Myth

The Bank of England is independent of the government

Replies

Reply - 1

The Bank of England has been wholly owned by the government since 1946. It's very hard for any organisation to be independent of the government that owns it. The Bank of England definitely is not.

Reply - 2

The government granted the Bank of England some independence in 1997, but kept a right of veto over all it does, which means that the independence is pretty limited in practice.

Reply - 3

The only real tool available to the Bank of England is quantitative easing, and the Bank only undertakes this with the specific permission of the Treasury, who underwrites all its risk when engaging in quantitative easing activities. In that case to claim that the Bank of England is independent really does make little sense.

Reply - 4

The Bank of England is independent of the government so long as it does what the government wants. The Bank of England Act of 1998 provides a Chancellor with the option of overruling the decisions of the Bank of England. That means that the Bank simply has a veneer of independence.

Evidence

The Bank of England was nationalised by the Bank of England Act 1946. This said it was:

An Act to bring the capital stock of the Bank of England into public ownership and bring the Bank under public control, to make provision with respect to the relations between the Treasury, the Bank of England and other banks and for purposes connected with the matters aforesaid.

The most recent Bank of England Act was passed in 1998. This described itself as:

An Act to make provision about the constitution, regulation, financial arrangements and functions of the Bank of England, including provision for the transfer of supervisory functions.

Most importantly, this was the Act that supposedly created independence for the Bank of England.

This has to be understood in context. The Guardian reported on the intention to create this independence in 1997, saying:

The Chancellor, Gordon Brown, set the seal on a frenetic first 100 hours of activity by the Blair government when he stunned the City and Westminster yesterday by handing control of interest rates to an independent Bank of England.

From next month, the Government's attempt to take the politics out of interest-rate decisions would mean the Bank would have 'operational control' of monetary policy.

What this makes clear is that the purpose of the move was political: it was to reassure markets that a new Labour government would be seeking to prudent with regard to government finances by passing control of interest rates to the Bank of England.

However, the reality was that all was not quite as it seemed. Section 19 of the 1998 Act said:

19 Reserve powers.

(1)The Treasury, after consultation with the Governor of the Bank, may by order give the Bank directions with respect to monetary policy if they are satisfied that the directions are required in the public interest and by extreme economic circumstances.

(2)An order under this section may include such consequential modifications of the provisions of this Part relating to the Monetary Policy Committee as the Treasury think fit.

In other words, subject to some procedural arrangements which were not onerous for the government to comply with, the Chancellor could at any time overrule the Governor of the Bank of England and the Bank's Monetary Policy Committee. This then was 'independence' with a massive proviso attached, which was that what the Bank did was acceptable to the Treasury. The result has been a close working relationship.

This has been especially true since 2008. Since the time of the global financial crisis, which began in that year, the base rate of the Bank of England, which it used prior to the crisis to influence inflation policy, has been at 1% or less, and now (June 2020) stands at just 0.1%, which is a record low. In this situation it is generally accepted that monetary policy implementation through the mechanism of interest rate changes is ineffective, because any rate change is too small to have any real impact. This is the problem of what is called the 'zero-bound'.

In place of interest rate adjusts the Bank of England adopted what it called quantitative easing. The Bank of England says of quantitative easing that:

Quantitative easing is a tool that central banks, like us, can use to inject money directly into the economy.

Money is either physical, like banknotes, or digital, like the money in your bank account. Quantitative easing involves us creating digital money. We then use it to buy things like government debt in the form of bonds. You may also hear it called ‘QE' or ‘asset purchase' — these are the same thing.

The aim of QE is simple: by creating this ‘new' money, we aim to boost spending and investment in the economy.

