There is an article by the likes of Andrew Bailey, current Governor of the Bank of England, and Mark Carney, his predecessor in The Guardian this morning. With other central bankers they argue:

This crisis offers us a once-in-a-lifetime opportunity to rebuild our economy in order to withstand the next shock coming our way: climate breakdown. Unless we act now, the climate crisis will be tomorrow's central scenario and, unlike Covid-19, no one will be able to self-isolate from it.

I do of course agree. I also agree with this:

To meet the goals of the Paris agreement requires a whole economy transition: every business, bank and financial institution will need to adapt. The pandemic has shown that we can change our ways of working, living and travelling, but it has also shown that making these adjustments at the height of a crisis brings enormous costs. To address climate breakdown, we can instead take decisions now that reduce emissions in a less disruptive manner. That requires us to be strategic. To build back better.

But there are issues when they make this claim:

Following the global financial crisis, only a fraction of fiscal spending improved sustainability. This time, governments' stimulus packages can be more ambitious; for example, some are already accelerating the transition to clean energy, retrofitting homes and buildings, and linking financial support to climate-related conditions laid out by the Task Force on Climate-related Financial Disclosures (TCFD).

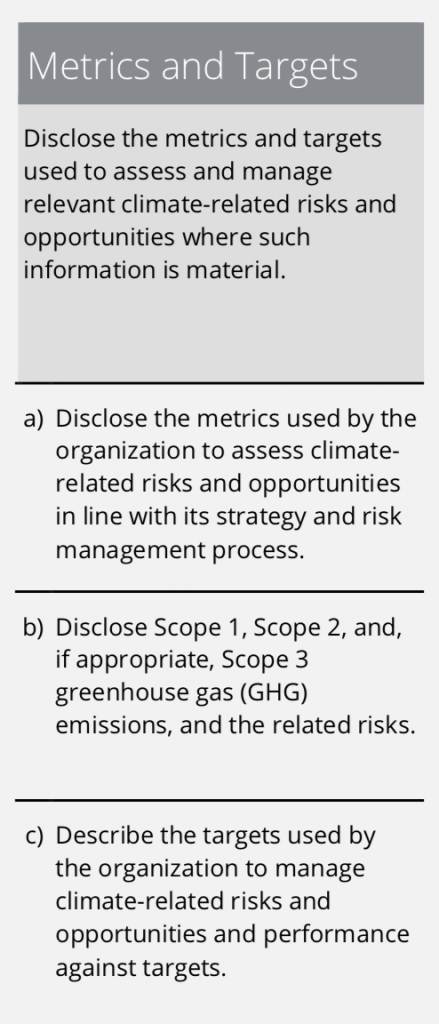

It's when they get to the Task Force on Climate-related Financial Disclosures that I have the problem. And that's because they are simply not up top the job that they claim that they will do, That is because as a result of the work I have been doing on sustainable cost accounting I have become pretty familiar with this thing: The greenhouse gas protocol splits greenhouse gas emissions into three categories. Thankfully, they're pretty easy to define:

The greenhouse gas protocol splits greenhouse gas emissions into three categories. Thankfully, they're pretty easy to define:

I've reproduced the Protocol's own description just to make clear that they really do think there's not much to this. Except that there is. And that's because right now business has decided for reasons all of its own that only Scope 1 and 2 emissions are of importance. Mark Carney's Task Force on Climate-related Financial Disclosures summarises its reporting requirements pretty succinctly as follows:

Note that category (b). It says that Scope 3 need only be disclosed ‘if appropriate'. And what defines 'appropriate'? Nip up to the top of the column and you will find it is when management think that it is 'where such information is material'.

And as it turns out, almost no one does seem to think Scope 3 is material. So we end up with the absurd situation where airports claim they are carbon-neutral because they ignore the emissions from the planes that fly from them and coal mines can make the same claim because they say someone else burns the coal that they mine, and they claim that's got nothing to do with them when glaringly obviously that's untrue.

My points then are very simple ones.

First, any accounting standard for greenhouse gas emissions that does not require Scope 3 disclosure is incomplete. In fact, it's not a standard worth calling by that name because it ignores a crucial issue.

And second, anyone who claims they are carbon-neutral and ignores their Scope 3 emissions is making a claim that is simply not true.

But now Carney is saying that financial support should be linked to this wholly inappropriate standard. And that's wrong.

Thankfully there is a better option. That is sustainable cost accounting. That will work. And that's what financial support has to be linked to because it makes Scope 3 disclosure mandatory.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Greenwashing from the central bankers to go along with what I have read today from ‘Source’ on the Covid Corporate Financing Facility, that offers loans without any any consideration of those companies impact on the environment.

