I have published a new paper this morning as part of the work I am doing that is funded by the Polden Puckham Charitable Foundation on how to pay for a Green New Deal. In it I ask whether Mervyn King was right to suggest, as he has, that quantitative easing has inevitably resulted in inflation. As the introduction notes:

There have been widespread reports that Mervyn King, the former Governor of the Bank of England is now deeply critical of Andrew Bailey, his current successor in office. King's claims appear to be threefold.

First, he is suggesting that the Bank of England was far too willing to use quantitative easing during the COVID crisis, with it in effect funding government expenditure during this period.

Second, he says that this willingness to create new money during this period has now led to the current inflation crisis.

Third, it is King's suggestion that the Bank of England realised this far too late, and therefore reacted too slowly to the onset of the current inflationary period, failing to increase interest rates at the time when King suggests that this was required. Quite when that was is not clear, but it was definitely before they acted.

Add this all together, and what King is really saying is that if you print money you get inflation[1]. Unsurprisingly, this simple notion which has long been beloved by right-wing politicians has now won support and amplification by those politicians and media friendly to their cause. The obvious question to ask in that case is whether King is right?

I would not, of course, have written the paper if I thought he was. What I assemble is data that shows that although QE clearly did increase the money supply it did not in any way influence inflation upward. Indeed, there was no hint that inflation might take off until the autumn of 2021 when it was very apparent that it was other factors (Covid reopening, supply chain issues, war, sanctions, energy company profiteering, etc) that very obviously created the situation we now find ourselves in.

That research is in part based on long term inflation data, including this from the Bank of England via the St Louis Fed:

The QE period has not been inflationary: it has been exceptional for its stability.

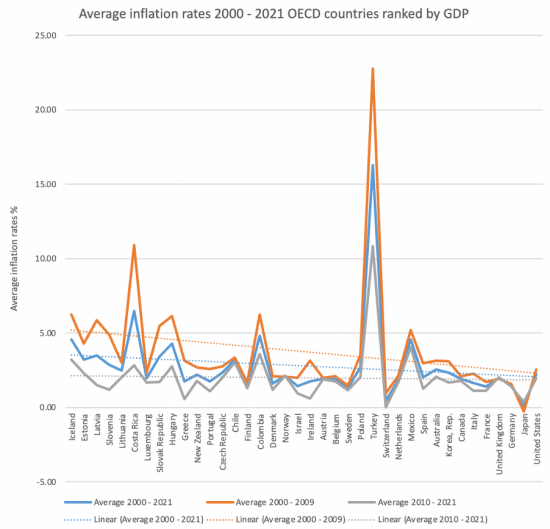

There is more evidence on this from inflation data from the World Bank that I have analysed. Take this data for the OECD:

From 2000 to 2009 inflation rates were markedly correlated with the size of an economy. From 2010 they have been stable and lower for eleven years. The QE era delivered stability. As a result I suggest it is impossible to claim that an eleven-year lag suddenly reversed in late 2021 when other causes of inflation are so easy to find. Money creation was not the cause of this problem.

What do I suggest as a result? This:

If Mervyn King has got everything wrong about inflation, as has the Bank of England, what should be done? I suggest the following:

- Since the inflation we are facing is beyond our control now, largely arising outside the UK, no monetary policy reaction is required at all. Interest rates should be cut to where they were in mid 2021.

- Make sure people survive this inflation i.e. protect the vulnerable who might otherwise suffer as a result of their loss of purchasing power (which should be the priority now). The UK government is now showing some awareness of this need, but it is partial.

- Provide support for business to prevent the risk of recession caused by people buying less as a result of the poverty created by inflation. This will probably require selective loan schemes of the sort required during the Covid era, but with considerably more vetting being applied. This is especially important because unless it happens the current pressure on spending power is going to spillover very quickly into serious unemployment.

- Address the systemic issues giving rise to the political, economic or social failure that resulted in the inflation. So, in the UK's case:

- address Brexit;

- continue measures to tackle the impact of Covid on society;

- tackle the causes of war in Ukraine;

- address the vulnerability in supply chains;

- reform energy supply and make it more sustainable, and

- address the global crises (I use the plural deliberately) developing around food, climate change and other pressing issues.

- Stop the government profiteering from this inflation. So, for example, in the short term the tax take on fuel and energy might be capped at 2020 rates meaning that VAT or duty cuts could be put in place to reduce inflation without imposing cost on the government, who otherwise profits from rising prices[2].

- Change taxes to take purchasing power away from those on high incomes and earnings who represent the one part of the economy where demand-pull conditions might exist.

As I conclude:

As this note shows, the claim made by Mervyn King that quantitative easing is the cause of the current inflation in the UK is wrong. The facts do not fit his case. The economic theory he uses does not fit those facts. His prescription is as a result also wrong. In fact, what he would do if he succeeded in having his way would make the economic situation in the UK very much worse. That is why we have produced this note.

