The Corporate Accountability Network has published a new report on the tax accounting of Tesco plc this morning. It's important to note that Tesco was picked because almost everyone knows of it. It also engaged with requests for data. It is the first of a series of companies to be investigated and not an isolated example. It is not in any way considered exceptional.

The work had a simple objective. As the report notes:

In this note the accounts of Tesco plc for 2021, 2020 and 2019 are reviewed to see if the entries in them with regard to corporation tax quite literally add up. We also checked to see if they gave a clear impression of the tax bills owing by the company in each of those years.

As a matter of fact, the accounts of all companies do add up with regard to tax: they have to or the double-entry within them would not be complete. The concern is that there is insufficient information disclosed within the accounts to show how this happens, with the potential that the full tax charge for a year might not be understood as a result.

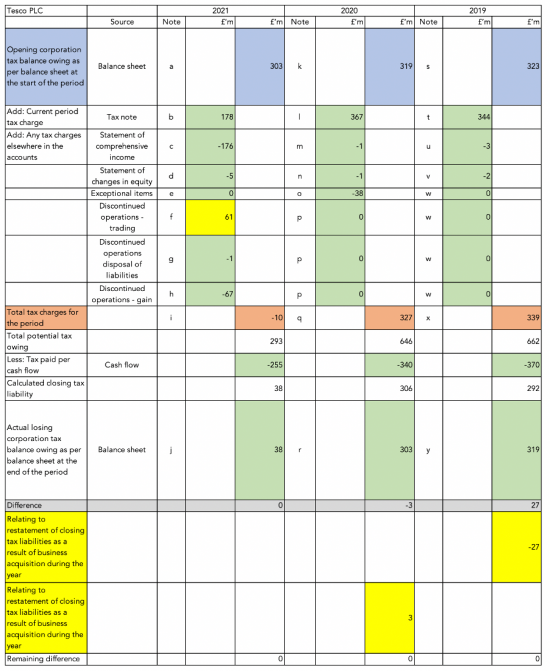

There was insufficient disclosure in the accounts of Tesco plc for each of the years ended in 2019, 2020 and 2021 to understand how its accounts did add up. A reconciliation of its tax liabilities was only possible with the use of additional data supplied by the company.

The differences were not small. The figures highlighted in yellow in this reconciliation table for Tesco had to be supplied by the company as they were not available in the accounts:

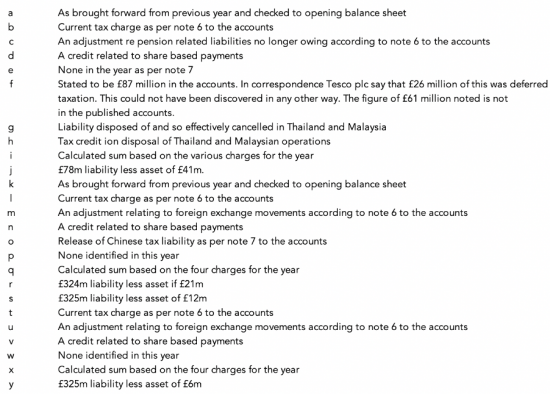

These notes help explain this reconciliation:

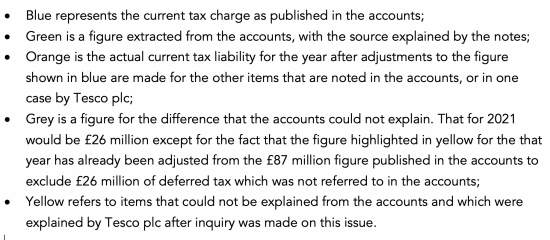

And the colour coding has to be explained:

Three figures had to be supplied and explained by Tesco plc to make the above figures balance:

- In 2019 the closing tax liability was inflated by a sum owing in respect of Booker plc, which was acquired during that year, which sum did not reflect trading in the year. As Tesco plc have pointed out, this did not need to be separately disclosed with regard to that acquisition, but it did mean that the accounts could not be shown to add up using the data disclosed within them;

- In 2020 an immaterial business disclosure took place and £3 million of tax liability was transferred as part of that disposal. As Tesco plc have pointed out, this did not need to be separately disclosed with regard to that acquisition, but it did mean that the accounts could not be shown to add up using the data disclosed within them;

- In 2021 tax of £87 million was shown to be due on discontinued trading operations (see section H of the data appendix). This sum was not split between deferred and current tax liabilities arising. Tesco plc has advised that £26 million of this sum related to deferred tax, leaving the current tax charge as £61 million. This information could not be ascertained from the accounts meaning that the accounts could not be shown to add up using the data disclosed within them.

