called their private offices and through hedge fund managers and the like. But the point is, for them, the cost of food, fuel and heating is simply irrelevant. They do not even experience the cost of living in the way that we do. Other people manage all of that for them. They don't go down to Sainsbury's, Tesco's, Lidl or whoever else it might be that they buy their groceries from. They get people to do it. And as a result, they do not know what is happening in the real world.

In a very real sense, they are entirely detached from it. And as long as share prices keep rising, their world feels secure and unchanged. And so they're carrying on partying. That is my fundamental point. They believe their wealth is large enough that no crash will harm them, and in truth, for some of them, that assessment may be correct.

And in all of this, the shadow banking system, much beloved by the wealthy, is where the hidden risk in this boom is concentrated. It is estimated that at least $2 trillion is invested through this market. Some of that lending is being used to fund share purchases, and there is borrowing for speculation going on. If the value of the shares that are being bought falls sharply, much of this lending will not be repaid. This is a matter of fact. The bad debt that will then arise will transmit from the shadow banking system into the mainstream banking system, and the mechanism for that is clear, and we have seen exactly where this leads.

2008 tells us exactly what happens when a financial bubble meets bad debt. The crash came, the banks failed, and the government stepped in to bail them out. The cost of that bailout was then passed to the public through austerity. Wages stagnated, public services were cut, and ordinary people paid the price. The wealthy know the state will underpin them. The rest of us have no such guarantee. This is not a fair system, and it is heading for another test.

There is little that most of us can do about this, but some people will have a few choices available to them. If you do have control over your own pension savings, consider moving them to lower-risk holdings. Prioritise preserving value over chasing returns in the period ahead because that is going to be important, and if you have some savings of your own in your own hands, head for cash. Make sure you can pay your bills and pay down debts if you can. But I know that this will mean nothing to many people. They have few savings. They do not have the ability to control whatever pension fund they have, and I do get that, which is why in other videos I've talked about what I think the government will need to do for people in that situation.

But, this time, the government needs to plan for when the crash comes. That is the point I'm making continually at present. This time, when banks and institutions are bailed out, they should pass into public ownership. The lifeboats should not just rescue the wealthy. They should claim what is rightfully ours.

So why are the wealthy then still partying? That's because the financial system is not designed to serve the interests of most people. Let's be clear about it. But it is designed for the benefit of the wealthy. It channels savings into speculation rather than to productive social investment. It does not create jobs. It does not preserve the environment. It does not do anything for most of us. It protects the wealthy when things go wrong and leaves others to bear the cost.

The question is not whether another crash is coming. It is whether we are ready for it. This time, we must use the crisis that is inevitably heading our way to demand a system that works for everyone.

This party will end. What matters is who controls the morning after. And this time it should be us.

That's what I think. What do you think? There's a poll down below. Please let us have your comments. Please share this video if you like it, and please do like it if you like it. And if you want to support our work, please do buy us a coffee. There's a link to do that down below.

Poll

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Well we need higher taxes on the income of the ultra rich otherwise they will continue to party, buy more assets etc!

Thanks all round again!

Might part of the matter be that, on a spectrum between democracy and olgarchy/plutocracy, our society/“the West” have been moved markedly towards the latter pole?

Might our society be more cohesive, coherent etc., when/if Democracy is assessed according to output/actual results rather than by overly symbolic voting inputs?

I think that what we are seeing is a heady mixture of all those points above but one of them stands head and tail above the rest of them: the banks and investors know that they will get bailed out for sure.

The central bank reserve account is there right now cushioning the huge risks the financial sector are taking, so why not push up your guaranteed pay out and max it out – go further even? The government will have your back and even book your excess ‘profits’ as proof that their policies are working (won’t they Rachel?).

What makes this worse is that the same government does not think it has to help the people who vote it into power and protect them from the risks of unemployment, sickness, education, shelter, old age, environmental degradation and infrastructure that is wearing out.

Potholes for example are not being created by welcoming immigrants; they are a symptom of the financialization of the money supply in this country, its capture by the rich, for the rich and the inane political belief that it will ‘trickle down’. Even whilst the super yacht business grows and private jets abound (and offshore)!!

For yachts, 2021/22 sales were ‘extraordinary’ with lower volumes but (note) ‘larger yachts’ on the order books this year.

For private jets, at the beginning of this year, demand for them was up but supply was tight. If we were being looked after, maybe it would be less of an issue. These items are our potholes, our services, our needs not being met. This is simple mis-allocation of money. It is exclusive private sector markets pushing public need out of the way. My sources are below.

https://www.superyachtsmonaco.com/news/2026-superyacht-sales-forecast/

https://elliottjets.com/demand-is-up-inventory-is-down-what-aircraft-buyers-need-to-know-in-2026/

Much to agree with

On your first point, that investment managers are trained to invest in stocks and shares, I agree, they are.

Historically, over, say, the past century, stocks and shares have been a good investment, unless you put all your money at just the wrong time (before a crash). And they avoid this by “cost price averaging” that is trickling money in. But the last century coincided with large population growth. And because, as you say, there is a relatively fixed stock of assets, then of course the price will increase. And this itself justifies the strategy. It’s a positive feedback loop.

