I have just posted this thread on Twitter:

This is a thread on the impact of price changes we were expecting as a result of government policy, Brexit and Covid before the war with Ukraine, plus those we're now getting because of it. Stick with it. Everyone's going to be hit hard by what the government is letting happen….

In case this thread is too long for you this is a summary. We're in a crisis. Energy and food costs are going to increase the cost of living of low-income families by 14% a year, or £300 a month. More than 70% of households will go into debt unless they cut their spending, a lot.

Given that most households will not be able to borrow to cover costs there is a massive economic recession coming our way instead as families cut out discretionary spending. The leisure sector will be hammered. Unemployment will rise. Banks will suffer massive bad debts.

Sunak should know this. If I can predict it based on data in this thread so can the Treasury. He needs to take action. He can afford to - tax revenues are way above budget - and by using QE if need be. Doing so he could peg energy costs and beat inflation.

Will he? That's the question I am asking as I lay out the evidence and what he could do in this thread. If he doesn't, you need to worry, because within a year we could be in meltdown. The evidence is in what follows. It may be the most important thread I have written.

-----

I recently highlighted who might gain from the potential increase in average UK domestic energy tariffs from approximately £1,200 a year, to about £3,000 a year, as current fixed cost energy supply contracts now imply to be likely.

As I noted, most of the benefit of this increase in profits will go to energy companies located somewhere in the supply chain between the point where oil and gas comes out of the ground and where that energy does through a wall into your house.

The increase in profit to your actual energy supplier will be fairly small. In fact, the government benefits a lot more by collecting more VAT and by dumping the cost of failed energy companies onto you through increased daily standing charges.

That does, however, mean that most of this price increase benefits other companies in the supply chain. My estimate is that their share of your annual payment might increase from £43 a year to more than £1,700 a year, a near enough 40-fold increase.

As I noted when I first wrote about this, the only appropriate description for this is exploitation. You are being ripped off simply because governments are collectively letting the oil and gas companies and oil traders get away with this.

The object of this blog post is to consider what the implications for some sample UK households of these energy price increases, and some of the other changes in both income and prices, might be. After all, it's not just energy that is changing in price.

It is my belief that until we do understand what these impacts on real people might be that it is unlikely that we can properly appraise the appropriate responses to be demanded from energy companies, the government, and others to tackle the poverty crisis that we face now.

For the purposes of this exercise, I am using data supplied by the Office for National Statistics on household income and expenditure. This is available here.

As usual for the ONS, this data is a little out of date. It relates to March 2020. It's also a bit ‘clunky'. By that a mean it's presented in a fairly cumbersome style and to use it I have had to do some summarising and rounding.

That rounding means that some of the data in the tables I present in this thread does not quite add up. Don't yell at me! I used what I had to work on and have done my best to turn it into something that makes sense. What I ended up with is plenty good enough to be useful.

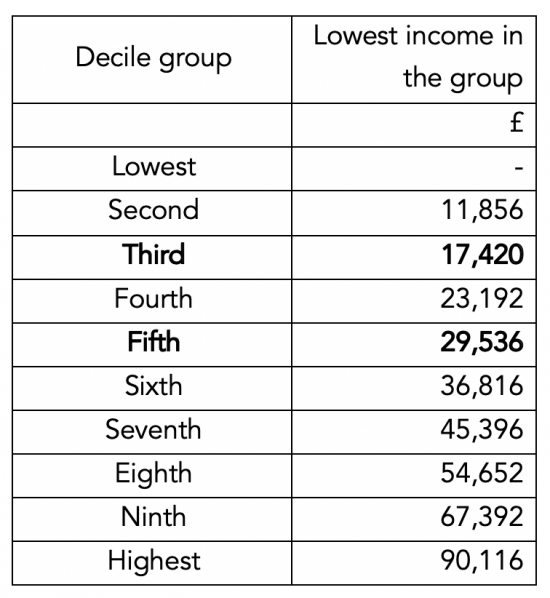

Importantly, this data is split into what are called decile groups. For those not familiar with deciles, they split data on a population into ten groups of equal size, in this case including an equal number of households in each group, with each group having a broadly similar income.

Using the ONS data, the deciles of equal size split by income group in March 2020 were split as follows into income bands, with income being stated before tax:

My work concentrates on those who are in the third and fifth and top bands. Those in the third band have income of about £19,100 a year on average after tax. On average people in this group earn just a bit more than the minimum wage, working full time.

I also chose to look at the fifth band, where average income after tax is about £29,500, or very close to UK median earnings at present. Before tax, and assuming a single income earner in the family, earnings would be 33,400 per annum.

It is important to note that I am assuming there is only one income earner in the household when making these observations. There may, of course, be two.

