There is a very strange feature that, as far as I can see, has not had much attention paid to it so far within the Whole of Government Accounts for the year to 31 March 2023 that were published yesterday.

Ignoring the fact that, as I noted yesterday, these accounts were subject to qualification by the National Audit Office because about 90% of the data from local authorities required for their preparation was either unavailable or had not itself been audited, some parts of this data might be considered reliable, and this might be true with regard to interest costs arising during the course of that year and pension liabilities owing at the end of it.

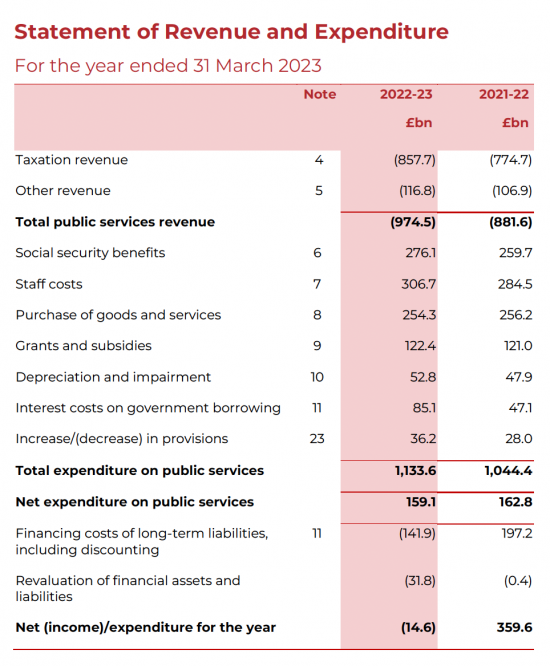

This is the income statement that was included in those accounts:

Ignore, for a moment, any of the information excluding that for finance costs, which you will note total (£141.9) billion, as noted near the bottom of the data.

Ignore, for a moment, any of the information excluding that for finance costs, which you will note total (£141.9) billion, as noted near the bottom of the data.

Then, note what is peculiar about this figure. Everyone would expect the government's overall financing cost during the course of that year to represent an expense, but that is not the case. The figure of (£141.9) does, in fact, represent net finance income arising during the course of the year. That is why the figure is in brackets. It is the opposite of what is expected.

There was a cost of £197.2 billion in 2021/22 when interest rates were much lower, but there was finance income in 2022/23 when interest rates had risen.

This is the exact opposite, of course, of what the government has been saying. And remember that these accounts are prepared in accordance with International Financial Reporting Standards in a similar fashion to the accounts of major PLCs. This data is meant to provide a true and fair view. In this case, using those accounting standards, there is no reason to think that they do not.

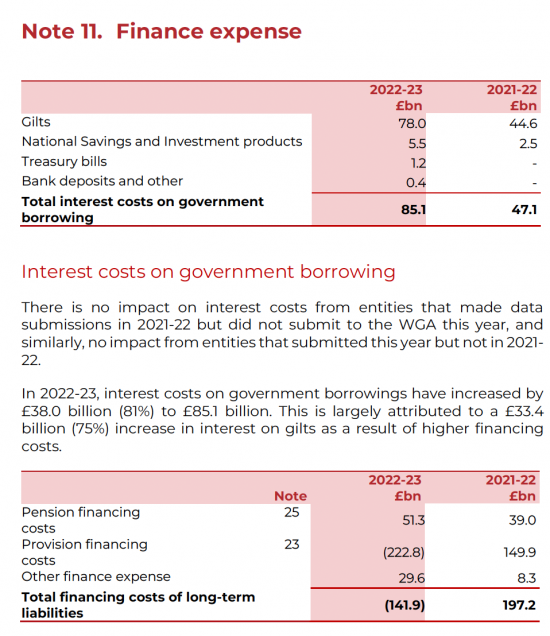

The explanation is to be found in the notes to the accounts, the relevant one of which is as follows:

Ministers might well, of course, seek to highlight the significant increase in the apparent interest cost arising during the course of the year. However, whilst it is true that the costing question rose, that is offset because the cost of financing future pension obligations fell very dramatically because of the increase in interest rates, which therefore meant that a much smaller provision is required for such costs, meaning that in overall terms the government actually had, in a proper accounting sense, net financial income rising during the course of the year of in excess of £140 billion.

