As the FT has reported this morning:

High levels of UK inflation could persist for longer than expected, the Bank of England's new chief economist said, suggesting he agrees with the more hawkish elements of the Monetary Policy Committee.

Worryingly, we have another debt and inflation fetishist at the Bank. What that means is that if the cost of living is rising - as is expected - he will want to increase it still further by increasing interest rates. It's very hard to make up a policy more callous than that.

There are also very good reasons to dispute what he has to say. I could argue the point, but I noticed this blog from the IMF put out before its autumn meeting and think it makes it very well, so I will share it instead:

Inflation Scares in an Uncharted Recovery

By Francesca Caselli and Prachi Mishra

A key question is what combination of events could cause persistently faster price gains

The economic recovery has fueled a rapid acceleration in inflation this year for advanced and emerging market economies, driven by firming demand, supply shortages, and rapidly rising commodity prices.

We forecast in our latest World Economic Outlook that higher inflation will likely continue in coming months before returning to pre-pandemic levels by mid-2022, though risks of an acceleration do remain.

The good news for policymakers is that long-term inflation expectations are well anchored, but economists still disagree about how enduring the upward pressure for prices will ultimately be.

Some have said government stimulus may push unemployment rates low enough to boost wages and overheat economies, possibly de-anchoring expectations and resulting in a self-fulfilling inflation spiral. Others estimate that pressures will ultimately be transitory as a one-time surge in spending fades.

Inflation Dynamics and Recovering Demand

We examine if headline consumer price index inflation has moved in line with unemployment. Although the pandemic period poses many challenges to estimating this relationship, the unprecedented disturbance doesn't seem to have substantially altered this relationship.

Advanced economies are likely to face moderate near-term inflation pressure, with the impact softening over time. Estimates of the relationship between slack, the amount of resources in an economy that aren't being used, and inflation for emerging markets instead seem to be more sensitive to the inclusion of the pandemic period in the estimation sample.

Anchoring Expectations

Inflation during the pandemic has been well anchored, according to measures of long-term expectations known as breakevens drawn from government bonds in 14 nations. These closely watched gauges have been stable so far during both the crisis and the recovery, though uncertainty about the outlook remains.

A key question is what combination of conditions could cause a persistent spike in inflation, including the possibility that expectations become unanchored and help spark a self-fulfilling upward spiral for prices.

Such episodes in the past have been associated with sharp exchange-rate depreciations in emerging markets and have often followed surging fiscal and current account deficits. Longer-term government spending commitments and external shocks could also contribute to expectations becoming de-anchored, especially in economies with central banks that aren't believed to be able or willing to contain inflation.

Moreover, even when expectations are well anchored, a prolonged overshoot of the inflation target that policymakers have set could cause a de-anchoring of expectations.

