I spoke this week at a conference organised by PricewaterhouseCoopers on the legitimacy of tax systems. The conference was held under the Chatham House rule and as such I am not reporting what was said. I am, instead focusing on one particular issue that I raised.

My presentation focused upon the need to understand the tax system as a whole. As I explained tax is one of three or four funding streams for government spending, which I refer to as G in what follows. The funding streams are:

- Tax (T)

- The change in government deposit taking (often, and incorrectly, called borrowing) in a period (∆B)

- The change in base money in a period (∆M)

- Aid (A)

As a result:

- G = T + ∆B + ∆M + A

This is an accounting identity: as a matter of fact, it must be right.

What this does, of course, mean is that it is impossible to say that tax funds government spending. However, it does not mean that there is no relationship between tax and government spending because there very clearly is. What the identity describes is a system in which tax, money creation, government deposit-taking and spending all co-exist in intimate relationship. Those relationships are macroeconomic, and what is clear is that if the system is properly viewed as a whole both fiscal and monetary policy are involved.

That is because, as I also explained, once tax is liberated from the idea that it is a funding source there are six reasons to tax:

1) To ratify the value of the currency: this means that by demanding payment of tax in the currency it has to be used for transactions in a jurisdiction;

2) To reclaim the money the government has spent into the economy in fulfilment of its democratic mandate;

3) To redistribute income and wealth;

4) To reprice goods and services;

5) To raise democratic representation - people who pay tax vote;

6) To reorganise the economy i.e. fiscal policy.

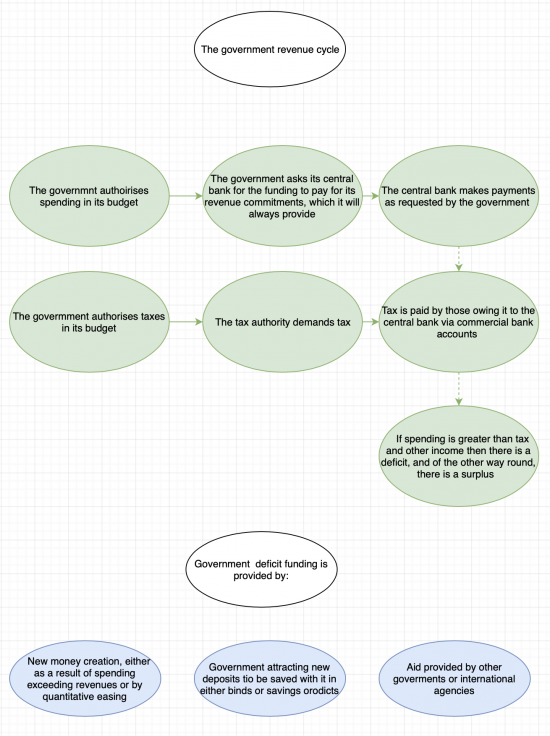

When asked to suggest how the legitimacy of tax systems could be improved my suggestion was straightforward. I proposed that PWC should, if it was committed to this issue, publish an explanation of how tax systems really work, and then provide detail of how tax fitted into the government financing cycle of every country in which PWC works – which is around 160 jurisdictions. This is data that they do, of course, have to know to work and offer advice in such places. The data would explain these processes:

The items highlighted in green are, in effect, an expenditure and income account. Breakdowns by type of income and expenditure would, of course, be required. Those in blue explain the funding used for this process and so form part of the balance sheet (capital, for money creation; liabilities for deposit-taking and equity via the income statement for aid).

Importantly, the accounting and decision-making processes with regard to tax revenues should be explained. This is a multi-stage process:

- The tax bases available to a government must be explained. These include:

- Income such as wages, profits, savings income, rents and dividends;

- Sales;

- Capital gains;

- Wealth;

- Land;

- Transactions;

- Minerals;

- Carbon;

- And so on.

- A tax ‘base rate' for each base should be suggested. This is the standard rate at which it would be expected that a tax on this base might be applied. We are quite used to this idea as they are already in operation for most taxes in most countries;

- If it is decided not to tax a base then this needs to be explained, with reasons given;

- After that, detail of the cost of allowances and reliefs given, plus the benefits from higher rates of tax needs to be provided, with enough explanation by tax so that the major decisions taken in determining the reliefs and higher rate charges can be understood. This then suggests the theoretical tax take to be collected using the tax system actually in use;

- From this should be deducted the cost of tax avoidance, hopefully analysed by tax and cause;

- Then the cost of tax evasion should be deducted, analysed by tax

- After that t the cost of bad debt should be deducted, split by tax, which is the tax the government knows is owing but fails to collect despite that, with reasons for failure given,

- And that then explains tax actually paid, split by tax.