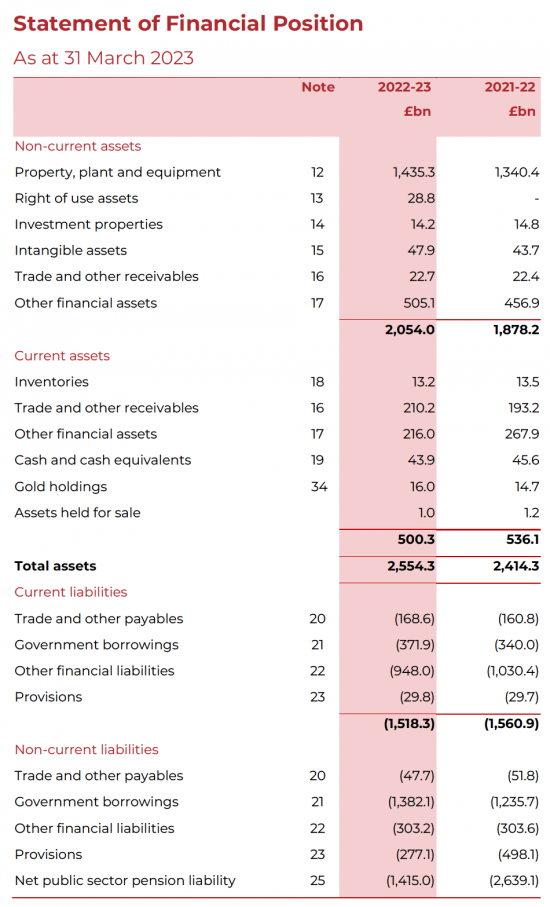

That then led me to look at the government's balance sheet at the end of that year because if this was the case, then there must have been a dramatic change in the government's financial position as a result of this reduced cost of pension financing, and that is exactly what the accounts show. This is the year-end balance sheet:

The critical figure to look at is net public sector pension liabilities as shown under non-current liabilities, and as is clear, this potential cost fell from£2,639 billion to £1,415 billion during the year, or a decline of £1,224 billion - or almost half the UK's annual income.

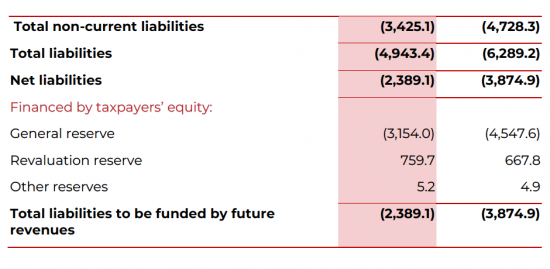

What is more, the total UK government deficit fell from £3,875 billion to £2,389 billion or by £1,486 billion (or, near enough £1.5 trillion) in total, or well over half the UK's total annual income for this year. And I stress that this happened in a single year, and all because interest rates rose so much that future pension costs are now considered to be vastly more affordable.

The good news is that the UK is now, near enough, £1.5 trillion better off than it thought. That money should, as a result, now be available to be spent on making sure that those pensioners for whom the provision is being made might have a country in which it is possible to live in their old age.

The good news is that the government should be trumpeting this - the supposed burden of costs on our grandchildren has been reduced considerably, and we can concentrate on giving them an inheritance instead.

And, because the Bank of England is going to keep interest rates high, whether that is appropriate or not, what we can be sure of is that this situation is not going to change very much for some time to come.

So, does this matter? The answer is that, of course, it does. If we take financial management seriously - and we should - then this cancellation of net interest costs is massively important. It changes the whole austerity narrative.

And the same is true of the government's net financial position. What many claimed was unaffordable suddenly appears to be a matter of no great consequence, albeit the crushing burden of current interest rates on people now suffering them will continue - but the government appears reconciled to that, so it might as well take advantage of the upside.

