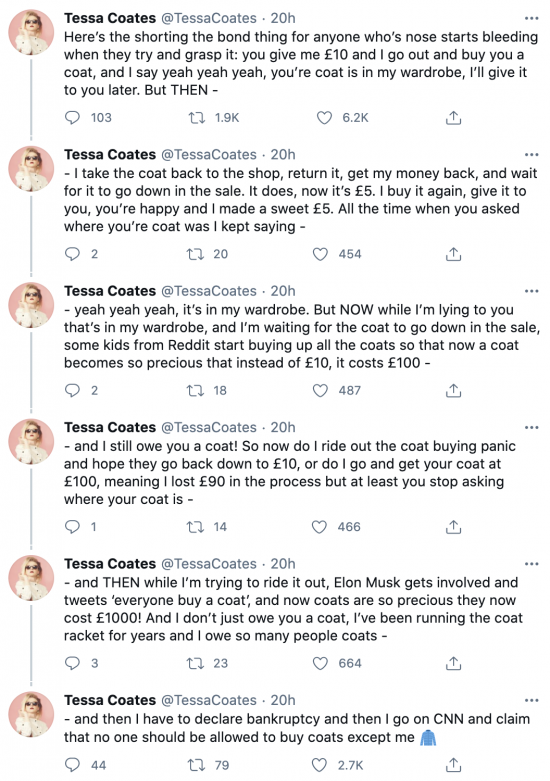

This is great:

I wish I'd written that. But I recognise merit when I see it - and that is very good.

Five things.

First, don't short unless you have very deep pockets.

Second, don't play games with shorting.

Third, don't have any sympathy with the big players who have been abusing shorting for years and now do not like being abused using the rules of their own game.

Fourth, stop stock borrowing, especially by the likes of pension funds.

Five, stop shorting and the abuse that goes with it.

This speculative waste of effort is massively destructive. It really should be game over now, for the sake of everyone. And yes, I know it will be claimed that some market liquidity will be lost. But candidly, that may be no bad thing anyway. It's highly unlikely that a trading window of more than 10 minutes a day is really required to manage most legitimate trading. The rest is useless froth that is ultimately paid f0r by innocent savers.

I will await the trolls on this one and give due warning that I will be heavy-handed with the delete button.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

It was interesting to see Facebook jump in yesterday and close down the Robin Hood Group. Apparently only the billionaires are allowed to play and when it goes against them they throw over the board in a fit of peak. Reddit still running as it’s a stand alone, and Musk got involved because the hedge funders had tried shorting him on numerous occasions so he got the chance to pile on and give them a black eye. But yes, I agree, it should be regulated much stronger, but then much of the financial industry is sleight of hand, rinsing money through various life stages to baffle and mystify whilst making off with the loot.

I have to agree with you Gordon – I wonder if it was Facebook investors who lent on them because they have skin in this game too?

Those premiums on the CDS’ must be really hurting.

There is only one form of regulation though for shorting and that is to stop it completely. Shorting works a bit like insurance – in the real world you can only insure what you own; here you are invited to insure another party in order to profit from someone else’s loss. So you could literally insure someone else’s house and you get a pay out if it burns down. The bank benefits from the fees and the premiums – especially if the failure is delayed or does not happen. This is basically how Satyajit Das describes the process in the documentary ‘Inside Job’ and Das wrote a text book on how to do the math on these.

Question: What might you do to get someone’ s house to burn down if you had a vested interest in it doing so?

Or if you were financially supporting a leading BREXITEER party because you’d purchased credit default swaps on companies who might fail because we’ve left Europe? So, because the finance sector plays by different rules because politicians haven’t the testicular material to stop them, the moral hazard of seeking to influence the outcome in favour of the shorting party is fully realised at the detriment of society.

It’s totally at odds with the idea of ‘investment banking’; it’s ‘divestment banking’. And it is more than morally dubious – it’s legalised plunder. And it’s got to be fucking stopped. Now.

I have to say that I enjoyed watching the GameStop thing that effectively called out the shorting.

I also had some sympathy (admiration even) for the guy living with his parents near Heathrow who was able to get a millisecond’s advantage over the City and profit from that.

In both cases it highlights the utter worthlessness of much of the financial markets.

Yes. High Frequency Trading (the modern version of “front running”) was made difficult for the big boys by the “spoofing” from the chap in Heathrow. They couldn’t let a him get in the way of their money making schemes. I have sympathy here, too.

However, the Squeeze in Gamestop is collusion and manipulation…. and wrong. It only appeals because the victims are even more horrible.

As a Government bond trader I can say that for most of my adult life I have been short some securities. It is an essential part of providing liquidity to clients. If a client calls and wants to buy $50mm of a particular government bond I will always make an offer even though I don’t have any in my inventory – that is what customers expect and want. Furthermore, I won’t even quote high (to avoid the trade) if I don’t have the bond – I want to give the client a fair market price and not tempt them to look elsewhere to trade. Consequently, I spend a lot of time short various bonds. How do I deliver if I don’t have them? Well, my Repo trader will borrow them to allow me to fulfil my obligation to deliver until I have bought the bonds back. The Repo market is huge and allows banks to lend money to one another without credit risk and other such good stuff.

I hope you would agree that me shorting government bonds is “part and parcel” of doing my job.

On the other hand. If I shorted stock in XYZ Corp and then put out a rumour that the CEO was cooking the books that would make me a bad person – indeed, it is illegal and I would go to jail. Equally, if I bought a stock with advanced knowledge of good results that would be bad and illegal.

So, shorting in itself is not wrong if it is helping create a good market place for legitimate users. What is wrong is market manipulation by shorts OR longs.

The difficulty is creating regulations that stop manipulation but allow legitimate activities….. and regulators have been grappling with this for a century or more and the rule book is very big…. but human ingenuity is amazing when there is a fast buck to be earned! It is hard to define manipulation “in advance” but we know it when we see it.

In this case, I think the ramp/squeeze orchestrated (yes, they colluded and manipulated) by the “little guys” is just as bad as the original “offence” or shorting and then bad mouthing the stock by Hedge funds. Nobody looks good and the ordinary investor rightly worries about the integrity of the whole system.

It gets even more complicated if you are ask “Are the shorters performing a public service?” – for example Muddy Waters (Research, not Blues legend) have exposed various frauds over the years by researching and shorting stocks. Look at Wirecard it took the combined efforts of shorters and jounalists to expose the fraud…. which was a good thing.

