This post began life as a Twitter thread. It builds on a post made here, yesterday. Some added charts and links have been included.

-----

As some will have noted, there were a lot of reports yesterday on the fact that £50 billion of banks notes are missing in the UK economy. This got me thinking. And as a result I have to suggest that finding that £50 billion of cash would not be hard. Here's how to do it.

As the Public Accounts Committee of the House of Commons has noted, around £50 billion of banknotes in issue have no explained use. In other words, they do not appear to be used for regular cash transactions. What their alternative use might be is not known.

Some could be in the possession of tourists, who have not bothered to exchange them on leaving the country. But the amounts involved would be small.

A bigger sum might be cash savings under the proverbial mattress. This is entirely plausible. It is possible that some of this will be related to benefit fraud: the amount of savings a person has can have a significant impact on their ability to claim a number of benefits.

There is no doubt that a significant part of this money Is used within the shadow economy. That can cover activity where tax is evaded, of course. But it also includes drug dealing and many forms of human trafficking and abuse.

No one is finding it easy to come up with an innocent explanation for the missing money. I cannot.

The Public Account Committee has suggested that the Bank of England is indifferent to this issue, even though in it acknowledges that the value of notes in issue is way in excess of those that appear to be required to meet the needs for regular cash payments within our economy.

The question then arises is whether anything can be done about this, and the obvious answer is that this is an issue that could be quite easily addressed if the willpower to do so existed. The way to address it is actually remarkably easy.

To address the issue what has to be done is that at short notice it is announced that all the UK's main denomination banknotes (£5, £10, £20 and £50) are to be replaced. No more than a couple of weeks notice should be given.

The change over period from the old to the new notes must be very short. A maximum period of a month should be allowed, but if possible, a shorter period of perhaps no more than two weeks should be provided.

It would then be the case that within a period of four weeks, at most, most literally the entirety of UK notes in issue would cease to be legal tender, and be replaced.

It's a fact that designing and introducing new banknotes is normally a very time-consuming, and lengthy, process. But, this exercise does not actually require the design of new banknotes. All that needs to happen is that the colours of existing banknotes be swapped.

So, for example, the brown used for the £10 note, could now be used for the £5 note. The blue from the £5 note could be used for the £20 note. And so on. That is all that is required. The designs need not change: just the colour must.

And yes, I know that will create issues for some colourblind people, But I am not sure that in this case that is a major impediment to progress, although I would, of course, be willing to hear objection.

During the four-week transition period old notes could, of course, be spent. Replacement new notes, with a total value of about one-third of the sum previously in issue, could then be injected into the economy. Because that's all we apparently need.

At the end of the four week period, or any time during it, a person could present old notes and ask for new ones. But in the case of any sum in excess of £200 the person making the deposit would be required to identify themselves.

The usual money laundering rules for proof of identity would apply e.g. a passport, driving license or an equivalent range of documentation would be required to swap notes. Without proof new notes could not be obtained once the transition was over.

In addition, any request for an exchange of notes in excess of £500 would require that the money first of all be paid into a bank account. This money would then become traceable.

The bank through which cash deposits were made should be required to seek explanation from the depositor as to the source of the money. A very low threshold for suspicious transaction reports should be applied. HMRC should have the power to freeze deposits, instantly.

Five things would immediately happen. First, the vast majority of this £50 million would either be found, or it would cease to be in use and cease to be legal tender, and therefore cease to be available for criminal or fraudulent purposes.

Second, this cash would now have identifiable ownership. Of course some will be disguised, but the power for HMRC to freeze accounts and investigate funds must be used: this is a one off chance to freeze the shadow economy. The tax take will increase.

Third, criminal trading will become harder to undertake. This will be a massive benefit to society.

Fourth, by eliminating cheating we will have a fairer, more equal society and one in which honest small businesses will have a better chance of flourishing because they will not be undermined by dishonest ones.

Fifth, it could be argued that the national debt is reduced, although that is very much open to question for reasons I will publish soon.