What is more, if we consider the debt narrative - which only focuses on a very small part of the true story of debt, as I have long suggested, and significantly overstates that cost in ways I have also long highlighted, then this also matters. GDP on 31 March 2023 was approximately £2,650 billion per annum, according to Office for Budget Responsibility data. Total government liabilities - including all pension liabilities - were no more than 90.1% of that sum at that time. In the worst possible scenario, government debt is now less than is claimed by the Office for National Statistics, and because interest rates are now higher, this situation might have got better since then. The debt narrative that governments (both before the elections and since) have been peddling is quite seriously wrong.

If only the government prepared proper financial accounts on a regular basis - as any business would - then this would have been obvious long ago. We would have been spared a great deal of economic nonsense that has been claimed since then. We could, at the very least, have had a more informed debate.

And if the government wants to argue that this approach is wrong - and say that this accounting is not appropriate, they then have to justify why:

a) they have adopted it

b) they say these accounts are true and fair

c) they require companies to use it.

There are reasons to discuss whether these accounts are true and fair, in my opinion, but that option is not open to the government - they have already said that they are. So, they must address facts on the basis that they are right. The missing local authority figures will not change the figures I note materially. And, in that case, what this data shows is a situation where the government debt narrative is totally wrong, and the government's financial position improved by £1.5 trillion in a year.

Now, what is the influence of that on government policy going to be?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Won’t some claim that the £1.5-trillion fall in the National Debt is due to austerity, and hence that this demonstrates austerity works?

No, the part of the debt relating to austerity (gilt borrowing) rose

NAO for first time cannot sign off Whole of Govt Accounts because of the crisis in local govt auditing and huge backlog in audits.

I blogged about that yesterday

Your point is?

It is very unlikely to significantly impact these figures

Brilliant work and analysis! I guess that realising that interest rates can move their goalposts so much might mean more space for *insert spending increase or tax cut here*

I am not saying I have found a panacea – as I hint, there is much to question in this accounting, but the point is it destroys their narrative

It destroys the narrative for those interested (such as us lot that visit the blog). But it will not be raised my main stream media (MSM), because that would require explanations and discussions & we can’t have that, educate UK serfs – nah! – this is a regular problem: reality is there is no MSM interest (deliberate?) in outlining it. That said, even if the population was suddenly “educated” – hey folks £1 trillion better off (or words to that effect), this would not change the ideologues in gov.

Apologies for the negative tone. Very interesting blog btw – devil in the detail etc.

Let’s see what happens…

I’m completely confused. Why would rising interest rates mean that pension liabilities are reduced? I didn’t think that Governments had savings that would earn them more interest if the interest rates went up.

If I have to fund £100 in a year and the interest rate is 0% the cost of paying in a year’s time will be £100 now

If I have to fund it but the interest rate is 100% then I only need put aside £50 now because I can earn the other required £50 in interest over the next year

So, if the interest rate is higher the amount I need to put aside for a future bill is lower

Does that make sense?

Yes and no. It makes sense if I have the £50 and have it in an interest bearing account. But I thought the problem for Government is that they are in debt and don’t have any money stashed away earning interest. I’m obviously being a bit thick here.

This is the accounting framwork they chose.

It is their decision to account in this way.

It is their belief this is true and fair.

And they claim there is a debt

Their accounts show there is not in the way they claim.

That is the point. Undestand I am engaging with the narrative. All accounting is about narrative. It is always about a chosen perspective. I am using theirs to show that their claims make no sense.

That makes sense to me.

It seems highly relevant despite different details, to how in 1977, I took out a 90% repayment mortgage, debt was 2.5x salary, repayments about 23% of salary cheque.

With interest rates at 17-20% and inflation hitting 20% +, my equity quickly and painlessly rose from 10 to 25-30% and on and up, and the inflation on my salary allowed me to keep payments steady as debt and hence interest decreased, hence I repaid capital faster than expected, so I paid it off years early. It always seemed wrong to me that I did so well out of the oil price shock. But in high inflation times, your debt got less and less.

Others who had taken fixed rate deals a few years earlier at lower rates, got big shocks when deal expired.

Of course Pension payments will be reduced in an ongoing manner, contrary to previous expectations as Life expectancy has stopped rising and is indeed falling, so fewer will reach pension age and once the war time generation and early boomer generation die, the total pension payout both public services and state will reduce dramatically, whilst the payments to the pension pots (held by HMT but not isolated) continue to rise…..

