It felt like the morning for a Twitter thread on the national debt. I just published this:

We have just had another week when the media has obsessed about what they call the UK's national debt. There has been wringing of hands. The handcart in which we will all go to hell has been oiled. And none of this is necessary. So this is a thread on what you really need to know.

First, once upon a time there was such a thing as the national debt. That started in 1694. And it ended in 1971. During that period either directly or indirectly the value of the pound was linked to the value of gold. And since gold is in short supply, so could money be.

Then in 1971 President Nixon in the USA took the dollar off the gold standard, and after that there was no link at all between the value of the pound in the UK and anything physical at all. Notes, coins and, most importantly, bank balances all just became promises to pay.

A currency like ours that is just a promise to pay is called a fiat currency. That means that nothing gives it value, except someone's promise. And the only promise we really trust is the government's.

If you don't believe that it's the government's promise to pay that gives money its value, just recall when Northern Rock failed in 2007. There was the first run on a bank in the UK for 160 years. But the moment the government said it would pay everyone that crisis was over.

There's a paradox here. We trust the government's promise, which implies it has lots of money, and we get paranoid about the national debt, which suggests the government has no money. Both of those things can't be right, unless there's something pretty odd about the government.

And of course there is something really odd about the government when it comes to money. And that is that the government both creates our currency by making it the only legal tender in our country and also actually creates a lot of the money that we use in our economy.

How it makes notes and coin is easy to understand. They're minted, or printed, and it's illegal for anyone else to do that. But notes and coin are only a very small part of the money supply - a few percent at most. The rest of the money that we use is made up of bank balances.

The government also makes a significant part of our electronic money now. The commercial banks make the rest, but only with the permission of the government, so in fact the government is really responsible for all our money supply.

This electronic money is all made the same way. A person asks for a loan from a bank. The bank agrees to grant it. They put the loan balance in two accounts. The borrower can spend what's been put in their current account. They agree to repay the balance on the loan account.

That is literally how all money is made. One lender, the bank. One borrower, the customer. And two promises to pay. The bank promises to make payment to whomsoever the customer instructs. The customer promises to repay the loan. And those promises make new money, out of thin air.

If you have ever wondered what the magic money tree is, I have just explained it. It is quite literally the ability of a bank and their customer to make this new money out of thin air by simply making mutual promises to pay.

The problem with the magic money tree is that creating money is so simple that we find it really hard to understand. We can have as much money as there are good promises to pay to be made. It's as basic as that. The magic money tree really exists, and thrives on promises.

But there's a problem. Bankers, economists and politicians would really rather that you did not know that money really isn't scarce. After all, if you knew money is created out of thin air, and costlessly, why would you be willing to pay for it?

What is more, if you knew that it was your promise to pay that was at least as important as the bank's in this money creation process then wouldn't you, once more, be rather annoyed at the song and dance they make about ever letting you get your hands on the stuff?

The biggest reason why money is so hard to understand is that it has not paid ‘the money people' to tell you just how money works. They have made good money out of you believing that money is scarce so that you have to pay top dollar for it. So they keep you in the dark.

There are two more things to know about money before going back to the national debt. The first is that just as loans create money, so does repaying loans destroy money. Once the promise to pay is fulfilled then the money has gone. Literally, it disappears. The ledger is clean.

People find this hard because they confuse money with notes and coin. Except that's not true. In a very real sense they're not money. They're just a reusable record of money, like recyclable IOUs. They can clear one debt, and then they can be used to record, or repay a new one.

The fact is that unless someone's owed something then a note or coin is worthless. They only get value when used to clear the debt we owe someone. And the person who gets the note or coin only accepts them because they can use them to clear a debt to someone else.

So even notes and coin money are all about debt. They're only of value if they clear a debt. And we know that. When a new note comes out we want to get rid of the old type because they no longer clear debt: they're worthless. When the ability to pay debt's gone, so has the value.

So debt repayment cancels money. And all commercial bank created money is of this sort, because every bank, rather annoyingly, demands repayment of the loans that it makes. Except one, that is. And that exception is the Bank of England.