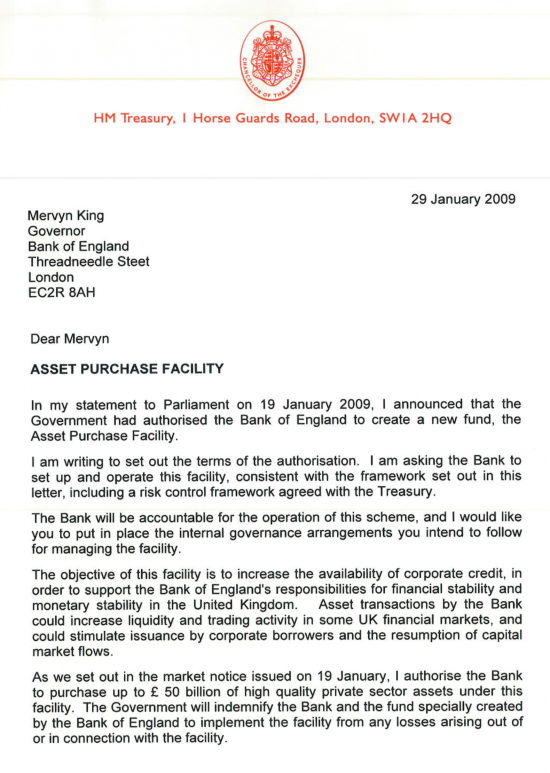

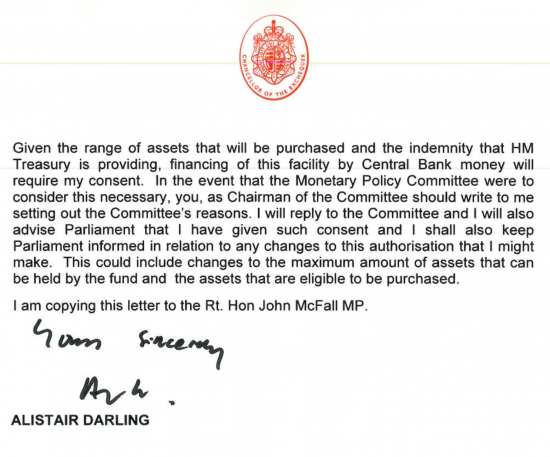

Since 2009 £635 billion has been injected into the economy this way by the Bank of England buying government bonds. £10bn of other assets have also been bought. This is now by far the most important tool available to the Bank of England to influence the economy and control inflation, which is the task demanded of it in the 1998 Act. However, in January 2009, in a letter that now takes some hunting to find on the web, the then Chancellor of the Exchequer Alistair Darling set out the terms on which all QE has been provided, which means that the letter is worth sharing in full:

Three things should be noted.

First, the Treasury had to authorise quantitative easing, and has always had to do so since then.

Second, the Treasury authorised the assets to be invested in, and again, always has.

Third, the Bank of England is indemnified for all its gains and losses on QE transactions, which means the Bank of England is only the agent of the Treasury on all such transactions.

To therefore claim that the Bank of England is independent of the Treasury makes no sense at all. It simply is not. Its major policy is managed under the control of, and for, the Treasury.

Central bank independence is a policy goal of neoliberal economics that seeks to undermine democratic control of the economy and the accountability of the government for it, but it is not what happens in practice.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“The government has been wholly owned the Bank of England“ – um, I think the “been” is superfluous (and as written sounds like a global capitalist conspiracy: the bank owns the government?!).

It is hard to see how any company can be independent of its 100% shareholder.

Which just proves how hard it is to copy edit your own work…edit coming

With Gordon Brown doing what he did (pulling the wool over the voters eyes with the move to supposed BoE independence) who needs a Conservative Party?

He wasn’t a great Chancellor….I said so at the time

The single thing I would give Gordon Brown credit for is that (unlike almost every Conservative or Tory Government since the days of Bolingbroke), as PM he at least does not appear to have panicked when the national crisis hit us in 2007-8.

Unless someone cares to challenge either proposition.

He also kept us out of the Euro

Blair would have gone in

Good point. Credit where it is due.