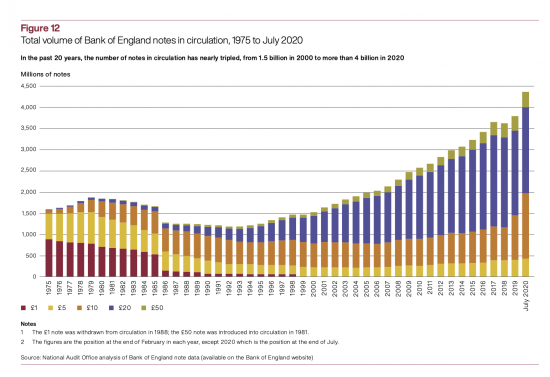

How much would it cost? The National Audit Office happened to publish a survey on the cost of producing currency during the course of 2020. They estimated there are 4.5 billion notes in issue.

This chart shows the use of banknotes over time:

They also indicated the cost of printing notes was about 7p on average. Only one-third of notes will be replaced. That implies a cost of £105 million to replace the necessary banknotes. Banks might also need to be paid for the additional work involved.

The benefits of reissuing all notes should massively outweigh the costs though, most especially if a significant number of investigators are employed to pursue data and collect tax owing and pursue criminal enquiries.

And let's also be clear, even if no cash was recovered (it's possible, although unlikely) significant criminal activity would have been discouraged. It's a win either way.

So will the social benefits outweigh the costs? I think so. I look forward to the argument from the politician who says otherwise.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

The new notes would also be guaranteed to be free from COVID-19 when issued.

You do know India just did this a few years ago, right? It killed thousands of poor people who had to walk for days and then wait in line at banks for days to change out bills. Plenty of cash under the mattress types lost life savings. They didn’t have anywhere near the right amount of cash ready and many people had to forgo many purchases because they didn’t have change. It crippled their economy and by all indications didn’t snuff out very much black market activity at all. But because Modi and propaganda it was wildly popular anyways. Everyone felt like they were making sacrifices to root out corruption.

Obviously the UK could probably avoid most of the hardship, but it still wasn’t effective.

We are a very different society

And the use of cash here is very different

I am aware of what happened in India

I think lessons could be learned and we could make this work

Here is a good paper on India.

https://pubs.aeaweb.org/doi/pdf/10.1257/jep.34.1.55

It seems to me that it would work better in the U.K. as we are not a country recognised in the main for cash transactions.

India has just had the biggest strike in history with agricultural workers blockaded from going into Delhi – not reported here on the mass media of course.

“…the power for HMRC to freeze accounts and investigate funds must be used:…”

Does HMRC have the staffing to even consider this at present ? Seems unlikely.

I really don’t think they would be impossible to find if reasonable pay was offered

Like many of your ideas, without numbers it’s just airy fairy wishful thinking.

How many additional staff do you calculate would be required at HMRC to police bank accounts as you are suggesting and what level of pay do you consider reasonable to attract the level of staff competent enough to do the policing?

“The tax take will increase.”

By how much? If you can’t answer how much the extra staff would cost and how much they would bring in, then you have no idea whether employing all those extra staff would be a worthwhile exercise.

“The bank through which cash deposits were made should be required to seek explanation from the depositor as to the source of the money. A very low threshold for suspicious transaction reports should be applied.”

How low? I would imagine many millions of people would have a few hundreds of pounds in cash in a jar or tin at home. Explanation? “I saved it over the years.” what then?

The few hundred pounds is not the cases anyone will look at

What price do you put on having law and order, and an environment where honest business can flourish?

I would of course stratify the sample of data and weight the research based on that

But bluntly, I suspect £30 billion or more would never turn up

As someone who has had extensive contact with the benefits system I can say that someone will look at a lot less than a few hundred pounds.

In that case, I agree that is the case

I would strongly reorientate resources to the tax system

Is this proposal similar to the Indian demonetisation of banknotes in 2016? And wasn’t it done for similar reasons – ie flushing out hoarded cash? My impression was that it had a deleterious impact on economic activity, and did not do much to flush out black market money. And where would we swap the cash? Would we be charged to swap?

India and the UK are massively different economies – and with massively different banking penetration in the population

India did not work as hoped

I think that because if the differences it could here

Fair enough.

“…. any request for an exchange of notes in excess of £500 would require that the money first of all be paid into a bank account. ”

I am uneasy with the drive to oblige or push everyone into using or requiring a bank account, for reasons discussed on another thread.