So what is special about the Bank of England? Let's ignore its ancient history from when it began in 1694, for now. Instead you need to be aware that it's been wholly owned by the UK government since 1946. So, to be blunt, it's just a part of the government.

Please remember this and ignore the game the government and The Bank of England have played since 1998. They have claimed the Bank of England is ‘independent'. I won't use unparliamentary language to describe this myth. So let's just stick to that word ‘myth' to describe this.

To put it another way, the government and the Bank of England are about as independent of each other as Tesco plc, which is the Tesco parent company, and Tesco Stores Limited, which actually runs the supermarkets that use that name. In other words, they're not independent at all.

And this matters, because what it means is that the government owns its own bank. And what is more, it's that bank which prints all banknotes, and declares them legal tender. But even more important is something called the Exchequer and Audit Departments Act of 1866.

This Act might sound obscure, but under its terms the Bank of England has, by law, to make any payment the government instructs it to do. In other words, the government isn't like us. We ask for bank loans but the government can tell its own bank to create one, whenever it wants.

And this is really important. Whenever the government wants to spend it can. Unlike all the rest of us it doesn't have to check whether there is money in the bank first. It knows that legally its own Bank of England must pay when told to do so. It cannot refuse. The law says so.

As ever, politicians, economists and others like to claim that this is not the case. They pretend that the government is like us, and has to raise tax (which is its income) or borrow before it can spend. But that's not the case because the government has its own bank.

It's the fact that the government has its own bank that creates the national currency that proves that it is nothing like a household, and that all the stories that it is constrained by its ability to tax and borrow are simply untrue. The government is nothing like a household.

In fact, the government is the opposite of a household. A household has to get hold of money from income or borrowing before it can spend. But the gov't doesn't. Because it creates the money we use there would be no money for it to tax or borrow unless it made that money first.

So, to be able to tax the government has to spend the money that will be used to pay the tax into existence, or no one would have the means to pay their tax if it was only payable in government created money, as is the case.

That means the government literally can't tax before it spends. It has to spend first. Which is why that Act of 1866 exists. The government knows spending always comes before tax, so it had to make it illegal for the Bank of England to ever refuse its demand that payment be made.

So why tax? At one time it was to get gold back. Kings didn't want to give it away forever. But since gold is no longer the issue the explanation is different. Now the main reason to tax is to control inflation which would increase if the government kept spending without limit.

There is another reason to tax. That is that if people have to pay a large part of their incomes in tax using the currency the government creates then they have little choice but use that currency for all their dealing. That gives the government effective control of the economy.

Tax also does something else. By reducing what we can spend it restricts the size of the private sector economy to guarantee that the resources that we need for the collective good that the public sector delivers are available. Tax makes space for things like education.

And there is one other reason for tax. Because the government promises to accept its own money back in payment of tax - which overall is the biggest single bill most of us have - money has value.

It's that promise to accept its own money back as tax payment that makes the government's promise to pay within an economy rock solid. No one can deliver a better promise to pay than that in the UK. So we use government created money.

So, what has all this got to do with the national debt? Well, quite a lot, to be candid. I have not taken you on a wild goose chase to avoid the issue of the national debt. I've tried to explain government made money so that you can understand the national debt.

What I hope I have shown so far is that the government has to spend to create the money that we need to keep the economy going, which it does every day, day in and day out through its spending on the NHS, education, benefits, pensions, defence and so on.

And then it has to tax to bring that money that it's created back under its control to manage inflation and the economy, and to give money its value. But, by definition it can't tax all the money it creates back. If it did then there would be no money left in the economy.

So, as a matter of fact a government like that of the UK that has its own currency and central bank has to run a deficit. It's the only way it can keep the money supply going. Which is why almost all governments do run deficits in the modern era.

And please don't quote Germany to me as an exception to this because it, of course, has not got its own currency. It uses the euro, and the eurozone as a whole runs a deficit, meaning that the rule still holds.

So deficits are not something to worry about, unless that is you really do not want the UK to have the money supply that keeps the economy going, and I suspect you'd rather we did have government money instead of some dodgy alternative.

But what of the debt, which is basically the cumulative total of the deficits that the government runs? That debt has been growing since 1694, almost continuously, and pretty dramatically so over the last decade or so, when it has more than doubled. Is that an issue?

