The Institute for Fiscal Studies has issued its Green Budget (i.e. its forecasts for what it sees the budget scenarios to be) for autumn 2020 even though no budget is now expected. I think it fair to say that some of what they say is unsurprising, most especially as the work is being done with Citi, the US bank that has extensive operations in London.

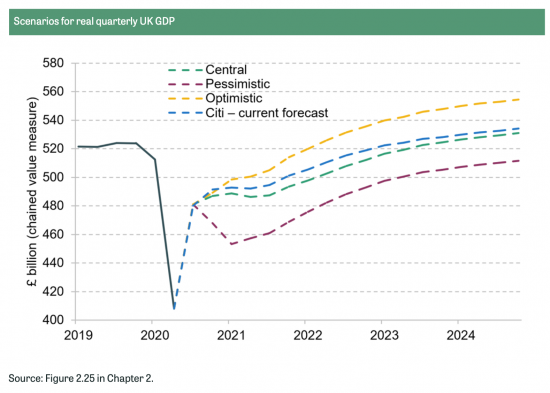

They forecast growth as follows:

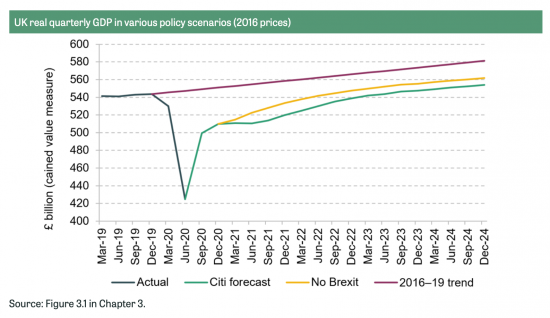

They make clear that this is impacted by Brexit:

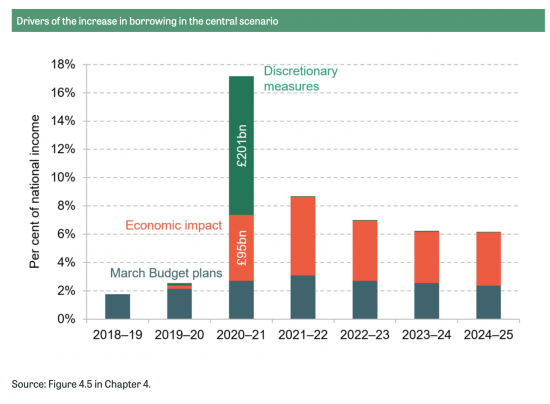

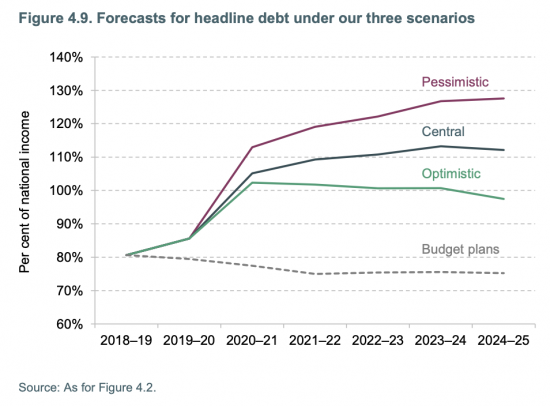

And then they show the impact on the government's balance sheet:

It is annoying that this last is stated in percentage terms, as is this chart:

The implication of both is, however, that the government will have to undertake what the IFS thinks to be borrowing over the next five years, and at rates much higher than those forecast in March 2020.

As the report says:

The UK has traditionally shown itself to be a relatively flexible economy. This reputation is likely to be tested to the extreme over the coming years. We expect substantial restructuring of the UK economy in the years ahead as it responds to the new shape of demand from UK consumers in the wake of COVID-19 and the new shape of trading relationships in the wake of Brexit. Such restructuring implies a more protracted economic recovery and a substantial loss of economic capacity as some of the expertise and capital specific to now shrinking sectors becomes surplus to requirements.

In other words, expect turmoil, massive rates of corporate insolvency, major economic restructuring (the basis of which they do not seem to predict) and the need for significant state support.

And as they add:

In addition, we think COVID is likely to have hampered public and private preparations for the end of the Brexit transition period, compounding the near-term economic cost. We expect GDP growth in 2021 to be 2.1% lower than in the event the UK were to remain in the EU Single Market and Customs Union. In a normal year, this would be enough to push the economy into recession. Some of this growth is likely to be made up in 2022.

A third of the deficit will, in that case, be Brexit related, in their opinion. And it is their opinion that this must be compounded by moves towards austerity. As they say in their summary briefing:

Persistent policy support will be needed to help the economy through this transition. However, fiscal policy will also have to tread a fine line between supporting growth in the near term and charting a path to fiscal sustainability in the medium term. This is a significant challenge.

It is an obsession that permeates the report, that is paranoid about 'sound government finances', without appreciating that this is precisely what we now have. For example, they say:

This year's deficit will reach a level never before seen in the UK, outside of the two world wars of the 20th century. But what matters much more for the long-run health of the public finances is how complete the economic recovery will be. With the cost of borrowing at a record low, additional spending now that helps to deliver a more complete recovery would almost certainly be worth doing. For now, the government should focus on designing and delivering such support. But, in the medium term, getting the public finances back on track will require decisive action from policymakers. The Chancellor should champion a general recognition that, once the economy has been restored to health, a fiscal tightening will follow.