The REAL concern here is not the fate of a few hedge funds or Robinhood traders it was the risk of collapse of a broker and all the panic that would create. This raises questions about the ability to trade on margin, the excess cash in the system and so much more. Brokers compete on costs AND the amount to leverage they offer and this risks instability to the whole financial system. We might have made banks less risky but the shadow banking system is still a bit of a jungle….. and leads me back to one of my big themes – Credit Controls. It is not enough to control the price of credit through interest rate policy, we need a more granular approach that defines “productive” and “unproductive” lending and then regulates accordingly. BRING ON GREEN BONDS.

I agree with the last

And note what you say – which is what current market conditions require

But one question – for now – and that is how does anyone know that repo is actually based on real bonds? Is it really? Or is the promise that a bind might exist enough? And what in that case if the security was called upon? What then?

That is my fear in all this.

Not sure you understand what repo is if you are saying

“and that is how does anyone know that repo is actually based on real bonds? Is it really? Or is the promise that a bind might exist enough?”

I think I do

I am referring to collateral

And that is the basis of the repo market

There is a huge difference between the repo market for government bonds and the market for borrowing equities.

In bonds, the repo market is mainly about borrowing and lending CASH with the government bonds acting as collateral. They make good collateral because they are highly liquid and are of certain value on not very volatile. The repo trades motivated to borrow and lend BONDS to cover short positions is a relatively small part of the market and the whole show is watched by the Fed because any problems in the repo market are early warning signs of problems. You ask “what happens if the bonds I borrowed get called back?” – well, you get them somewhere else and if you can’t then you will fail to deliver. Indeed, one thing that the Fed watches out for is the level of “fails” in the market as an indicator of strain in the system…. and since they own large quantities of Treasuries they occasionally do become the “lender of last resort” for US Treasuries (as well as their traditional role in cash). Primary dealers in US Treasuries are nearly always net short USTs as they are routinely shorted to hedge the interest rate risk on their inventories of non-government securities. Overall, the system works well, I think…… partly because it is a rather small dealer community where the traders all know each other and there is relationship beyond the next trade.

Stocks is a different story (and one where my knowledge is less extensive).

The first thing to note is that stocks make poor collateral for lending. Not only are they volatile, the level of volatility and market direction are highly correlated to the possibility of you having to exercise your right to seize and liquidate the collateral. (Lehman did not go bust in a climate of steadily rising stock prices). Consequently, all the “repo” in stocks is about covering short positions with no real other underlying raison d’etre. The problems of short selling are long standing and various rules try to prevent abuse; eg. you can’t sell a stock short unless you have actually borrowed the stock. etc. But as a short seller you are very much at the mercy of the stock lending institution and there are a lot of games played to make life uncomfortable for the shorts. All part of the fun.

I was talking bonds / gilts only

Thanks

My point is that I suspect the scale of supposed collateral is much bigger than the actual quantity of bonds available

“and that is how does anyone know that repo is actually based on real bonds? Is it really? Or is the promise that a bind might exist enough?”

This statement reads as if you think that repo’d bonds doesn’t actually have to be delivered, or some sort of promise will do instead. Repo contracts reference real securities and are contractual obligations to deliver.

When you are short a bond, you have to deliver that specific security. When you borrow it through the repo market, you are borrowing that specific security, and you have a contract for delivery of those specific bonds. Not some other security or some vague promise.

When you talk about collateral, that is the other side of the repo market. When you are long bonds, you can lend them as “GC” or general collateral for cash. The amount of cash will be dependent on the security itself – there will normally be a haircut to represent the risk of that security.

So government bonds have essentially no haircut, whilst qualifying listed equities will have a much larger one.

Otherwise, the bond and equity market repo are very similar. Shorts have to cover/borrow specific securities in exchange for lending cash, longs can lend general securities for cash. But the contracts are for specific securities with specified delivery dates on both ends of the deal.

Still doesn’t change the fact that short sellers still have to deliver stock they don’t own, are forced to borrow it and so can easily get caught by short squeezes as currently being witnessed in small cap stocks.

I take your point

I would add that I have read quite a lot of academic commentary that says these bonds are borrowed and used more than once

I was asking whether that is true or not

And if so, what happens if the overnight market is bigger than the available gilts, as QE makes possible?

Or is that why the ECB is lending repurchased bonds out again?

These are real questions, based on concerns I have seen expressed

I do not claim to be greatly knowledgable on the actual operations of repo, because I am not

“I would add that I have read quite a lot of academic commentary that says these bonds are borrowed and used more than once”

This happens all the time, but there is nothing suspicious about it. Normally market makers keep very little inventory, to minimize balance sheet costs. So when a customer buys a Gilt from them, they will go borrow that in the repo market to cover. Then another customer sells bonds to the market maker, and he is now net flat in his position, but long in the repo. So he will lend those bonds he borrowed back out again.

What repo doesn’t enable financial institutions to do is leverage up the scale of the positions, just the cash liquidity. I.e. you can lend the same bonds multiple times, but then just end up needing to borrow them in exactly the same size.

“And if so, what happens if the overnight market is bigger than the available gilts, as QE makes possible?”

Given there are net positive amounts of a particular security, or securities in general, you start with a net positive amount outstanding. Cash is also normally in plentiful supply, so for someone to be net short significant percentages of a given security is rare. Maybe 1-2% of a given bond issue, maybe 5% tops for liquid large cap stocks.

You only get weird situations in small caps when the market get more than 100% short a stock because of a peculiarity of the calculation and margin system, meaning the market is effectively more than 100% short a stock but actual outstanding shorts will be less than 100%. Sometimes through derivatives as well, but they are cash settled so don’t affect the supply of the underlying security directly.

“Or is that why the ECB is lending repurchased bonds out again?”

It’s just a way for banks to place excess reserves back with the ECB at less penal rates than the huge negative rates they are charging.

“These are real questions, based on concerns I have seen expressed”

People shouldn’t be concerned about short selling. It simply isn’t the danger people claim. It is near impossible for even groups to drive the price of a security down too much through short selling alone – not least because having to borrow increasingly expensive and scarce paper acts as an in built short circuit mechanism. Shorts can get squeezed out far far more easily than long positions, which can last indefinitely. Shorting is also pretty expensive to fund – you are paying both the cost of the return on the security AND the cost of financing the trade itself. Short positions are almost always quite short term i nature, simply because of the cost of holding them.