I am grateful to Tesco plc for supplying this information when request was made. The required information could not have been ascertained in any other way.

As I explain in the Corporate Accountability Network report, the implications of the findings are important and universal: Tesco is just being used as an example here. In particular, what the report shows is that the headline figures for tax paid in a set of accounts can be quite misleading:

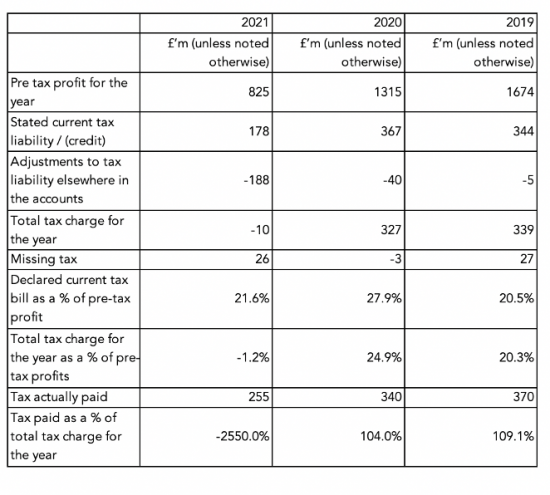

Almost all analysis of tax due by company is based on the figure for tax owing as reported in the notes to the income statement or profit and loss account. Very often those doing that analysis do not differentiate the figures for current and deferred tax: that in itself produces gross distortions with regard to real taxes owing since deferred tax is just an accounting entry and no such tax liabilities ever exist, as such. But worse, as this analysis shows, tax figures can and do readily pop up elsewhere in the accounts, and are very often significant. As this analysis shows, the income statement of Tesco for 2021 shows a tax liability owing at a rate of 21.6%. After adjustments are made for other figures in the accounts that changes to a refund owing of 1.2%. I think that material to the understanding of the accounts. I very strongly suspect that this matters.

The report suggests a range of parties to whom this might be of concern. I pick out three here. First there are shareholders:

This accounting test is a basic test of accounting credibility. Can the company make reliable statements to its members? If it cannot, what dependence should be placed upon the other statements included in the accounts? Should shareholders have to go to the lengths we have to establish the true position of the tax data within the accounts of the entity?

Then there are tax authorities:

The correct statement of tax liabilities is of significance to tax authorities because they are dependent upon the correct statement of accounts as the starting point for the estimation of tax liabilities owing by all limited liability entities. Although the items referred to in this note do not, in themselves, impact profit, they can have a consequence. In particular, if the estimation of minimum effective tax rates is to become commonplace with regard to multinational corporations then the correct statement of the tax due and paid by a company becomes a matter of some considerable significance and the lack of appropriate accounting data to prove that this is occurring will be of importance. As such ensuring that this disclosure is correct has now become a matter of some significance.

Correct statement about other entities not subject to minimum effective tax rate calculation is also important because much of the risk assessment process undertaken by tax authorities to decide those whose affairs should be audited is dependent upon statistical analysis, and the failure to appropriately state accounts could impact the quality of that work with a misallocation of scarce tax authority resources arising as a result.

And, of course, there is civil society:

The tax paid by large companies has become a matter of considerable concern to many organisations within civil society during the 21st century. Those organisations are dependent upon the provision of correct information from companies to ensure that any review that they undertake is reliable. In that case any test that proves the reliability of the information supplied is of considerable significance to civil society and any difference arising should be a matter of some concern to those engaged within it.

What can be done about this

As I note in the report, the obvious solution to the problem that we have identified is for Tesco plc to ensure that its accounts do reconcile in the way that we have noted that they should each year.

We suggest that a reconciliation demonstrating that this is the case be added to its tax note within its accounts in each year in the future.

We suggest that the same requirement be made of all companies, irrespective of size. Given the importance of tax within accounts we suggest that this basic test of credibility is an essential part of accounts in an era when tax is such a significant issue for all companies whatever accounting rules apply to them.

We also suggest that the total tax charge for the year be disclosed in the way that we have suggested possible in this note.

