The Bank of England cut interest rates slightly yesterday, against my expectations.

Noting this, nothing they did changes my sentiments expressed in my video and post published yesterday. There were many reasons for that.

First of all, the vote at the Bank of England was 5 to 4 to make this very modest cut. There is no confirmation as a result that this direction of travel will continue. The UK economy badly needs major cuts in Bank of England base rate. I have no confidence that they are on their way.

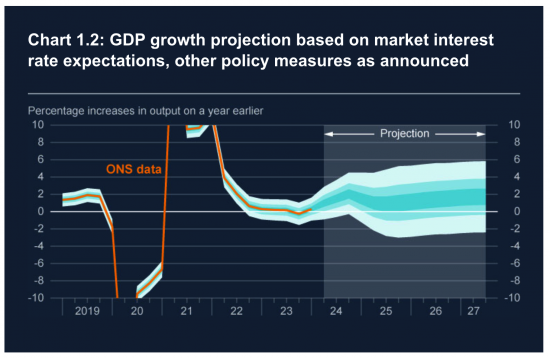

Secondly, that is despite the fact that, as this chart published by the Bank yesterday shows, it is their belief that inflation is now well and truly under control.

Whilst, due to a statistical aberration, the reported inflation rate will increase later this year, the Bank would appear to be confident that the trajectory of those rates is markedly downward, with the expectation being from 2025 onwards that rates should be below 2%, which is the target. This table makes that clear for the later periods.

What that same table makes clear is that the Bank has no intention of cutting base rates significantly despite the fact that inflation will run below expectations from 2025 onwards. The plan is to restore real interest rates to a level of about 2 per cent.

The real problem with this plan is that the higher the real interest rate, the greater is the cost of investment. Investment has been low since 2008, and the real interest rate during that period has, most of the time, been negative. How and why the Bank believe that investment might increase because it is now going to impose positive real interest rates on the economy is very hard to work out. Most certainly, the bank is continuing to work against Rachel Reeves' objective of delivering growth.

To continue to justify this policy of high interest rates, the Bank would now appear to be adopting a number of ruses. For example, it is creating a variety of inflation rates to suggest that it has reason to be concerned even though the overall level is below the target rate. So, for example, they produced this chart which differentiates inflation and inflation excluding energy costs, which it is expected will fall:

The increase in energy costs was, of course, one of the major and entirely external reasons why inflation rose in the first place. Now that it is falling it is being used as an excuse to keep interest rates high. That appears to rank as hypocrisy.

The same is true when they seek to differentiate inflation rates for physical products and services, as they are. Throughout the whole history of inflation, the single figure in an index for the change in this rate will have always reflected considerable underlying variations in the rate with regard to differing goods, products and services. That is inevitable and should be widely known. It must have been known by those who set a target based on the single index figure. But now the Bank is trying to argue that because the rate of inflation in services is above target, even though there is actually deflation in the price of goods within the UK economy, they have reason to be concerned about inflation rates in services when that figure is not their target, but the overall rate is. I believe that this action on their part is disingenuous. I believe that the resulting policy is also deeply damaging.

The net outcome of all these shenanigans is that the Bank is honest about the fact that growth is going to be weak. It will be lower than many other economic areas:

Unemployment is also going to rise, as I have long suspected is the Bank's aim:

And, this punishment will be delivered so the Bank can overshoot its totally arbitrary 2 per cent inflation goal:

And just for the record, the Bank has not delivered the fall in inflation. It happened everywhere. The cause of the inflation and its decline must be external in that case, as I always argued. Panic buying after Covid and market rigging when war in Ukraine broke out created inflation, and increased interest rates did nothing to correct those things:

So, we end up with a situation where rates remain massively above any rate required to control inflation and any rate required for the well-being of the country, its economy and the people who live here.

Worse, the only thing we know is that the Bank intends to maintain strong positive interest rates that will continue to depress the net incomes of millions of households in the UK as they struggle with mortgage and rent costs. At the same time, the incentive to invest will be low. Just about nothing Labour wants will happen, and apparently, Rachel Reeves is quite content for this to happen.