That is not the reason for this change

OK, the goverment has decided that higher interest rates reduce the provision the government makes for pensions and this has the consequence for the National debt you are pointing out.

Can you or someone else please explain how this bit of financial tomfollery is achieved?

Pensions the goverment is liable for (whether basic state or those of their employees such as civil servants and teachers) are met out of current expenditure, not from any accumulated fund as private pensions are.

How does the rise in interest rates reduce the sums going to be required by the goverment in future years?

If I have to fund £100 in a year and the interest rate is 0% the cost of paying in a year’s time will be £100 now

If I have to fund it but the interest rate is 100% then I only need put aside £50 now because I can earn the other required £50 in interest over the next year

So, if the interest rate is higher the amount I need to put aside for a future bill is lower

Does that make sense?

I really hope it changes their narrative. But for some reason I highly doubt that Reeves or Starmer will admit that there is now no blackhole. I expect them to continue to push their incorrect black hole narrative, and that more “difficult decisions are to come”. But I really hope something positive comes from this.

Richard, perhaps I am being obtuse but while the presentation and analysis is amazing I cannot quite work out exactly why the effect of the interest rate rise has just such a dramatically large impact on the balance sheet? Can you tease that out?

I am sure the impact of inflation, ironically is beneficial for government from the perspective of the outstanding debt, but that is a separate issue.

If I have to fund £100 in a year and the interest rate is 0% the cost of paying in a year’s time will be £100 now

If I have to fund it but the interest rate is 100% then I only need put aside £50 now because I can earn the other required £50 in interest over the next year

So, if the interest rate is higher the amount I need to put aside for a future bill is lower

Does that make sense?

May I suggest that some commentators are missing the point that this relates to a forecast. How much will we need in order to fund future pension liabilities – liabilities that extend over tens of years? With the interest that can be forecast to be received at a higher level than it was last year, the amount that is forecasted to be needed is less.

But, with respect to economists everywhere the figure is useful only to compare the figures for this year with last year. None of the figures are actual. Forecasts can be wrong.

Entirely correct

But this is their accounting using their perspective and they cannot therefore claim there is debt when thee accounts show there is not.

Your example is effectively a PV. The reason I hesitate is twofold:

1) The sheer scale of the drop in liability, for the rise in interest rates; it is halved. I recognise there is a huge switch round in provision financing costs, but Note 23 you did not reproduce that I could see, and I can’t quite grasp what is actually going on.

2) The interest rate is ephemeral – here today, gone tomorrow. Even the BoE claims interest rates will fall, so in a few months the benefit arising in provision terms, could in turn be be halved (at least in theory, and illustrative). This seems to me an unstable basis to change a provision so much because of the inherent uncertainty of the assumptions about future rates. I leave to one side the problem of finding any valuation; and here I agree with Clive “So why do we obsess about the size of the national debt?”.

Two reasons; first, those whom are best served by everyone worrying about it are determined to keep it that way, because it is in their interest to protect the status quo at all costs. Second, Government has learned to do this for three hundred years (and Britain was well served by the advantages it gave Britain for long periods); and government is spooked by the thought that the public understands how the time value of money works, to spend now and postpone payment (until it is much less material).

I question why IFRS is used

I question why these costs are accounted for as they are

I question why gilts and central bank reserve accounts are liabilities when they are capital

But, this is their accounting using their perspective and they cannot therefore claim there is debt when the accounts show there is not.

I am challenging their narrative using their data

I am not pretending the accounts are right. All accounts are narraive from a perspective. They chose this perspective and their narrative based on it is wrong. That is what I am saying.

Now you have addressed the issue in this form, it does also raise the matter of how best to deliver a transparent set of whole of government accounts.

This is relevant, and it affects Scotland significantly (in an out of proportion way) every single year with GERS; which of course, deliberately, is a strangely conjured accounting confection, presented in isolation from any UK accounts – quite obviously so that nobody can reconcile anything with UK Government accounts, or anything at all outside itself. Extraordinarily, hardly anyone outside this Blog ever challenges the obvious, comic absurdity of that calculated insult to our intelligence; least of all our economic fraternity, or the Scottish Press and media.