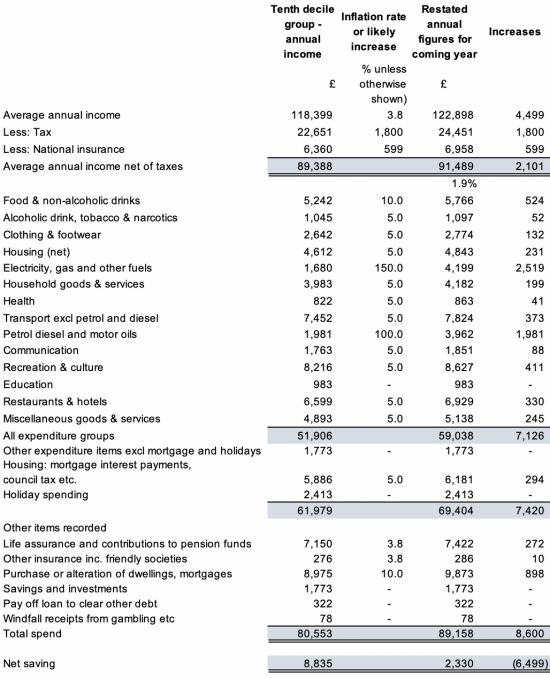

To provide contrast to these two groups I also looked at the tenth decile – the top income earners. They have average pre-tax income of £118,400 a year. After tax they enjoy £89,400 at present according to the ONS. Obviously, some at the very top enjoy very much more.

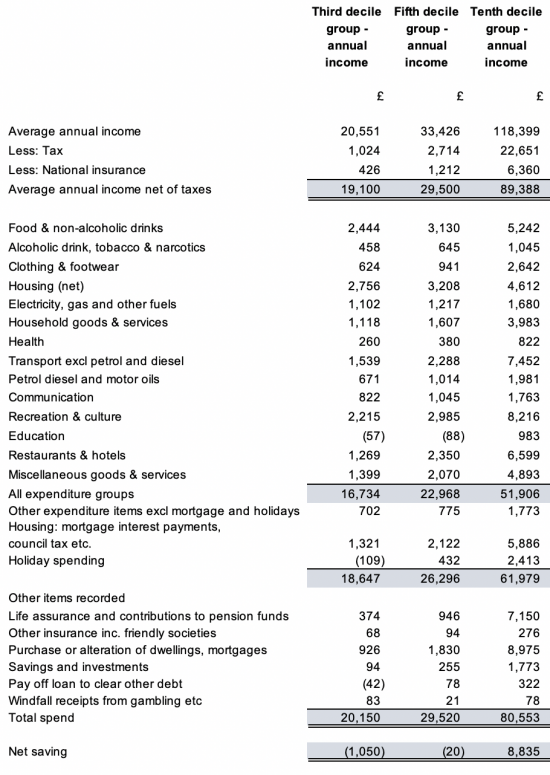

Having summarised the income, tax and national insurance paid according to ONS data for these groups I then also summarised their average spending according to the ONS. I had to do this under broad headings. The actual data is many pages long and more detailed than shown here.

If I just use the data for these three groups as the ONS presents it then it is as follows:

There are three things to note straightaway. The first is that the ONS data implies that the third decile – the minimum wage earners (near enough) don't already make ends meet. It's not clear how the ONS explain that, especially as their savings are already small.

The fifth decile - the average earners – broke even in March 2020, near enough. And the top decile of income earners were doing just fine, which is no real surprise to anyone because that's the way our society is stacked.

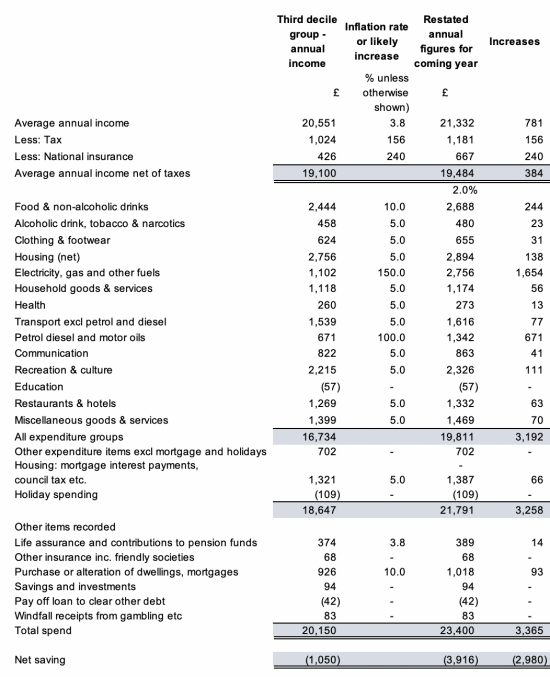

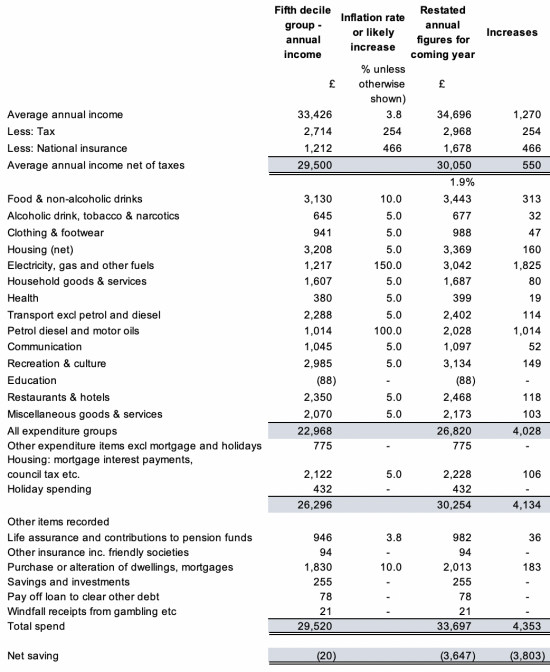

Having established this data I then had to make some assumptions on relevant inflation rates to suggest what might happen. On income, I have assumed 3.8% pay rises – because that is the latest ONS estimate of pay rises, excluding bonuses.