I would actually go as far as to say that banning short selling is the most short sighted thing a regulator can do. Firstly, it is a sure fire sign of weakness, which tends to make long positions head for the exit. It also means that in any market distress there is no natural demand to buy a security, which means forced sellers keep driving the price lower forcing others to cut losses and sell. With short positions around, you at least have some people actively looking to buy at lower prices. This is the kind of thing that happened in the GFC in 08 with the PIGS bonds. Shorting was banned and it set off a doom loop.

Noted

Unlike Clive Parry you do not reassure me

@Tom,

You make some valid points about the benefits of short-selling, particularly when governments and companies are trying to project and sustain optical illusions – whether with good or malign intent. Your example of the PIG bonds in the aftermath of the GFC is particularly apposite. In May 2009 Mrs. Merkel went on a solo run in an attempt to bring the hedgies, vampire squids and disaster capitalists to heel by trying to outlaw naked short-selling. Their fury was unlimited and the spreads on vulnerable sovereign bonds increased. Furher political missteps and the failure by the ECB to intervene effectively resulted in Ireland, Portugal and Greece losing their economic sovereignty in 2010. Eventually Mario Draghi secured sufficient political support to declare he would “do what it takes” to protect the Euro in 2012.

I would argue that short-selling forced the EU authorities to take the necessary steps to remedy fundamental structural failings of the Euro System. Without this, the politicians would have tried to keep kicking the can down the road indefinitely. Of course, it would be far better if we didn’t have to rely on short-selling to achieve this, but it was ultimately in the broad public interest that the dysfunction was highlighted and, eventually, tackled, when politicians and policy-makers initially refused to do their jobs.

I will struggle to agree with that

I suspect it was on the ground politics that forced change

The thread has got a little mixed up but I’ll try to answer some of the questions posed:

@ John S Warren

“but has the advantage of requiring a return for little effort; it comes to you, with the offer of a free lunch.”

Not sure this is the case. It is a lot harder to make money from short than longs, because of the costs and liquidity risks involved. You could also say buying an asset which goes up in price is also a free lunch by the same logic. The risks of going long or going short are mostly symmetrical, with an edge in favour of long.

“however how the wider risks from a broader, responsible perspective to stability, and to liquidity; and ‘moral hazard’”

Other than the slightly dubious moral case of profiting when something fails, I’m not sure there are any other real arguments against shorting. There are very few cases (if any) where short positions alone have driven an otherwise sound asset into failure. I can’t think of any off the top of my head. There are quite a few cases where short sellers exposed problems with issues that hadn’t otherwise been noticed (Worldpay, Enron) or simply got involved when the assets in question were already circling the drain.

If anything, at the moment short sellers and the hedge funds that do it had an awful time over the last few years. It’s very niche and very difficult to do well.

“Is there some quantitative technique of Bayesian probability invoked (and how could that plausibly be done)?”

Yes, there are a lot of risk metrics which are measured, normally based on volatility. But bear in mind that these work both ways, so long positions have exactly the same risks as short positions in terms of how much money you can make or lose, so are regulated in similar ways. With the caveat that shorting can lose you an unlimited amount.

“I am also a little surprised to hear how profitable it is for pension funds. I was not aware that returns on pension fund investments for pension funds were dazzling in recent years; or, is the logic of this; that this is the kind of activity required for a decent pension fund ROI to be made?”

It goes back to what I was saying in an earlier post. Shorting really has two functions for a pension fund. The first is liquidity management, with a sidebar in some fees for doing so. Lending stock to smooth cashflows.

The second is risk management. Let me explain. Let’s say you are a pension fund which is only allowed to go long. You own shares in Bank A, because you think they will outperform. The whole market goes up 10%, Bank A 11%. Great! It goes down 10%, Bank A 9%. Not so great.

Now let’s say you can short Bank B shares against Bank A. Markets goes up 10%. Bank A 11%, Bank B 9%. Fund makes 2%. Not so great, but still OK. Market goes down 10%. Bank A goes down 9%, Bank B 11%. Fund still makes 2%. Great result when the market as a whole is down 10%.

This is the reason most pension funds take some short positions (through their asset managers). It is to run their portfolios on a relative value, market neutral basis. It reduces risk, catastrophic loss chances and volatility of returns at the cost of reducing the outright return. Which for a pension fund is very important. Smaller, less risky, smoother returns are far better for pensions fund management than larger more volatile ones.

They do this with interest rates as well, with the short position coming from their liabilities rather than actually shorting bonds.

And on the whole it works. Pension funds have managed to weather both this Covid related crisis and the 2008 financial crisis with minimal damage to their funding positions, which would no have been the case if they were long only.

I go as far as to say the vast bulk of short positions held across all arms of the financial are held on a relative value/hedging basis. I.e. the owner of the short position has a corresponding long in another asset – often even issued by the same entity (short 2 year bonds vs long 10 years bonds in the same name, for example). Outright shorting is simply not that common

@ Vince Richardson

“Manipulation is another thing altogether, shorting gets a bad name because of manipulation part ,it has to be allowed otherwise its not a free market.”

I’d agree – but add that manipulation can also happen when people are long assets. You could argue what is going on in Gamestop shares at the moment is manipulation as coordination to drives prices higher could also be described as price manipulation.

@ Paul Hunt

“I have one dumb question. Why do fund managers lend shares to short-sellers when they know that, if the short-sellers are successful, their value will be reduced when they get them back?”

Lot’s of reasons, including the one you provide – tends to be small, tends to be a minimal effect on the overall value of a portfolio.

I mentioned liquidity and the fees raised for lending as well, but it is also worth nothing that different investors have very different time horizons as well.

For example, short sellers tend to be shorter term traders, because of the costs involved. So they might take a short to try and benefit from a view that a company will have poor results this quarter. A long term institutional investor will probably have a time horizon lasting in years or even decades, so this quarters results for a company is basically just noise, and they are looking at the long term outlook.

“In May 2009 Mrs. Merkel went on a solo run in an attempt to bring the hedgies, vampire squids and disaster capitalists to heel by trying to outlaw naked short-selling. Their fury was unlimited and the spreads on vulnerable sovereign bonds increased.”

The funny thing about this one was that by the time the EU banned short selling in PIGS bonds, almost nobody was short, and they were still collapsing in price. The HFs who were short had already taken profit, and had slowed the collapse down by buying when nobody else would. Most took profit way too early, having suffered losses on the trade for so long when spreads to Germany were static or even tightened, and were just happy to get out with any kind of result.