Much to agree with

I think the point here is that accounting data should be understood (particularly its limitations) and used properly. There is no “new” £1+ trn to spend….. rather (1) the fiscal rule that was constraining expenditure was absurd in the first place and (2) rules that might have meaning/value for a company don’t have the same meaning/value for a State reporting in its own currency.

Should a balance sheet include liabilities? Yes. Are Public Sector pensions a liability? Yes.

So, what “number” should we put into the accounts? Well, let’s consider a company offering a defined benefit (DB) scheme, first.

The company makes promises to its employees to make payments when they retire. We don’t know exactly what the payments will be – that will depend on the final salaries of existing employees, inflation and longevity. We ask the company to ring fence money to make sure that they are “good for” the pension payments and the obvious question is “how much should they put aside”?. Now, the truth is “we don’t know” but we can make an estimate and ask the company to hold assets equal to that number to meet their pension liabilities. So, if the company goes bust there is enough money left to pay the pensioners. That estimate depends crucially on interest rates and if rates are volatile so is the value of the liabilities. It also represents a price that a company could bay today to get someone else to take on the liabilities… and in some cases (where the scheme is quite mature ie. nearly all retired) companies will offload the risk for a one-off payment.

Now, theses rules where put in place to protect (current and future) pensioners but have had unintended consequences. It has accelerated the switch away from DB schemes and encouraged buying bonds rather than other assets.

Moving to government. As a starting point, why not use the same methodology? In the absence of a better idea Government should do the same. BUT (and it is a big BUT) we should be careful not to read too much into it.

Eg. One could think of this number as a single payment today that could “buy” the pensions of the Public Sector….. and it has just got cheaper by £1trn. Hurrah!! But, of course, where would the money to make the purchase come from? It would be borrowed….. at the new higher rate.

My fundamental take away from this is that the changes in Present Value of liabilities (pensions) and assets (future tax revenue) are massive…. So why do we obsess about the size of the national debt?

Your last point is the right one

But let’s be clear this does matter

Private setcor accounting – as you describe it – is being used here

And what is happening here is the corollary of what is happening in indexed bonds – their cost increases with inflation, this liability has been reduced by higher interest rates – the government cannot obsess about one and not the other, so this does matter.

A video is also coming on this

In that I argue that if gilts and central bank reserve accounts are really capital – and they are – there is no national debt at all

Yes, once again “micro” solution (in this case Private sector accounting) does not make sense at a “macro” level (ie the State).

And, yes, as you also say it IS important…. but only if use the data to drive policy. Is is better/easier to get better presentation of the full data…. or accept that we can’t get the full data and stop worrying about “rules” and focus on what matters – wise use of the nations resources? I think the latter is more feasible.

As I hint at – this method of accounting is wrong for governments. You obviously agree. I agree with your conclusion.

This surely ought to be headline news – – every month’s miniscule change in prices, interest rates or unemplyment gets headlined – but this should be massive.

Joe public is drowning in spurious narratives about tax and spend and debt and deficit.

Is even the Guardian or FT going to highlight this.

Maybe Richard you should offer them a piece on it.

I doubt they will take it

Richard,

Should we / I be sending this to the Scottish Government? If RR has put her name to this then she can barely argue against it.

The Scottish Government should be questioning Westminster’s current black hole assertion and demanding better funding and a return of the WFA.

Or is that too simple?

John

Why not? Give it a try.

Are you not saying yourself, however, that there might be some massive problem with the way these accounts are prepared so that we don’t have that extra money, but because the government has said they accept the accounts they have to accept the existence of the money, even if it may not actually exist?

The proble. with these accounts does not effect anything I am saying here

The big issue you are missing here is that it only makes sense by looking at both sides of the balance sheet.

There is a (significant) liability for public sector pensions. The government has made promises to pay employees when they retire and is expected to honour those promises, so there should be no denial that a ‘debt’ exists.

In order to put a value on the debt, standard DB pension discounting methodology has been used, albeit with more optimistic assumptions than private DB schemes could get away with.

This inevitably means that, as interest rates change, the value of that liability will also change.

For private sector DB schemes, if interest rates go up, the liability goes down and it is genuinely the case that assets can be invested at higher rates to meet that pension promise. However existing (fixed income) assets go down in value, so the net position is somewhat mitigated, depending on how well matched the scheme is.