Tax increases are based on the estimated pay rise at the appropriate tax rate assuming no increase in personal allowances, which is what is happening – so taxes are increasing in reality, as I show.

For national insurance I have allowed for the NI due on the increased income and the increase in rate of 1.25% overall income. Because NI is capped for high earners the calculation is different for the top decile than it is for the two lower deciles.

Thereafter I have assumed 5% inflation on most spending – which is consistent with most current forecasts (although if I am honest, I think these may be a bit low now), but there are obvious exceptions.

On food I have allowed 10% for the lower deciles and 5% for the top decile – because they have more flexibility and the ability to substitute products. The 10% is based on Jack Monroe's work and may be an underestimate. It may be worse as wheat shortages hit.

Domestic energy I have estimated at 150% as that seems to reproduce the prices we expect. Petrol I have estimated at 100% - or a doubling in the cost, which latest expert forecasts suggest likely.

I have assumed no increases in some discretionary costs. Most housing costs are hard to estimate because they vary so much. I have allowed for interest rate rises (very approximately) on mortgage costs. There is a lot of give and take here depending on people's circumstances.

Putting all this together the impact on people in the third decile of income earners (those on about minimum wage, working full time) is:

The impact on those on approximately median income is:

And the impact on high-income earners is:

What this means is that those on about minimum wage have a cost-of-living increase of about 14%. Those on median pay have an increase of less, but still of an eye-watering 11% a year. And those on the highest incomes see a much smaller increase of about 5.3% in the way I estimate it.

Remember all these numbers are approximate, and they are forecasts, but I offer them in good faith. If the government does nothing to help people in Rishi Sunak's statement next week, then I suspect that outcomes like this (or maybe worse) might happen.

Let's put hard numbers on these forecasts. Those in my lowest income group will spend £65 a week, or £3,365 a year more. Given they had no money to spare before this began they are now in a desperate situation. After pay rises they're still down about £3,000 a year

I don't say that lightly: I am incredibly worried about those on lower incomes right now. Brexit, Covid and government policy – all of which were pushing up inflation well before war began – are pushing millions of households in this country into near impossible poverty.

I stress – these families are facing near impossible situations. Let's not beat about the bush. Without much more help I can't see how their household budgets can come close to adapting to the additional costs that they face. There is no slack to cut.

Life is not going to be a lot better for those on average or median pay. They will see their weekly costs rise by £84, which is an additional annual spend of £4,350. They were breaking even before this. Now they aren't. They're going to be down £3,800 a year after pay rises.

Just like those earning £10,000 or more less than them, many in this group will not be able to make anything like the demanded level of lifestyle adjustments that this level of additional cost will require.

What is also apparent is that if they do try to make that adjustment – and most will be forced to – then the savings will come from their recreation budgets – for which there is going to be little money left in both groups if anything like the required savings are to be found.

The top earners actually suffer bigger increases in actual costs as a result of the inflation that we are going to see. On average they face additional spending of £8,600 a year. This is despite having earnings increases of £4,500 a year. Two cars and bigger houses have a cost.

The best off will differ from the other groups in one way: they will still be able to cover their outgoings including all their planned savings, pensions and mortgage payments. Their options on how to address the issues arising are much wider than those available to others.

There are some interesting comparisons to make before considering the consequences of all this. For example, the same 3.8% income increase is assumed for everyone, but for the lowest earners that results in a 2.0% net pay increase; the median earners get 1.9% and the top 1.9%.

Those lowest off pay slightly less in national insurance increase overall than the median earners in this group, and the top group have higher income tax increases to compensate for smaller NI increases. But there is nothing remotely progressive about this.

Importantly, overall tax rate on inflation driven pay rises next year might be as high as 50% overall, given the impact of national insurance changes across the board. There is in that case no pay solution that is going to solve this issue, although cutting the NI increase would help.

What is more, net pay rises are only 11% of cost increases for those on approximately minimum wage, 12.6% for those on median pay and 24.4% for those in the top decile. No one is getting a pay rise that compensates for their extra cost of living, but the rich are doing best.

In that case there are three questions to ask. First, does this matter? Yes, because as it stands it's likely that well over half of all UK households are going to face financial pressure they simply cannot manage over the next year as things stand. That is a nightmare for them.

It is also a nightmare for the government. These people will get very angry when faced with an insurmountable burden requiring that they cut back on everything but the most basic things in life, and even then will be challenged to make ends meet.

Politically we have not seen anything like this in the lifetime of anyone now living in the UK. How people react is anyone's guess. But I know that a mother who cannot feed her children is one of the angriest people on earth and there are going to be millions of them sometime soon.

To be blunt, I am not sure how this situation can exist without the risk of serious civil unrest, which it would be very easy for people to have sympathy with.

Second, my analysis only concerns the initial reaction to price rises, as people try to pay. As struggling households cut all their leisure spending back, or end it, the secondary reaction is going to kick in. That means large scale business closures, and then mass unemployment.

You cannot force most people in the country to spend all their income on basic costs of living and maintain a thriving economy. That's impossible. And £150 here or there on a saved council tax bill, or a bit saved on deferred payment arrangements is not going to solve that.