Constructive criticism is, of course, welcome.

[1] Kings claims can be found here https://news.sky.com/story/cost-of-living-bank-of-england-shares-responsibility-for-crisis-former-governor-says-12617190. The most detailed discussion of what King actually said in the Sky interview is here https://moneyweek.com/economy/uk-economy/603604/quantitative-easing-too-much-of-a-good-thing. Other coverage is at https://www.theguardian.com/business/live/2022/may/20/retail-sales-inflation-consumer-confidence-thg-ftse-economics-business-live; https://www.independent.co.uk/business/central-banks-drove-inflation-by-printing-money-says-former-bank-boss-king-b2083627.html; https://www.spectator.co.uk/article/mervyn-king-needless-money-printing-fuelled-inflation and https://www.euronews.com/next/2022/05/20/britain-boe-king

[2] This is clearly not a long term policy That would require that the cost of fossil fuel energy change to price it out of the market.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Kings is yesterday’s man, a dinosaur and either mis-guided or a liar who knows that all interest rises do is fill the pockets of creditors enabling them to get inflation generated profits on money where the interest rate was already agreed previously on credit (that’s how I see it anyway).

It’s about time he wound his neck in.

I am amazed that the views of Lord King receive any credence when he was the Governor of the Bank of England at the time of the financial crisis. I always imagine the Queen was thinking primarily of him when she asked ‘Why did they not see it coming?’.

I can see two immediate and rather large issues with what you have done.

The first is that you have compared nominal money supply growth with the year on year annualized inflation print. Which you can’t do if you are trying to compare them. You have to do it on the same basis.

If you compare the nominal CPI index with nominal M2, or the annualized yoy CPI with annualized yoy M2 growth, you see a very different picture.

They are highly correlated with M2 leading CPI.

Which suggests Meryvn King has a point.

I also note you have done no regression analysis, or any other statistical test before coming to your conclusion that money supply has no effect on inflation. Did you just eyeball the chart before making that claim? If so, you can’t really make it.

Your second problem is when you discuss QE and inflation across different countries.

Within this, your basic argument is that average inflation over the period from 2000-2021 (notably excluding the high inflation 2022) has decreased, regardless of QE.

Whilst this may be true, you can’t draw the inference it is because of QE. There are too many variables to consider it a linear relationship.

You simply cannot look at a host of countries as you have, some which experienced QE and some which did not, and all QE was to differing extents, then make the claims you have done. The fact that average inflation rates reduced across the board suggests QE was not the driver of this at all.

You could also argue, just as one of many potential reasons, that the period in question coincides with the era of independent central banks and inflation targeting. Which suggests that current policy on the whole has been successful, and that monetary policy (interest rates) under the control of an independent central bank is indeed the best way of controlling inflation in the long term.

I feel that you haven’t actually set out to do any research. You had an answer already in mind when writing this “paper” (which is not an academic or peer reviewed paper as far as I can tell) and then headed for that answer as fast as you could without doing sufficient (or really any) real analysis.

The whole point of research is to use the data to lead you to a conclusion, but you already had the conclusion firmly in mind and the data you used doesn’t tell you anything about that conclusion.

Of course I had a hunch in mind

I did research

And I have e provided my evidence that is clear

And the evidence holds, as I show, over a wide range of situations

I also show there is no link with M2

Now, why not address the issues?

Oh, and I am not convinced by your email address

Send your CV next time you post or you won’t get on

Neo-liberal advocates don’t like hunches about what is wrong with their world view.

Because most Neo-liberal advocates get paid to write absolute tosh in support of their lies and deceit.

Writing something just because you have hunch? All that effort? For no personal gain other than insight or learning?

Heavens, no!

They just don’t get things like curiosity, research, tri-angulation, real knowledge.

Neo-liberalism is fiat economics: they just made it all up from nothing; and nothing it is.

And nothing is want we less of please.

Incredible. There are three candidates that could be considered major causes of inflation; Covid, War and QE.

Why would QE be at the top of the list when, for many years, it has not delivered inflation? Whereas War is a well known track record as a driver of inflation (with evidence to support it).

Bankers got it wrong in the 1930s. Keynes contradicted them and got it right.

The financial crisis was brought about by over lending.

Allen Greenspan confessed he had it (sort of ) wrong. https://www.theguardian.com/business/2008/oct/24/economics-creditcrunch-federal-reserve-greenspan

Their forecast that austerity would balance the budget by 2015 ( and the Trioka’s forecast for Greece) were wrong.

When Gove said we’d had enough of experts, did he have these in mind? I doubt it.

What you are arguing is that consumer inflation doesn’t seem to be increased by QE (I agree that the very recent inflation can be adequately attributed to other causes).