I admit to not having that concern

And I do consider myself at the libertarian end of the spectrum

I think it is deeply insidious; we know what can go wrong with banks. We know what can go wrong with personal information in modern technology: through ‘permissionless innovation’ (Schumpeter’s term, now used on a colossal scale he never imagined) and the rise of surveillance capitalism, which is merely the next, much bigger step beyond mere financialisation toward a new and subtler, even more hidden form of control and manipulation. Liberty is not being served here, but sacrificed on the new altar of the smart phone age: personalised seduction through what I term the power of ‘effortless convenience’.

I suspect we have crossed the point of no return here anyway

John, Richard,

Surely you’d just exchange smaller amounts in different banks at different times?

£100 x 5 at different places, is still £500. I think even mattress collectors would do this, let alone criminals? Obviously if it’s just one person with the entire £50 million, they might struggle with divvying it up in a couple of weeks, but apart from that I’m not sure those rules would necessarily catch any crooks. I’ve no idea how money laundering works though, so maybe I’m missing something?

I’m all in favour of money under the mattress, surely it’s everyone’s right to be allowed to save that way? If they want. I won’t though: I’m still furious I found an old tenner in an old purse at the back of a drawer years after they had changed – I just can’t trust myself to remember what I’ve put where.

Hence the need to provide an identity for smaller amounts and the need for suspicious transaction reports …this is a critical part of this – the dots have to be joined

I’m going to agree with most other people on this issue, and actually disagree with you on this one, Richard. (I know, shock horror)

I don’t think it’s worthwhile – maybe in purely monetary and cracking down on criminality terms, it could be – but not in social and cultural terms.

People LIKE money – people enjoy talking about a new design, and enjoy the feeling of – and actual – control having cash gives them. It might just be an IOU, it might just be borrowed, but it’s a physical thing in your possession.

A bit like real books, as opposed to digital books that you can never own. I can lend a real book, and I can give it to charity: even though there are ethical issues there too – the author or publisher doesn’t get to maximise profit from the number of readers of that book, while they can if its digital. But I’m not buying something to own if I buy digital – just renting it. With cash money I have more choice too – I can give cash to a charity of my choice, say a homeless person, rather than signing up to subscriptions of a big conglomerate charity that give 50% of it to their CEOs salary. Just saying. And no, I don’t care if the homeless person buys drugs with it – it’s theirs and their choice after I hand it over. Who is the biggest crook out of those two choices? A debate for another day.

Encouraging the surveillance state as well, just to catch a few crooks – that could be caught by other means, and should be – doesn’t seem like a particularly ethical solution either. You need to allow the population – already hemmed in by a million restrictions on their behaviour – some degree of freedom, or the feeling of freedom, a feeling of a modicum of control in their lives. You take that away, impose the nanny state, we lose all sense of self-worth and you exacerbate the problems we have with people no longer caring about anything. This might be at the far end of the spectrum of effects, but your solution is one step in that direction.

For a piddly little £50 million? Nah, not worth it – get the fraud squad on it, or HMRC or customs or whoever, that’s their job, that’s why we do pay our taxes, to ensure those services are there (so we think 😉 ). If those services can’t do their jobs – should we be paying taxes at all?? Your solution that might, and only might, work on purely monetary terms, could have the effect of exacerbating distrust in government and their institutions.

On the flip side, everyone would be delighted with a new design of note being issued – gives us all something exciting to discuss. We aren’t going cashless anytime soon I think.

£50 billion, not million

Oh.

Oops.

Haha 😀 , sorry! I should have read the article again instead of the comments! You COULD have corrected my earlier comment. There was me thinking ‘what on earth is he moaning about,,,’, but I obviously still haven’t got the hang of this big numbers thing. (It would help me if you wrote them in scientific notion, but that probably doesn’t help most other people so, I guess I’ll have to live with it).

Okay, that does put a different slant on it – though I think the cultural and social effects still need to be considered – but on the ‘worthwhile’ part – I’d need to reconsider.