The answer is that it is not. This debt is just money that the government has created that it has decided not to tax back because it is still of use in the economy. That is all that the national debt is.

Think of the national debt this way: it's just the future taxable income of the government that it has decided not to claim, as yet. But it could, whenever it wants.

That's one of the weird things about this supposed national debt. When we're in debt we can't suddenly decide that we will cancel the debt by simply reclaiming the money that makes it up for our own use. But the government can do just that, whenever it wants.

This gives the clue as to another weird thing about this supposed national debt. It really isn't debt at all. Yes, you read that right. The national debt isn't debt at all.

That's because, as is apparent from the description I have given, the so-called national debt is just made up of money that the government has spent into the economy of our country that it has, for its own good reasons, decided to not to tax back as yet.

So, the national debt is just government created money. That is all it is. But the truth is that the people of this country did not, back in 1694 when interest rates were much higher than they are now, like holding this government created money on which no interest was paid.

You have to remember something else about those who held this government created money in times of old (though not much has changed now). They were the rich. If you don't believe me go and read Jane Austen's ‘Pride and Prejudice' and note how much Bingley had in 4% government bonds.

And there was something about the rich, then and now. They get the ear of government. And so their protests about ending up with government money without interest being paid were heard. And so, money it might be, but from the outset the national debt had interest paid on it.

The so-called national debt still has interest paid on it. But then so do bank deposit accounts. And they look pretty much like money too. Only, they're not as secure (at least without a government guarantee in place) and so the government can pay less.

But let's be clear what this means. The national debt is money that represents the savings of those rich or fortunate enough to have such things on which interest is paid by the government because it's been persuaded to make that payment.

Let me also be clear about something else. Those savings are not in a very real sense voluntary. If the government decides to run a deficit - and that is what it does do - then someone else has to save. This is not by chance it is an absolute accounting fact.

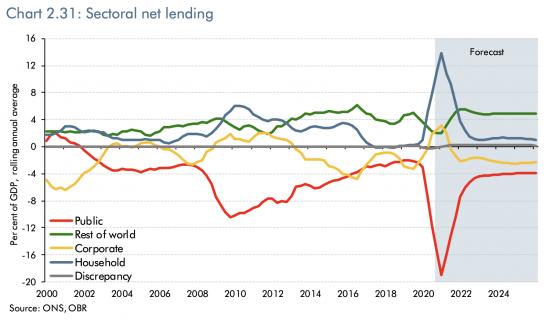

Where money is concerned for every deficit someone has to be in surplus. To be geeky for a moment, this is an issue determined by what are called the sectoral balances. There's a government created chart on these here.

The chart makes it clear that when the government runs a big deficit - as it did, for example, in 2009 - then someone simply has to save. They have no choice. And what they save is government created money. Which is exactly what is also happening now.

A growing deficit is always matched by savings. So who is saving? I am deliberately using approximate numbers, because they can quite literally change by the day. But let's start by noting that the most common figure for government debt was £2,100 billion in December 2020.

Of this sum, according to the government, £1,880 billion was government bonds, £207 billion was national savings accounts and the rest a hotch-potch of all sorts of offsetting numbers, like local authority borrowing. I don't think they do their sums right, but let's start there.

Except, these official figures are wrong. Why? Because at the end of December the Bank of England had used what is called the quantitative easing process to buy back about £800 billion of the government's debt, with that figure scheduled to rise still further in 2021.

I don't want to explain QE in detail here, because I have already done that in another thread, that I posted as a blog here. https://www.taxresearch.org.uk/Blog/2020/11/22/the-history-and-significance-of-qe-in-the-uk/

So let's, taking QE into account, discuss what really makes up the national debt, starting with an acknowledgment that if the government owns around £800bn of its own bonds they cannot be part of the national debt because they are literally not owed to anyone.

Around £200 billion of the national debt is made up of National Savings & Investments accounts. That's things like Premium Bonds, and the style of really safe savings accounts older people tend to appreciate.

Around £400 billion of the national debt is owned by foreign governments, which is good news. They do that because they want to hold sterling - our currency. And that's because that helps them trade with the UK, which is massively to our advantage.