I highlighted the last point, but it is repetitive, with foreign-owned debt being their excuse for this:

The economic response to COVID-19 has seen monetary and fiscal policy complement each other, as the Bank of England and the government both seek to support the economy. However, this complementarity is less assured in the medium term: upward pressure on inflation (and particularly inflation expectations) could lead to the Bank tightening monetary policy even if fiscal policy still needs to remain loose. The UK's dependence on foreign credit remains a notable additional vulnerability. More fiscal support will likely be needed in the near term. But getting the public finances on a sustainable trajectory in the medium term is also now a key challenge.

And as if to make clear that obsession they focus heavily on the foreign ownership of UK government gilts, before noting what they claim is the resulting cost of this dependence:

The COVID-19 crisis has pushed up government borrowing substantially, meaning that the Debt Management Office (DMO) will need to sell a much larger value of gilts than normal. Our central scenario is for over £1.5 trillion to be raised through gilt issuance over the next five years, double the £760 billion forecast in the March 2020 Budget. There is considerable uncertainty around this amount.

This sum is not all new debt, of course: much is rolled over debt. And they add:

The expansion of the Bank of England's programme of quantitative easing means it bought £236 billion of gilts between March and September 2020, almost exactly the same as the £227 billion of gilts issued by the DMO over the same period. As a result, private borrowing has not been crowded out by government borrowing. The financing cost of quantitative easing is Bank Rate, which is at record low levels, and has therefore further depressed government debt interest spending from already record lows as a share of receipts. However, the tilt towards Bank of England held debt means that the government's debt interest bill will rise sharply if Bank Rate rises.

To this they add:

The expansion of the Bank of England programme of quantitative easing means that virtually all of this new debt has been bought by the Bank. The cost of financing this debt is the Bank Rate. While this remains historically low, it helps to hold down the government's debt interest bill; however, debt interest spending will rise suddenly and sharply when the Bank Rate increases. Since government spending is now more closely tied to the Bank Rate, it will be even more important to ensure that the Bank of England continues to be — and be perceived as — independent and focused on its monetary policy mandate.

But they cannot, or do not, explain why this is the case. They say:

Quantitative easing reduces the effective maturity of government borrowing. This — combined with elevated issuance over the next five years — means that a 1 percentage point increase in all yields would now add £19 billion to debt interest spending in 2024—25, some 76% higher than the £11 billion forecast in March 2020.

So, for the sake of £8 billion, which is utterly immaterial in the context of this analysis, they want the whole of the economy to be run on the basis of the fact that there is austerity to come. The reasoning is not explained.

Nor is there a hint that there may be further quantitative easing to cover debt issues in the years to come, even though the chance that this will happen is extraordinarily high.

And there is no hint of the fact that since these issues are effectively made at base rate, and that the reserve balances in question are now likely to be in excess of £600 billion, and maybe more, the Bank of England has almost total control of short term rates as a result of this structure, as well as long term rates via QE. In other words, it is a strength and not a weakness. a

They also give no hint as to why rates will be rising in the next few years, when there seems little chance of that around the world with Fed, ECB and Bank of Japan policy as it is, so why they think the UK will be so out of line is hard to imagine. Unless, that is, because an independent Bank of England might decide to increase them for the reason that the IFS suggests, which is that, as they put it, without explanation:

Rising yields accompanied by stronger growth would be welcome.

So why do they say this, and what's the reason for the obsession? I can only offer one explanation, and come back to the fact that this report was written with Citi, which is a City-based bank as far as the UK is concerned. And, of course, it wishes for an increase in yield: that's a way for it to make money.

This report from the IFS is not objective in that case. Nor is it fair comment: it is simply a reflection of the obsession fo a bank with increasing interest rates, for which there is no justification, or need. And it is a reflection of the desire of that bank to suggest that bond markets are still in charge of those rates, when they are not. And it is a reflection of the desire of that bank to suggest that what we need is independent control of monetary policy, irrespective of fiscal policy, so that bankers have the best chance of delivering those increases in rates in the interests of bankers but not the economy as a whole.

This report has, then, to be read not as any form of objective review, bit simply as a manifesto for neoliberal policies that maintain the status quo in the interests of the banking community of the UK. The fall of the Institute for Fiscal Studies from any sort of credibility is just about complete. They are instead simply a cover for the wealthy to demand the policies that they desire. It would only take a 55 Tufton Street address for that to now be completely apparent.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Silly me!! I clicked on the article thinking that the IFS had had a Damascene conversion and was proposing a GREEN budget (as in Green Deal)…….. I should have known!!

How they get away with pretending to be fair, reasonable and objective I do not know. At least you are calling them out for being the servant of vested interests that they are.