Maybe veering slightly off-topic, sort of: I was considering there how we all view criminal actions and what that means for society’s behaviour. Briefly: criminality is not black and white – there are grades: that’s why we have different sentence lengths and type. Also the actual laws may not be good ones (eg old homosexuality laws). And everyone has different ways of viewing the morality of different legal, not quite legal or illegal behaviour (e.g. Tax avoidance vs tax evasion). So the more wealth inequality we have, the more unfairness we have, the more the great unwashed see how the laws only favour the already wealthy, the more those unwashed are going to veer into not particularly legal territory and be more accepting of that bahaviour when they see it. The institutional corruption and unfairness they see can only increase the volume of smaller illegal activity – either from people turning a blind eye or from actual activity. (I’m terrible at being brief, so can only hope that makes sense, but you have to admit the current uk gov’t isn’t exactly giving a very squeaky clean impression, and they are our legislators).

So I think that even if the biggest drains on the coffers are aspects of cash economy, it’s still the big – the corporate, the institutional, the wealthy – issues that need to be tackled first. If you have a society where laws are only for the little people, the little people are not going to be be too bothered about moral imperatives of those laws while watching the elite ignore the same laws with impunity. It might just be perception – but that matters, if you want compliance to the rules.

All accepted

Remember I was responding to the suggestion that no one seemed to know how to tackle this issue

Oh yes, of course, and as a solution, taking the problem in isolation and the resulting outcome in the short-term, it’s a good solution and has the simplicity of being able to work with what we already have.

It’s the framing of the issue: the missing £50 billion, and

The longevity of the solution: do we want to stop there being a missing £50 billion forever?

If you look at what the *source* of the missing cash is – you have outlined the most likely places for why it’s missing, which sounds about right, and from that analysis I would say the source of the problem is caused by distrust in government and institutions – you’ll probably think of better sources – why is it missing? You’ve located where, so now, why?

On longevity, your solution is replacing like for like, so can only be a short term solution unless you tackle the source of the problem. Things will go back to how they were fairly quickly after a fair amount of disruption, yes, but it doesn’t create incentive for a change of behaviour long term. It’s a distributed population-wide problem, so needs to be thought about in broad terms.

I think just as most people *want* to pay taxes, most people will want to be law-abiding and fair – it’s the ‘turning a blind eye’ people that will resolve the problem if they have trust back – actual criminals will always be trying to find ways to dodge and scam, but they have less wiggle room if the majority of the population are fine upstanding citizens that don’t turn a blind eye. If the problem is tackled by resolving the source, it will be a lasting solution, not temporary.

I think you are *already* tackling the problem with all you do on tax justice and fair accounting etc – yes, some of the nasty criminal behaviour will need to be crow-barred out, but in the main, people seeing a fair system that doesn’t penalise them at every turn will have the biggest effect. What we really need to do is convince government and the BoE etc that all your tax justice and accounting solutions will, in fact, resolve the missing billions by default. And I wonder if their lack of interest in finding a solution is because they already know this?

It’s not a head-on immediate fix, but in fact, you are already doing the solution!

I like that

But off this was a one-off step in that same direction?

Would that work?

So it’s a crime now to have your money stuffed under the bed, must we have to keep all our cash savings with the bankers who have driven the return to near zero. I’ve also read that legally speaking the banks own depositors money and if they wished to they could issue customers with shares. In view of the current economic worries and possible runs on banks then it would be prudent to hold enough cash to see you through a couple of months. Gold and BTC will be held instead If government insists that citizens can only hold small amounts of cash.

Also seen reported that the Mafia use old Lira banknotes as currency amongst themselves.

The point I m making is that even the cash is lent to people to use

Interesting idea. Of course, there are lessons to be learned from India but it would be much easier in the UK.

But, would it really solve the issue? If we split the illegal use of cash into three categories “savers”, “drug dealers” and “cowboys” (doing jobs for cash) I think we capture most of the notes in circulation.

No issue for savers, they just make the exchange. Some will choose not to or just forget but there is no problem, at any stage they can still roll up with notes, produce ID, deposit the money (and withdraw new notes if they so desire).