But what's also the case is that that because of QE UK banks and building societies have around £800bn on deposit account with the Bank of England right now. This is important though: this is the government provided money stops them failing in the event of a financial crisis.

And then there's very roughly £700 billion of other debt if the Office for National Statistics have got their numbers right (which I doubt: they overstate this). Whatever the right figure, this debt is owned by UK pension funds, life assurance companies and others who want really secure savings.

Why do pension funds and life assurance companies want government debt? Because it's always guaranteed to pay out. So it provides stability to back their promise to pay out to their customers, whether pensioners, or life assurance customers, or whoever.

So now I have explained how we get a national debt and that it's a choice to have one made by government. I've also explained that all it represents is the savings of people. And I've explained the government could claim it back whenever it wants. And I've covered QE.

So, the question is in that case, which bit of the national debt is so worrying? Do we not want people to save? Or, would we rather that they had riskier savings that our pensions at risk? Is that the reason why we want to repay the national debt?

Or do we want to stop foreign governments holding sterling to assist their trade, and ours?

Alternatively, do we want to take the government created money back out of the banking system when it's saved it from collapse twice now (2009 and 2020) and which provides it with the stability that it needs to prevent a banking crash?

Or is it the national debt paranoia really some weird dislike of Premium Bonds that suggests that they are going to bring the UK economy down?

The point is, once you understand the national debt it's really not threatening at all. And what you begin to wonder is why so many people obsess about it. To which question there are three possible answers.

The first is that the obsessive do not understand the national debt. The second is that they do understand it, but want to make sure you don't. And the third is that they realise that if you did understand the national debt there would be no reason for austerity.

Of these the last is by far the most likely. There's always been a conspiracy to not tell the truth about money, and how easily it's made. There's also a conspiracy to not tell the truth about the fact government spending has to come before taxation, and the law guarantees it.

And I strongly suggest that the hullabaloo about the national debt - which is a great thing that there is absolutely no need to repay and which is really cheap to run - is all a conspiracy too.

The truth is that the national debt is our money supply. It keeps the economy of our country going. It keeps our banks stable. And it also represents the safest form of savings, which people want to buy.

There is no debt crisis. Nor is the national debt a burden on our grandchildren. Instead, the lucky ones might inherit a part of it.

But some politicians do not want you to know that there is no real constraint on you having the government and the public services you want. What the government's ability to make money, sensibly used, proves is we do not need austerity. And we never did.

Instead, the opportunity we want is available. And we do not need the private sector to deliver it. The government can and should take part in that process as well, which it can do using the money it can create as the capital it needs to do so.

But in order to pursue their own private gains and profits some would rather that this is not known, so they promote the idea that money is in short supply and that the national debt is a danger. Neither is true. We need to leave those myths behind. Our future depends on doing so.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

You’ve excelled yourself this morning with several clear, easy to understand explanations.

I hope you send these to Andrew Bailey, who seems to think he decides whether or not the Government can have money and to Rishi Sunak, who, among other problems, doesn’t seem to understand the principle of sectoral balances.

I suspect they would pay no attention

Richard-once again- SUPERB!

Thank you

Is this some sort of school essay? I’m not sure why you spent what clearly must have been a long time writing something which so full of factual faults and errors. It’s out of the land of the fairies.

Go on then, explain – exactly – why that is the case

Excellent post.

I was particularly interested in this part:

“Tax also does something else. By reducing what we can spend it restricts the size of the private sector economy to guarantee that the resources that we need for the collective good that the public sector delivers are available. Tax makes space for things like education.”

This would explain a lot. The corollary of the above is that low taxation will increase money for the private sector and reduce it for things like education.

Right wing politicians are ideologically obsessed by low taxation, which they can easily sell (not many people like paying taxes). They are also vehemently opposed to public services. Taken together, low taxation, and an aversion to spend on public services, must mean that government spending enlarges the private sector – at the expense of socially useful spending.

Some will do very well from this. Members of the government, privately owned business, rich people with money to save. The rest of us (most of us) will not.

Might I suggest Stephanie Kelton’s ‘The Deficit Myth’ – out very soon in paperback?

