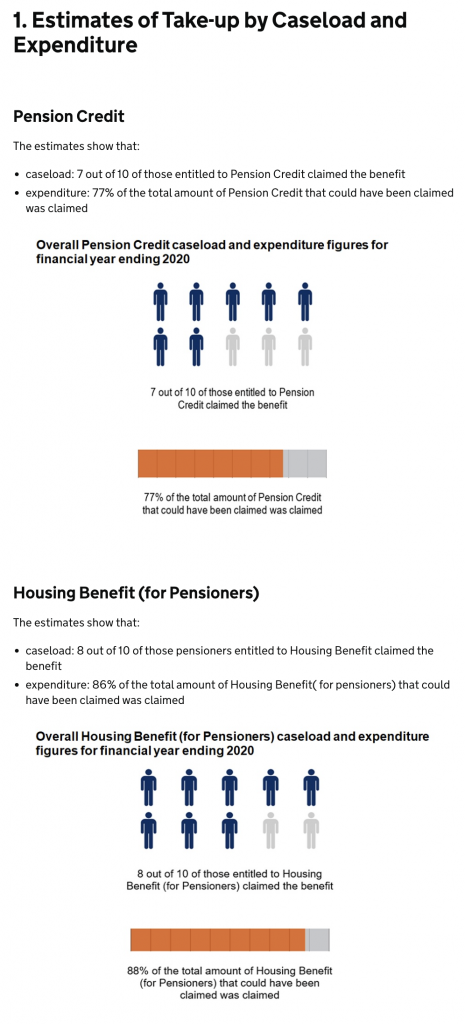

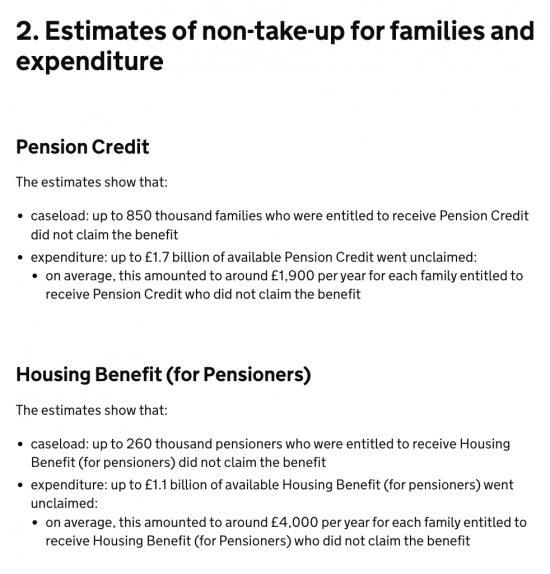

The Department for Work and Pensions has just published this data:

What this suggests is that significant sums that could relieve pensioner poverty are not being paid by the government, even though it has good reason to believe that they are owing. They quantify the sums unpaid as follows:

This is £2.8 billion unpaid that could make a massive difference to people's lives.

My question is a simple one. It is why aren't we seeing national television advertising campaigns to encourage people to claim these benefits they are due? Surely that is the least that the government should be doing if it really cared about those in need in the UK?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

While a TV advertising campaign might make the headlines, what about something via local groups, eg Churches, landlords, Clubs & Societies, Doctors Surgeries etc.

Anywhere where Pensioners might go and of course the people who might know them? Its people like the Housing Officer who might know or have the feeling that somebody is a bit short and can encourage or assist them in the right direction.

There is also DWP & HMRC information that might pinpoint potential recipients

Agreed

The campaign is simple

Have you claimed your benefits? That’s the question it needs to ask

Where do you check eligibility for these benefits?

I genuinely do not know the answer to that. I would be googling it.

Turn 2 Us is the usual place. Most govt agencies point to their benefits calculator for initial assessment.

https://www.turn2us.org.uk/Benefit-guides/Beginner-s-Guide-to-Benefits/Checking-benefit-entitlement

Thank you

Good to know

Turn2Us is good, yes – and also Citizens Advice offices are generally excellent on benefits. They also have the advantage that people who’re not online can walk in and speak to someone – and if they need extra help, CA staffers will help them with forms etc (so many people in the Uk struggle with literacy, when I did a stint for CA we had people who’ bring their post in to us so we could read it to them).

Thanks Cat

Ever since I acted as PoA for my mother, income-related pensioner benefits have been my bete noire; no one should be receiving them.