Cowboys have, presumably been recycling all the cash they take for jobs “as they go” so do not have vast hoards of cash that will draw attention to themselves. I suspect it would be a minor hiccup in their activities that would straight away resume with new notes. The only way to stop this is better enforcement by HMRC (and others) and, perhaps more importantly, a change in societal attitude to this activity. It appears to be that many “upright members of society” can’t resist a cash bargain…. and actually brag about it.

What will drug dealers do? They will change as much “old for new” as they dare in the change over window but after that old notes may still be used as currency in the underworld. They will trade at a discount to new notes but be perfectly acceptable for business. Indeed, in some parts of the world, a crisp new $100 bill trade at a premium to some grubby 10s and 20s….. but both still do the job.

In short, your scheme might help but there is no substitute for proper enforcement by real people on the ground.

Finally, I looked up the scale of the issue relative to other currencies (all data from CB balance sheets in GBP equiv)…..USA 1,300bn, Eurozone 1,200bn, Switzerland 70bn, UK 76bn. Not sure what that tells us; we know the USD is used all over the world and (so I am told) the EUR is the criminals currency of choice due to the large denomination notes (used to be EUR500, now EUR200)… but even so there are a lot of dollars and euros out there! Is there any pressure on their CBs to look at this?

Agreed

I make no pretence this is a perfect solution

I offered it as a solution, but by no means the only one

My concern is this: many people who ‘hoard’ cash are not in any way breaking any law. They have earned the money they are hoarding, paid their taxes, HAVE a bank account, etc. But at the moment, banks are shutting down all over the place (post offices as well.) I have a friend in the far north of Scotland who has to drive 52 miles ONE WAY to do her banking. And she has a car. Some of her neighbours are not so fortunate. These folks are hoarding cash because it’s difficult to get to a bank …and online banking doesn’t always suit–either the buyer or the seller. Some of her neighbours routinely withdraw large amounts of cash when they do manage to get to a bank, simply because they know it’s going to be a long time before they can do it again.

I live in a smallish city, but my own branch bank has shut. Ditto our main post office. Yet another major bank in the town centre is in the process of shutting. It’s getting harder and harder to exchange cash. A proposition like the one you’ve made would impose a lot of hardship on the wrong people …and leave them without access to the money that is honestly theirs. I would forsee real widespread terror–especially among the elderly, the infirm and the isolated–if this was to be implemented without taking all circumstances into account.

After all, hoarding cash is not a crime. What IS a crime is avoiding tax on what you earn–being part of the black market economy. While this proposal might flush out the black market miscreants, to some extent …although miscreants usually find a way to continue skirting the law …I fear it would impose lots and LOTS of hardship on good, law-abiding people who are simply finding it hard to access a bank or post office these days, or who don’t trust cashless card-based transactions (lose your card, forget your pin number, you’re in bother), or who don’t have computers, smartphones, etc to do online banking at all, or who don’t trust the banks themselves not to pull up stakes and leave town.

This is an interesting proposal, but I think it requires a lot more detailed work, to ensure that the wrong people don’t get hurt.

I agree that I outlined a proposal

I am not convinced that holding cash is necessary

I recognise the issue for retailers

I also recognise the problem with closing banks

I also know many young people who almost never use cash. That is a massive trend so the issue is very much age related

But no one is penalised by what I propose. Everyone could get value for their notes. They may have to explain them.

“I am not convinced that holding cash is necessary”

There is the problem. People who hold cash, not for nefarious reasons, are gratuitously placed in the position that they have to explain themselves; they have to convince a gatekeeper. Small cash businesses without a bank in remoter areas (this applies to a lot of small of communities in the Highlands) are already probably charged substantial sums for their bank to pick up their hard-earned cash, and it is too expensive. They have to drive significant distances to find a branch of their bank. Now they will have to explain themselves when they take it to the bank. The elderly may not trust banks; why the young do trust them is frankly a mystery to me: oh, I know, they have been seduced by persmissionless innovation, bought cheaply by the bauble of effortless convenience: but bought and sold.

We are being driven to a cashless society in a hurry by greedy banks who see an opportunity to exploit, and the chance to supply a bad public service cheaply with general political approval. We are being driven like sheep through our susceptibility to effortless convenience. And nobody cares. They will; as always, when it is too late to do anything.

