There are hints today that the government is planning to make climate change disclosure by large companies mandatory. Rishi Sunak has given this the nod, saying that it will be mandatory within five years, as if we have all the time in the world on our side. And, in another co-ordinated move with the Bank of England Governor Andrew Bailey made clear yesterday that this means an endorsement of his predecessor's Task Force on Climate-related Financial Disclosures recommendations. There are, however, major flaws implicit in this suggestion.

Rather than reinvent the wheel I am, for the second time this morning, going to republish previous comments, this time from June this year, when I wrote the following explanation as to why this proposal falls way short of what is required to tackle the issue of large companies and their climate emission reporting:

There is an article by the likes of Andrew Bailey, current Governor of the Bank of England, and Mark Carney, his predecessor in The Guardian this morning. With other central bankers they argue:

This crisis offers us a once-in-a-lifetime opportunity to rebuild our economy in order to withstand the next shock coming our way: climate breakdown. Unless we act now, the climate crisis will be tomorrow's central scenario and, unlike Covid-19, no one will be able to self-isolate from it.

I do of course agree. I also agree with this:

To meet the goals of the Paris agreement requires a whole economy transition: every business, bank and financial institution will need to adapt. The pandemic has shown that we can change our ways of working, living and travelling, but it has also shown that making these adjustments at the height of a crisis brings enormous costs. To address climate breakdown, we can instead take decisions now that reduce emissions in a less disruptive manner. That requires us to be strategic. To build back better.

But there are issues when they make this claim:

Following the global financial crisis, only a fraction of fiscal spending improved sustainability. This time, governments' stimulus packages can be more ambitious; for example, some are already accelerating the transition to clean energy, retrofitting homes and buildings, and linking financial support to climate-related conditions laid out by the Task Force on Climate-related Financial Disclosures (TCFD).

It's when they get to the Task Force on Climate-related Financial Disclosures that I have the problem. And that's because they are simply not up top the job that they claim that they will do, That is because as a result of the work I have been doing on sustainable cost accounting I have become pretty familiar with this thing: The greenhouse gas protocol splits greenhouse gas emissions into three categories. Thankfully, they're pretty easy to define:

The greenhouse gas protocol splits greenhouse gas emissions into three categories. Thankfully, they're pretty easy to define:

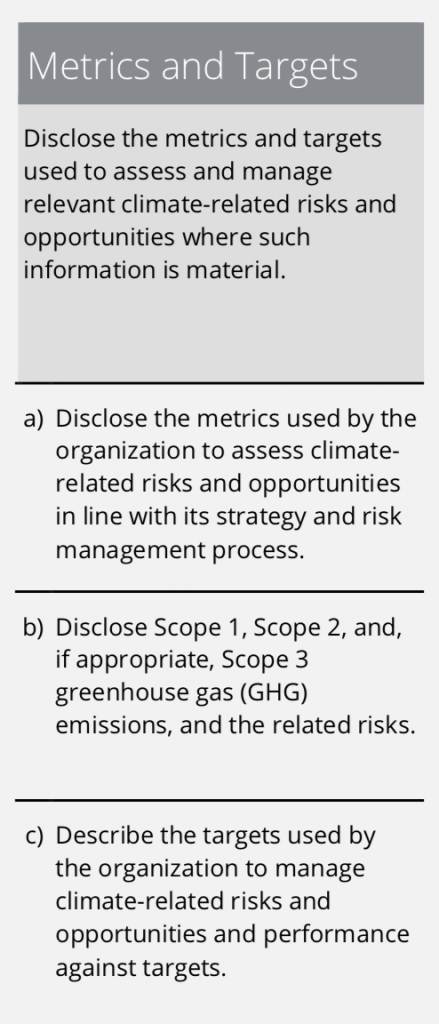

I've reproduced the Protocol's own description just to make clear that they really do think there's not much to this. Except that there is. And that's because right now business has decided for reasons all of its own that only Scope 1 and 2 emissions are of importance. Mark Carney's Task Force on Climate-related Financial Disclosures summarises its reporting requirements pretty succinctly as follows:

Note that category (b). It says that Scope 3 need only be disclosed ‘if appropriate'. And what defines 'appropriate'? Nip up to the top of the column and you will find it is when management think that it is 'where such information is material'.

And as it turns out, almost no one does seem to think Scope 3 is material. So we end up with the absurd situation where airports claim they are carbon-neutral because they ignore the emissions from the planes that fly from them and coal mines can make the same claim because they say someone else burns the coal that they mine, and they claim that's got nothing to do with them when glaringly obviously that's untrue.

My points then are very simple ones.

First, any accounting standard for greenhouse gas emissions that does not require Scope 3 disclosure is incomplete. In fact, it's not a standard worth calling by that name because it ignores a crucial issue.

And second, anyone who claims they are carbon-neutral and ignores their Scope 3 emissions is making a claim that is simply not true.

But now Carney is saying that financial support should be linked to this wholly inappropriate standard. And that's wrong.

Thankfully there is a better option. That is sustainable cost accounting. That will work. And that's what financial support has to be linked to because it makes Scope 3 disclosure mandatory.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Richard,

Using your example of an airport when looking at scope 3 emissions, you say that airports can claim they are carbon neutral because they ignore the emissions of the planes that fly from them.

Shouldn’t the airline company be responsible for those emissions?

