The UK pension system is built on a false idea: that savings and financial assets can guarantee security in old age. In this video, I argue that pensions do not ultimately depend on money saved in the past, but on the productive capacity of those still at work in the present. That is the real pension contract, and it is one the UK has steadily abandoned.

I explain how the state pension once reflected this collective responsibility, why Thatcher's reforms changed the whole theory of pensions, and why the savings-based model now dominant in the UK is fundamentally detached from economic reality. I also explore why demographics, weak productive investment, and the financialisation of the economy mean that many pension promises may not be kept.

This is not just a technical problem. It is a political choice, and one that may leave millions exposed to insecurity in old age unless we confront it now.

This is the audio version:

This is the transcript:

The UK pension system cannot deliver on its promises. To put it another way, that pension system is going to fail us all.

We are living, at the moment, with a pension system in the UK that is fundamentally confused about what pensions really are, and as a consequence, it is promising security in old age on the wrong basis.

The system is built on theory that does not match economic reality, and that mismatch is going to guarantee the failure of our pension system.

All of that does, I think, need explanation because those are big claims, but I've been thinking about them for three decades now, and nothing I have observed over that period has ever led me to change my mind.

Let's remind ourselves what pensions are meant to do. When we first got a state old age pension in the UK, which was unbelievably just before the First World War, well over a hundred years ago now, the state pension that was promised was for everyone who reached the age of seventy, and it was paid from then to the time of death with the aim of providing freedom from fear to those who lived in older age who could no longer work and were no longer able to support themselves as a consequence.

The fact was, though, that few people lived long enough to claim that pension in those early years. People's life expectancy was lower than seventy. So you had to be really old to get a state old-age pension at the time. But the critical point was this: the system assumed the collective responsibility of everyone in society to support those who were old. This was a universal provision for everybody who was elderly, made on behalf of everybody else in the society in which they lived.

This reflected the real pension contract, which exists in any society, and this real fundamental pension contract is something which is really important, and which I have to explain in a little detail before we go on with the rest of this video. Let me be clear about what I mean.

One generation, let's call it mine, does during their working life produce sufficient productive capacity as a result of their effort, that the next generation have that productive capacity left to them to use when that previous generation, mine, have retired and are living an old age. The assumption is that the next generation, by using that capacity, will generate income in excess of their immediate needs, and will, as a consequence, be able to divert part of that income to those who are in retirement to keep those elderly people free from fear. I'm not saying they would be kept in riches. They would be kept at least in a style which ensured they could see out their days in a way where they were not in poverty.

The support that was provided from those who were working to those who weren't would come out of the current income. Savings were not a part of this equation. This is an unavoidable, intergenerational contract that reflects an economic reality that those who are old need an income, and the only people who are able to provide it are those who are still at work, because income by definition happens in the moment to fund the consumption that takes place in the moment.

You will notice from what I just said that there is something really important about that statement. Income arises in a moment and is consumed in a moment. There is no transfer of capital at the time of consumption. The transfer of capital happens at the moment that a person effectively retired. They've accumulated constructive, productive capacity while they work, for the next generation to use whilst they work. This is a contract about working relationships and how the rewards of work are shared with the elderly now in retirement, sharing part of the income of those who are working now. That point is what we don't understand about pensions.

Pensioners can't live off savings. Try and eat the money that you've saved in your bank account. Try and eat your pension annuity. That is just a financial contract. You can't live off a financial contract. What you must live off is the production of people now working. They'll make your food. They'll make your clothes. They'll provide your services. They will provide your healthcare and everything else that you need. That's what really matters when we come to talking about pensions.

But the system has drifted away from this fundamental economic reality, which was reflected in the pay-as-you-go pensions which the state provided. They were pay-as-you-go, because quite literally, the pension for the elderly was paid out of the income of the government generated at the time that the payment was made. There was implicit in the tax system a transfer of value between generations, but that system began to break down.

Why? Because many people began to live longer than they had previously. The age of sixty-five, at which people were later on promised an old-age pension, began to look ambitious. More people lived for way beyond that number of years. Life expectancies had grown, and as a consequence, the government feared the cost of meeting this promise. They also feared the tax costs of funding it, as they saw it, and those with wealth resisted higher taxation to provide for the elderly. So, policy drift replaced clear design.