Because the government has no assets backing these liabilities and does not intend to invest assets at the new higher rate, then you can’t just look at the liabilities in isolation.

As these pensions will be funded from future borrowing, the cost of that future borrowing at higher rates need to be taken into account. Which basically gives you an increase of £1.5Tn, exactly offsetting the impact on liabilities.

There is no ‘free money’ created, all that has happened is that liabilities have gone down and this has been compensated by an increase in borrowing costs.

Effectively

A Downing FIA

Politely, take that up with the government and the NAO, both of whom say the presentation they have used is true and fair. If you disagree, your problem is with them, not me. I am just using their narrative, which also accords with IFRS.

But if you are right then in practice there is no liability – because future tax revenues will always cover sums owing with a massive margin, and legal backing. I really can’t lose on this one.

Richard, forgive me, but as someone unfamiliar with accounting I don’t understand *why* high interest charges have reduced the provision for pension costs.

If I tried to tell someone how the deficit had fallen by £1.5 trillion over the past year I’d be at a loss as to how to explain the reduced pension cost provision.

“the cost of financing future pension obligations fell very dramatically because of the increase in interest rates, which therefore meant that a much smaller provision is required for such costs,”

If I have to fund £100 in a year and the interest rate is 0% the cost of paying in a year’s time will be £100 now

If I have to fund it but the interest rate is 100% then I only need put aside £50 now because I can earn the other required £50 in interest over the next year

So, if the interest rate is higher the amount I need to put aside for a future bill is lower

Does that make sense?

And when rates go back down, as you have been calling for for ages, then this will reverse itself.

There is no new money amiable now, just as there will be no shortfall when the position reverses – this is purely an accounting issue, not a real cashflows issue. As a former accountant you should understand that.

Note, that as I said, whatever I say the Bank of England is saying rates will not fall much – and Trump is going to increase them

Stop silly point scoring is my suggestion to you

And I am not a former accountant – I am Professor of Accounting Practice, Sheffield University Management School

Hi Richard

Really fascinating but I’m not an economist or accountant. Could you explain in layman’s terms how “interest rates rose so much that future pension costs are now considered to be vastly more affordable.”

Many thanks

See another reply already posted on this

No, national debt hasn’t fallen by 1.5 trillion.

It is pretty important to distinguish between national debt and other liabilities, which you do not do here.

It’s also pretty important to understand that the discounted pension cash flows are only one side of the equation. You also have to discount the asset side (in this case the funding provision) as well, so the net change in financial position for the government on this case is zero. Indeed, depending on the discount rate used (Gilts + X usually) and the real uprating of pensions (triple lock) the reality is probably far worse than what is shown above.

On a different note: I seem to remember reading one of your posts a while ago ( I think on sustainable cost accounting?) ithat you don’t agree with discounting future cash flows in principle. Do you now?

I am using their chosen framework to argue with them

And no, in that case you do not discount the asets – unless they are deferred. It appears you do not comprehend that

And then let’s ask the obviopus questions. What is debt that is never repaid? Capital.

And what is money created by the government? Capital.

So, where is the liability here?

A few points to make here.

Firstly, you are conflating government debt with government liabilities. Pension liabilities are unfunded and considered off balance sheet in the UK system. You cannot directly equate the two in accounting terms without bringing them directly on balance sheet.

The actuarial valuation of these pensions is present value off the gilt curve (plus a spread most likely).

There are no current assets held against this liability.

Therefore the assets are future debt issuance and/or tax receipts. The appropriate accounting and actuarial treatment of this is also to PV. Which would also reduce the value of them.

It is therefore totally inaccurate to claim that government debt has fallen by 1.5trn. you can say liabilities have fallen, but given the effect on future cash flows the net position of the government is unchanged. You have to account for the asset side as well, not just liabilities in isolation given you are claiming that the decrease in liabilities means spending can be increased. You are effectively double counting.

Lastly, you said when discussing SCA that the full value of all “climate” liabilities would need to go on corporate balance sheets in completeness, upfront with no present valuation of the liability allowed.