If the airport is, wouldn’t the airport also be responsible for the emissions created by the airlines themselves, all the passengers and all their suppliers as well?

This is the corporate shrill argument

The oil company blames someone else for burning it

The car company says ‘we never knew someone would drive our products’

And so on

Nonsense!

Of course the airport is responsible for its actions

For heaven’s sake we are all able for the foreseeable consequences of our behaviour

And what you are really saying is ‘blame the consumer’ as if consumers have real choice – which is obviously untrue, even before advertising is considered

So, bluntly, your claim is absurd

Yes, the airport is responsible. So is the fuel company, the aircraft manufacturer and more

And before you say ‘that is double counting’ this is micro reporting and all accounting double counts

Of course the airport should be responsible for it’s actions and the emissions it produces.

That isn’t what you are saying though. You are saying it should be responsible for everything related to their business as well, from the bottom to the very top of the supply chain.

Aircraft fly between airports. Under your logic, which airport would be responsible for the emissions of the flight? Would it be shared? Would both of them have to account for it equally?

Double counting is an issue if you are going to make companies pay for the amount of emissions they create. You can’t just arbitrarily assign all the costs of an entire supply to chain to one member of it – though what you are saying seems to make out the every member of the supply chain would have to bear the costs of the whole supply chain. Which makes little sense.

Both airports are responsible

They both enable it

And I reiterate this is normal

If a can of baked beans requires product to move through ten subcontractors, each adding 10p to the value, before reaching the consumer for £1.20 the total reported turnover for the can sold within corporate accounts is £6.70

Is that double counting?

No, of course not

So more is what I am suggesting double counting either

And I am. not asking anyone to bear the whole cost

I am asking them to bear the cost of their elimination of carbon

You have not read what I have proopsoed, have you?

Turnover isn’t the right accounting measure to use here.

In your example, the baked bean can could go through an unlimited number of subcontractors, but there would still only be one baked bean can, and the same amount of profit or value created in the chain from that one can.

Turnover doesn’t actually mean anything in this context if you just aggregate it as you have done. You don’t suddenly have £6.70 worth of beans because it has passed through a supply chain.

Taxation isn’t based on turnover either, because of this.

The same logic applies to emissions. It should be pretty obvious but a given supply chain will create a certain amount of emissions, for which different parts of that chain will be responsible for different amounts. Counting emissions as you would with turnover doesn’t suddenly push more emissions into the atmosphere just because you introduce more accounting steps because you have used turnover as a metric.

Trying to account for emissions on an aggregated turnover basis simply makes no sense.

What you are saying with SCA (which I have now read, thanks) is that each part of the supply chain should be responsible for the emissions of the whole supply chain. Which is double counting. You compound this problem by the saying companies aren’t allowed to offset the carbon they produce. Which would essentially make it impossible for most industries to survive given that almost every activity generates some level of emissions.

I am not trying to account for emissions

I am trying to account for the cost of an entity eliminating em missions form its activity

If you are going to engage here please have the decency to read and understand what I have written

You have not

You are making up a straw man argument

To account for the cost of eliminating emissions from an activity, surely step one would be to calculate or in other words account for the amount of emissions of the activity?

How else could you do it? You can’t seek to eliminate something if you don’t know how much of it there is?

If you use turnover of the whole supply chain you will then double count how much of that activity there is. Which means if you then use that turnover number as the “supply” of emissions you will be trying to eliminate a vastly larger amount of emissions than the actual supply.

All of which is making your sustainable cost accounting idea look rather suspect.

Wrong

The cost does nit require precise estimation of the amount of carbon – only an awareness that a process results in it

Then the price is that if a process that does not do so

That’s it

Some very senior accountants get it, I can assure you

So now each individual process within a business has to be carbon neutral as well?

By that logic very, very few businesses would be possible, given most processes in the world require some emissions – even agriculture. Certainly little or no manufacturing would be possible, and transport would be dramatically curtailed. Healthcare and homebuilding would also be essentially wiped out if every process within every sector has to be carbon neutral.

Your fixation on having every individual process carbon neutral also misses the bigger picture. We don’t need each step or each process to be carbon neutral – not least because it is impossible if we want to maintain even a semblance of our modern lifestyles. What we do need is the system as a whole to be so – which is potentially achievable, but only if you offset process which cause emissions with processes which reduce them. Which is surely a much more realistic idea.

You also seem to keep trying to move the argument away from the errors you have made. You started by saying that a business has to account for it’s total emissions footprint on a turnover basis along it’s entire supply chain. having pointed out your error by using turnovers, you now say each company needs to make each process carbon neutral.

How on earth could a company guarantee that every supplier it uses has every process they use carbon neutral, let alone every one of their customers being so?

For example, just by reading your blog I am using energy. How could you you account for my emissions footprint? But under your rules you or your company is liable for them? Is my company supposed to be liable for all your emissions for reading your blog too?

It’s totally unworkable.

Does it say that?

No.

So why do you say that?

Because you are making this up

I think it’s time to end this pointless (on your part) exchange

Maybe it is a tiny step in the right direction until your comprehensive sustainable cost accounting is recognised and put into practice. However, corporations are not going to take climate measures seriously until much greater incentives and sanctions are enforced and genuine monitoring of progress publicised to shame companies who do not comply. Present corporate thinking is to do the bare minimum while keeping their main motivation on short term profit maximisation.