We should be adding up all the possible benefits and pats on the head (£10 Christmas “Bonus”) and paying everyone that amount as a Citizen Pension. It is not surprising that claims for Pension Credit, which used to be at 40% unclaimed, have dropped. Those receiving the New State Pension cannot claim Pension Credit as it is added to the old basic pension to form the new basic. This was the first step to add in the income-related benefits. It has worked.

In 2022/23 the Old State Pension will be £7376.20; the New state pension will be £9627.80. The Joseph Rowntree Trust calculate a minimum pensioner income to be £11057.28. I estimate the transfer of government calculated income-related benefits would give approximately £12,500. JRT excludes rent, Council Tax and Child Care(?). Mine excludes rent but includes Council Tax.

Recouping additional amounts would come from tax and savings. There would, I believe, be savings from not running the income-related system. There are also health benefits, and therefore cost benefits to the NHS, in not making people claim and benefits to the economy in pensioners having sufficient to live on.

Thanks

It isnt that you cant get Pension Credit if you get New State Pension, the 2022 rate is £182.60 for a single person compared with £185.15 for the New State Pension

This assumes that you get the full rate of NSP – the idea is that the NSP rate will always be above the Pension Credit rate BUT you might not get the full rate of NSP, or you may be entitled to additions in your Pension Credit eg as a Carer (38.85pw) or Disability (69.40pw) which will push anyone who only gets NSP into entitlement to Pension Credit

@john boxall, you are right. I should have said you will not be able to claim it if you receive the full basic New State Pension, although even that is slightly debatable. I was trying not to be too longwinded in my explanation.

There are other additional benefits you can claim, even if you are slightly over and not getting Pension Credit. However, unlike someone on Pension Credit, you will have to claim each one individually and may only get a proportion whereas if you are on Pension Credit they will be automatic.

I am not sure what “Disability (69.40pw)” refers to. It would be normal for someone claiming after State Pension Age to claim Attendance Allowance. However, this is not an income-related benefit.

Even better if we went to an automatic tax form where the Gov. who knows almost everything about you anyway and should surely know what Gov. benefits you are due would send you your completed tax form every year, you check it over and if it is correct thats all you have to do but the companies that provide tax filing services do not want this to happen. I think several countries do this already..? Denmark?

This is what happens in many countries now

I have had to think about the idea of doing this by Tax as it has some merits. I have come across it before and these were my thoughts. I cannot agree that this is better than an adequate basic pension. I say this for the same reason that I don’t think anyone should have to claim in-work benefits. They should receive a real living wage; pensioners a living pension.

So, why do I think this way? It is all to do with giving confidence and diminishing anxiety. Proving poverty and even more showing each and every change in the amount you live on from month to month is debilitating. Informing “the government” of every tiny change in your income gives people “brown envelope anxiety”. With basic pensions or income that does not need a state “top-up” people have a lot better chance of launching into a better paying job, being active in their community and staying out of debt.

Your ideas of information campaigns are worthy. However, they will not get through to many of those who need the support. They despair when told they are on a “legacy benefit”; they give up when they think not receiving one benefit stops them from receiving others. They did not set out to be an adjunct to the taxation staff and often lack the capacity to do so effectively.

Can you develop further?

I think I explained that I would like to see a Basic Pension for all in line with the JFR Trust figure that would take everyone out of means-tested benefits. Benefits to provide housing would have to continue until we had housing itself on a better footing; it might concentrate minds.

In-work benefits are not really of benefit to the worker. They would benefit more by having a wage that properly covers all basics and is paid by the employer. I would not include housing and/or child care as they should both be dealt with elsewhere. In-work benefits actually benefit the employer. How much easier – and fairer – it would be to say companies must pay a proper living wage but they can claim “benefits” in the form of loans or grants from the government based on their accounts. They would have to show why the business cannot “afford” the living wage. Paying the highest in the company excessive multiples of the lowest or paying dividends that favours the shareholder above proper wages would be taken into account.

I would like us to stop is asking people who did not take a degree in “Benefits” to deal with this hugely complex system.

I could go on about people being more effective members of society if they have the sense of agency that comes with a guaranteed regular income but I don’t think this is what you want. Ask me questions if I have missed what you want to know but remember, these ideas are just my thoughts and opinions – I came on here to learn from you!