But wasn’t Brown the first Chancellor to overtly create money out thin air with his baby bonds?

Since 1971 all have done so

I get the idea of injecting money into the economy by buying Corporate Paper. However, the bit I always struggle with is the Bank of England buying Government Bonds. Who do they buy these from (and therefore who is getting the proceeds) and why does this benefit the economy?

They buy them from pensions funds, life assurance companies and banks in the main

The aim is to force them to buy other assets and increase real investment

Iy does not work well – mainly inflating asset prices

We now need Green QE instead

Interesting – particularly because the Pension Regulator seems to be ‘encouraging’ a higher and higher level of pension scheme assets to be held in gilts in order to lower volatility in valuations.

Indeed, surely, the last 12 years (or longer?) has dispelled the myth that entrepreneurs are pacing up and down like caged lions with dozens of great ideas constrained only by their inability to borrow. That view is nonsense. Money is available for good investment (and bad) opportunities but there are precious few around.

The cash that is pushed into the economy by is being hoarded by people that are fearful (50 year gilt yields at 0.5% are testament to this). The government must be the investor of last resort (again 50 year gilt yields at 0.5% tell you that they are failing to do this).

Agreed

A great deal of capital has been generated over many decades by insurance and pension funds; from an endless, burgeoning population of ordinary people invested in (tax efficient) pension saving. By nature these funds are largely risk averse; the natural home for much of it is, and will remain, gilts. At the same time the proposition that entrepreneurially generated wealth and capital is risk seeking, or even particularly entrepreneurial, or innovative is largely an illusion.

Adam Smith was right; the successful operation will often seek the easiest way to success, including the cartel or monopoly, if it can do so. Businesses do not always enjoy competition, once they succeed; they will buy the patent to crush the competition, or use market power to squeeze out competitors. They are rarely bold innovators (save if they began with their own start-up), nor do they invest readily in high-risk investments.

Often the initial investment in new technology is made by Government funding: the public sector. For example, the very first key element of the Google software was developed with a Federal grant. Private investors, faced with high risk, prefer to come in parasitically on the back of public sector (someone else’s) investment. Finding a public sector grant becomes a useful standard proof of project credibility for the investment community.

The dot.com ‘bust’ of the late 1990s is, however an excellent example of the sheer daft, comic, lemming like but revealing character of the scale of folly into which the investment community is only too capable of sinking. The private sector is a lot less impressive than its PR would like the public to know. The Financial Crash should never be forgotten, because the private sector never forgets how to do it again; and again; and again.

As is often the case, we agree

Spot on.

Ownership means that any “profits” from QE belong to us… those profits being the interest received from the government in the form of coupons on gilts they own. In short the cost of issuing gilts that are bought by the BoE is, by definition, zero.

Independence DOES exist for the “little things” – yes, the bank gets to tweak the base rate each time the committee meets and they might even get to choose which biscuits they get. But for all the big things the government is in control (as befits a democracy). Either it can change the Bank’s objectives (which would, presumably result in the BoE altering policy) or it can give direct instructions.

So, why the charade? First, it was pure theatre in 1997 by Blair/Brown to show they were “financial grown-ups”. As theatre, it was successful – gilt yields declined and the yield curve flattened. Second, in the past, rate setting has been used by Chancellors for shameless electoral purposes without any checks/balances (the Barber Boom being the classic example). “Independence” reduces that risk. If a Chancellor wants to intervene it will be a “big deal” and be subject to public and Parliamentary scrutiny. Alistair Darling DID intervene, it was subject to intense scrutiny and, if I may say so, he was proved to have acted wisely.

To be honest, I think the current institutional structure works well as long as we have sensible people driving the bus…. but that is another blog or six!