This provides the basis for some tax decision making, presuming you understand the rest of the funding cycle. I suggest PWC should or could make best estimates of these figures, or indicate why it is not possible to do so, as a result indicating areas of required reform that would be of use in itself.

Combining this data with that in the chart of the government revenue cycle what we would then know is:

- The amount of money created;

- The amount withdrawn from the economy again through tax;

- The increase in base money;

- The increase in funds deposited with a government;

- Any aid received;

- Borrowing in foreign currencies;

- What the government spent, stated in sufficient detail to understand that spending, including capital spending;

- What the government balance sheet looks like.

This is, of course, no more than requiring a government prepare a set of accounts. If multinationals can do this it is absurd that governments cannot. And if a government does not prepare such accounts then best estimates are needed to inform tax debate, not least to embarrass them into action by requiring that they do these things.

And then if you want really informed decision making you would add in tax spillover analyses. These, in the form designed by Andrew Baker and me, examine how a tax system undermines itself, for example by offering differential tax rates that encourage avoidance, or by underfunding of the tax authority that encourages evasion. It also explores how the tax system is undermined by other jurisdictions, and how in turn it might undermine them. The result is not just a risk rating, but also a clear plan of action for things that need to be addressed.

My suggestion to PWC is that they could massively increase understanding of tax by explaining all this. And they could as a result provide a massive public service by promoting the understanding of tax in its full context and by providing data, wherever possible, by jurisdiction so that better tax decision making could take place right across society.

Of course, PWC might say this is too hard, but I really would not believe them: if they do not have this ability then no one has, and I believe it is possible to make these estimates. I would understand though if they wanted to cooperate with others. I, for one, would be more than willing to partake. Critically, the aim would be to make this detailed, but still accessible.

I am hoping that this is an idea that they might just think is worth pursuing. I am sending this post to PWC.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Fascinating Richard.

Let us hope PWC contribute something positive. I think however that the the ‘light’ in the ‘Age of Enlightenment’ is now very dim as the shadow of orthodoxy looms over it.

And then, what did I hear on the radio today – our economy which is wanting to create high quality, highly paid jobs wanting to sack more civil servants to fund this, that and the other.

So, it’s OK to sack the civil servants in a COLC because your tax pays for them and they are an expense to you. Fascism again!!

Don’t hurt me – hurt someone else.

Why not avoid hurting anybody?

You couldn’t make it up could you?

2+2 = 5

And too many of us will not have been paying attention.

Cuts in public spending. It is always about efficiency (ask Elon Musk about the superb “efficiency” of his modern slaves in China working 996 or longer – locked in and working six 12 hour days from 9am to 9pm per week – because they have no effective legal rights. So that is where the tens of billions come from.)

And never about capacity or resilience or equity.

I doubt PwC has any interest in doing any of the work that Richard suggests. Nor most government. It suits them to have ignorance on these sorts of issues.

Sorry, feeling cynical today.

To tie in Lord Judge’s comments one could say that the legislature authorises the Governments Spending Plan.

Given the scandalous levels of waste brought about by the corruption and procurement incompetencies I would argue that there is a need to tie parliament in to the process you have set out as it unwinds. Certainly if I was a BoE director being asked to pay £37 billion into a black hole I would want some parliamentary assurance that it continues to have confidence that the spending plan it originally approved is being followed, especially so with the current executive. Why would expenditure commitments be treated any differently to its international law commitments?

Again it is important to stress that much of the exercise you define happens in retrospect, whilst one accepts that it is the Department that authorises the final payment it does so long after the spending plans have been constitutionally approved. The role of the NAO in this process should be much more pronounced.

Here’s a graphic showing the change in government deposit taking (often, and incorrectly, called borrowing) (∆B) as at 2021 for many countries.

https://howmuch.net/articles/state-of-the-worlds-government-debt-2021

Need to replace the word ‘debt’ with govt deposit taking

Japan still has the highest debt to GDP ratio in the world at 257%, which is significantly higher than other developed countries.

The COVID-19 pandemic significantly increased government debt around the world, with 3 countries now over 200% of debt to GDP and 32 over 100%.

At the opposite end of the spectrum, a handful of petro countries carry very little debt, including Kuwait (14%), Russia (18%) and Saudi Arabia (31%).

The coronavirus pandemic is far from over, and many countries are continuing to spend a lot of money to support their economies, suggesting government debt will only continue to get worse in the future.

Thanks