My simple understanding of economics is that consumer inflation might result if QE had meant consumers had money to spend on more things than manufacturers could supply. But QE doesn’t seem to me to put money into the hands of consumers, it increases prices of bonds (by raising demand such that people are prepared to sell). That is likely to spread quickly to share prices, since investment funds tend to deal in either more or less interchangeably, and maybe more slowly into other assets.

That prompts two questions.

(1) Has QE caused inflation in asset prices? Assessing whether things like bonds or shared are priced more highly than their underlying value is quite a technical issue, given the volatility of those markets, but I have seen claims from before the recent war-triggered drop in stock market indices that they had become inflated. And there is the question of whether house price inflation, which is widely reported, is related to that.

(2) Will QE eventually filter into consumer inflation, and how long will it take? I assume shares, bonds and other assets are mostly eventually realised as spendable money; for example I spent 40 years contributing to a pension fund that invested in those sorts of assets and is now cashing in some of them and paying me a pension which I spend as a consumer. And my late mother’s savings (some of which were based on share and bond investments, and the largest part of which was a house with paid-off mortgage) has facilitated spending by her heirs. In those cases it took decades for increases in asset prices to hit actual consumption, but I don’t know whether that is typical and Mervyn King is looking too soon.

1) Yes, undoubtedly – and as a direct result – that was a policy aim

2) There is no evidence of this happening – and I do not agree there is a link although others I note claim there is

Thanks. In which case:

(1) Is asset inflation a problem and does it need controlling? It seems to me that raising central bank interest rates might actually be counter-productive here, and targetted taxation might be better if control is needed. But I am unsure, because investors in such assets are often international meaning there could be unintended consequences in terms of things like foreign exchange rates.

(2) If that is true then what is QE (of this conventional sort) useful for – and what is it not useful for? I can see its usefulness after the banking crisis when the knock-on effect on business capitalisation created further risks, but is it useful to stimulate a sluggish economy at other times?

1) Tax is the answer on increasing wealth

2) QE is a sham, as I explain in the paper

“Inflation is always and everywhere a monetary phenomenon…”

Friedman said this in 1970 and it has been taken as an article of faith by neo-liberals ever since. Mr. King is no different… and he is also wrong.

The problem is that no amount of evidence will shake that faith and we will continue to suffer as a result.

So, it has to be pointed out that he is wrong , time and again

Ram damming as Colin Hines calls it

Some who are old enough will get the reference https://www.youtube.com/watch?v=S94Bh3Qez9o

The zombie dinosaurs of the Right clearly hate acknowledging the supply-related causes of cost-push inflation no matter how obvious those causes are.

They want to attribute the problem to demand side causes: wages, stimulus, QE etc. despite a complete lack of evidence because that’s what they want to do. Like good little parrots its what they are used to and what they are trained to do.

They did it in the early ’70’s when they got away with blaming wages and unions for the OPEC oil crisis stagflation and they’ve done it ever since.

There’s no big wages this time around and the they are not denying the supply chain issues they just overlook them and point to demand related issues instead, when demand is just about low enough to sunk us into recession. FFS.

Whatever credibility Mervyn king might’ve had, he’s just lost it

Richard,

Am I right in thinking that all discussion of responses to the current price rises is confused by a lax use of the term inflation. I understood that inflation in its strict economic sense is a general fall in the value of money due to its oversupply relative to the capacity of the economy in which case the Friedman statement is a tautology. However surely most of what we are currently experiencing are relative price changes caused by specific events which have disrupted particular markets and which, therefore, is not strictly inflation and will not be solved by monetary action. I came across this article which it seems to me to address the issue well.

Sorry, forgot link!

https://www.clevelandfed.org/~/media/content/newsroom%20and%20events/publications/economic%20commentary/2002/ec%2020020515%20is%20it%20more%20expensive%20or%20does%20it%20just%20cost%20more%20money%20pdf.pdf?la=en

I do not agree that definition of inflation

Inflation represents a general increase in prices and consequent fall in the purchasing value of money. It is measured as a percentage rate and not as an absolute measure. This is important: just because after a period of above-average inflation the inflation rate then falls this does not mean that prices then return to their original level or that a currency regains its original value. For that to happen a period of deflation is required. Deflation represents a general fall in prices and a consequent increase in the purchasing value of money.

Thank you for commenting. You have not done so before, or have only done so a few times, and the tone of your comment suggests that you might be trolling. As such please now email me providing evidence that you might be the person you claim to be with evidence of a persistent pattern of posting on other social media such as Facebook or Twitter using the name that you have now used to comment here so that I might decide whether I wish to let you comment on this site. My decision on whether to then accept comments from you will be final. The more information you provide the easier it will be for me to make a positive decision. Any disclosure you make will be voluntary. You do not need to respond if you do not wish to post again.