The leisure, tourism and travel sectors are clearly going to be hardest hit by this. The ONS data shows that everyone who can likes going out in the UK. But that's not going to happen with bills rising this much. There is going to be economic meltdown in these sectors.

Third, once these secondary effects kick in so does the financial crisis as debts, rents and mortgages, as well as utility bills, go unpaid. People without the money to pay their debts cannot settle them. The consequence is that a full-blown debt and banking crisis is on the cards.

How big a crisis? Something that makes 2008 look like a picnic, I suggest. That's the magnitude of the crisis that we are looking at if people simply cannot pay their bills, as seems likely based on this quite fair data analysis of the problems most households are facing.

So, what can government do? I stress I ask that question in that way deliberately. That's because I can't see anyone else doing anything about this crisis, or having the power to do so. It is either down to the government to tackle this or we are in very deep trouble indeed.

First, the government has to acknowledge this problem, and its scale. Rishi Sunak has the chance to do that in his spring statement next week. I cannot see that happening but have to hope I am wrong.

My problem is that I recall all too well Sunak's first response (and his second, and more) to Covid and they were all too little, too late, or riddled with holes that let fraudsters have a party at our expense. I have to hope that for once he might get this one right but doubt he will.

Second, the problem has to be acknowledged to be a universal one. It would be relatively easy to announce some measures for those on Universal Credit for example, and they'd be welcome. But, my data shows that the problem we are looking at extends way beyond those on UC.

Third, in that case tinkering of the sort announced earlier this year to tackle the increases in energy cost schedule for 1 April onwards are not going to be enough: something much more radical is required. Council tax rebates and enforced loan schemes won't work this time.

Fourth, the problem is not only with domestic energy bills. I've shown that the increases in these are down to energy company profiteering that exploits us all in this thread.

The problem now extends to road fuel and food prices as well. Both are also likely to go up, and again because of profiteering in most cases because it is not cost increases that are driving up these prices, but shortages that are being exploited by speculators that are doing so.

Fifth, we have in that case an inflation driven crisis in our economy caused by speculators and not real cost increases from things that might compensate for the price increases, like wage rises.

Understanding this is important because it tells us what will not work to tackle this crisis. Most especially, increasing the official interest rate will do nothing to stop these speculators. All those increases will do is pour even more hardship on hard-pressed households.

In that case Rishi Sunak should be sending out a very clear signal to the Bank of England to not only stop the increases in interest rates they're imposing on us right now, but to reverse them too. People need all the help they can get right now.

There is another message that Rishi Sunak also needs to be sending to the Bank of England, which is that he might need a lot more quantitative easing (QE) quite soon. The government's response to Covid was entirely paid for with money created using QE.

No debt, no tax and no borrowing paid for the £400 billion cost of Covid. Money creation by the Bank of England did. And what we know is that money creation of this sort did not create inflation in the previous 11 years, and nor is it, or will it, now.

In that case, the crisis our economy now faces can be addressed using QE, if necessary. However, QE does create problems of growing inequality. To tackle them taxes on the best-off need to go up, and we will also need a windfall profits tax on energy companies.

What else can Sunak do? The answer is that he must intervene in markets to prevent the impact of the exploitation that we are seeing driving people into the financial problems that I am suggesting are likely to happen in this thread.

Tinkering will not do. Instead, he has to hit the problem head-on. He has to cut road fuel prices to prevent them pushing all other prices up. That means cutting VAT and other duties to keep these prices at 2021 levels. That's the price we need to pay to beat inflation.

And then he has to be really radical. We need subsidised household energy pricing, imposed compulsorily on all energy suppliers. That means setting the tariff for the energy consumed by an average household at 2021 levels. The government must subsidise that cut in costs.

If this was done only larger houses should be required to pay the market price for whatever energy they consume above that average use. This would encourage energy-saving measures by them and suit the green agenda. That makes this fair, affordable and green.

These measures do, however, only address the immediate problem. Then we have to solve the long term one. That requires three things. Green energy; new jobs and better pay. This is where the Green New Deal comes in. This has always been designed to deliver all three, everywhere.

The jobs would be installing insulation to cut energy costs as more than 30% of UK houses are uninsulated at present. We also need more double glazing, and then heat pumps rather than gas boilers. On top of that, solar, wind, tidal and other new energy is required.

Then there is new green housing that is needed and the transformation of transport and office spaces. Just about every business process needs reengineering too. The number of jobs that becoming net-zero could create is enormous, as we cut our emissions.

All of this is affordable. QE and tax could pay a part. But so too could redirecting the financial wealth of the UK to this task. There is £8.4 billion of financial wealth in the UK, most in pensions funds and ISAs. The rules on these need to change to deliver green funding.

If ISAs had to be saved in government-backed green bonds paying competitive interest and one-quarter of all new pension contributions had to be used to fund the green transition more than £100 billion a year could be provided to create the transformation of our society.

Sunak could change ISA and pension rules to require that. Then we could be weaned off not just Russian gas and oil, but all the gas and oil that threatens life here on earth. This is possible. And we could have more, better-paid jobs using the savings.

In other words, we do not need to go into recession now. With imagination we could be setting ourselves up to tackle the immediate inflation issue and the long-term issue that created it. Will he do that? I don't know. I can only hope so, for all our sakes.

What I do know is that if Sunak does little or nothing, we face the biggest economic meltdown of my lifetime with millions of households who have never faced poverty joining those who already know all about it. If that is not enough to make him act now, nothing is.