In the 1970s, the state did try to produce new state pension designs. These were earnings-related pensions. They were called the State Earnings Related Pension Scheme, or SERPS for short, but that became the thing that broke the camel's back. It was that system that looked expensive. Politicians couldn't break the commitment to the state old age pension, but they did break the commitment to the state earnings-related pension, which did provide a supplement to the basic pension.

Thatcher, as on so many things, was the turning point. She broke the fundamental pension contract. She ignored it. She said there was no such thing as the state, remember. She believed in individual responsibility, and she ended the collective responsibility that the state had to provide viable pensions for all. Instead, she said, that provision became a personal responsibility. We would have to meet it by saving to provide the funds that were required for our old age.

The entire theory of pensions changed as a result. It was no longer the state that would supply our pension. It wasn't even our employer who would provide our pension. It was us acting as individuals who were told we had to do so. Pensions then became dependent upon investment returns. That shift still defines the pension system that we have in the UK today.

There are then two pension models now in use in this country, but only one pension reality, which is that we still have that fundamental pension contract in operation. The pay-as-you-go pension that we have, which is the basic state old age pension paid to most people in this country, as of right, either because they've earned enough during their lifetime by paying enough National Insurance to claim the pension or because if that's not the case, their pension has been topped up by other benefits to ensure they don't live in poverty; that still continues.

But many people in the UK now have savings-based pensions, which assume markets can deliver future income for a person throughout their remaining life, either by drawing down the sum saved over that lifetime or by buying a pension annuity, which is guaranteed to provide an income for the remainder of life, with there being a gamble between the pensioner and the life assurance company about who will last longer than expectation.

Only one of those two pension systems we now have in operation aligns with the fundamental pension contract, and the UK has chosen to model most of its pension provision on the one least grounded in reality, which is the savings model.

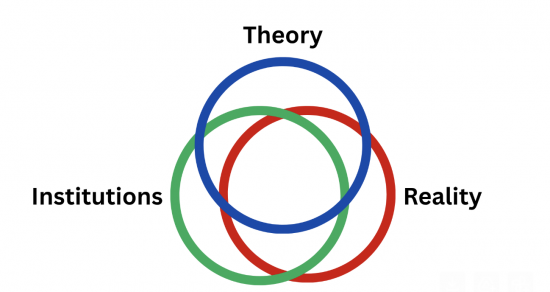

Let me try to explain this using a bit of diagrammatic representation to assist understanding. There are now three circles that you can see on the screen.

The first one to the right is described as reality, and that represents the fundamental pension contract. At the top of the screen, you'll see something called theory, which is the theory that underpins pension provision: what was the pay-as-you-go scheme until Margaret Thatcher came along, and what is now the save-to-provide-for-your-old-age scheme that she fundamentally introduced during her period in office. And on the left of the screen, you can see the institutions that supply our pensions. There are two types. One is the government, and the second is pension funds, normally run by private sector organisations.

The pay-as-you-go that I talk about aligns theory, practice, and institutional form in a way that the diagram on the screen now shows.

There's a massive overlap here between reality, theory and the institution involved, which is the government, because the fundamental pension contract is reflected in the payment of the basic state old age pension. There is a transfer of value from those in work, reflected in a sense by the tax that they pay, which is balancing the payment that the state has promised to make to pensioners, and this is reinforced through the provision of this arrangement by the government itself. So, reality, theory and institutions align. This system works. That's the point of this model.

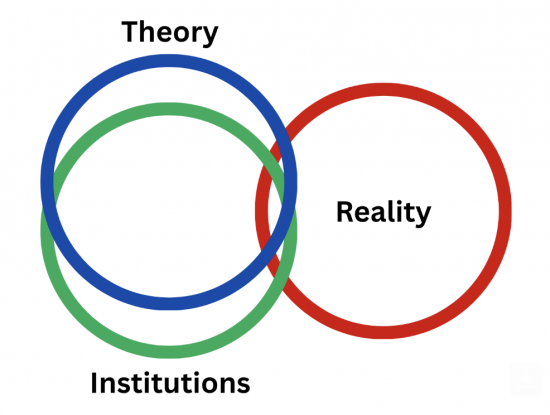

And then we come to the third diagram, and this is where we look at the savings-based model, and as you'll see from the screen now, the circles do not align.

Why is that? The reality is that the fundamental pension contract, which is the collective acceptance of responsibility to provide for those in old age, is not reflected in the savings-based model of pension provision. So reality is stuck out, far removed, with a tiny overlap with both the theory and the institutional structure of the organisations providing this form of pension.