The short ban then made all the institutional investors panic and they started to offload their long positions into a market with no buyers, which started the whole thing off again.

The EU then compound their error by banning short CDS trades (an insurance derivative designed to protect against bond losses). Only problem being that if you can’t go short a CDS, nobody can be long either. The insto’s were long PIGS bonds but had also bought CDS to protect against losses on those bonds. But now the banks were banned from being short CDS, so couldn’t issue more and were forced to cover those CDS shorts. Which meant the institutional investors no longer could no longer insure their PIGS bonds, and were forced into selling even more of them.

From memory, all the HFs were out of the trade by the time Greek bonds hits 10-11%. Not least because if you are short, you are the one paying that 10-11% to fund the trade. It just gets too expensive to be short after a while. They ended up hitting 35% for perspective – which was nothing to do with the HFs or any short selling. It was longs trying to exit positions into a falling market with no buyers.

Basically, by banning shorting thinking that evil short sellers were the reason behind falling bond prices rather than the fundamental reason – that the PIGS were heading towards bankruptcy, they actually made the problem far worse than it otherwise would have been.

Thanks, Tam for your detailed consideration of the points I raised. I remain uneasy when you referred to “the caveat that shorting can lose you an unlimited amount.” My concern is the chain-reaction that this may tigger if this activity proves not to be small or peripheral.

Your concern is well placed

@ John S Warren

No problem.

I should probably not have used a turn of phrase when I said that shorting can lose you an unlimited amount. In theory it can, as an asset price could go to an infinitely high price, but in reality asset prices tend only to go so high or low in a given timeframe and margin calls will stop people out of positions well before.

In practice, you can lose all the money you have by being short. But that can happen by being long as well, so I don’t think there is a huge difference.

In the end, I don’t think short selling is anything to be particularly worried about. Market manipulation is, but that happens to drive up asset prices just as much if not more. Short selling does get a bad reputation as people make a moral judgement on profiting when something is failing – but without it things would almost certainly be worse, with more volatile markets and investments. It might sound a bit grubby, but it fulfills a useful and important purpose.

My issue is a simple one

Why not require that people own the assets they deal in?

@Tom,

Many thanks for your detailed and considered response.

I think we’ve all had very useful, productive and informative exchanges here.

However, with the finance and real estate sectors (plus the Tech Titans and some ‘super star’ firms) dominating capitalism in the western advanced economies, we have major challenges with the governance of capitalism. I fear most on the progressive-left aren’t up to the job, because their is an instinctive affection for statist solutions and instinctive desire to overthrow, supplant, suppress or supercede capitalism.

In any event, the number of voters isn’t there. A majority of voters are in the contented comfortable classes and they have a material interest in the economy that extends beyond their jobs to include property, pensions and investments. They will not vote for any party which will pose the slightest threat to the economic rents they have accumulated in these.

They would, if they could, but FPTP does nit let them

And, you ignore the impact of climate change and other events, inciuding Covid, which may have a long way to go as yet

First, to Tam, apologies for calling you Tom. I’m very grateful for your contributions on this thread.

Second, to Richard, on the barrier FPTP poses to the progressive-left, it is only one of many barriers that exist. Focusing on this is similar to saying “We can’t beat you at Rugby Union, so we’ll switch to Association Football to decide our contests from now on.” And it ain’t going to happen. Labour had its chance in 2011, but bottled it.

But the Tories would beat Labour under any code, mainly because of their own attributes which have maintained them as the longest-lasting party in the established democracies, but also because the Lib Dems (with around 4 million votes) keep queering the pitch. And then we have the nationalists, the anti-capitalist, anti-western left, climate fantasists and extremists and purveyors of identity politics who repel large swathes of the voting public. The Tories can keep an even more inchoate, disparate and fractious number of factions within its tent, bit the left is like a centrifuge.

The best we can hope for is enough of an opposition than can impose some scrutiny, restraint and accountability.

Tam,

You argue that the unlimited downside is only ‘theoretical’, but I will take some convincing that your are describing a risk Bell curve; that the real risk is the same on both sides.

Thank you for this explanation which helps to clarify the distinctions around when it comes to (1) ‘being short’ when making a commitment to effect a trade, (2) ‘short-selling’ when the objective is to make a profit by exposing an unjustified overvaluation of an asset and (3) ‘short-selling’ as an exercise in market manipulation.

I’m always uneasy about bans of activities that in many instances can generate benefits but can also cause harm, because it tends to drive out the participants generating benefits and drive those causing harm underground where they escape regulation.

I have one dumb question. Why do fund managers lend shares to short-sellers when they know that, if the short-sellers are successful, their value will be reduced when they get them back? I know they make money that they can pocket from lending them, but surely the value of the portfolios they are managing will fall. Is it because the initial value of the shares they are lending tends to comprise such a small share of the portfolio that the drop in value is disguised by movements in the prices of other assets in the portfolio?

Apologies for the dumb question. Please feel free to ignore it.

That’s not dumb

It’s inexplicable to those who stand back and take the big view

Thank you, Richard. I was also hoping for some input from practitioners on the board, such as Mr. Parry.

“The first thing to note is that stocks make poor collateral for lending. Not only are they volatile, the level of volatility and market direction are highly correlated to the possibility of you having to exercise your right to seize and liquidate the collateral. (Lehman did not go bust in a climate of steadily rising stock prices). Consequently, all the “repo” in stocks is about covering short positions with no real other underlying raison d’etre. The problems of short selling are long standing and various rules try to prevent abuse; eg. you can’t sell a stock short unless you have actually borrowed the stock. etc.”

The real test of stocks/shares operations here is the capacity of the borrower to cover the short position. If the borrower does not have the resources to cover the short position it should not be possible to do it; I suspect the downside risk here could begin chain-reactions to the whole system that other trades do not cause. This is just a casino operation (but I doubt if a player would ever be given the credit required for some ‘short’ positions in a casino), but institutional ‘short’ borrowers are given special ‘money’ prerogatives because this casino comes dressed seductively as if it was a cathedral of financial probity. It is time to crack-down on ‘shorting’, but of course we are largely governed in so-called ‘free market’ states by the craven creatures who bow the knee to this wanton activity.

If someone wishes to defend ‘shorting’, please explain the real improvement to economic stability and the real benefits to the community that is provided by stock shorting?