I can live with the structure…

It does not need the charade

And here is Mervyn King asking the Chancellor for permission on 17 Feb 2009 –

“I should be grateful if you would confirm whether you are willing to authorise the Monetary Policy

Committee to use the Asset Purchase Facility for monetary policy purposes in line with the

proposals described here.”

https://www.bankofengland.co.uk/-/media/boe/files/letter/2009/governor-letter-050309.pdf

There are other interesting statements in the letter, which I had bookmarked. I think the Chancellor’s reply will be available, but requires some detective work.

Didn’t take that long, here’s Alistair Darling’s reply on 3 March 2009 – https://www.bankofengland.co.uk/-/media/boe/files/letter/2009/chancellor-letter-050309.pdf

For some reason, Chancellor letters are in image format, so I can’t extract the relevant approval.

I could find the later ones – it was just the January one I could not

They all prove the point…

There are several places to find a reference to the two later letters. Most recently, I found them referenced in the last set of BEAPFF accounts, which I mentioned elsewhere on the blog are only available in image format (like Chancellors’ letters).

I’ve transcribed an interesting note in the last BEAPFF accounts –

“On 21 June 2018, the MPC reviewed its previous guidance on the level of Bank Rate at which the MPC will considerwhether to start to reduce the stock of assets purchased by the company. The MPC continues to expect to maintain the stock of purchased assets until Bank Rate reaches a level from which it can be cut materially, reflecting the committee’s preference to use Bank Rate as the primary instrument for monetary policy. The MPC now intends not to reduce the stock of purchased assets until Bank Rate reaches around 1.5%, compared to the previous guidance of around 2%. Any reduction in the stock of purchased assets will be conducted at a gradual and predictable pace.”

It’s a bit like juggling the NAIRU. If you don’t like this target, I’ll set another that’s higher – or, in this case a lower target.

I guess later updates to this guidance are available somewhere – was it formally changed around the time the BoE admitted that unwinding QE was at most a very remote prospect?

Are they still pretending to expect a rate significantly above the zero-bound?

No one is expecting a serious rate rise for a very long time unless they’re a scaremongering politician if very limited economic understanding

The letter says that the asset purchase facility is to be financed by the issue of treasury bills. This seems to contradict everything else I have read about QE which says instead that it is financed by new central bank money, created “from nothing”. Does this amount to a substantive difference given that treasury bills are issues by the debt management office?

Read what the BoE said happens

It is new money

Well yes, the things I read before include BofE literature. Still, it’s confusing the letter appears to say something different.

I’d asked before for your view about what happens to the bonds held by the Bank as a result of QE when they mature. I think we are to believe that the government pays the bank and they cancel the funds. If they don’t do that, then the BofE is effectively monetising government debt, which would be inconsistent with the Maastricht treaty.

It is monetising government debt

That is precisely what is happening

And it has been decided by the EU that is consistent with the Maastricht Treaty because the EU is always capable of concluding what it wants when it has to

And it is doing well over a trillion euros of QE this year

One small point that is perhaps overlooked by those who still have the predilection to claim that the mechanics of the banks methods to produce the £50bn requested by Government, demonstrate it is not new money; is that the Government’s suasion of the Bank is founded – in substance entirely – on it “indemnifying” the Bank of England (second sentence, fifth para., of Darling’s letter).

What with?

It’s promise to pay – that’s it

The charge is not to BoE equity then but to government loan account at the BoE itself cleared by QE….

I notice that Stephanie Kelton, in response to Neil Ferguson (an unreconstructed, unapologetic neoliberal) on C4 News tonight (I guarantee there ‘high-fives’ in C4News when they knew they had these two on the same interview): when Ferguson argued that because after WWII the US reduced the debt for several decades, although stimulus now may be required (which even Ferguson seems forced to concede), he still argued the debt must in time come down, arguing from precedent (a US ‘golden age’); Stephanie Kelton seemed to concede the general point, albeit with qualifications; arguing rather that debt reduction (not merely deficit reduction) will happen naturally from stimulus now, to achieve economic growth rather than from austerity.