Watching the news last night, it seemed as if there was a celebratory mood at the news of the puny cut in rates the Bank announced. I feel nothing of the sort. My concerns about the Bank and its destructive and unjustifiable policies remain as profound as ever.

Nothing suggests to me that it has the interests of this country at heart.

Everything suggests to me that we have a central bank and government who at least think that they have their feet on different pedals when it comes to economic policy - one on the accelerator and the other on the brake. Nothing good can ever come of that.

We're in an economic policy mess. It's time to admit it, and sort it out.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

You don’t say why..why would they want unemployment to go up?

To reduce demand and so inflation…

In their minds these are related

People who are unemployed suddenly don’t need food or housing? Is that the reasoning? Or is it that the unemployed don’t have spare cash to spend on going out etc, which will indeed reduce demand for entertainment and similar services. But then you’ll get restaurants and pubs going out of business, so I’m mystified why it’s seen as a good thing.

I do not understand the Bank either

Much to agree with. Outside of this blog, in the MSM, there is no discussion on the points raised/made. The BoE is treated as some sort of priestly college – guarding the sanctuary and never questioned, because……..

At the risk of sounding like a broken record, if it is not possible to hold substantive discussions (of the sort in this blog) with those that “guard the sanctuary” & politicos on issues of importance to the whole population (e.g. employment) then we don’t have a democracy.

The silence from those recently elected/selected is instructive, the failure of the MSM to question politicos ditto.

You hit a nail on its head

Absolutely… Worse still than the BoE and its praetorian guard’s reluctance to engage – I only noted one very brief self congratulatory interview with a very smug Andrew Bailey yesterday – there are few if any, meaningful pieces in the wider MSM, that open up, rather than close down discussion on monetary policy, let alone wider macroneconomics.

More often, uncritical reporting fails to raise any questions as to the role of the BoE and its bias, let alone question the democratic deficit it represents.

The quality of macroeconomic debate depends on it being aired in the first place.

Even the basics of MMT are still very much suppressed, and/or misrepresented, and neoliberalism is barely raised as the dogma driving this new government as it did Hunt and predecessors.

The “maxxing out the credit card” lie was peddled again by Reeves this week, without it being questioned, let alone challenged.

Even taking the Guardian as representing the centrist press, where a balance might be hoped for, Larry Elliott occasionally references MMT and associated matters, but far too often peripherally. Chakrabortty is thankfully more direct in linking Osborne’s austerity with Runtonomics, but Toynbee is nothing more than a starry eyed Starmer fangirl, and it seems Blair is still writing Rawnsley’s pieces 20 years on. Official orifices.

This is Gramscian hegemony in action. When I was involved in my own very minor way in trying to open up early climate action debate some 20+yrs ago, there was organised suppression seeking to limit the examination of environmental matters, as well as in spiking it through corporate disinformation campaigns, and we are in a comparable setting now. I suppose we just have to keep on banging our heids against that wall.

Much to agree with

Toynbee completed her sell out today

« If the people of the nation understood our banking and monetary system, I believe there would be a revolution before tomorrow morning. »

(From Henry Ford)

The supposed quote was really a paraphrase originally by Charles Binderup 19 March 1937 in the House of Representatives (Congressional Record—House 81:2528):

It was Henry Ford who said in substance this: “It is perhaps well enough that the people of the nation do not know or understand our banking and monetary system, for if they did I believe there would be a revolution before tomorrow morning”.

Note the words “in substance” indicating a paraphrase.

The nearest Ford seems to have come to saying this is a passage in his 1922 book My Like and Work at page 179:

“The people are naturally conservative. They are more conservative than the financiers. Those who believe that the people are so easily led that they would permit the printing presses to run off money like milk tickets do not understand them. It is the innate conservation of the people that has kept our money good in spite of the fantastic tricks which financiers play-and which they cover up with high technical terms. The people are on the side of sound money. They are so unalterably on the side of sound money that it is a serious question how they would regard the system under which they live, if they once knew what the initiate can do with it.”