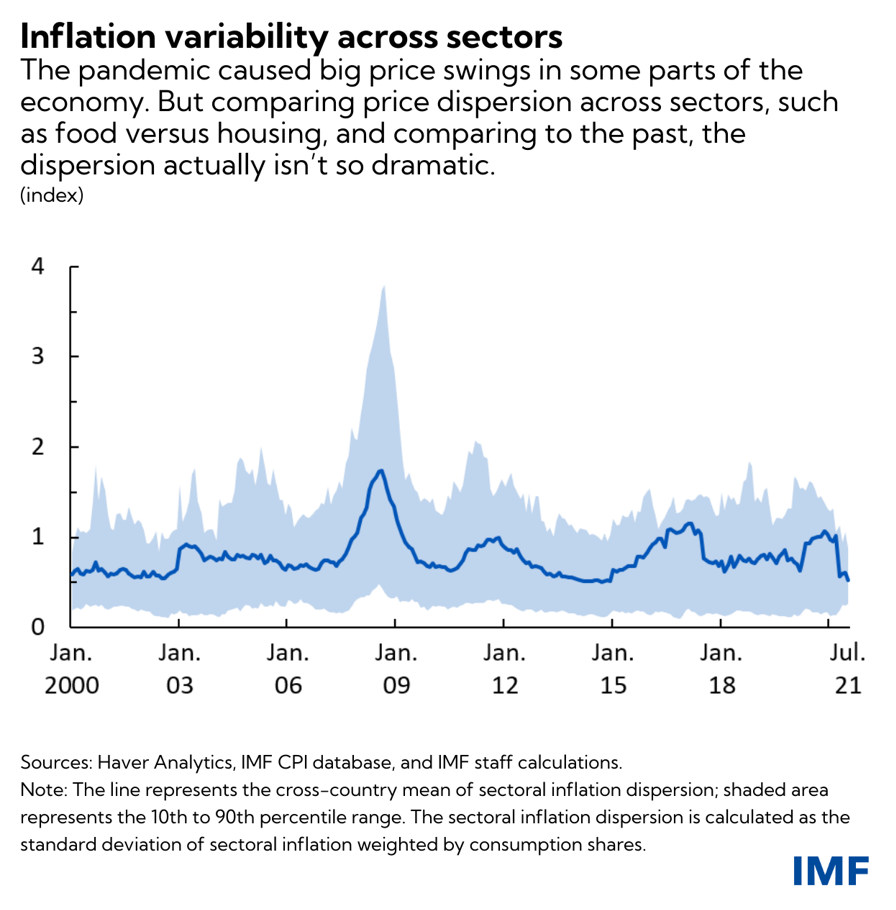

Sectoral Shocks

The pandemic has triggered large price movements in some sectors, notably food, transportation, clothing, and communications. Strikingly, the dispersion or variability in prices across sectors has so far remained relatively subdued by recent historical standards, especially compared with the global financial crisis. The reason is relatively smaller and shorter-lived swings in fuel, food, and housing prices post the pandemic, which are the three largest components of consumption baskets, on average.