Actually there doesn’t seem to be any conditions on these loans.

It’s not just RR either. BP, Shell, Stagecoach….and on.

It sticks in the craw to be honest.

What would you no recovery prefer and mass unemployment ??

These loans aren’t providing a recovery and they’re not stopping redundancies.

Rolls Royce are laying off 700 people in my area, yet they’ve received £300 million through CCFF.

I’d prefer if the loans came with conditions. For instance can’t RR use their experience to move forward wave power, and retain staff in this country?

Maybe this isn’t viable but to just give companies a loan with no conditions isn’t going to transition to a green economy, nor retain jobs.

At least make it a condition that these companies can’t just pay huge dividends now. This has only been ‘suggested’ according to the article.

What’s the point in a government loan if there’s no return for the public?

How can you include Scope 3 emissions?

It would lead to double counting as your scope 3 emissions are someone else’s scope 1 or 2. On top of that how can you even measure scope 3 emissions attributable to a particular company in any sensible manner.

using your example of an airport, it’s Scope 3 emissions include the planes that fly, as you say. But then do you have to include the emissions of building those planes as well, and the fuel, which both belong to another company, and then are you going to try and measure exactly how much those planes fly, then attribute bits of those emissions to different companies? Or are you going to just double or triple count some of those emissions?

Apart from the crazy level of complication that this would lead to, it doesn’t seem at all realistic or practical, notwithstanding the double counting. Which seems to be why everyone looks just at Scope 1 and 2.

So what?

This is micro and not macro data

Double counting does not matter

Elimination does

You aren’t even making sense. Double counting matters a huge amount when you are saying a company should be responsible for their own carbon emissions. If you double count everything, you make it so they are responsible for other people’s as well.

You have invented this SCA idea. Why don’t you give an example of how it would work in practice? Would this blog be responsible for all the people’s emissions reading it, for example?

See the reply provided to another person

Yet us you not making sense

You are promoting denial of responsibility by false accounting

“Double counting does not matter”

Hilarious, but not unexpected.

As ever, all you are appear to be trying to do is to create a new role for yourself and justify your own existence.

Go on then, why does double counting not matter?

It is what happens in corporate accounting.

A tine if baked beans could easily be sold by the manufacturer, wholesaler and retailer before being consumed

Is that wrong?

And yes, it nets out at profit level, but nit at turnover and scope 1 2 and 3 are effectively turnover measures

You are the one making the silly claims here

You are saying double counting doesn’t matter. If that is the case, each company would be accounting for not only their own emissions but those of other companies and end users as well. If anything, accounting for things you are not directly responsible for and have no way of measuring would be false accounting – which says a lot about the problems with your idea.

This becomes rather important when you also claim that in SCA that company should have to PAY for all those emissions or be rendered insolvent.

So if you have a supply chain company A to B to C, company B has to pay the cost of emissions for A, B and C. As does company A and C.

Not to mention the difficulty in actually calculating what those emissions would be, specifically in the case of scope 3 emissions. Does BMW have to pay for the emissions created when someone drives their cars? Which is very dependent on how much those cars are driven. Does BP also have to pay for the emissions for the driver’s fuel? The way you are making it out, both do.

I get the distinct impression that you haven’t bothered to think things through in any detail – which is why I asked you to give us an example of how it would work in practice with your own Tax Research LLP, which you should be well acquainted with.

Does Tax Research have to account for all the emissions created by the users of the blog? If so, how would it calculate the amount of those emissions?

You really are being rather absurd here 0- and I think you know it

That, or you have not read SCA properly

SCA is not about paying for emissions

SCA is about paying the cost of eliminating emissions

And it is a specifically micro measure

And micro specifically always double counts as I have shown

But if it could be shown in a plan that cooperation was possible to eliminate emissions that would be great

However, re Scope 3, no one seems to have any difficulty with this

And since all consumer emissions are outside the scope of reporting – because they are not businesses (maybe you don’t realise that) they have to be in corporate reporting or no one ever deals with them

How does Tax Research do this?

Well first you will note SCA does not apply to it: no SME is because they do not create serious emissions in most cases that are not covered by Scope 3 of large entities – so that addresses so8ible counting very effectively

And second, it would by planning how to reduce electricity use as much as possible – and by design I suspect that is possible but I accept I have not done it as yet

But this will not have any relevance to you because you think BMW has to pay for emissions when someone drives its cars

No, it has to make its cars emission free

And that’s what you’re missing

SCA is vastly more radical than you think and completely different from what you think

I suggest you go and re-read it

ED NOTE

As I suspected this poster resorted to ad hominem attacks for which there were no foundation in this comment, which related claims already made that I had answered.