Ordered, thanks.

Thanks, Richard, for setting this out in such an understandable way. I always thought austerity was a choice. Sent straight to “print and keep for future reference”.

Thanks

Great article, thanks for providing. Really easy to understand and am sharing widely! I really think the work of economists like yourself, Anne Pettifor and Stephanie Kelton is going to bring about a real mindset switch eventually.

I was just wondering if you could clarify two things I’m still not fully clear on, where you say ‘The chart makes it clear that when the government runs a big deficit – as it did, for example, in 2009 – then someone simply has to save.’ Would this only be the case if the government choses to run a national debt, rather than monetising the deficit? I’m not quite clear on that.

Finally, where you make the point about the reasons why politicians are reluctant to deviate from politics of austerity and book balancing, how specifically do politicians and their donors benefit from this myth in a way they couldn’t benefit from dispelling it, as I would have thought they could justify greater tax cuts without it? Is it that they tend to hold more money in assets that value could potentially be eroded by inflation? Or the idea that businesses are ‘wealth creators’ rather than governments so need to be deregulated? Or simply a desire to maintain inequality that seems them in a more privileged position than others? Alternatively, I wonder whether the almost religious devotion to Reagenomics they can’t bring themselves to shake plays a part, or maybe politically its an easier sell as people relate to household budgets and it feels like a less abstract concept. Would love to get your insight on this.

Thanks!

a) Monetising simply swaps the way the saving takes place. It still exists

b) The answer is that the small state has to place resources in the private sector – from which rentiers make gain – as Covid cronyism proves. This is the explanation for the policy. It is private corruption over public gain

Great explanation Richard – but will Kuenssberg and Peston et al say anything meaningful in their Budget economics explainers.

So who benefits from QE or Fed stimulus?

“They take home nine figure sums for 2020 despite faltering economy …. on back of Fed stimulus” [1]

“Billionaire hedge fund boss pays himself UK record of £343m” [2]

Do these “people” earn these sums or are they gifted? Easy money; you sweat as they’ve just scooped up millions of hours of your labour.

1. https://www.ft.com/content/754d5e92-4c7c-4a0a-aa9d-4050fb2282cd

2. https://www.theguardian.com/business/2021/mar/01/billionaire-hedge-fund-boss-pays-himself-uk-record-of-343m-chris-hohn

Thanks Richard.

I know why you have been so active this morning. Because this paranoia is going result in a lot of harm being done.

Spot on

I admit not all this was written this morning

Excellent piece (and almost values-free!!)

Judging by Hague’s foreshadowing piece in the DT this morning, the core message will remain lost among the headlines tomorrow and night and in Thursday’s papers.

Among the budget bingo – “mending the country’s finances.” – 10 times or more???

At least

Add ‘hard decisions’

‘Tough choices’

And ‘There is no magic money tree’

I am in the midst of Timothy Snyder’s ‘The Road to Unfreedom’ and his depiction of ‘inevitability politics’ encompassing such phenomena as ‘ TINA’, ‘replacing policy with markets’ and the killing of new ideas is such a powerful contextual lens, and sums up this debt paranoia perfectly.

No wonder we are as a result getting fascist-like ‘eternity politics’ – a politics fed by the inequality created by inevitability politics.

Snyder’s thesis is spot on as far as I am concerned if only to give a rough shake up to the liberals who have been far too complacent and complicit in getting us to where we are today.

It is indeed time to wake up and take sides.

Clearly, when Kuensberg, Peston, Marr, Morgan et al ask “how are you going to pay for it?” when a spokesperson is promoting more spending for the public good such as more investment for carbon reduction, NHS, social security, education, justice, etc all they need to do is to refer them to the Exchequer and AuditsDepartments Act 1866 and this will convince them. If they are still in doubt then check with Andy Haldane at the Bank of England to see if he understands his own rules and the laws he is required to adhere to.

The answer to “How are you going to pay for it?” is always “With money.”

Two further reasons why the so called national debt is not debt

,

1) When the banks failed in 2008 the UK government became the lender of last resort for those banks. That by definition means the UK Government could not be borrowing from someone else. It must have created the money itself.