Thanks, Bernard

“Deathwatch beetle capitalism” is really at its worst with what the Americans call the FIRE sector (Financial, Investment and Real Estate). The US stockmarket is falling because it judges the Federal Reserve has triggered a recession by keeping base rate too high for too long:-

“US investors triggered a major sell-off on Wall Street on Thursday set off by fears that the job market is cooling, manufacturing is slowing and the Federal Reserve has left cutting interests too late to head off a recession.”

https://www.theguardian.com/business/article/2024/aug/01/investors-trigger-major-wall-street-sell-off-recession

Meanwhile over here the inflationary housing bubble is taking off again and the Treasury, BoE, Scammer & Co are all trying to pretend that such an unnecessary inflationary housing bubble has no inflationary pressure on wages. This is a nation run by corrupt and ultimately stupid individuals, stupid because they are weakening the economy and they’ve been doing this at least since the early 1970’s with the Tories’ Financial Big Bang.

https://www.theguardian.com/money/article/2024/jul/30/uk-house-prices-rise-zoopla-homes-for-sale

Why it never occurs to politicians on the left that the FIRE sector knows it’s imperative to control a country’s central bank with its “place” persons eludes me but then we don’t really appear to have any political parties on the left anymore with clout do we!

Typo, I think. Para starting statistical aberration says downward trajectory of interest rates. Should that be inflation rates.

Thanks

Edited

Have Ms Reeves support for the huge new homes building programme, taking money out of circulation and the BoE’s frankly crazy stance set in motion the path to a very deep recession?

Why is it acceptable for newly qualified company/commercial lawyers working in the City to be offered ever increasing starting salaries of currently up to £170k with commensurate increases up the employee chain but a 5% pay award for local government employees will break the UK?

The last point about high inflation being global and going down got me thinking, do you have any data on the (lack of) correlation between the interest rates different countries set and the rate of inflation?

The chart in the blog is some evidence of that

But I have not got time to search out more

Why do you think investment rates were low when real interest rates were negative? Seems odd in one way.

If the biggest customer in the economy – the government – says it will not buy private sector investment is always going to be low. If the government refuses to invest at the same time that makes things even worse.

Not odd at all when you think about it. We have had a 14 year squeeze on living standards for the majority of working people. The cost of living crisis did not start in 2022 (inflation secondary to invasion of Ukraine) or 2020 (Covid). It started with Alistair Darling post 2008 crash and accelerated massively under Gideon Osborne.

If people have no disposable income to spend then why on earth would business invest?

Weren’t rentier returns also much higher than productive investment levels, and the banks risk averse when they could hold securitiy over property ?

Threat of deflation averted then, but always keep core inflation in mind in any assessment. Core inflation excludes food and energy which can be volatile due to world markets, foreign policy decisions and weather. Policy makers always watch this even though it’s not part of the target it’s a significant component of it.

Nonsense

This is just differentiation as an excuse

Better to consider non-core infaltion as that hits lower incomne households harder

An excellent idea

If we are to differentiate between types of inflation, then let government’s primary aim be to reduce that which hits the poorest hardest.

The basket of goods approach was picked up by Jack Monroe highlighting how basic price rises hit the poorest, and how food inflation had a differential effect.

Mr Chen,

“Core inflation excludes food and energy which can be volatile due to world markets, foreign policy decisions and weather”.

I confess that is the most hilariously unfortunate definition of inflation I have ever seen. Of course economists like it, because they can’t handle these pesky phenomena in the real world that are – wait for it – “volatile” – and difficult to forecast easily. This is all rather like a boxer saying to a fast moving opponent he just can’t lay a punch on; ‘stop it; stand still ’til I hit you’.

This is the upside down world of economics; measure that which is inert, static and easy to measure. So they measure everything that is of little significance, just because they can measure it. Economists just do not have the tools, or even the methodology to do much of real significance, so the inflation baskets used are unsatisfactory. We can’t embarrass the “experts” (sic).

I moght add economists are so hopeless, they still can’t forecast what they do flimsily measure, without falling over.