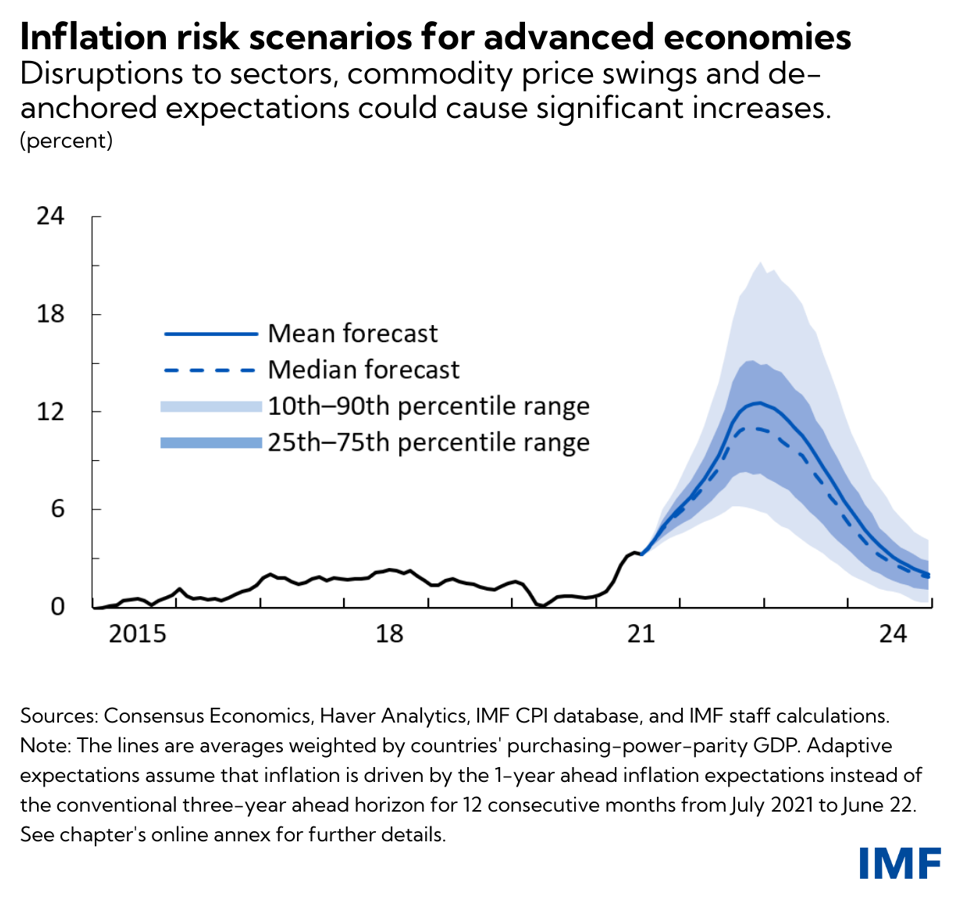

Our forecast is that annual inflation in advanced economies will peak at 3.6 percent on average in the final months of this year before reverting in the first half of 2022 to 2 percent, in line with central bank targets. Emerging markets will see faster increases, reaching 6.8 percent on average then easing to 4 percent.

The projections, however, come with considerable uncertainty, and inflation may be elevated for longer. Contributing factors could include surging housing costs and prolonged supply shortages in advanced and developing economies, or food-price pressure and currency depreciations in emerging markets.

Food prices around the world jumped by about 40 percent during the pandemic, an especially acute challenge for low-income countries where such purchases make up a big share of consumer spending.

Simulations of several extreme risk scenarios show prices could rise significantly faster on continued supply chain disruptions, large commodity price swings, and a de-anchoring of expectations.

Policy Implications

When expectations become de-anchored, inflation can quickly take off and be costly to rein back in. Ultimately, central bank policy credibility and price expectations are difficult to precisely define, and any assessment of anchoring can't be decided entirely based on relationships in historical data.

Policymakers therefore must walk a fine line between remaining patient in their support for the recovery and being ready to act quickly. Even more importantly, they must establish sound monetary frameworks, including triggers for when they would reduce support for the economy to rein in unwelcome inflation.

These thresholds for action could include early signs of de-anchoring inflation expectations, including forward-looking surveys, unsustainable fiscal and current account balances, or sharp currency swings.

Case studies show that while strong policy action has often tamed inflation and expectations for it, sound and credible central bank communication also played an especially crucial role in anchoring views. Authorities must be alert to triggers for a perfect storm of price risks that could be individually benign but when combined may lead to significantly more rapid increases than predicted in the IMF's forecasts.

Finally, a key feature of the outlook is that there are significant differences across different economies. Faster inflation in the United States, for example, is projected to help drive the acceleration for advanced economies, though pressures in the euro area and Japan are estimated to remain relatively weak.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Richard, the commodity market has moved centre stage again, currently on the back of the spike in wholesale gas prices. The media just plug the evil Russians line, but it would be helpful if you could explain how these markets function, since I cannot believe that is the key.

If I get time…

I think a little perspective is need. CPIH is based at 100 in 2015. If the BoE was hitting its 2% target since then the index should be at about 114; it is 112. For the BoE to hit its target (on an 8 year view) by end 2022 (when, perhaps, some bottlenecks in supply have eased) we need to see prices rise by about 5%. So, I am sorry, but inflation at 4% or even 6% over the next year or so is not a problem from a macro economic perspective (although I accept that for many individuals it is an issue). It only becomes a problem if medium/long term inflation expectations rise. At present, that is not happening despite the best efforts of headline writers to generate the next “panic”.

I also think we do need to see a rebalancing of our economy in favour of labour over capital and this best happens through rising wages and benefits…. with incomes for the wealthy (rent in its broader economic sense) being held stable. Yes, that will mean some inflation but I would see that as redistribution. The standard line that inflation hurts the poorest most is only true if Government policy makes it true! (Ie. NI rises and public sector pay caps and benefit caps/cuts.)

I DO side with your view that inflation is unlikely to embed itself… but even if I am wrong (yes, it has been known!!) the consequences are relatively minor.

Agreed

[…] Cross-posted from Tax Research UK […]

According to the labour cost index published by eurostat, labour costs in the euro zone are down compared to this time last year. There is zero inflationary pressure coming from wages.