The lender of last resort is close at hand for bonds, and the structure of bond trading seems to create a completely different environment. What you have described very well on this thread Mr Parry, and only highlighted by recent events on Wall Street is something that, if unchecked, is the road to perdition.

(I really should temper my resort to religious analogies, but they now seem so appropriate).

As a bond trader, I tend to agree that the stock market is a casino…… but it is probably the “sour grapes” of an old fashioned government bond trader watching the equity traders having more fun and making more money.

But seriously, the argument in favour of shorting is that it improves market liquidity. If I want to buy a stock I don’t want to have to wait days for a seller to show up. Shorting as part of market making and liquidity provision is, in my view, a good thing.

“Naked” short selling (where you sell hard without having borrowed the stock in the hope that the violent down move in price will panic other stockholders into selling) has no benefit to anyone.

Where the border lies between “good” and “bad” short selling has filled a rule book about 30cm thick… and still not answered the question.

John,

Pension funds who are long only lend stock all the time. Partly to earn a bit through the fees generated, but more often than not to manage liquidity. Pension funds don’t get their interest and dividend payments in at the same time as they pay out the monthly distribution to pensioners, and often the most cost effective way to bridge the gap is just to lend things out through the repo. Much more cost effective than liquidating investments then having to re-buy them a few days later just because you have a cashflow mismatch.

I’d also note that most hedge funds are not directional. They don’t actively go long or short the market in any great size. What they do is take a group of stocks they think will outperform the market, and go long them. Then as a hedge, they take a group of similar stocks they think will underperform, and go short them. Long Bank A vs short Bank B.

I don’t think there is anything wrong with this type of value investing, not least because it tends to be less risky for the investor – but you do need the ability to go short to invest in this manner. This type of investing adds great value to pension fund long term type investors as it adds greatly to the diversification of their portfolios, so typically in a market crash a someone invested in such a way will suffer much less downside.

I’ve mentioned other reasons why shorting is useful in a post to Richard above.

I see massive piles of risk that will eventually be borne by society when things fail

Do I see unacceptable risk as a result?

Yes, bluntly

You see profit

I see moral hazard

Who is right? Me, because I have no skin in the game and you clearly do

Yes, I can see there may be some improved liquidity, from the perspective of the lender most of all; and it may require som due diligence, but has the advantage of requiring a return for little effort; it comes to you, with the offer of a free lunch. I need to know, however how the wider risks from a broader, responsible perspective to stability, and to liquidity; and ‘moral hazard’ (in market and wider society terms) are reconciled. From the persepective of the impartial spectator – in the form of a wise regulator (okay that stretches credibility given Britain’s track record, but allow me a little slack, and imagine it). Is there some quantitative technique of Bayesian probability invoked (and how could that plausibly be done)?

I am still struggling to see much beyond a lot of market and social risk for insufficiently reliable or secure returns. There are some risks that may be of low probability, but which are catastrophic and irrecoverable if they happen. Furthermore I am not sure that ‘shorting’ risks are low probability; the profits are huge, but so are the losses, and these are very hard even to quantify ‘a priori’. I find this grotesque; something that should never have passed muster in the first place. I do not see that kind of risk profile in principle to be a form of business, but rather as simple gambling. If you are going to gamble, use your own money – up front.

I am also a little surprised to hear how profitable it is for pension funds. I was not aware that returns on pension fund investments for pension funds were dazzling in recent years; or, is the logic of this; that this is the kind of activity required for a decent pension fund ROI to be made?

Finally, I have never understood why the separation of activities between institutions in the financial sector (for example retail and investment banking, but the same principle is relevant throughout the financial sector) was ever terminated, and replaced – for example – by the strange device of ‘chinese walls’, as they used to be called; I never thought the proposition either convincing or satisfactory; on the simple principle that for justice to be done it must be seen to be done. You cannot see a ‘chinese wall’ (and I speak as someone who has walked on the Great Wall of China, so I know what a Chinese wall should look like).

I would have though that in the 21st century, when ‘money’ is essentially an abstraction represented by a keyboard entry, supended in the imponderable ether, the separation of institutional financial powers is even more important to the health of the community than when it was first instituted, mainly after the 1929 crash; and dismantled by neoliberalism, solely for ideological reasons. This comment may seem to stray rather far from the issue of ‘shorting’, but I think it goes to the root of the matter of inadequate regulation. Unregulated markets are never free; and we pay a heavy price for indulging them.

The Big Bang was a disaster

Clive,

“So, shorting in itself is not wrong if it is helping create a good market place for legitimate users. What is wrong is market manipulation by shorts OR longs.”

I tend to agree with this. This is what a functioning market does ,it makes educated guesses. Manipulation is another thing altogether, shorting gets a bad name because of manipulation part ,it has to be allowed otherwise its not a free market.

Best example is the 2008 housing crisis where several very smart traders shorted the US real estate business as well as every bank that had an association with real estate or derivative products based on mortgages ,they made billions after being ridiculed at the time. A few saw what the many misunderstood. There is nothing wrong with that kind of short selling in my view.

I always like Warren Buffets comment about derivatives,(but I’d say it applies to short selling) if two men shake hands in a room on a deal and one of them doesn’t understand what he has agreed to then more fool him.

Taking a short position is just as much a gamble as taking a long position, albeit with limited upside and unlimited downside. Any sensible person has a stop-loss, and settles their exposed position before they become bankrupt.

And of course markets must be regulated to prevent abuse. There is no such thing as a free market really: a market does not exist without common rules of business.

What concerns me about shorting, certainly with shares is that you are in effect creating profit out of borrowed money or stock with all the down sides it brings with it.

Its worth pointing out that Usury was banned or restricted by the three Abrahamic Faiths because they realised that somebody could end up with all the money – literally in those days by doing no more than making money out of money rather than constructive activity. Possibly it is an idea we need to revisit.

To the direct question – is the collateral pool large enough to support all the collateralised lending that takes place? – then the answer is yes – certainly in the US. Most dealers clear through BoNY (Bank of New York) and the collateral what is pledged is actually delivered and all trades are Delivery versus Payment DVP to ensure no credit exposure.

The clearer and “see through” any potential snarl-ups. Eg. A sells to B who sells to C who then sells to A again. A cannot deliver to B until they get the bonds from C…. who is waiting on B who is waiting on A. Dealers also hold sufficient excess collateral to allow this to happen risklessly. The Fed have done a lot of work on this in the last few years and I think the system is pretty sound.

In the UK, I can’t imagine it would be different.