The situation is about to change, or is already changing, because fertility rates have fallen and continue to fall. This means, going forward, there will not be an increasing number of people pumping money into the stock market. In fact the reverse, where an aging population withdraws savings which are not replaced by savings of young people. Now we have a positive feedback loop in the other direction. As more money is removed, prices will fall, causing less money to be invested. Now the stock market has become a Ponzi scheme (if it wasn’t before). If, primarily older, people can withdraw their savings before the crash they will be winners. Everyone else will lose.

We seem to be in a Wiley Coyote moment, where the stock market has run over the edge of a cliff but doesn’t yet realise. His fall, and the crash, are inevitable. And “this time it’s different”, because the demographics have changed. The stock market may never recover.

Thank you

Excellent analysis … but also …

… as well as current-event crises, the rich – and most of us – are denying the imperatives of climate change. Our planet is finite. Talk of Mars and the squandering of precious resources on rockets and the idea of mining the moon are ridiculous. Some space initiatives are probably worthwhile but the pollution caused by many projects makes them unforgivable.

… and also …

Knowing as we do that climate heating is increasing – perhaps accelerating – can the planet cope with the CO2 and other pollution caused by people rich enough to fly whenever they fancy?

Does the world have the resources to equip *every* community with …

… motor vehicles to the same extent as North America and Europe in particular? No! What then is our policy?

… high-rise flats when there is little chance that, quite soon, electricity will be available to operate the lifts?

Because of the war-created oil crisis, people are now starving in Asia and elsewhere (Afghanistan was featured on Al Jazeera recently). Yet many deceive themselves with talk of *net* zero CO2 emissions … when what is needed is ZERO EMISSIONS (while *net* zero only has validity in aspects of the agricultural sector.)

I doubt those questions occur to Musk

One obvious point I might make about stock markets is the demise of the defined benefit pension scheme and the ‘With Profits’ policy.

I have a defined benefit pension so my fund managers are not looking at John Boxalls ‘pot’ and what its worth

This means that they can invest in things like Solar Farms, commercial property etc which of course are very ‘illiquid’ and the percentage invested in these things isnt that large at least there is some.

While ‘With Profits’ funds are opaque and have limitations again it makes it possible to diversify into things other than stocks and shares

Currently however its often difficult for fund managers not to place money in the stock market because defined contribution pensions and investments requires them to do so.

This may be of interest

@jamessquared is an IT professional & on that forum I am @johnof wessex

https://national-preservation.com/threads/the-ai-bubble.1426083/

That brequires registration

Those who believe that “The Market” will sort everything out are in fact correct. But they have missed two very important points. First, it takes time. Rather than supply and demand reaching equilibrium at a specific price point instantaneously, the required movements play out over a significant period. Second, the Invisible Hand is not the hand of the benevolent, shining, blue eyed God of Sunday school fairy tales. The invisible hand has no moral compass, no social conscience and no scruples.

So the curves of supply and demand will come into alignment as predicted at some specific price point, but it may take a year or two and the invisible hand will modify demand to fit the curve by killing off one or more hundred million people as required.

Keep shouting Richard! Some people are listening.

I will be shouting

To follow on from Tim Kent’s points, I note that in 2025, according to the ABI, UK consumers allocated £7.4bn to annuities. That was 87,600 new annuities, of which only, shockingly, 18,000 were increasing (either by a fixed compound percentage or by RPI-linking). That £7.4bn has effectively left the stock and bond markets as far as the individual is concerned. They have exchanged a whole bunch of uncertainties for the certainty, security, and value of an insurance contract.

Sure, annuities may not be for everyone, but I firmly believe that they remain the optimal retirement income product, period.

If you might be thinking about this option within the next few years and have a “defined contribution” plan, whether with a life office or a SIPP, I’d certainly say that it would be prudent to look at switching your fund, temporarily at least, to a cash or deposit fund to give you ” breathing space” while some irrevocable decisions are being made. This will stabilize your fund value, pretty much, which is good. Although I am an authorised IFA, this is not advice, just information, but it makes good sense to me!

That data is quite depessing.

And i think the suggestion is sound.

There isn’t much new under the sun.

“…the real object of the concocters of railway schemes…[has been] to rob and delude the public by getting their scrip into the market at a premium, and to rob and swindle their subscribers in particular by squandering and embezzling the deposit money “.

The Bankers Magazine, Sept. 1845.

🙂

Another old quote from The Banker’s Wife by Catherine Gore (1843). She was describing the country estates of the time.

“Affording a favourable type of that rich and smiling order of home landscape which seems almost to embody a portraiture of our social institutions: nothing salient – nothing discordant – a limited horizon – a pleasant foreground, with symbols of peace and prosperity interposing between…in order to gratifying the taste of those who care less whether Lazarus be sitting famished and suffering at their gates, than that the gates should be of sufficient solidify to exclude the spectacle of so piteous an object”.

Mrs Gore was scathing in her condemnation of self-seeking but is forgotten today. Gated communities were ever thus, then!

Very good

Gratify & solidity are the right words!

It’s not clear to me exactly what is mispriced. Nvidia, for example, is selling a huge amount of AI hardware. Some are claiming the upcoming Spacex IPO is ridiculously overpriced, but Spacex has a couple of near monopolies (starlink and taking anything to low earth orbit) and a gigantic following of retail investors. Due to its size the passive fund industry will be forced to buy it. I wouldn’t be surprised if it skyrocketed; nor would I be surprised if it flopped.

The multiples of profits reflected in the valuations are absurd. Can’t you see that? If not, feel free to lose your money.