I would like to see some actual proof that increasing interest rates as ever decreased inflation. Do not quote the inflation in the 70’s due to the oil price increase. It came down in the end when the higher oil price worked it’s way throughout the economy.

I suspect there is none

In the early 1980s Paul Volker was head of the US Federal Reserve and raised interest rates, up to 20% at one point. Inflation did come down over the next two years, albeit at the cost of rising unemployment.

I leave it to others to say if it were correlation or causation.

The danger in raising interest rates, when there is a high level of private debt, is that it could cause a crash. That might ‘cure’ an inflation problem but not in a way we would want. The ‘cure’ being worse than the disease itself.

It’s best to follow the IMF advice and adopt a ‘wait and see’ approach but I suspect the government /BoE will want to be seen to be doing something so there could be trouble ahead.

This obsession with interest rates as a corrective device is very worrying.

On R4 this morning the ‘worry’ was that inflation would not be a blip and would be ’embedded’ in the economy for a long time.

I mean come on – it’s too bloody early to tell surely? Do they really think that we are that stupid?

Yes

Maybe we should reduce interest rates the 4-5% that is normal to kick start economies. Oh wait we can’t anymore without going nominally negative as well as actually negative (taking into account CPI) Maybe we just realise the can kicking has come to an end and the long term debt cycle had played out with our debt based currency system. So we re-set using central bank digital currency to trap people in the system. Some take a haircut. The question is who?

Living beyond our means and refusing to entertain normal boom and bust will soon be beyond our hubris to control.

I think the hubris might be yours

“[N]ormal boom and bust”.

There is your problem.

David J,

If you are wanting to make the point that we cannot go on reducing interest rates indefinitely to resuscitate a flagging economy, then I would agree.

We have two alternatives. Don’t bother trying, or use fiscal measures to regulate the economy – either upwards or downwards. I’m not sure which will be needed at the moment so I would be inclined to wait at least until the start of the New Year before doing anything.

‘Stuff’ is going to cost more. Everything, food water, steel, energy, everything. But not in the UK alone. The reason is that we have externalised the true costs of energy for over a hundred years. We made energy cheap by subsidising it and putting the true costs into the commons in the form of carbon, pollution, plastic in the seas etc. This is now coming home to roost. It’s what Capitalism does and since no-one wants to talk about the cause, not the symptoms, it will get a whole lot worse. The UK will suffer badly, partly due to the self imposed idiocy of a no-deal Brexit, secondly because our democracy is broken, which is why we have the clown in No10 and Sir Rodney Woodentop as Loto. In the last few years we have had a plague (which will be back with a vengeance as we didn’t vaccinate the rest of the world as Pharma needed to make huge profits), locusts across Africa and the ME, Huge storms and downpours, Floods, and volcanoes. It’s all going to get a huge lot worse as there isn’t a politician on the planet with a plan. We are heading to the biggest inflationary wave in human history. We might stave off a short term blip but long term it will be horrendous. China has fired up its coal power stations this week to keep the show on the road, but we are running out of road. Fast.

A simplistic view

To buy goods and services from other countries, the UK has to sell goods and services of equivalent value to those countries.

The effect of Brexit has been to reduce the goods and services we can sell, so that we now have to buy them from other countries (even blue passports)

This will surely cause the value of the £ to fall, so that the same basket of goods will cost more.

I can’t see how raising interest rates will do anything to solve this type of inflation

You are right on both counts

Do proper economists really not see this?

Who are proper economists?

“To buy goods and services from other countries, the UK has to sell goods and services of equivalent value to those countries.”

I’m not sure why you think this. There are many countries in the world which will do whatever it takes to run a trade surplus. Usually this involves some steps to lessen domestic demand by a combination of taxation and a low exchange rate. They end up also having to feed money into the capital accounts of the deficit countries, like us, to stop their exchange rate from dropping.

The deficit countries do have the advantage, at least in the short term, of not having to sell an equivalent value.

If anyone “surely” knows how currencies will move relative to each other they’d be a awful lot richer than they are.