Meanwhile, Mr Chen, the real world is somewhere else, far, far away from all this economic measurement of nothing much; somewhere economists have never seen, or been; or are even interested in venturing. Just sit behind a desk and do some basic, abstract maths, for a living.

You are assuming the economists in question can actually understand the mathematics involved.

Many years ago just after I had completed my PhD, I was asked to teach a course called “Mathematics for Economists”. It turned out that there was no syllabus for it and the person who taught it before had left without leaving any lecture notes. It was assessed by coursework most of which was missing and there were no past exam papers from which I could glean what was required.

I was, however, given a book “Mathematics for Economists” by Taro Yamane. The book obviously contained far too much for the course so I tried to find out what was required. I was not told in so many words, but the requirement seemed to be that all the students produce some impressive looking work and everyone passes. The external examiner would not be a problem because, if a piece of work contained some complicated equations, he wouldn’t be able to understand it anyway.

Economists love Greek symbols. It’s how they prove their virility.

Good morning

I was reading this piece by Dan Neidle today about the government’s £22bn “black hole” and alot of the figures, such as how much tax can be raised through CGT and higher income tax relief reforms, seem to be lower than yours

https://taxpolicy.org.uk/2024/08/01/rachel-reeves-raise-22bn-of-tax/

is his analysis credible?

Sorry – I had to read it

Many figures, such as that on pension tax relief – could come from the Taxing Wealth Report

He is absurdly cautious on capital gains, but good on eliminating reliefs.

In some areas he reveals how pro wealth he is, but overall he is in the right area.

I’ve mentioned this earlier. I suggested then that the BoE is trying to allow the pension funds, in particular, to repair their financial situation. And they don’t care who they hurt. I suspect (but have no evidence to show it) they fear (or perhaps know?) that some funds will be unable to meet their commitments in the not to distant future. Coffers are low after the long years of low interest rates; I suspect these were not allowed for. Now, the need is to protect the system.

This makes me wonder if private pensions based on investing in private sector is actually long term sustainable. Can any evidence one way or the other be provided, as I don’t know where to look?

Rich:

You are about as wrong as you could be, the recent increases in gilt yields (resulting in an increase in the rate at which liabilities can be discounted) means that DB pension funds are in the best health they have been for many decades.

Private (DC) pensions are very different to DB pensions, so you should not compare or confuse the two. If you have questions, you should speak to a professional advisor, not try and seek advice online.

You do know most pension advisers know nothing at all about economics?

Commission rates, maybe, but the economy or even what drives returns? Pull the other one.

The government has a target unemployment rate through NAIRU. How disgustingly obscene is that? If you are unfortunate enough to be made deliberately jobless by economic policy then you are, effectively, ‘working’ for the government to help control inflation. Your reward is less than destitution level benefits.

The BoE aims to protect capital, and the relative profitability of capital, by ensuring that wages are pegged down at every opportunity.

NAIRU is one of the theoretical devices that is used as a tool to justify this wage oppression.

As a tool of suppression, it actively works against both absolute and relative redistribution and to increase the benefits of capital to its managers and holders.

It is a reductive and crassly simplistic concept, linked to the discredited Philips curve, but with the implicit (if not explicit) aim of maintaining low wages. It’s theory, innit ?

Recently, Bill Mitchell produced a graph showing that the average % profits has increased against labour costs, and is still increasing, and we all know the graph that shows % Labour costs in GDP has fallen since the late 70s, so labour takes home a lower share of aggregate economic production, and has done so increasingly, for almost half a century now.

We also know that in the UK wages still have not recovered in real terms, and/or are pretty much flatlining, since 2008.

The BoE is wedded to Thatcher’s aphorism that unemployment is a price worth paying.

(presumably excluding the banksters).

Meanwhile…. at a financial institution near you.

Have just finished reading ‘Germinal’ by Emile Zola and the harrowing situation he describes does not really seem to have changed much in the ensuing 150 years… should we despair or is there hope somewhere?

In social housing -my line of work- Laboured has begun tinkering already.