My thanks to economist Howard Reed for reviewing the data in the thread: any errors are mine.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Fascinating. Thank you for the number crunching. Forward contractual order flow that I am seeing from September is 8 per cent down year on year (UK), 2 per cent Europe. Shows actions in socially aware countries are having effects. Sunak with over 200 million in the bank is not socially aware.

Supporting food banks is high on my agenda, but individual action is but a piece of fluff on a gaping and bleeding wound.

An excellent article Richard, Thanks and do keep up the good work.

The only thing I can add is that while I believe the Green New Deal to be the right solution it is blindingly obvious that neither this government, nor our current working practices are capable of efficiently delivering such a thing.

By way of an example, during the New Labour years my elderly mother living on her own benefitted from a series of New Labour Green schemes.

Unfortunately because they were delivered via a structure of multi-level sub-contracting, the contractors that eventually did the work, particularly in the case of the people who installed the new boiler and loft insulation, would meet almost any definition of Rogue Traders. A terrible service and quality of work that could not possibly cost anything like the money allocated by the Government. Followed by a wall of unaccountability.

Once upon a time the state employed people…..

Quite right.

Direct employment of qualified people, decent training and a professional inspectorate to maintain quality, all within an accountable management structure.

One can only hope that Sunak is doing his usual trick – being all bullish and ‘tough’ sounding and then relenting as he stares down the barrel of possible social rejection of the hardship that is to come. I hope so.

It feels to me that Governments may have done some sort of tacit deal with oil and gas to have their last profit ‘hurrah’ before perhaps insisting on change? Who knows?

But then again…………………..the situation we are in was always going to happen. How can I come to such a conclusion?

I’ve just finished the long road that is the book ‘The Road to Mont Pelerin’ (2009). Throughout the book I’ve been fascinated and frustrated by the elusive nature of Neo-liberalism – it’s contradictions and the feeling that is something never actually completed as a theory of economics and political economy even. The ‘road’ peters out quite often into nothing. But as I’ve literally just completed my read, I’ve been surprised at just how prescient the book is.

But if looking at Neo-liberalism as a theory of economy returns thin gruel, it is when its protagonists start expanding and propounding their ideas as some sort of moral code for society (p.440) where I think the mal-intent behind it (remember that Neo-liberalism (NL)/MPS has always relied on financial support from vested interests) is reified.

Frankly, where we are now was always going to be the end game – the end result of Reagan and Thatcher’s bold leap.

Never mind all the promises of lower prices, more choice through competition and freedom etc., that Ron and Mags made. That was never ever going to happen. It was the notorious ‘double speak’ of NL (p. 444-445).

No – from the sub-heading ‘A Neo-liberal Primer’ until the end of the book (pp.433-446), Mirowski does NL the favour of taking it seriously as a way of not only organising markets but as a way of organising society. And it is here – under the more rigorous glare of social theory perhaps – that NL gives itself away in its own words. NL is found wanting. Big time.

It transpires – almost self confessedly using the words of Hayek & Friedmann themselves – that NL is not even liberal or democratic; it is about freedom but a selective form of freedom for the anointed righteous – which also implies slavery for those who are not anointed, not part of the ‘special club’. What NL requires of unanointed society is to be compliant.

As someone else has said (and I paraphrase) all that is required of you to express YOUR freedom as a neo-liberal slave is to go shopping and not quibble about the prices – whether it be widgets or oil and gas or the way in which it seeks to commodify all natural human interactions (forget co-operation folks). And BTW – your rights are secondary to the rights of your service or product supplier.

Basically where we are now is hardwired into the NL credo. It’s always been there. From the way it has bullied national and global institutions (including Governments) until they relent and use its ideas, to its view that democracy and liberalism are opposites – not bedfellows; to the way in which God-like Hayek made judicious room for his ideas but no countervailing ones. NLs actually like strong and pervasive states as long as they are strong and pervasive about the things that NLs hold dear:- protecting the rights of those in powerful positions in markets and society.

Or to put it short, protecting their sugar daddies – those who have paid for them to enable to exist.

At the very end of the book both Hayek and Friedman are taken to task over the ‘totalitarian’ aspects of a large pervasive state that acts as an advocate for markets only. This is done by drawing comparisons with of all people the Nazi theorist Karl Schmitt (I cannot believe that Schmitt lived to 1985; in my view he should have been executed with others after Nuremburg). Quoted at length, Hayek believes only in ‘limited democracy’; Friedmann does not believe in it at all.

Schmitt’s democracy repressing, chilling observation ‘Sovereign is he who decides the state of emergency’ can certainly apply to Hitler, Stalin, Trump, Bush Jnr, Bliar, Putin and yes…..Boris Johnson. Think BREXIT, the proroguing of Parliament.

In our current situation then, we have arrived at the terminus of our Neo-liberal age. It’s a free for all for suppliers and rentiers. The ‘democracy’ we are in is in the words of Hayek there to ‘sanitise’ that which needs to be done to keep the profits rolling in for the anointed. And of course the profits that will be used to keep Neo-liberalism supported in politics and our universities. It’s a wonderfully self-perpetuating system. Hat’s off to them – rigged beautifully.

But in short, for politicians and voters alike – we’ve been had. Big time.

So, let’s see what happens next. When will we realise?