There's a strong overlap between the theory and the institutions, of course, because the theory that underpins this idea of savings-based contracts was based upon the idea of individual responsibility, and the ability of the individual to save in a private sector institution who would maximise the rate of return on an investment to ensure that there were sufficient funds for a person supposedly to live on an old age, although, of course, nobody lives on funds in their old age. What they live on is the resources made available by those still at work.

The assumption within this model is that the savings will provide the capacity to buy those resources from people who are at work. That is not about collective responsibility at all. This theory assumes what reality cannot deliver then. The theory is that savings will always meet the requirements of pensioners, but the reality is that only by collective action can we meet the needs of all of those who are in retirement and prevent them from suffering real poverty, and prevent them from living in fear. The consequence is that we are suffering a pension system, which is built on the basis of an idea that generates a systemic failure.

Savings cannot solve the pension problem. That's partly because you can't consume savings, and partly because you don't know what savings will be worth in your old age, and in reality, if the younger generation do not wish to provide you with a pension, they can easily get out of doing so. They could, for example, inflate the value of your pension away, or they could simply refuse to buy whatever are the financial products that you have saved in; therefore, deflating their value to the point that there is no value to them, so they do not have to transfer income to you.

The point is, savings can only work if they enable future production and financial products, which is what we are using as the underpinning of the pension arrangement, cannot and do not always reflect that future production value. This is the key point you've got to remember.

However smart your financial instruments are, it's actual physical product that we need in old age. Physical product and service, and that can only be generated in the moment at the time that you require them. Income is still then required to be transferred from the people who are at work to the people who are in retirement in this model but the mechanism for transfer, through the savings system, where the value of savings and the value of the financial products in which savings are made are completely uncertain, is one that is so uncertain that the savings mechanisms that we are using are uncertain to work. That's because there are three assumptions implicit in this savings model, and as I will explain now, all three of those assumptions have failed.

The three assumptions are that, first of all, there would be sufficient savings opportunities for everybody if a model that in the 1960s and seventies was used very narrowly by some larger companies, could be expanded to everybody. It was assumed when this system was made national, and now applicable to everybody who is basically at work by state compulsion, that there would be sufficient resource available in society to use the savings that people were putting aside, and that there was also a direct link between saving in shares and in buildings, and in bonds, that would create the real productive capacity that would enable this transfer of value as people reach old age on an intergenerational basis.

But that hasn't happened, and the whole model is also going to fail for another reason. It was assumed when this model was put in place that demographics would support it. In other words, there would be an ever-growing population in the UK so that the number of people in work would always grow faster than the number of people in retirement, and so the number of people in retirement making claim upon the pension funds would be small enough to ensure that those in work could always meet their needs.

All these three assumptions; that there would be a scheme capable of expansion to a national level, and that the savings put into this scheme could be used for productive purposes, and that demographics would remain stable in the sense they would always grow, have failed. Those assumptions are false.

What has actually happened is that pension funds have grown far faster than productive investment opportunities have inside the UK economy. As a consequence, the UK economy has not focused upon creating productive capacity, but has instead prioritised the creation of financial returns over production, and wealth has been shifted into rents and not into real output, none of which can guarantee that future generations will be willing to transfer their income to pensioners on the basis of these claims to wealth which cannot be justified on the basis of real, actual economic capacity created.

As I've explained in another video recently, when I looked at the stock exchange, the capacity that is created by stock exchange investment, which has dominated most of UK pension saving for a long period of time, is remarkably limited in the UK. In fact, the cost of pension subsidies provided by the state to pension savers has been considerably greater in recent years than any amount of money that has been diverted into the creation of new productive capacity as a consequence. This means that the first two assumptions underpinning this supposed savings-based pension contract have failed.

And then there is the demographic reality to consider as well. That is that the number of children being born in the UK to each woman of childbearing age has fallen considerably over the period when this system has been in operation, so that instead of there being more than two children being born to each woman, on average, it's now down to 1.4 across the UK as a whole, and in some parts of the UK, like Scotland, is lower than that.

As a consequence, the number of pensioners in proportion to the number of people working is rising, and the demand for a transfer of income is growing without there being any underpinning within this failed savings-based pension contract to support that transfer of value. As a consequence, this is not working, and immigration has not offset this trend, much as I would like that it did so. The system as a result, is facing growing structural pressure.