2) The central banks of the USA, Eurozone, Canada, Switzerland, Sweden and Japan all provided the same support for their distressed banks. Given the major banking nations were all supporting there own banking systems the UK government was not borrowing internationally.

The so called debt is not debt.

Correct

Excellent as usual Richard, however, have you seen the post by Ben Bradshaw MP, gloating over the lack of challenge by Labour MPs, to the policy of opposing raising Corp tax? It is compounded by the fact that the 3 MPs he highlights, are engaged in attempts to sell an alternative policy. If they can’t be bothered to take on their own colleagues, what hope have they got on the doorstep, or in the media.

I sincerely hope someone takes your “fantasy R4 interview” on air, and really has a go at changing the narrative

I will look

The National Debt should be renamed the National Credit, makes one feel better just changing a word. We get so hooked up on that negative meaning of the word “debt.”

On the big matter, which we hear so much about (usually with a very solemn face )…paying the debt back…… this is no ordinary debt.

What kind of debt can be cancelled by the debtor? Us mere mortals cannot do this, but a govt can cancel its own debt anytime it likes either by raising taxes, cutting spending or, just as important, printing money to fund govt spending. Everyone understands the first two points but few get that there is actually a third way, believing somehow that it is cheating/immoral/reckless/ruinous,(insert indignation of choice)

But it really is that easy. Sadly that goes against every basic belief about debt that every single one of us is taught from a very early age.

We need to steal that M&S advertising slogan…..”THIS is not just debt; THIS is government debt.”

That is actually very good…

You could add

”THIS is not just debt; THIS is government debt. FEEL the difference. ”

….Or “you can taste the difference”

Or maybe using the old Carlsberg meme. “If Carlsberg did debt ,it would be government debt”

Though you are likely to run into copyright infringements at some point.

Well done.

Unlike “Piro”, I can’t find any factual errors at all….. and I have tried.

Thank you

They should build a life-size model of the Grantham grocery shop somewhere in the House of Commons where it will cause the most obstruction to MP’s moving about their business because this is monetary system budget model that most lazy ignoramus MP’s in the UK worship!

Leave a copy on Jeremy Vine’s desk?

I am not in the studio tomorrow – now done from distance .

Doh! I am so 2019….

🙂

Thanks, Richard.

I’ve sent a copy to my MP (Tracey Crouch) asking for her (or the Government’s) comments. She didn’t respond last time I sent one of your posts, but I dream I might get through to her sometime.

Thanks

Excellent article. It’s so annoying to hear the national debt myth repeated constantly in the media – I hope the truth makes a breakthrough at some point soon. The country needs it.

Craig

As gilt rates rise debt service rates rise especially where gilts are tied to inflation…… FT on budget today… Richard – can you respond to this? IE: the QE mechanism used by this government? I’m not seeking to argue with you BTW. Just confused. I read Martin Sandbu in the FT who reminds me of you.

Thanks

Four things

1) Short term interest rates are very much under gov’t control via central bank reserve accounts

2) long term rates are largely under gov’t control via QE

3) Current yields on index linked bonds are negative, and significantly so. This is only £400bn of debt.

4) I’d there any real inflation risk?

So in theory the cost could rise. But why would the government let that happen?

Thanks. Just hard to get a fix on all of this. I need to read more on your site. Many more options it would seem than the MSM suggest.

Absolutely…..

“So in theory the cost could rise. But why would the government let that happen?”

Quite, and this post – if belated student can congratulate prof – is really excellent stuff…

I wonder is there an increasing crack in the media narrative:

http://www.progressivepulse.org/economics/bbc-economics-correspondent-starts-to-get-it

and even BBC radio 4 news

mentioned here

http://www.progressivepulse.org/economics/love-is-all-we-need

It is good news

We are in touch…..

Excellent explanation. Should be on school curriculum. Might have some trouble with hubristic and greed merchants.

Oddly, this IS what I learnt at school (in ‘O’ Level Economics…. back in the 70s).

“For Governments, spending come first; tax and borrowing (gilts or overdraft) decisions follow. Banks lend first and then borrow”. I suspect that 40 years of woolly thinking and political dogma have led us to forget what was seen as self evident.