This is key:

Quoted at length, Hayek believes only in ‘limited democracy’; Friedmann does not believe in it at all.

And with that goes simple not caring

Yes – neatly put: in other words, ‘Atlas Shrugged’.

Excellent analysis. Real numbers bring home the severity of the situation.

My fear is that the Tory response will be “Poor people spending so much on leisure, culture, hotels and restaurants?? Shocking! That’s where they should cut spending before the State offers help!” (Yes, really, there are quite a few who think like that).

I also fear that “second round effects” (ie. unemployment leading to lower incomes, still) will be tough – and it is already showing up in the restaurant trade.

The only area where I might quibble is that the 5% inflation rate that you use in non food/energy is a bit high. In the face of spending in other areas falling off a cliff it is hard to see higher prices sustained in many of these sectors. But let’s be clear this is nit picking.

This was the response from Nick Ferrari on LBC when he interviewed me in Friday, albeit to his previous interviewee

I said very directly that he was wrong, choosing to re-raise the issue

Richard,

Most of what you are saying defies basic economics, logic and reason. It does not stand up to reality. I am sorry to point this out to you but most of what you have claimed is either false or would actively make the problem (inflation) worse.

“As I noted when I first wrote about this, the only appropriate description for this is exploitation. You are being ripped off simply because governments are collectively letting the oil and gas companies and oil traders get away with this.”

This is absurd. Oil and gas are traded at market prices globally. You seem to have forgotten basic supply and demand economics. There is a lot more demand than supply, driving prices higher.

You seem to be under he false impression that governments can simply dictate the price of commodities on the open market. And were governments to impose a price lower than current market prices, suppliers would simply supply other willing to pay more – the very foundation of a market in prices.

“Fourth, the problem is not only with domestic energy bills. I’ve shown that the increases in these are down to energy company profiteering that exploits us all in this thread.”

I don’t think you can call selling on the open market “profiteering” as I have mentioned above. They are simply selling at the current market price, not increasing their prices arbitrarily to benefit unfairly.

Moreover, you have not considered that oil and gas companies for a long time were not making profits at all when prices were far lower. Does this “profiteering” then work in reverse, or only when prices are high? If you are limiting the ability for companies to make a profit (which in essence you are arguing for, especially when you mention windfall taxes) then you will simply have fewer companies in the industry, less oil and gas, less supply and higher prices again. QED.

Again you seem to have forgotten (or simply not known) your basic economics.

“but shortages that are being exploited by speculators that are doing so.”

Do you have evidence that speculators are driving prices higher, or is it simply a lazy assumption blaming evil speculators rather than the truth – that it is simply a lack of supply and increased demand driving up prices. Speculation and hedge funds are a minimal part of commodity markets – they are simply too big and driven by fundamentals for speculators to have significant effect on them.

“Fifth, we have in that case an inflation driven crisis in our economy caused by speculators and not real cost increases from things that might compensate for the price increases”

Again lazily blaming speculators, with no evidence. The real world of course is saying that prices are increasing because of a lack of supply, an increase in demand and the massive increase in money supply thanks to QE and other government spending.

“Most especially, increasing the official interest rate will do nothing to stop these speculators.”

Increasing interest rates reduces demand, reducing inflation. Economics 101.

“There is another message that Rishi Sunak also needs to be sending to the Bank of England, which is that he might need a lot more quantitative easing (QE) quite soon. ”

I think it is at this point you totally lose all rationality. Your answer to rising inflation is to lower interest rates and to increase the money supply and spending still further. Which would increase demand with no increase in supply. It is the very recipe for even higher inflation.

What do you think would happen if you reduce the cost of borrowing even further when inflation is high is likely to be? Do you think people will borrow less or more? It’s really hard to see how you can even come up with something so ridiculous.

“No debt, no tax and no borrowing paid for the £400 billion cost of Covid. Money creation by the Bank of England did. ”

QE is still debt which eventually needs to be repaid, and even the reserves created by the BoE carry interest. Are you living in the fantasy that governments can print money with no limits, and that money is of fixed value?

“And then he has to be really radical. We need subsidised household energy pricing, imposed compulsorily on all energy suppliers. That means setting the tariff for the energy consumed by an average household at 2021 levels. The government must subsidise that cut in costs.”

By doing this you haven’t solved the problem – if anything just made it worse. Supply and the cost of supply will remain unchanged, but you have passed the costs on to government. This in itself acts as a massively subsidy, which will increase household demand and therefore inflation. If anything, it will directly make the problem worse as people use more energy as the government picks up the tab.

Then you have the secondary issue of how this huge subsidy will be paid for. I am sure at this point you will say something stupid like “more QE” or “MMT” but this is simply not realistic. Printing ever increasing amounts of money to pay for spending is in itself inflationary and is straight out of the banana republic playbook. It is not serious economic policy.

Lastly, once those subsidies are in place, they become politically near impossible to remove.

“If this was done only larger houses should be required to pay the market price for whatever energy they consume above that average use. This would encourage energy-saving measures by them and suit the green agenda. That makes this fair, affordable and green.”

I think statements like this show how little you have thought (or simply how little understanding you have) of what you are suggesting. Anyone under the average of energy use can use more for free, and every single household would essentially have their zero cost rebased to “average use” which would mean every household could simply use far more energy at the same (or lower) net cost. How will this encourage energy saving at all?????