Glad you agree

It seems to me that the IFS should have written “IF the bank rate increases” rather than “when the bank rate increases”… the Bank of England base rate has been at or near zero since 2008 and indeed the BofE has been consulting commercial banks about reducing base rate *below zero* next year. So positive rates look a long way off and indeed if we take the macroeconomic experience of the 2010s as normal then we might expect bank base rates never to be positive (or at least not above 1% or so) again!

I agree

That is why I call this a Manifesto

And bluntly as about as relevant as one from the LibDems

From Ben Wray this morning on “Source Direct”

http://c0mmonw3al.activehosted.com/index.php?action=social&chash=389bc7bb1e1c2a5e7e147703232a88f6.709&s=1ea5351bef6e60caad7b105e387a6030

I noted

We are of like mind

Infinitely

Fucking

Stupid

…………….again.

I wish we could take them to the nearest vet and have them humanely put down.

The IFS claims to be “Britain’s leading independent microeconomic research institute”. They study the economic behavior of individuals and businesses, not the economy of the whole country. Famously, they “don’t do macro”, and they have essentially given up on the vain (in both sense) task of trying to build an enormous macroeconomic edifice from the ground up from tiny microeconomic bricks. So why do they keep talking about macroeconomic topics?

Because Citi gave them money to do so and provide cover for their manifesto

So when people give you money, do you write what they want you to write and provide cover for their manifestos too?

No

I’m known for my refusal to bend to other peoples’ whims, as some people would no doubt testify today if they were to comment here.

“The expansion of the Bank of England programme of quantitative easing means that virtually all of this new debt has been bought by the Bank. The cost of financing this debt is the Bank Rate.”

Do the IFS economists still believe this nonsense when firstly the BoE now pays interest on reserves to determine base rate? Secondly, do they really believe the BoE has need to be spending the future reserves which Treasury issued gilts are when BoE conversion to current reserves in the Treasury Department’s BoE current account with the BoE has already taken place therefore the gilts (future reserves) have to be cancelled to avoid double spending? Clearly IFS economists are clueless how a reserves based monetary system works because they can’t distinguish between future and current reserves. They should get another job outside of economics!

Why would Citibank want an increase in yield? They are an investment bank in the UK, not a retail bank.

They want the money market operations…

I think that you will also find that they have a retail operation

Their money market operations make up a tiny (less than 1%) amount of their revenues and net income. Rates rising a small amount isn’t going to change that dramatically. That is across Europe as a whole by the way, not just the UK.

They also have basically no retail banking. 400 staff out of 10,000 in Europe, and all of that is in wealth management, not transactional/high street banking, where interests rates rising aren’t going to make any difference either.

So it looks to me like Citi don’t really have an axe to grind one way or another when it comes to UK rates. It also looks like you are just pulling these claims out of thin air because firstly, you clearly know nothing about banking, and second, you would rather smear the IFS by claiming Citi are bribing them somehow to write certain things than actually argue the points they make.

Go on then, why do you think Cioti might want a rate increase, because they clearly do?

You think it would harm their business?

Tell me why?

Do they?

I’ve read much of what they have written, and I don’t see them arguing for a rate increase at all. They do say one might be necessary if inflation expectations start moving consistently higher though – calling it a risk for the UK economy. They go into great depth about their inflation outlook and the risks for both sides of it.

But nowhere do they state interest rates should be raised. That’s something you have claimed they said, when they haven’t.

As for their business, rates rises would probably cost them a huge amount of money. They would make tiny bit more money on their money market operations (which let us recall is under 1% of their revenues), but then lose a huge amount on the $200bn of bonds they hold. Why on earth would they want rates to go up?

Retail banks might want higher rates, and Citi might want that in the US (where they are a retail bank) but in the UK it doesn’t benefit them at all.

Which just goes to show how little you know about banking – but are willing to throw mud at people’s hard, high quality work without so much as a second thought.

I quoted the relevant bit

Well Citi bank and all the other banks can dream on.

You get the feeling that the banks haven’t quite realised who is calling the shots re gov debt rates. Despite the writing being on the wall for the last 11 years that it is not the markets and they still haven’t woken up to the fact that they are in effect indirect employees of the state’s monetary policy. Martin Wolf said years ago that bankers are just civil servants, he is absolutely correct.

The central problem with individuals at the IFS is they either don’t understand how the UK’s reserves based monetary system works or they pretend they don’t because they’re corrupt. They get away with it because the majority of voters are lazy and never think to ask whether the government really needs to balance its books despite repeatedly reading about the government finding huge sums to deal with major crises.

Technically they never both to ask why should the government have the power to create gilts and pay interest on them. This is after all a monopoly power. The same with the BoE having the monopoly power to create reserves to buy these gilts, the voters never question why they should have this power or indeed why they should want to buy them in the first place.

Of course the idea that gilts are inactive reserves which are made into active ones through BoE purchase enabling government spending never enters voters minds. You may as well ask them about the mechanics of the Americans going to Mars in the 2030’s!

If you suggest to the voters they’re effectively like gullible little children in regard to the monetary aspect of how the country’s economy works they go all huffy, belligerent and pompous. It’s hard to take this country seriously given the wholesale unwillingness to be intellectually diligent. It would seem only the utmost pain infliction is going to rouse them from their feckless outlook on life!