OK, the academic concerns that have worried me are misplaced

I am reassured

Why do fund managers lend bonds/shares? They get fees for doing so and investors benefit from the extra income. Sure, it does allow speculators to go short…. and that might drive the price lower……but in the end, shorts must cover at some point….. and that will drive the price back up. If I were to sell USD 1bn 10year notes in the US Treasury market the price would drop a bit. If I then bought them back straight away the price would rise….. and it would end up higher than it started and I would have made a loss in the process, almost certainly. In the long run, short selling does not impact the price…. but the income earned from stock lending is real.

Even if wholly true, what is its point? It turns money itself into the primary purpose of all economic activity; skip the difficult bit, and just concentrate on money; in spite of the fact that money is there to primarily to enable economic activity not become the primary economic activity.

The deeper irony is that the ideology responsible for driving this emphasis on money itself as primary, is neoliberalism; which of course makes the fundamental claim that money is not a real economic activity at all; for neoliberalism, you strip the veil of money from the activity, and the real economic activity is barter.

It is not an accident that the antroplogical roots of money is found in religion; because it understand the nature of ‘absolute value’ and the reverence required to ensure it is not sullied. Essentially stock shorting, which monumentally increases risk is precisely the operation that money should not be allowed to engage in.

Maybe this is a daft question but could the liquidity Clive talks about being provided in the repo market not be provided by the government just taking back the bonds? …I.e. making government bonds non-tradeable. That seems to me be the simple solution and dispenses with the need for an ever growing raft of regulations of a secondary market. Sorry if this woild put you out of a job Clive and others but then there are lots more useful things we need to get done with our human resources.

The issue repo addresses is the lack of trust in banks. Large depositors do not have a government guarantee on their funds, gilts are bought and sold instead to meet this need for security. So making them non traceable would not help.

But if there was always the ability to return them to the government then the security is provided – that’s what a I meant by “non-tradeable”. It would mean government bonds no longer have a maturity date as they could be redeemed at any time. I am not asserting this is a solution, I am just asking if it might be…..stupid questions sometimes turn out not to be so stupid after all so I am just “testing the water”.

But that would not suit the government at all – leaving it at the whim of market rates

Not a good idea at all…

Absolutely – the VAST majority (95%+ ??) of trades are “General Collateral” meaning I don’t care what government bonds you send me. If I need to borrow a bond (to fulfil delivery to a client of a bond I don’t own) then I need to specify exactly which bond and that is called the “Special” Repo market. It is more interesting than the GC market but in terms of volumes it is far, far smaller. USD repo is a huge market, most trades are just “overnight” with typical volumes of USD1 trillion a day. It is so important to the smooth running of the financial system that the Fed is all over it to ensure there are no problems or abuses.

In 2008 the market stood up very well even though Lehman Brothers was a very big participant in the market (indeed, that part of Lehman’s business was bought by Barclays). Since then, the Fed has further strengthened the market’s robustness and integrity.

So, my message is – Government Bond Repo is a good, important and well regulated market.

Clive

What is the UK volume?

And who really owns the bonds used?

Richard

Mr Parry,

“In 2008 the market stood up very well even though Lehman Brothers was a very big participant in the market (indeed, that part of Lehman’s business was bought by Barclays).”

In 2008 I am not sure “the market stood up very well” quite does it. Indeed, the ‘stress testing’ requires to become more and more elaborate just to keep pace with the efforts to circumvent the rules. Why? Presumably because this dangerous activity is indulged; not in the best interests of the stability of money, or even the system; but because it so profitable, feeds those who do well from it and facilitates a certain kind of activity (worthwhile or not); the fact that in consequence we face endless cycles of boom, bust and crash is just the price we must pay for having this ‘best of all possible worlds’.

It may be the case that it can be justified in a closely supervised bond trading environment (I bow to your knowledge) but am sceptical about stocks and shares. I do not write this in any expectation that it makes the slightest difference; but I do think it worth making the observation.

I agree with you

My fear is that what is actually happening is akin to fractional reserve banking with too little capital base

But that is just an instinct

I mean that the REPO markets (not stock markets) stood up well despite the failure of one of its central trading firms. Everyone who had lent money to Lehman against UST collateral did not lose a penny. Indeed, the smooth continuous operation of the repo market at that time was what prevented a worse crisis. My friend ran the repo department for a large US broker dealer in London during the crisis (and just recently retired). She was called by the CEO from NY every hour to find out whether his firm was going to go bust and it was her ability to maximise money borrowed from the collateral available that saved the day. This was in stark contrast to 1987 when the ability to trade and finance really dried up.

I like to draw a real distinction between bond repo and the stock market. The fun and games in Gamestop have little systemic implications and frankly, I am tempted to just stand back and watch the show. All that really matters is that the brokers and clearers have taken action to protect themselves (mainly limiting positions and making sure they have enough collateral) so the the game is between consenting adults and there will be no “collateral damage” if you will excuse the pun.

The bond repo market is critical and market abuse in Government bond markets gets you shut down…. think of Salomon Brothers – the biggest bond trading house in the world put out of business for trying to corner a Treasury auction.

Thanks, Tom and Clive. I, for one, am getting an education. I thought I knew something about stock markets worked.

For the best education watch the last few minutes of the movie Trading Places…….

*how stock markets worked.

Some years ago Adair Turner made the “socially useless” comment about much of what banks do. The other day we were discussing “Green Bonds” for Socially Useful purposes.

Perhaps we need to apply that metric more often to finance and banking. Would the world end if we put a stop to some of the more casino-like behaviours?

I like it

…. the other quote I like is from Paul Volker “the only useful thing that the banks have invented in the last 20 years is the ATM”.

You are right – and I have said it before on this blog – we can’t rely on the price (interest rate) to control borrowing. We need more than just an assessment of monetary risk/reward to determine whether money is lent. We need Credit Controls that differentiate between (say) (i) margin lending to speculate (which is safe, profitable but not useful); (ii) mortgage lending (safe, moderately profitable and useful…in the right quantities) and (iii) lending to real business (risky, time consuming but desperately needed for a vibrant economy).

This also links in with Richard’s observation that The Big Bang was a disaster (deregulation of finance, not the start of the Universe). I have mixed feelings about it as I would never have been able to join the pre-big bang industry as I went to the wrong school. But, what it did was fly in the face of 3,000 years of financial wisdom – that different functions in the system have to be separated to avoid conflicts of interest and that the whole system needs tight State supervision. Most of our problems have these issues, at their heart. But more than that – if you separate the functions out then you have the ability to regulate in a much more granular way. For instance, if residential mortgages remained the province of Building Societies you could cool the housing market by imposing restrictions in this sector without damaging business lending conducted by Commercial banks.