Her further comments will be deleted as a result

Blocking her posts just makes you look juvenile. You haven’t answered her questions properly if at all, so why don’t you give that a go instead.

As far as I’m concerned, you are losing the battle on this one. SCA is so full of holes you could use it as a net and go fishing with it. Which is probably what you are doing for grant money, let’s face it.

Isn’t it odd how you use almost identical language?

I wonder why that is?

I read the article this morning. It seemed that the Green Deal was being embraced by the heart of the financial establishment. Good news!!

Thank you, Richard, for pointing out the problems with their approach….. and I won’t hold you personally responsible for ruining my day.

You can

Many do…..

I think the only thing absurd here are the contortions you are making to avoid facing the problems with SCA.

Paying for emissions and paying for the cost of eliminating emissions are both a cost. The cost has to be accounted for and the distinction you make is frivolous. If anything, paying for the cost of eliminating emissions is yet another flaw in SCA – very few (if any) industries are emissions free, even at a low level and especially if you include Scope 3. (I’d love to see if you can name a single one, because I can’t). But your focus on each individual company being zero emissions rather misses the point – which is that we want the system as a whole to be zero emissions, but it is not necessary (or even possible) for each individual part of that system to be zero emissions.

Micro specifically does not double count. That is just nonsense. What would any serious accountant say if you told them it is OK to double count something?

Regarding Scope 3, it seems you do actually have some difficulty. Not least that you are simply plain wrong when you say that consumer emissions are outside the reporting scope.

I quote from the GHG protocol:

“Category 11:

Use of Sold Products

Category description

This category includes emissions from the use of goods and services sold by the reporting

company in the reporting year. A reporting company’s scope 3 emissions from use of

sold products include the scope 1 and scope 2 emissions of end users. End users include

both consumers and business customers that use final products”

Link: https://ghgprotocol.org/sites/default/files/standards/Scope3_Calculation_Guidance_0.pdf

End users INCLUDE consumers……

So moving to to Tax Research. I am somehow not surprised that your first answer is to simply avoid the question, saying SCA doesn’t apply to Tax Research.

But let’s say it did. You then say Tax Research would plan to reduce electricity use as much as possible. Having read SCA, a company that can’t become carbon neutral is made carbon insolvent and should be shut down. You also say that under SCA offsetting isn’t allowed.

Now maybe I don’t fully understand Tax Research’s business, but as far as I can tell no part of the business is carbon negative, and every part of the business (Scope 1, Scope 2 and Scope 3) are carbon positive. By this logic, Tax Research should be rendered carbon insolvent and cease to exist. You can’t offset, and every part of your supply chain creates emissions, not one part reduces them.

I think the above highlights some of the many flaws in SCA – having read it. Each company is forced to be zero emissions, when in reality production of any kind requires some emissions. Even green, zero emission energy sources require a huge investment in both financial and emissions terms up front. Under SCA this would be impossible. Then you compound the problem by including Scope 3 emissions, and double count to make it even worse. It’s pretty clear you haven’t even though hard about the problem – you don’t even have a proper answer for your own Tax Research. Just a wishy washy excuse, basically.

You haven’t even done your research carefully – as your understanding of Scope 3 shows. Did you just cobble SCA together one morning when you saw Greta Thunberg on TV to try and get in on the act? Is it an attempt to secure some funding for yourself? I don’t see your name involved with any of the significant global groups who are researching, developing and writing the evolving Green accounting standards over the last 20 or so years, so your epiphany strikes me as rushed as your work.

This is getting mildly tedious because it is clear that you are not engaging with answers given and are coming with a closed, and also uninformed, in the sense of having not properly read what SCA is about, mind.

If you had you would know Tax Research LLP is not concerned because it is a small company and the suggestion does not apply to them because the issue is almost entirely with large ones

And actually I can clear my Scope 1 and 2 by buying decisions – using a sustainable supply. So, you are completely wrong on that. Your claim is false, which makes the rest of what you say look implausible.

Whilst what you are saying on Scope 3 completely baffles me. Of course Scope 3 is end user emissions. But the cost to cover in SCA is how to eliminate the company’s contribution to those emissions i.e. the cost of transforming its processes until they are carbon neutral

The ICAEW have completely understood this – hence their support for this project

You need to understand what it is saying

SCA does not account for carbo

It accounts for the cost of eliminating carbon in the emissions created by large companies – which is a sufficient target

It does not then accept that status quo – which is what carbon cost accounting does. It consciously requires the corporation to change it