It was never designed to deliver in the situation that now exists in the UK with regard to an ageing population. The system is then failing. Theory does not match economic reality, and whilst institutions might match the economic theory of pensions that is in operation, they too do not match the economic reality of the world with regard to pensions because they do not reflect how pensions actually work. They now operate as short-term profit-maximising companies seeking to attract business. They have no interest in creating long-term value which will underpin what their pension customers will want in retirement. The fact is there's a massive mismatch between most pension providers and those they are meant to be serving, and the failure of fiduciary duty that runs through this is quite staggering, and they are not held to account as a consequence.

Much of the promised wealth that is, in fact, now held in pension funds does, in fact, now represent financial assets which may quite simply not exist when push comes to shove because there is no value within them that represents a claim on assets that a succeeding generation will be willing to forego to support the previous generation now in retirement. As a consequence, a failure of the fundamental pension contract is now built within our pension savings schemes. Failure is inherent in what we are doing.

The consequence is clear. Pension promises are unlikely to be met now. Economic insecurity in old age will increase as a result, and pressure on governments to support those who might be living in poverty is going to increase. Neoliberal pension policy will be exposed as fundamentally flawed as a consequence, and it will be too late to do anything about it because decades of wasted time will have been spent creating edifices called pension funds, which will prove to be valueless.

So what do we need to do? There are things that we can do to change this.

One is to change the narrative. We need to talk about that fundamental pension contract. We need to understand it. We need to ensure that our pension system reflects it. We need to understand that the state has a role, a collective role, and a collective responsibility to ensure that there is this transfer of value. As such, it needs to make sure that pension savings are now invested in a way that is both clear, transparent, and accountable, which is far from the case at present, but which must also create real productive capacity within the economy, and I have suggested ways to achieve this outcome.

We need to change the way in which tax relief are provided to pension funds so that as a condition of the tax relief given when a pension contribution is made there is a requirement that a proportion of all new contributions saved, I suggest 25%, must go into the creation of new productive capacity within the economy to ensure that a transfer of value between generations takes place. Over time, I suspect that that proportion will need to increase.

The state must also step up to the mark. It needs to reconsider the creation of a state earnings-related pension scheme again, after all, there is a relationship implicit in the contributions that we make to the state and in the return that we expect from it with regard to a pension. If we have a progressive taxation system, and we do to some degree, we could reasonably expect the state to also provide an earnings-related pension as a consequence. That would be important in my opinion, and would reduce our exposure and dependence upon this failed savings idea.

But most of all, the state must brace itself for pension failure, and if it doesn't talk about it now, that failure when it arrives will be all the worse. As a consequence, we need to talk about this. That is why I'm making this video. The current pension system is designed to fail, but my point is that design can be changed. Policy realignment could make pensions coexist with economic reality again. The choice we have available to us is to act now before pension failure becomes unavoidable. I still think that is possible, but we must act soon.

That's the reason for this video. That's what I wanted you to understand. I'm sorry if it's all been a bit complicated. It's necessarily so, because this is an issue of enormous importance, where deliberate opacity has been created by the neoliberal finance system to ensure that the City of London has profited enormously out of pensioners, but pensioners have been left exposed to considerable vulnerability as a result.

That is the thing that I take objection to, but you may disagree with me. You may not agree that there is such a risk. If so, take part in the poll we've got down below. Leave your comments. We will try to read them all. I suspect there will be a lot on this occasion, and if you like this video, please share it because this discussion is one that we need to have in our society now. At the same time, please subscribe to this channel, and if you're so inclined and think that discussions like this are really important, if you'd like to support the work that we do by making a donation, we'd be really grateful.

Poll

![]() Loading ...

Loading ...

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

The OECC is urging Ms Reeves to make Britain’s tax system “more efficient and growth-friendly”, and if delivered there would be more total compensation available in the soviet for government to move around.

Workers stung by a £100,000 HMRC tax trap are being put off work. The Organisation for Economic Cooperation and Development (OECD) published Foundations for Growth and Competitiveness 2026 report on Thursday, April 9.

In it, it issued a series of warnings to the Labour Party Chancellor Rachel Reeves about how tax policy may be hurting Britain’s protracted hunt for growth. It urged Ms Reeves to make Britain’s tax system “more efficient and growth-friendly”.

It argued that “distortions such as kinks in the income tax schedule weaken work incentives” – one of the most controversial examples of this is the tapering of the personal allowance when yearly earnings rise above £100,000.

So?