That was the way in which I meant it a disaster

The end of City privilege on access was good news

I completely agree with that. I think you are right about the social aspiration of Big Bang, but I saw a change in culture that is not the better for being an unintended consequence of a blunder we are still paying for. Big Bang incidentally destroyed the separate and highly reputable Scottish banking sector; they became simply part of the City of London banking world and because they were smaller had to embrace that culture to survive; either as predator (RBS) or prey (BofS), and they were not, in my opinion (see the Crash 2007-8) the better for it; nor were other banks – whose greatest triumph was created BY the Crash – they really are ‘too big to fail’. They are indispensable and impregnable, with little real, substantive responsibility for their actions.

The crash reflected the culture of Big Bang. It also effectively destroyed the great Mutual Fund financial institutions, in which Scotland had established a wonderful tradition (the ‘Jewel in the Crown’, the TSB is now just another bank). What we have is one corporate template fits all; now it is just a matter of what is done online (another disastrous blunder in the relentless march of Surveillance Capitalism).

I think outstanding amounts (not traded volumes) are about GBP 400bn. The vast bulk of these will represent banks pledging their gilt holding to borrow money. (Little reason for pension funds to borrow money against their gilt holdings.) Banks (or “Monetary Institutions” is the categorisation the DMO/ONS uses) own about GBP 800bn.

I think this confirms that this is not a “shell game” and that there is plenty of collateral to support all the Repo activity there is.

It can be disconcerting to think that when I borrow cash and deliver my collateral that the bank will then go out and borrow using “my” collateral as “their” collateral but it does all make sense and it does work. Just think of the system as a huge array of pigeon holes where every time money moves from one pigeon hole (Barclays) to another (Lloyds) gilts of equal value move in the opposite direction…. all over seen by the the person moving the money/securities.

I am nit convinced of that holding figure. The House of Commons library suggests the £800bn includes all financial institutions, and banks would be somewhat less than £400bn – maybe somewhat less than £300bn. So I am not convinced as yet that gilts are not being borrowed fur this purpose.

Other categories include Pension funds, Insurance Co.s and other financial institutions So, I think Monetary Fionancial Institutions are basically Banks.

The European Central Bank define MFIs as…”central banks, resident credit institutions as defined in Community Law, and other resident financial institutions whose business is to take deposits or close substitutes for deposits from entities other than MFIs and, for their own account (at least in economic terms), to grant credits and/or make investments in securities. Money market funds are also classified as MFIs.”…. in a word – Banks

So, I think in broad terms 800bn is held by banks.

Also, there will be quite a lot of reverse repos from the Pension/Insurance sector. Banks hold gilts for regulatory reasons but these are usually fairly short maturities. On the trading side dealers are typically always short of government bonds in long maturities. The gilt book will, on average be flat but the corporate bond book will nearly always be net long so it requires hedging which means being short gilts. What happens is that Insurers and Pension funds will allow gilt dealers to “cherry pick” the issues they need to cover their short positions and post their long positions as collateral…. and pay a fee for doing it.

I think there are a lot of think in finance to worry about but the government bond and repo markets are the least of our worries.

Clive

That is completely impossible

Last year overseas had £400bn, pensions funds more than and life assurance well over £500bn, that Bank of England around £400bn and there were only £1,600bn in issue. Data here. https://commonslibrary.parliament.uk/coronavirus-government-debt-an-explainer/ and banks were not all that £300bn.

So banks own very much less than £800bn. I would be surprised it it is £200bn

Hence why my incomprehension at how repo works here

Richard,

I see Mr Parry’s point. My way of expressing that is to ask for a watertight definition of a ‘bank’. It is very hard to provide one. In the 2007-8 crash one of the problems, as I understand it was the way banks in the US effectively were looking to insurance to cover their risk, without anyone noticing the bigger ‘risk’ profile this created. I stand to be corrected.

Dean Baker takes a relaxed view, he says whilst most of the stock market is “wasteful” it is just a form of gambling, which the govt allows, so juts tax it ,then at least the gov t gets a share.

https://rwer.wordpress.com/2021/01/29/the-gamestop-game-and-financial-transactions-taxes/

I’m not sure I follow your argument that government would be at the whim of the markets Richard. I thought a

sovereign government with its own currency can set whatever interest it wants on its bonds.

That is, in my opinion, achieved through control of gilts and now central bank reserve accounts. It does not happen by whim alone. That is my point

Sorry, silly error on my part…. I just pulled the data off the DMO website. It seems they have included BoE holdings under MFIs….. so, yes, your GBP200bn is about right. (What’s 600bn between friends?!)

Is your concern that banks are borrowing money and saying “don’t worry, I have set aside collateral for you in case I go bust, trust me it IS in the vault with your name on it”…. and then pledging the same collateral to another lender?

And, are then then looking at the data and saying how can the banks that own only £200bn have positions of £400bn? Are they pledging collateral twice?

If this is your concern then rest easy! Collateral is delivered and ownership rights are transferred to the lender of cash (although the “economics” of owning the bond still lie with the borrower of cash) which means that in the event of default there is no problems seizing collateral – it is already in your account. If it’s in your account you can sell it. Actual delivery of collateral is the key.

So, how do we get 400 as a “market size” with only 200 in collateral? Well, if A lends £200 cash to B who lends £200 cash to C then £200 in collateral will go from C to B and then to A. Just £200 in collateral but outstanding transactions of £400.

Also, as a footnote the data on holdings is NET. (You can see negative numbers in 2005 to 2007 as banks held the fewest gilts possible on the “banking book” and ran substantial short positions on their trading book). So in this case they would reverse repo in the bonds they were short of for hedging purposes and repo out their long positions……. all counted in market data when the numbers say they have no gilts!

I am going to have to think about that

You have nit allayed my concern, so far

Yes, there are long chains of transactions where A sells to B who sells to C and on and on…… but at each stage there is ALWAYS an exchange of cash for securities. The value of the securities always matches the value of the cash and the process is done by the clearer who does ensure that both sides (cash and bonds) actually move simultaneously.

Outside of Government bonds there there is CLS for foreign exchange which eliminates “Herstatt risk” (delivering EUR in Europe and not getting your dollar in NY).