If this is your view there, but your treatment of the pension liability above allows present valuation, I would just like to clarify if you accept the need for it or if you still refute it?

With the greatest of respect, you really should know what you are talking about before writing here.

You say that pension liabilities are off balance sheet, but the whole point is that they are on the Whole of Government Accounts balance sheet, as they are in International Financial Reporting Standards accounts.

So very politely, you are talking utter drivel and are now blocked.

There aren’t any assets backing these liabilities, that’s the point you keep ignoring.

Is it because you don’t understand this, or because it blows a hole in your entire argument?

Wow – that’s staggering

The asset is the legal right to a future income stream

And the legal right to create money

Do you have any comprehension of economic and legal reality?

A commentator literally says that pension liabilities are considered ‘off balance sheet’, by whom isn’t clear but it would be nice to clarify who it is that the commentator is referring to.

Your inference is that the commentator is themselves saying that they are ‘off balance sheet’ and to block said commentator. Just wowsome logic

Pensioners liabilities are glaringly obviously on the government balance sheet or we would not be discussing them in the context of their accounts.

It would seem that you and the commentator are both foolish enough not to notice that.

Our country is now at war with Russia. The firing of British cruise missiles has brought it about. The UK is in danger like never before yet all the media are silent . During my lifetime I have taken part in massive protests against the possibility of war . The establishment of American missiles and bases. Why no banner headlines.? Most people I speak to don’t even know we are at war. There is no popular mandate for war. It is not debated in Parliament.

There are 11 American bases in middle England . Near where I live

in Milton Keynes. These bases which bear the name RAF are the most logical targets for the Russian hypersonic missiles against which there is no defence. The travel at 10 times the speed of sound and can do as much damage as a nuclear missile. Targeting these bases would attack two of Russia’s main allies at the same time. Where are the warnings? Where are the banner headlines. Our missiles are useless against the Russian defence mechanism . Armageddon is possible. My information comes from retired American marines and CIA operatives who have reliable contacts . See YouTube. Massive protests are needed like never before.

I live near Mildenhall…

It does not feel comfortable

40 miles from the Holy Loch.

It’s not easy to relax.

I worked through the beginners videos you did on youtube. They are excellent. I realky feel you should produce a major course for those of us who would really like to understand this better (not just mmt)

A full dummys guide please, !

It is soemthing I am thinking about

Just to say thankyou for explaining the interest point about the pension provision.

I’m so glad I wasn’t the only one who didn’t ‘see’ it!

Tax research.org.uk

That puts in to perspective, just how little the rich gave to the many millions in poorer communities for climate damage mitigation. We should be wiping out the debt of the poorer countries!

Your tax research shows that the government are not implementing policy, they are signed up to which is evidence based policy. Transparency goes hand in hand with evidence.

A bit late in the day, but why hasn’t the OBR made any comments on this?

I’ve always felt they serve no useful purpose, so I can’t say I’m surprised, but shouldn’t they have commented.

They will claim it is not in their remit

Richard Murphy said “But if you are right then in practice there is no liability – because future tax revenues will always cover sums owing with a massive margin, and legal backing. I really can’t lose on this one.”

How on earth do you come to this conclusion from the evidence presented?

Current tax revenues don’t even come close to matching sums owing, hence the vast amount of government borrowing required in an annual basis.

There is quite clearly a significant liability being built up for public sector pensions (and even more so for the state pension), which needs to be funded from tax revenue, where that tax revenue is set to be insufficient and becoming more so, based on projections from a variety of different organisations.

Your basic premise is at odds with all know government borrowing forecasts – what numbers are you using (and from what source) to come to this conclusion?

A Downing FIA

With the data available, how can you say that

Odd

Two email addresses

Two ip addresses

No trace of a person of your name on the website of your claimed employer, or anywhere else

A troll?

Your lack of understanding of assets, cash flows, legal, entitlements and money creation suggest a maybe lackmof understanding of the issue you claim to have knowledge of

Richard, apologies if I’ve missed it but if we include future pension liabilities in the Whole Govt Accts why can we not include future tax income streams too?

As I have noted to others here, I would argue that we should not include pensions as future tax revenues will always exceed them – and money creation can always settle them – but accountancy rules are not intended to reflect that reality. But that is another issue.