I would be interested in reaction, if you saw this?

I will watch in the morning

I did a zoom meeting tonight

I intended it rhetorically; like the indemnity itself.

Here’s the clip of Stephanie demolishing Ferguson – https://www.channel4.com/news/economist-stephanie-kelton-on-us-unemployment-crisis-the-only-game-in-town-is-the-federal-government

I did not get the same impression from this as John did. For me, Stephanie gave a clear account of the MMT position.

Ferguson claimed, as historians know (LOL), that the US ran sustained fiscal surpluses and brought the debt down after WWII. Stephanie forcibly pointed out that they did not run surpluses, and that the debt/GDP only came down because the denominator exploded. In a way, it was a pity time ran out and she got the last word. I’d have liked to hear him defend his indefensible position.

The other debate of interest was on Sky News, where “Former BP boss Lord Browne, Nobel prize-winning economist Joseph Stiglitz, economist and author Stephanie Kelton, and Stephen Moore, senior economic adviser to Donald Trump, spoke to Sky’s Dermot Murnaghan about the future of work and the economy after the coronavirus crisis” – https://news.sky.com/story/after-the-pandemic-predictions-of-how-world-of-work-and-economy-will-change-11999508

Stephen Moore spouted his usual nonsense, which was ably countered by both Stiglitz and Kelton. Otherwise, it’s well worth watching. Stiglitz and Kelton agree on most things, although Stiglitz makes it fairly clear he’s still a debt-worrier. They both agree that UBI is not so great, and that guaranteeing jobs is better. Kelton says there is also a place for a UBI, e.g. for people who can’t work, perhaps in agreement with the JG+UBI approach that seemed to be favoured on this blog recently.

Thanks

I will look at the Sky one

One does wonder why Gordon Brown gave the BoE its so called independence. Traditionally politicians had not had that bad a record on keeping inflation down to reasonable levels over the decades,except maybe the 1970’s ,but that was an external oil price cause.

I have seen the view that the BoE actually directly opposed the Coalition government’s 10 years of deflationary austerity policy by implementing expansionary policies of low interest rates and QE.Which was a roundabout way of saying they thought the gov was wrong. Except for the fact that BoE policy did was not successful in achieving that. It did rescue the stock markets and property markets,but this really only helped the wealthier in society who have property and shares. End result; the poor stayed poor.Mark Carney even said that he was not concerned with the “distributional effects” of QE. With an attitude like that one has to wonder whether we should give the BoE any type of independence, if the best they can do is to subsidise the already rich and the financial sector.

Adair Turner called for Overt Monetary Financing in a crisis,but said that it was a huge taboo. Seems to me we have arrived at that point, this crisis may well be a watershed moment on an open money printing policy.

We already have that

It’s happening in the UK

And the US

And the EU

There is no point doubting it

Have we?

If we have, then hallejuha,

I can rest in peace.

Please tell me again ,we have achieved this.

I think we have….

>It is monetising government debt

then why on earth don’t they do ahead and do this openly, instead of all the rigmarole around buying back bonds and pretending all they are doing is encouraging institutions to lend or invest, and suppressing interest rates?

Because they’re playing games to get round Maastricht

This makes a kind of sense and would explain why we did not have a great depression following the 2008/9 financial crash. Doing this via QE however, has regressive consequences, as the Bank is well aware.

Which is why we need Green QE

I agree. But perhaps those regressive consequences are the reason that the vested interests in the financial sector allow this backdoor debt monetisation to happen.

Maybe

But as MMT shows, we have a choice over that

Which is why I find it deeply annoying that many on the left reject MMT

MMT makes sense to me from what I have read about it. I’m also fairly persuaded by Richard Werner’s disaggregated credit macroeconomics stuff, which also advocates monetising debt more openly, financing the PSBR via non tradable bank loan contracts. What are the left objections?

I confess I am not familiar with the detail of his proposal