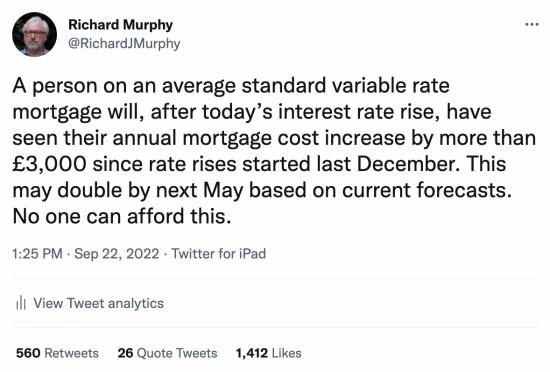

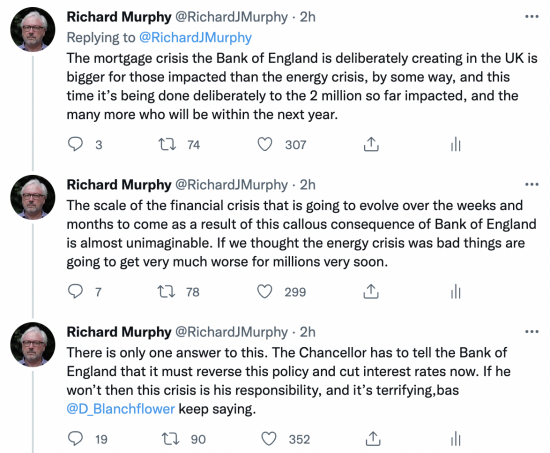

I posted this on Twiter today:

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I think we will be eternally grateful that when our Co-op Bank mortgage was up for renewal in January 2022, then we opted for the slightly more expensive (at the time) five year fixed rate offer. I think the US system where the rate is fixed for the term of the mortgage would be better as that way the borrower knows where they stand and is not at risk of being wiped out by arbitrary changes they can’t control.

“I think the US system where the rate is fixed for the term of the mortgage”

completely disagree, you are taking a high 25/30 year bet at an arbitrary point in time ie when you buy. People could have been locked in at 12-13% from the 90s. What we do know is that interest rates can’t go through zero so where they and the were rock bottom and the term structure was flat it really was a brainer to lock in for as long as possible.

But they knew they could afford it

I think people want security. For example the whole issue about pensions. Some nebulous ‘it might be cheaper in ten years time’ really does not figure on the time line. While ‘sign on the dotted line and it might cost you triple next year’ probably does.

As I understand it, US mortgages are usually fixed for the term, but allow early repayment. So the borrower can usually remortgage if a lower rate is available.

Thankfully our mortgage was recently paid off, but we went for a series of 5 year or longer fixes, probably paying over the odds for most of the time compared, for example, to a tracker or a set off mortgage. But at least we got what we paid for, which was certainty that the monthly payments would be affordable.

Banks should not be allowed to increase their mortgage interest rates mid-term. They are already making money from you, and will continue to do so until the mortgage is paid off. In some ways it will be worse for people who rent, who will have to pay more to fund someone else’s mortgage.

I agree.

As far as I am concerned, variable rate mortgages are a lender bet on higher income from higher interest rates – not really a choice to borrowers.

It’s a con.

Surely the Govt must realise that “Middle England” cannot afford such increases. In the late 1990s, it was widespread negative equity which swept in New Labour.

Or will the tax cuts be enough to buy them off in sufficient numbers to win the next GE? If England continues to elect such imbeciles, how can the Union possibly survive?

They are so out of touch with reality they really do not care