I won’t bother picking holes in the other things you say. What you have written is a wish list of fantasy economics, not based in the reality of basic economics or even logic. I’m not sure how you claim to be an economist when what you have said is so far removed from basic economic reality.

What you have produced is a hastily written polemic to appeal to a certain audience. It is childish and would certainly fail even basic GSCE level inspection. In short, it is nonsense.

Where to begin with this utter nonsense?

First, I have been a professor of political economy. Let’s assume I know basic economics. Let’s also presume that when I say as a political economist that the economics you say you believe in is just a belief system unrelated to any observable truth in the real world. There are, for example, literally no significant markets that do not involve exploitation in the real world. In particular the energy markets are very obviously oligopolistic, at least, but with central coordination (in practice) on prices are more like monopolies. The US challenged the abuse of such markets for more than a century, but not much now. I oppose the abuse inherent in them still . You deny that abuse exists and so exonerate it. Tell me why you want to do that? Do you really know anything about economic theory after week three of the first semester?

Second, you say there is no alternative to this. Maybe you know nothing of the command economies of WW2, designed to prevent corporate abuse of shortages. We face the same scenarios now. I assure you, we can beat that abuse.

Third, you claim QE need be repaid. Tell me why precisely? And given money creation is double entry tell me how the double entry of unwinding QE works and with what consequence for liquidity within the economy? If you can’t – or explain the relationship between QE and money creation in a period of money contraction (which I am suggesting will happen) – then I suggest you quietly back off.

And how you can say I am suggesting anyone gets free energy in my proposal is impossible to work out.

As for your suggestion that I would fail GCSE economics – you are right. I would write a note of protest to the examiner for having wasted students time teaching an utterly irrelevant and wholly dogmatic curriculum. I would certainly never try to answer the futile questions.

So, let me promise you this: unless you show the ability to rise above the mundane don’t waste your time replying.

ED NOTE

I asked this commentator to rise above the mundane

She didn’t. She resorted to ad hominems instead.

So I deleted the drivel she offered for publication.

That’s called editorial freedom.

Dr Jefferis,

The remarkable feature of your tirade is that you did not address the core issue for the Blog; Richard’s analysis of the forecast income shortfalls for the selected deciles from the ONS household data. It is not even clear whether you agree or disagree with the conclusions he reached or assumptions used, yet that is the most important information offered. My view was that in providing that information, and given all the caveats about detailed accuracy, it supplied an invaluable insight. You may disagree with Richarcd’s conclusion, but it would be graceless not to acknowledge it addresses an important issue, and there is a persuasive case that it is making on the scale of the impact on households. The impact of these effects on our society will be crippling, and will have consequences far beyond the measures offered by the conventional wisdom on which you appear to rely. You do not even appear to notice. You provide not a single scrap of evidence that you understand just how much the world has suddenly changed.

“You seem to have forgotten basic supply and demand economics. There is a lot more demand than supply, driving prices higher.” You obviously read to many abstract economic texts. The real world is quite different. There is a fundamental problem with your “market” economics here. The domestic energy market in the UK is not a market. The domestic energy suppliers literally do not supply energy to their customers. The contracts are not what they seem. The “market” is a fake; completely phony. Allow me to give you an illustration, from the real world, coal face. Tens of thousands of customers lost their energy supply in the winter storms in the UK late last year. Customers who contacted their energy supplier for either help or information discovered that a) their energy supplier did not supply their energy; b) their energy supplier offered neither help nor information, because they had no resources or ability to provide either. They had no part in the supply of energy, the restoration of supply, or the communication with users. None. All an energy supplier supplies to the consumer in the UK is a price, and a bill. The contract the user has with the energy supplier is not even like any other commercial contract in law; if you seek compensation for loss of supply it is not the responsibility of the “market” energy supplier to give it, but a (to all intents) hidden ‘network provider’the consumer probably never knew existed. The compensation is fixed by government regulation. Let me spell this out for you in simple terms – this is not a “free market”; it is government sponsored sham market. You should know that.

Everything else you have to say may be debated, but on first cut look at your approach, Dr Jefferis, watch out for these tricky GCSEs; I am not convinced you are ready.

If Jefferis was still around I’d direct her to the other book I’m reading at the moment ‘ How China Escaped Shock Therapy: The Market Reform Debate (2021), by Isabella Weber.

One of the source texts is a Chinese document on state economics called ‘The Guanzi’ – a document that emerged around the ‘Warring States period’ (475-221 BCE – it’s beginnings might also be earlier than this). The Guanzi – apparently a rather large document – was a sort of collection of wisdom about markets during huge change in Chinese society – observations and tactics to deal with change and ‘how to make the country rich’ for those running the State.

p.18 ‘In modern economics prices are one of the purest forms of a quintessentially economic variable, belonging to the exclusive domain of the market. In contrast, the traditional Chinese discussions on prices engage in broad reflections on the relationships between the spontaneous activities of the people, the peoples needs and wants, market forces, political power and regulation by the state’.

Basically even in ancient China, there was awareness of monopoly power and market behaviour in favour of producers and a willingness by the state to intervene to stabilise prices of core commodities like grain for example for the good of society in general.

As we saw in Michael Hudson’s ‘And Forgive them their Debts’ (2018) where ancient civilisations already knew how to deal equitably with debt by not always insisting that debts be paid , it seems that the modern world somehow chooses to forget these wisdoms.