But the main work since 2008 has been in derivatives. Unwinding the Lehman swap book was a mess so now, most derivative trades between dealers settle with Central Clearing Counterparties to reduce risk…. with cash collateral being moved daily to reflect mark-to-market risks. (complex derivatives and Credit default swaps still tend to be done bilaterally but there is some progress there to reduce risks).

Since 2008 banks have about 3 times as much capital as they did before (for a particular level of risk) and regulators are far better at assigning risk levels to different products. Banks are are far more liquid – the key requirement being that they must be able to survive without access to interbank borrowing for a month. The settlements system is much more robust and means that a default is highly unlikely to set off the dominoes.

Not glamorous stuff but it has made our financial system much safer.

OK

But that does not explain how there is a bigger market than there are gilts available

Where do the rest come from?

This is beginning to sound like fractional reserve banking.

It is the way you count the trades.

A lends cash to B, B lends to C. Cash goes from A to B to C; collateral goes from C to B to A. Just one piece of collateral worth say £1.

The BoE surveys the dealers and asks (1) what amount of repo do you have outstanding (out)? (2) what amount of repo do you have outstanding (in)? (see link below)

https://www.bankofengland.co.uk/boeapps/database/index.asp?Travel=NIxSTxTDx&levels=2&XNotes=Y&B7537XNode7438.x=15&B7537XNode7438.y=11&Nodes=X7438X7504X7537X70129X70250&SectionRequired=D&HideNums=-1&ExtraInfo=false#BM

So, A answers ‘0 and 1’, B answers ‘1 and 1’, C answer ‘1 and 0’ to give an aggregate answer of 2 to each question…. even though there is only £1 of underlying collateral.

So, is anyone at risk? No. A has given out cash and holds the collateral; B is flat (no cash or collateral); C has cash but has given out collateral.

So, if that’s true, is this any way to run a banking system?

It was almost unknown pre 2000 so the answer has in principle to be no

sorry – I genuinely don’t understand what your concern is. Banks borrow and lend money and take/give collateral to make the system more secure. What do you propose?

It has been done like this in the US (give or take a few tweaks – quite big ones since 2008) since I have been involved (1985). In the UK we used be much more lax about things because there was a belief that banks did not fail so people were a lot happier to lend unsecured – particularly to clearing banks. That has changed hence the much greater use of collateral in lending.

So, my question is, might there be a better way than this to achieve security?

Given no one planned this use for gilts is it the best that can be done?

This is deeply opaque. I am not criticising, but that you got market data wrong suggests that is the case. So what could be better?

You are discussing bonds, and perhaps these trades are sufficiently closely monitored to ensure the collateral is not outstripped by the lending. In equities who can say the same. How could all these chains of collateral be checked and acted on; who is doing the audits, in real time in the 21st century keyboard world?

I am not convinced that they are

Hence my concerns

Yes, I did pull out the wrong data – sorry for that. But I don’t think that data is really telling us anything useful.

I guess the first thing to observe is that ‘back in the day’ all this borrowing and lending went on as it does now…. just with no collateral. This proved problematic in 1987 when thing completely froze in most markets but with the US faring better than most because its repo market was already highly developed. 2008 tested the system again and it was found wanting in many ways… but the repo market was not one. The last decade or more has been about improving the safety of the system. This came from two directions; first, making sure that all market participants were more credit worthy and second, to make sure that the system would be resilient in the face of a bank failure.

The first prong was all about capital/liquidity – banks now have (roughly) 3x as much capital to support a given level of activity – maybe more. But capital is not enough, banks go bust because of liquidity problems (which may or may not be due to perceptions of solvency). It became apparent that any business model that relied on short term interbank funding of longer term assets (Northern Rock) was dangerous so liquidity rules have been tightened and it has had two effects. (i) Interbank unsecured lending has declined to tiny volumes in anything longer than overnight trades – that is why LIBOR is being abolished… it just does not trade. (ii) that duration of banks’ liabilities are substantially longer than they used to be and they are paying a lot to achieve that.

The second prong is about making the system safer in the event of a failure and this is tackled in two ways (i) collateral and (ii) Central clearing. The first thing to say is that you can’t pledge your asset more than once. Delivery ensures that this is the case. So, your main concern is unfounded. I think your uneasiness is related to the potentially long chains of trades where collateral is passing though many hands. Can this cause problems? Yes, it can and the remedy is central clearing counterparties. If A sells to B and B sells to C both trades are novated to the CCP (A sells to CCP, B buys from CCP and B sells to CCP, C buys from CCP). B’s trades offset so there no movement of bonds, there may be a small cash movement. A and C both hold trades with the CCP so if either A or C fail the only affected party is the CCP. The CCP always has sufficient collateral from its members to cover any losses they might incur…. and then some.

This system is now used for most straight forward derivatives. It is also used in the US Treasury market for trades between Primary Dealers and this includes repo transactions…. I have confirmed with a GBP trader that this is also the case in the UK. CCPs are not used when equities of non-government bonds are used as collateral.

So, I really do think your concerns for the safety of the system are mis-directed. The repo market operates well and safely….. what risks/problems that there are lie elsewhere.

Finally, I think this comment (and any reply you offer) should end the thread. Very happy to spend time chewing over any bond market/banking system issues but it might be better done “offline”…… normally I would suggest a beer or two but lockdown forbids.

Clive

I have learned a great deal, and really appreciate your time

I am now inclined to accept your assurance

Best

Richard

Richard,

As you have not closed replies, while I respect Mr Parry’s opinion, and great knowledge of bond trading, I wished to make this point before you close:

Quis custodiet ipsos custodes? (Juvenal)

“I think your uneasiness is related to the potentially long chains of trades where collateral is passing though many hands. Can this cause problems? Yes, it can and the remedy is central clearing counterparties.”

This was always exactly my concern, especially for equities. Nevertheless, the question I wouls ask here is, who are the central clearing counterparties? CCPs as I understand it are operated by major banks, but I remain to be convinced that banks are the best people to regulate such undertakings. I accept CCP’s are authorised, by ESMA in the EU, but I am less clear who in the UK since Brexit?

In any case, and with apologies to Mr Parry, but my question remains. Who guards the guards?

I have to say I’m bemused by some of the online share platforms preventing individuals from buying shares in GameStop. Ig state they have stopped it so they “can ensure the quality of service delivered” !?!?! They seem to be trying to save the hedge funds a big loss which feels very cartel like.