You have me completely confused but worried. Nearly all my current income in retirement is from the pension scheme of my former UK based employer, a large and well known corporation. The scheme ‘promises’ me a monthly payment until I die, index linked to the CPI. With a bit of luck I have another 10-20 years to go. Should I be worried or not?

Potentially, yes

My own father when in that situatiion always was

He could see how absurd it was that his wellbeing was dependnent on irrational valuations and games polayed by chancers.

He was right

I keep making the point and a lot of people just dont get it that wherever you get your pension from its whoever is in work at the time that pays it.

Secondly at least with State Pensions the State can decide where it gets the money from to pay the pensions, private providers will be simply sweating whatever assets they have and damm the consequences.

As you have pointed out look at the University Superannuation Scheme & Thames Water, that isnt going well

There is a Para Handy* story about an old woman who has just been widowed, she does a ‘flit’ abandoning her home and takes passage on the Vital Spark to (Lochgilphead?) which is where the workhouse is. She didnt take the MacBrayne steamer as if she bought a single ticket then her plight would have been obvious to the world.

The crew realise her plight and have a whip round for her, they also tell her about the State Pension that has only just been introduced.

With the proceedings of the whip round and knowing that she can claim a pension she is then able to return home on the MacBrayne steamer with her future secured.

Thats what the pre state pension world could bring to many and one that many in the Uniparty want to bring back.

* Para Handy was the captain of the ‘Vital Spark’ a puffer – small steam boat that traded on the Clyde and West Coast of Scotland in the stories written by Neil Munroe

Thanks

There is a collection of 3 papers available for download from the Scottish Currency Group website which address these key issues relating to pensions. They are, of course, proposals for a future pension system for Scotland plus proposals for investing Scottish local government pension funds in the interim.

“Pensions in an Independent Scotland”

“A People’s Wealth Fund – investing the National Pension Fund”

“The Community Wealth Building Act 2026 and the Fiduciary Duty of Scotland Local Government Pension Funds”

Publications repository – Scottish Currency Group | Scottish Currency Group

I see the truth in all you say. But even if it weren’t, the generation (say 45 and under) who cannot now buy a house, will be renting in retirement, with insufficient pension to pay rent, and thus needing housing benefit.

I’m 86, and I can’t help realising how incredibly fortunate my generation is/was. Free schools. Free degree education. NHS. Available well-paid jobs. And even with all that, I’d be poor if it weren’t for a substantial legacy from a friend. How bad things will be for my children and grandchildren doesn’t bear thinking about.

Thank you for this excellent piece, Richard. The way that people should view annuities, in my opinion, is that they are useful to cover lifetime essential expenditure requirements as they offer a lifetime guarantee. So, if, say, your essential costs (food, utilities, council tax, etc.) were, say, £2,500 a month and you only had £1,500 a month coming in from state or DB occupational pensions then you might use enough of any DC pot to buy an index-linked annuity providing £1,000 a month to give you this “baseline income”, if you have such a thing. Today, many people I deal with have surprisingly large DC pots (but for how long this will be the case is an entirely different question!) and may decide to allocate, say, one-third of such a pot to an annuity paying careful attention to the death benefit options, and leave the rest in the pot for future use. Doing this brings the comfort of financial security as far as essential expenditure in old age is concerned.

Thanks

Another danger is paying for residential care.

A retired friend is married to a retired man who now needs residential care.

She never worked; they own a house jointly and saved to provide capital to pay an income.

She is now told that because they have savings she must pay for his residential care. That care could well last for several years, and, at £1200 a week, is rapidly eroding their savings. (His state pension and attendance allowance are paid directly to the home, and set against the £1200 weekly fees)

She has been told that when the savings are exhausted they will put a charge on her house and when she dies, or sells the house, the costs will be claimed against the value realised on selling the house.

She is now scared about how she will live on a single pension with none of the additional income they planned.

A reasonable concern

One of the pension areas that really makes me angry is auto-enrolment. Every employer must enrol every employee in a pension savings fund if they earn £10,000 a year or more and if they are between the ages of 22 and the current state pension age. Someone on an income of £10,000 a year cannot afford to contribute to a pension scheme, but, unless they opt out, and very few do because it is complicated, they must do so. The pittance of a pension that will result from this compulsory savings scheme for the very low paid s not going to make a measurable difference to their income in old age, while it may have a serious effect on their life expectancy as poverty kills….

A great deal to agree with

This is a City support scheme, not a pension arrangement.