It is not hard to see why. Ignoring past wisdom clearly benefits those who presently hold the debt or the commodities that the State is not encouraged to interfere with. Ignoring the wisdom of the ancients clearly enables greed.

If only Jefferis and many others would just ask more questions about why things are as they are and stop pretending that life as it is today in the 21st century is the only way to be and that we all agree.

It’s not, and we don’t all agree.

These matters have been questioned for centuries and mankind DOES know better, and Richard’s proposals for Sunak are part of a tradition of intervention from more enlightened times.

The simple fact is that we are living in a time of excessive greed. Capitalism is effectively out of control and the balance of power is out of whack. ‘There Is No Alternative’ is a lie, plain and simple.

Thanks

He’s a multi-millionaire and his wife is the daughter of a billionaire. So probably the last person you’d want to be a chancellor.

A good analysis, a fair ‘ball-park’; and you have done us all a public service.

Nobody is listening. The Conservatives are patting themselves on the back; a world crisis has saved their PM. Rejoice. Standing ovation for a political liability; a man without qualities. Declare a triumph, throw garlands in his path; he has survived his own incompetence. What an achievement! That is all that matters. They are now talking about the next election. They think they have won it. Johnson is Churchill (no, don’t laugh): He talks of a new world order, a new line in the sand; from “the Baltic to the Black Sea” (Churchill, 1946: “an iron curtain” has descended, “from Stettin in the Baltic to Trieste in the Adriatic”). He hasn’t tried the Churchillian delivery yet; or the cigar, or the V-sign (he might do that the wrong way round). Yet. No, don’t laugh, it isn’t funny. It really isn’t funny.

If you want a Churchill, you have to sack the unfit incumbent first; In 1940 they didn’t make the ill-judged mistakes the Conservative spivs are chancing now; instead they dumped a duff PM in Chamberlain during the darkest hours of the war because they could recognise a dud even that late, and hd the courage not to hide from the truth. They turned to Churchill. In 2022 the Conservatives are so profoundly, weak and inadequate, they would re-elect Chamberlain. But by 1940 even the Conservstives were not all still clnging in reckless hope to the failures who had brought them to the edge of disaster, as the answer to the problem. Johnson is no answer to any problem.

On the other hand, perhaps laughter is all we now have left. Nobody is listening. It seems the public are listening to Rees-Mogg instead, at least the Conservatives believe so: the court jester’s court jester, telling everyone that Johnson’s unarguable failures and egregious unfitness for the role of PM is all trivial “fluff”; and you can scarcely argue with Mogg on something that is so closely tied to his own persona; someone who is, after all the apotheosis of political fluff himself, must know ‘fluff’ when he sees it. You think?

Nobody is listening.

I fear you may be right

I felt further moved to add this to my review of ‘The Road to Mont Pelerin’ on the well-known web-site:

‘What we have is a set half baked (even less actually) economic ideas (Neo-liberalism) that have only got traction in the world because wealth has seen an opportunity to look after its interests and funded it into existence. And not only that, the philosophy behind it apes the very thing that it was apparently against – fascist authoritarianism.

Neo-liberalism is not some sort of reforming philosophy therefore: it’s a philosophy of power transfer and acquisition only in my view – it is not even anti-authoritarian or anti fascist – it has at its root no qualms about using authoritarian or fascist methods to further its central aim – to enable producer interests and supremacy ahead of other valid interests in society.’

The arguments against your suggestion all come down to “you can’t buck the market”. In particular,

So, let’s look at the market…..

WARNING> MY MATHS IS POOR AND WITH ALL THE DIFFERENT UNITS OF MEASUREMENT THERE COULD BE MAJOR ERRORS>>>>> but I hope not.

Oil production/consumption figures are massively distorted by COVID but the UK is still a significant oil producer in round numbers we have a deficit of about 600,000 barrels a day (on consumption of 1,500,000 bpd). WTI (West Texas Intermediate, the global oil benchmark most actively traded) currently trades at USD105 versus USD80 a barrel in 2018/19.

As a nation, we have no choice but to pay the global price on the shortfall but we DO have choices about our own production. North Sea producers are amply rewarded at USD80 a barrel – anything more could be taxed. On the imports, it would cost about £4bn a year to subsidise things to get us back to 2018/19 prices. (Maybe £5bn owing to the rise in Brent/WTI spread).

In the context of the whole UK budget and the pain caused by energy prices, this seems a small price to pay.

On gas the numbers are bigger and complicated by the large amount of gas used in electricity generation. Interestingly, Henry Hub (US gas benchmark) is still below 2018/19 levels (yes, really) which tells us that the spike we see in Europe is NOT global and that, over time, supply chains could adjust so that whatever subsidy is put in place today could be time limited.

Dutch TTF gas is currently at EUR100 MWh (from EUR 25 in 2018/19). Average domestic use is 12MWh. There are about 25mm households. We produce a bit more than 1/2 our annual gas consumption so the subsidy would cost about £8bn.

These numbers are large… but using the new unit of money measurement it is about “1/3 a Track and Trace programme”.

You hit on the simple point that subsidy is easily the lowest cost here

1 i lived in a house without central heating , a house built in 1874, but we did not die from the cold

2 i was born in 1940 and did not die from starvation. Uk is an obese nation. Cutting down on rations is a boon for the NHS. Come down here and see the fat freak show.

With respect, you entirely miss the reality of modern life