Now, I am not saying that MMT was fully fledged 40 years ago but all the elements were there.

Because we are all having to manage our household budgets, the idea of the Magic Money Tree (or MMT [in both senses]) is counterintuitive.

Your explanation of money is excellent – and it should be taught at all schools!

But what I would also like is a clear explanation of MMT limits. “Controlling Inflation” is all very well, but how much MMT money should be spent? Upon what should it be spent ? How should this spend be controlled in an ideal democracy? Full employment is a great aim, but should not the quality, usefulness and planet-saving characteristics of the employment be controlled or encouraged in some way?

Without more emphasis on explanations of the limits, we ordinary people will have trouble believing faithfully!

MMT is about how things work

Not what should be done

That is politics

It is not easy to separate National Economics from Politics.

Surely MMT should address it’s consequences, and discuss necessary limits and methods.

Everybody knows you can’t get something for nothing – and Physics says so too.

If hoi polloi & TV presenters can’t be recruited to the faith, the cause may be lost!

“Everybody knows you can’t get something for nothing . . . ”

IF there are unemployed resources then employing these resources {by increasing aggregate demand} to produce more goods and services will be the equivalent of ‘getting something for nothing’? {Ignoring any negative externalities from the production of more goods and services}.

I am not sure what your point is

Postkey

What I was hoping for was some cogent easy-to-understand argument to convert believers in the irrelevant household-budget economic model, within the general populace, and particularly within media economic commentators, to show them the light of MMT.

Richard,

Would this article be true if the government had signed up to the European monetary system?

Can Greece for example create its own money to pay off its debts to the EU ?

We know the answers but it reinforces that not losing control of the central Bank remains key.

The most worrying tendencies for me in the utterances of the Bank of England is that really believe it is important for them to be independent. They need to be put in their place ; and politicians need to understand they have more power than they want to believe.

But do we really want to encourage this government to flex its muscles?

Yes, if they mess it up we can always replace it with a better one.

But is there a better one in the wings?

The Labour Party seem hobbled by conventional economic/household thinking ; the left are divided on MMT; and proponents of MMT are divided amongst themselves.

In the end there cannot be just a nationalistic response. The European monetary system needs to be reformed and international co-operation is required for both effective funding of the international response to Covid, restoring international growth and trade, and reprioritising of action on global warming .

You may have to translate your blog into German.

The issue is harder within the EU, but QE still works, subject to political negotiation

A thought exercise: suppose Corbyn had been elected and embarked on his multi-nationalisation plans requiring, the CBI estimates, £200billion government spending. Since the plans would represent a huge threat to the Established order is it conceivable that Corbyn would not be told by the ‘independent’ Bank of England that his plans were unaffordable, regardless of the 1866 Act, and that Corbyn would have to accept it? But if this were to happen it would demonstrate that there is an authority higher than both the government and the Bank of England, overseeing and controlling what is and isn’t acceptable to it. If so where would this authority reside, and does it matter?

Very interesting point. The BoE did in fact go against the Collation govt’s deflationary policies by lowering interest rates and implementing QE. So in fact enacted inflationary monetary policies in some part contradicting the govts deflationary reducing fiscal deficit policies.

What would be stop the reverse happening is a very good question.

It is true that creating money is easy (too easy in fact) and that BoE can facilitate government debt creation by monetizing them (creating new money to buy them). It is not true that this has no negative consequences.

Money creation is always a theft from people who have had money already, assuming interest rates are unchanged. The new money supply increases prices and lowers how much those people can buy with their money. It is a form of a stealth tax, wealth is transferred from holders of money/fixed income instruments to the government, who gets the new money first. Never ending increase of government debt requires never ending money creation, which means never ending inflation and unbound wealth transfer. The speed of transfer (tax rate) is controlled by how quickly debt increases. In the extreme case it could become an hyperinflation. With the current annual deficit 20% of GDP there is a real risk the UK will end up with this scenario.

After reaching some level of the debt the process is practically irreversible. It is politically impossible to reduce the deficit significantly as it will cause a huge depression. The only way to increase deficit and pile more debt to keep the system going on.