For once, we have to differ

When we realise that cash is simply a bank debt instrument – and it is – then these objections seem hard to understand to me

“[C]ash is simply a bank debt instrument “. It is a bank debt instrument that has been issued with the umbilical cord cut to the bank. It is a form of instrument that is free of bank control. You focus on the criminality this may serve; I accept that is a problem that requires to be addressed seriously, but I also recognise that the banks (and government) may also be misused by the interests that control them. The assumption that this can always be passed off as the “public interest” or “national interest”, candidly do not trust; and I am confident the evidence is there that trust should never be taken for granted by the public. On the basis of past (recent or distant) experience, why should the public gratuitously trust banks or government on such a matter that may prove critical to personal liberty?

We are drawing that line in different places

May I just add, I think Rob’s observation telling: “I felt like it was an attempt to drive us towards digital currency, where you cannot hold it without the government knowing (unless you are friendly with the government and take advantage of loopholes available only to the wealthy)”.

My earlier post on ensuring that there is a legal right to make certain payments ibn cash doesnt seem to have appeared so here is V2

It seems to me that what is needed is some sort of national ‘cash plan’

That includes ensuring the availability of cash via free to use cashpoints and the provision of banking facilities.

It must also include the right to pay certain bills or make certain purchases in cash.

Part of the strategy also needs to include the abolition of the £50 note, ways of making it harder to use cash for either criminal purposes or to avoid tax. Possibly this might include limits in the amount of cash individuals are allowed to hold without an explanation or a limit on the maximum value of cash transactions.

I also suggest that similar restrictions should apply to other currencies held or used in the UK.

I am not suggesting that cash be eliminated for one second

I am suggesting that all that is required by the economy be provided

And no more….

I agree with abolishing the £50 note – there is literally no need for it

I suspect the £20 should probably go the same way in due course

And I am not saying anyone should be banned from paying cash – but presumably you know there are reasons for very good reason now why larger sums have to be explained, and so are usually refused, and rightly so?

PS I cannot see I have deleted anything and you have nothing left waiting for moderation – so do not know what happened to the other comment

I commented on this last night and it hasn’t been posted. A glitch?

No – not a glitch – but it fell out of view overnight

Sorry

I sometimes do this and every few hikes go back and check that looking at recent comments has not meant I have missed something

Surely 5 and 10 notes have already been recently replaced, additionally 20 notes are in the process, if they actually put an end date on the old ones then they would have to be exchanged.

At the not, it looks almost as if banks might start to charge us to hold savings with them in the form of negative interest rates, I believe some business accounts already do. Also, access to cash banking is getting more difficult, cash machines and banks disappearing. No surprise that more is held under the mattress then.

What’s more worrying is the committee view that this creates problems for fiscal policy, because the money isn’t collected through taxation, something we know isn’t true.

I felt like it was an attempt to drive us towards digital currency, where you cannot hold it without the government knowing (unless you are friendly with the government and take advantage of loopholes available only to the wealthy)

They’re is a problem for fiscal policy

Tax is charged to control the impact of spending on the economy

Unless that is charged fairly the ability to intervene in the economy is reduced by not havbiogn control through the tax system

I fully comprehend MMT

MMT has to fully comprehend that a functioning and fairn tax system is integral to it

Far too few who promote MMT do so

When they do MMT will be mixup mo0re effective

And tax can also then be used to deliver what is really necessary – a fairer society

One issue on a practical level might be that (particularly) the elderly are targeted by those who wish to swap out old colour notes for new colour notes. Many of us who handle cash infrequently may be pretty poor at spotting the new defunct coloured notes.

But they will remain convertible

Richard,

A possible modification to your suggestion. Rather than swapping the colours of bank notes could we not just begin to print the year on the notes? US dollar notes have dates on and I know from the voluntary work in South Sudan that people will only accept dollar bills from the most recent years. It might be easier for people here to look for the date on a bank note than remember which colour is the legal colour.

Neat!

If I were to make one more point – V3 i suggest that

1. We need to look at the reliability & accessibility of the banking/money transfer system, and

2. Take a much tougher line on Fraud, at the moment it often seems that no action is taken when large sums of money are fraudulently taken, despite of course it being clear what account they were transferred to.