Thanks Richard, you are giving me an education every day. Could we not fund the NHS by having a state owned pharmaceutical company that could produce all the generics. We would be able to create skilled jobs in science and medical research. We could find new antibiotics and I can’t understand why we haven’t already done this.

I suspect we do not need to do so

Generics are not the issue

Another great article Richard.

It is genuinely insane that the government is preparing accounts as if it is a private business.

Applying DB when it’s wholly inappropriate is deeply, deeply bizarre.

That said, in regards to this destroying the arguments Reeves is making… I worry that the response would be that clearly we’re on the right track, and we must continue in this fashion to fix the foundations, etc etc. Given Reeves’ pride about running a forecasted surplus during the Budget, and that awful Resolution Foundation paper calling for surpluses to save for a rainy day, it feels like we’re bound for dark times no matter how nonsensical and paper-thin the justification is.

After sleeping on some of the excellent feedback on this blog yesterday, it occurred to me to speculate about what the Tories might have done with this had they won the GE in July. This *was* all on their watch after all. I reckon they could have orchestrated so much positive spin on the back of this. I wonder if they wouldn’t have called this “money from down the back of the sofa” then thought up some dastardly wheeze like tax-cuts for their billionaire backers. It’s a thought. I kind of suspect that one of their Tufton Street egg-heads would probably have seen this coming and, in the event of a Tory GE victory, had a cunning plan all ready. Am I giving them too much credit?

Good old Labour on the other hand, scared of their own shadows, will most probably just ignore it all. Not just hopeless at macroeconomics but clueless about strategic communications. The Tory media would ask them far too many “difficult” questions about something they – Labour – can’t be bothered to understand. You have to despair.

Theoretically, with the Tories in govt, their tame media – equally clueless – could be counted on to back them up in whatever fantastical wheeze they decided to put out there and we would have had to grin and bear it. And would the OBR have cottoned on with the Tories in the driving seat? They don’t seem to have noticed anything so far, do they? Maybe taxpayers have dodged a bullet by throwing the Tories out.

I agree with Stephen Mitchell and John Lawson about the imminence of World War Three and the peril we are in. The former US Ambassador Jack Matlock, fluent in Russian and Ukranian, served as Ambassador to the Soviet Union from 1987 to 1991 and attended the meeting at which the US is widely believed to have promised Russia that in return for Russia agreeing to German reunification, the West would not “leapfrog an inch eastwards”. Matlock said, “Now, there’s been a lot of debate as to whether President Gorbachov was promised that there would be no NATO expansion to the East. There was no treaty signed saying that. But as we negotiated an agreement to end the Cold War, first President Bush, at a Malta meeting in 1989, and then later, in 1990, almost all the Western leaders, told Gorbachov: if you remove your troops from Eastern Europe, if you let Eastern Europe go free, then we will not take advantage of it.” Speaking in 2015, Jack Matlock added, “I think we’re in a very dangerous situation right now, in regard to Russia, over Ukraine. Six months ago, a year ago, when people were talking about Cold War II, I said, this is silly; this is not Cold War II. The Cold War was about a worldwide confrontation over ideology; it was about communism. And the conflict with communism. And it occurred all over. Latin America, Africa, Asia.

Now what we’re seeing now is a conflict in an area which 30 years ago would have been a local problem, in one country. How can that lead us to Cold War II?

However, as things have developed, and as I see debates now as to whether the United States should supply lethal weapons to Ukraine, I wonder what is going on.

When I see all these debates and saying, oh, Russia’s only a regional power. What does that mean? What does that mean particularly in their own region? And I think the elephant in the room, which nobody is referring to, is the nuclear issue. No country which has ICBMs, ICBMs—10 independently targetted warheads, very accurate, mobile (so they can’t be taken out)—no country with that is a regional power, by any means. It can mean other things.

The most important thing we did in ending the Cold War was cooling the nuclear arms race. If there are any issues for this country to face, that are existential, that’s it.

But, I’ll tell you. If the United States gets further involved in what is, in the minds of the Russians, territory which has historically been part of their country, given the present atmosphere, I don’t see how we are going to prevent another nuclear arms race. And that’s what scares me.”

https://jackmatlock.com