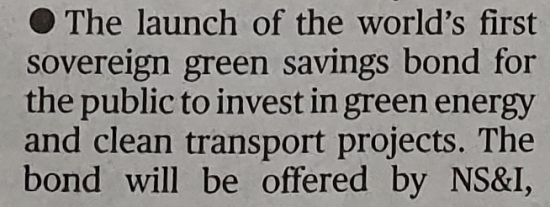

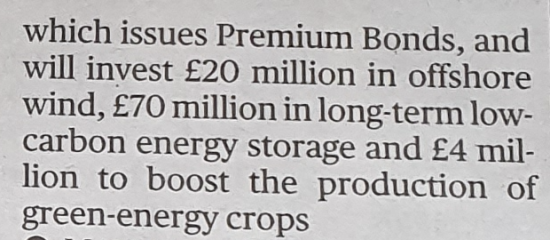

According to the Sunday Times this is going to happen in the budget:

I suspect that the figures are so precise that this is a cast-iron leak. I have posted this thread on Twitter in response:

How long does it take for a good idea to get wings? Colin Hines and I first proposed green bonds in 2003. A week ago Starmer used the idea. Now, apparently, they are going to be announced in the budget, in a half hearted way. That's progress, but there is a long way to go.

If bonds are to be used to fund the recovery three things are essential. First they have to pay an above average rate of interest. Second, they have to be government guaranteed. Third, the link to investment has to be very obvious and real.

So, the bonds have to guarantee investment where people are. There should be regional, Scottish, Welsh and Northern Ireland bonds in that case.

And there should also be bonds so people can indicate how they want their savings to be used. Health, the green new deal, housing and education bonds are obvious starting points.

Then the bonds have to be proven to have links with the resulting investments. Proper accounting is key to the success of such schemes.

But, most important, these bonds need vigorous backing. So make them the only savings available in ISAs for a start. Produce a variant for pension fund use too. That way, we could apply at least some if the £60bn spent subsidising pensions each year to social purpose.

Most important of all, make clear that this delivers four things. The first is capital for the green new deal. The amounts the government is taking about are timid. We need maybe £100bn a year, and that is possible by redirecting savings to these bonds.

Second, give savers a fair deal. 1% would be fair now. And it is wholly affordable.

Third, make clear this is about inter-generational solidarity. Savers are older people. They need to invest in jobs for younger people.

And then guarantee to make up the funding wherever there might be shortfalls, using QE created money if need be, so that this scheme can deliver jobs in every constituency of the UK- which are what is needed.

The government's plan is half baked by these criteria, but it's a start. Now make it the #realgreennewdeal.

There is more on this and the reasons for this policy here.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Most importantly for me is that Green Bonds are clearly flagged as being National Savings and Investment products not government borrowing products. Indeed if there was social justice in this country (not two main political parties masquerading as Murdoch’s Kamikaze Prole Party) treasury bonds would be issued under the auspices of the NS&I department.

Agreed

Thank you for taking the time to provide such a detailed and considered response.

We’re not as far apart as you might think. At core it’s a difference about tactics and strategy. For me, all public spending, whether current or capital expenditure, is an investment in the health, well-being, security and economic prosperity of society — and it should be assessed and allocated on the basis of how efficiently it achieves that objective.

Any positive gap between government spending and revenue is met by borrowing — which creates private wealth. I agree a range of instruments can be used to incentivise a broad range of savers and investors to place a share of their wealth in these instruments so as to secure the necessary funds. For simplicity it is possible to distinguish between bonds for which liquid secondary markets exist and savings instruments.

Since governments, for all sorts of reasons, have a tendency toward ‘deficit bias’, bond trading, in addition to providing other benefits, imposes a discipline on them. The use of savings instruments imposes far less discipline. However, the opportunity to impose discipline in this way is often abused by hedge funds, investment banks and the disaster capitalists to push and consolidate the financialisation of economies and to emasculate fiscal policy in their own interests. It was attempts by the EU and the ECB to curtail this abuse that extended the Euro crisis in the aftermath of the GFC for 4 years up to 2012.

The use of this proposed savings bond in this instance could be seen as a tactic to reduce the scope for the discipline (and the abuse of this discipline) imposed by bond market participants. However, given the sums indicated, it will have a minimal impact – and probably will provoke a concerted pushback. Strategically, I would argue that a case should be made for a much greater use of these bonds and that the focus should be on validating and legitimising the public spending it funds as a means of reducing the often abused discipline provided by bond market participants.