We can now use 100% of our right to buy receipts to fund schemes (instead of 50%) and can also use them on Section 106 schemes when we could not at all under the Twatties ( I am sure that you know to whom I am referring?).

However, this ignores the fact that our internal rate of return from scheme loans in the housing revenue account effectively tracks the BoE rate, and that the services and material we consume to build affordable homes are also affected by the BoE rates as well, as costs in construction seem to sticking at +20%.

So any gains here are lost because of interest rates. Affordable housing schemes will more expensive and consume available capital and headroom in HRAs.

So to us here in development, none of this makes sense.

Laboured really needs to sort this out.

There is only one government made up of elected members, not two and the BoE needs to be brought to heel and put in its place.

Thanks

Surely there is someone at the Bank of England willing to be interviewed.

Why?

To be effectively interviewed, by somebody knowledgable would expose them all as having no intellectual kit on what so ever.

They ain’t stupid – why would they want to be questioned and thus justify themselves?

Andrew Bailey has scarcely finished his avuncular waffle to the British public on a 0.25% cut in interest rates; and he has already been overtaken by events, dear boy; like an errant schoolboy, unable to keep up with his betters. The FT reports this amid tumbling Tech shares and sharp NASDAQ price falls:

“US bond yields tumbled following the jobs data as investors flocked to the safety of Treasuries and bet that the Federal Reserve — which held interest rates steady on Wednesday — will be forced to respond to a weakening economy with rapid cuts in borrowing costs. The US 10-year yield sank 0.14 percentage points to 3.83 per cent, the lowest since December. Investors now expect the Fed to lower borrowing costs by a full percentage point by the end of the year, implying it will have to deliver an extra-large half-point cut at one of its three remaining meetings. ‘The Fed rolled the dice one more time on Wednesday and they’ve been proved wrong,” said Steven Blitz, chief US economist at TS Lombard.

Friday’s jobs numbers ‘don’t spell recession, but the Fed has to act, and a 0.5 percentage point cut in September is now firmly on the table. They could even move sooner, before the meeting,’ he added.”

The BoE, independent – of whom, of what? This will be interesting.

See my blog post, just published

Thanks Richard.

As this piece says, the initial rise in inflation was due to external factors, and raising interest rates could not affect the UK’s internal inflation rate. Leaving the control of inflation to the BoE, who can really only change interests rates surely needs to be ended asap. As it is, it seems to me that the BoE may be pursuing their own agenda.

In my view this would be the economically competent thing to do. Rachel Reeves surely must have recognised that the UK’s fiscal and monetary policies are fighting each other, as Richard has said. It must have occurred to her that this is an untenable situation, so the BoE needs to be brought back into the Treasury, correcting Gordon Brown’s error.

The sooner the better.

The ZIRP policy pursued by the BOE and other central banks after the GFC in 2008 upto 2022 did little to help spur investment in the real economy. As the West stagnated China’s economy continued to go forward with it becoming the workshop of the world. Labour productivity in the UK has remained low as it has in many western economies. Now the current high rate policy is very punishing for both investment and for consumers whose spending is a key driver of the UK economy. High interest rates make it so much harder for ordinary people and small business to pay off loans, credit card debt etc.

Let’s be honest the Bank of England doesn’t give damn about the struggles of ordinary people to make ends meet. For most of its history it was a private institution committed to looking after the interests of the rich. Nothing fundamentally has changed in its outlook despite being nationalised by the Attlee government in 1946. The way it bailed out the too big to fail banks after their criminal activity brought about the GFC in 2008 illustrates my point.

The new government is also committed to sanctions on Russia which have deprived the collective West, especially the EU, of a source of cheap energy. The sanctions have done little to damage Russia’s economy but have are a self inflicted economic wound for the West including the UK. Another complicating factor for the UK and western economies is the Houthi blockade of the Red Sea which is driving up prices due to the much longer routes which shipping has to take. The UK economy will be further hit if Trump is elected and steps up the trade war against China. This could have significant impacts on western trade with China depending on how far Trump takes things.