If tax paid differs to tax declared we also suggest that an explanation of the differences arising should be made.

To assist achievement of these goals we suggest that when a company is not required to publish a cash flow statement it should now include a statement of the amount of corporation tax paid in a year in its tax note to its accounts.

To reinforce this requirement, we suggest that the items that we note now be required by International Financial Reporting Standards; by UK generally accepted accounting principles and by UK company law.

This is a real issue I will explore in other blogs to follow and in more research now underway. Our companies have to be accountable for their tax liabilities and the data that we are getting from them is not good enough.

Important note: Tesco plc made this statement on this work which is also noted in the report:

The assertion that numbers in our audited accounts do not add up in relation to tax is incorrect. We take our tax reporting and tax compliance extremely seriously, and our corporate tax reporting adheres to all relevant accounting standards. The detailed tax disclosures in our consolidated accounts are in line with market practice and comply with the International Reporting Standard IAS12 in relation to tax. We have provided full explanations for each of the points raised with us, and we strongly disagree with the tone and conclusions of this report.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

[…] have published a report this morning that reviews tax disclosures in the accounts of Tesco plc. The question I asked is […]

[…] that case making sure that the disclosures that I suggest are required in blogs here and here this morning are very important. Cutting off opportunities for abuse before they arise is […]

Tesco may feel aggrieved when they abide by the tax laws yet are singled out in the report.

This Tesco customer is encouraged to continue shopping with the company, for the fact that they have cooperated with the CAN to enable the report to be made. I hope every other company you ask will also provide the information needed.

Have I got this right:

* in each of the three periods you looked at, Tesco paid more actual cash tax than the accounts indicated? (Just corporation tax, or other taxes too?)

* in each of those periods, the discrepancies between the numbers you could calculate from the accounts and the true position could be resolved by one line item or one note in each year, in each case relating to a single acquisition or disposal?

* as things stand, none of those single is required to be separately disclosed?

I am all in favour of better accounting information, and many of the changes in the last decade or so seem to make a company or group’s accounts less useful, not more. But in this case it seems rather small beer. I expect you can find much more deserving targets for opprobrium.

You have not really got this right

In this case it is true that the differences do relate to M&A in some way, but they are not small

And the resulting g presentation of data leaves an impression of tax owing that is quite surprising

There is no way of concluding that a single entry is missing from all accounts (so far, no accounts looked at balance)

And so far none of the accounts appear to provide a reliable view of what tax was actually due for a period and why significantly different sums might be paid

I would all that pretty big beer suggesting serious likely errors in corporate valuation

OK! As may be apparent, I’m not an accountant. I was just looking at the three yellow numbers, which show a delta of £61m, £3m and £27m. Presumably there was an earlier stage in your analysis when you realised there were one or more things leading to a net difference of £61m, £3m and £27m between what you calculated and what the accounts said.

A million pounds is a large number, of course, and everyone would like accounts to at least balance – and I agree it would make sense to pull the tax disclosures together in one place rather than, as seems to be the modern way, spreading them out and burying them among many different statements and notes – but in the context of a £25 billion company with revenues approaching £60 billion and operating profits around £2 billion and actually paying £255m, £340m and £370m of tax, the odd million or few here or there in its reported accounts does not seem that great, I’d suggest; particularly when the final reported seem to be correct.

I’d say that in terms of risk appraisal saying there is a liability of £178m when there was a refund of £10m owing, suggesting much of not all of that £255m paid is coming back soon, is a big issue and very material when a business should be valued on after-tax cash flow

I guess here the base assumption is that we cannot trust our tax authorities to be on the case regarding collection of the correct amount of tax. Also, the suggestion is that along with accounting information there should be full disclosure of their tax position in accounts so that every reader of the accounts can establish their tax position. The fact that we can not trust our tax authorities to do what they should and we need to have oversight is a problem. Who amongst us has this time to examine the accounts in such detail. I would expect our tax authority to do so but know that they are not adequately funded or staffed to do so properly. They are pitted against corporations with resources to buy in the services of the biggest accountancy firms to find ways to minimise their tax bills and often these same firms are advising the governments on their tax rules. Do we look in the wrong place in that case? Should we tackle these monoliths of accountancy firms who have a win win environment right now? I get angry when I see the plush offices of these accountancy firms all over the world and believe mostly that they are inherently “crooked” in order to perpetuate their growth and continued existence.