Labour has tentatively started on this course with its proposed Recovery Bond, but a comprehensive and forceful case needs to be made to change the terms of the public discourse.

So I’m actually arguing for pushing harder and faster and on a broader front. And to take on the nay-sayers confidently.

I do not think that market discipline exists any more: QE has shattered that

I happen to think bonds from real people would impose much more discipline: that is teal accountability

Are you not seeking to create a distinction between these bonds and other government borrowing instruments when there is no difference in reality? All government borrowing creates private wealth and it has an almost sacred duty to maintain, and potentially increase, the value of this private wealth. It is fairly typical of many on the left to try and draw a distinction between “good wealth” which is held by people the left would like to have an opportunity to increase their wealth to make provision for the ‘rainy day’ and for the future and “bad wealth” that is held by evil capitalists.

This distinction is also driven by the ‘tennis club’ accounts that governments use which employ arbitrary distinctions between current and capital expenditure. This exercise imposes another layer of arbitrary distinctions.

And, if these bonds have a hgher yield, what is stopping current bond investors also demanding higher yields?

That’s a pretty depressing comment Paul, from the comment re ‘tennis club’ arbitrary distinctions between current and capital expenditure onwards. The reality is that if you did know about government accounting you would realise that this distinction, not just beloved of tennis clubs but of all proper accounting systems is wildly underused by government, which fact in itself is a major contributor to our financial malaise.

The rest is, regret, almost as financially incoherent for someone who has commented here quite so often.

The reason for suggesting these bonds are different from other government borrowing is that they are. Your comment is like saying Premium Bonds are the same as gilts. They are not.

Nor is an NS&I savings account like a gilt. So why say it is?

Nor is it true that all government borrowing creates private wealth. Government spending not recovered by tax does that. I am not suggesting that. So, again, the claim is wrong.

The point you miss is that spending not recovered by tax – which is what MMT as well as QE suggests possible – will always create savings. That is private wealth.

I am not making a ‘distinction between “good wealth” which is held by people the left would like to have an opportunity to increase their wealth to make provision for the ‘rainy day’ and for the future and “bad wealth” that is held by evil capitalists’. Politely, that suggestion is just you being rude.

What I am saying is that if there is private wealth, 81% of it held in state subsidised forms, then it is wise to direct that wealth to social purpose. It becomes capital that way – something that MMT does recognise exists and which can be used to fund activity in the private sector. I am, through NS&I, via a state investment bank, seeking to use that capital for public good. If you have a problem that that, what is it?

Finally, you ask ‘And, if these bonds have a higher yield, what is stopping current bond investors also demanding higher yields?’ Nothing is stopping them. But maybe you aren’t aware of this, but different products in financial services do carry different returns. This is a particular, limited, and controlled access product that I am suggesting, with a particular social purpose. It won’t suit all savers. It won’t be available to many institutions who hold almost all gilts. The market is, then, already segregated. If you can’t see that this provides a mechanism for controlling the demand, I am sorry. I am not sure what more I can do to help.

Indeed if there was social justice in this country treasury bonds would be issued under the auspices of the NS&I department. Wholeheartedly agree with this Helen

Apart from the inappropriateness (to put it mildly) of the budget being leaked, the figures suggested here at at least one and maybe two orders of magnitude too low to have any impact

£94 million? It barely even registers as tokenism.

Coronavirus is bad, but global warming is an existential crisis, and action was required yesterday.

The Paris targets were probably not enough (a 50:50 chance of avoiding catastrophe by staying below 2 degrees, while accepting all of the adverse impacts that would involve, and an evens chance of much worse) and in any event required the widespread deployment of new carbon capture and storage technology before it had been invented or developed to the scale needed, and we are probably going to miss them anyway. Anyone who can should be considering what they can do, from avoiding flying to changing their electricity supplier and buying fewer things made more locally.

If you think parts of the world are unstable now, strap yourselves in, because it is going to be a bumpy ride if the Gulf Stream switches off, the Antarctic ice shelves melt, and the permafrost outgasses. Even if the deep sea clathrates stay stable.

You’re out pessimisticing me 🙂

The trouble is, you are also right