One more point, an external debt is not a good thing. Foreigners can start selling their holdings, which would cause GBP to collapse. All those trillions of GBP assets would be worth much less in real terms.

This is so crass it is hardly worth bothering it

But just in case you can engage with argument, please note that in fact QE always increases the wealth of those already wealthy. It does not steal from then. It is a gift to them. Just go and look at the data and stop coming here with crackpot ideas and consider facts instead

Resorting to insults is hardly a sign of being classy.

If you fail to grasp my argument please explain why running an unlimited deficit funded by money creation never ended well, ideally please provide an example. No, “it is different this time” doesn’t count as evidence.

QE wealth is a paper wealth. If you hold a bond its present value increases now as interest rates go down but at the maturity it will always be the same. In other words, price jumps but then it gradully drifts down and you lose all the gain due to the QE jump. If you sell your bond holdings now you will lock the gain but you will pass the loss to the buyer. The problem is there is no way to sell all those inflated assets owned mainly by rich. If they try they will push price down. The situation is analogous to a stock bubble, it transfers the wealth from people who bought early and sold close to the top to people who bought at the top. In an aggregate there is no additional wealth created. The wealth is only created through increased population or productivity (mainly technology).

I pointed out your argument is wrong

Government deficits always create private wealth – that’s what the sectoral balances show. Please say why this is not true and why in this exception alone double entry does not apply if you seek to argue otherwise

And if you want to argue that QE has helped those least off please provide the data. The BoE says it is explicitly designed to help the wealthy, and it has achieved that goal.

And then note QE is not paper wealth, It simply substitutes bank balances for gilts. That is it. It creates no wealth, but that substitution has distributional consequences that favour the wealthiest by making assets in short supply

So, no wealth is created, but asset booms are created. I agree. hence why I argue for taxes to correct them, because they do not reverse unless QE does, and that’s not going to happen

The situation is similar to a scenario when I (private sector) have £1, I will lend it to you (the UK gov) and you give me it back as a gift. After that you have a liability to return £1. I have £1 and your promise to return £1 (an asset). The total net wealth stays the same (the loan I own cancels out with your liability).

You can only say that the gross wealth increased (I hold £1 and I have your promise). This increase of my wealth is conditional on your ability to pay the loan back.

You can repeat the whole procedure as many times as you want, I will always own £1 after each iteration. As a result you can have trillions of labilities I can have trillions of assets. What are the chances you can return me all those money? Pretty slim, you can’t pay me your loans back because you ability to pay is limited by your ability to earn money which is much smaller. Of course you can borrow even more from me to pay back previous loans but this changes nothing. Your promises are worthless, so it is my huge wealth.

The goverment ability to print doesn’t change the argument. The goverment can only print money, not real things and services, which are limited. In nominal terms (money) the goverment can pay it but it can’t in the real terms. Private wealth can increase in nominal terms infinitely but there are limits for its increase in real terms.

You ignore the fact that the state can never fail

It creates the money

You are also being absurd, and I am sure you know it

And the reality is that by printing money the state can increase liquidity in the economy – which is vital to ensuring real resources are used

But you ignore that

You haven’t read what I wrote. “In nominal terms (money) the goverment can pay it but it can’t in the real terms.”

The goverment can’t default in nominal terms but it can in the real terms (money will buy less stuff and services). In the case of the hyperinflation this is becoming an absurd. Bags of money to buy a loaf of bread.

Your attempt to insult me is an indirect acknowledgment that you agree with me. You have no arguments.

There are limits how much the goverment can squeeze out of the economy by providing liquidity.

There is no risk whatsoever of hyperinflation

Politely, stop being silly

If you knew anything about the exceptionally rare history of hyperinflation you’d know one of the conditions for it are likely to exist in any major western state right now.

And politely, you come here anonymously and are rude whilst talking total nonsense – so, you’re banned

Dear Richard, I have recently started reading your blog and as an average punter who knows little of the economic theory behind taxes I find it highly informative. I think it would be useful to publish your writter threads in some sort of epub or pdf, as a sort of primer to refer to. Thank you

So do I

I just need someone to do it…who knows what they’re doing