The Bank of England has published three critical charts this morning that explain what it thinks might happen as we get over Covid 19.

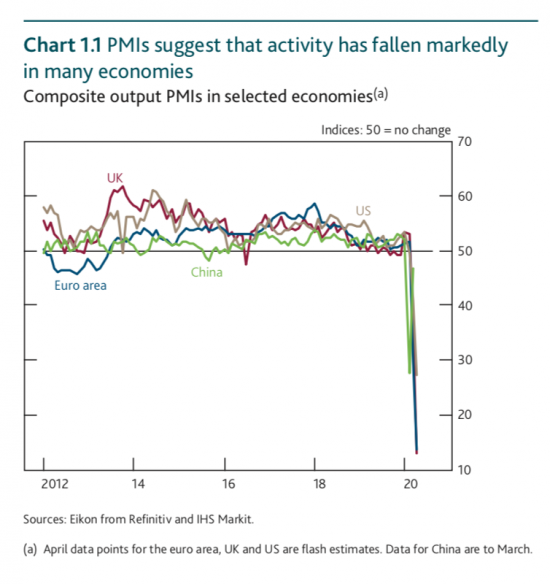

This is what they say has been going on across the globe:

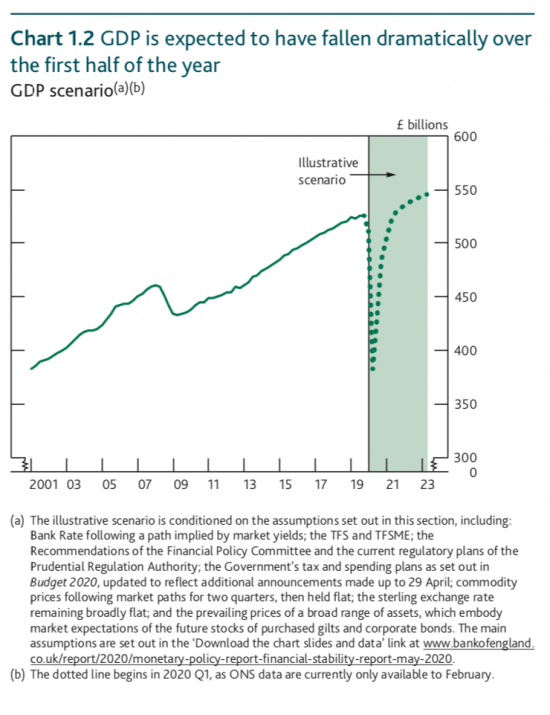

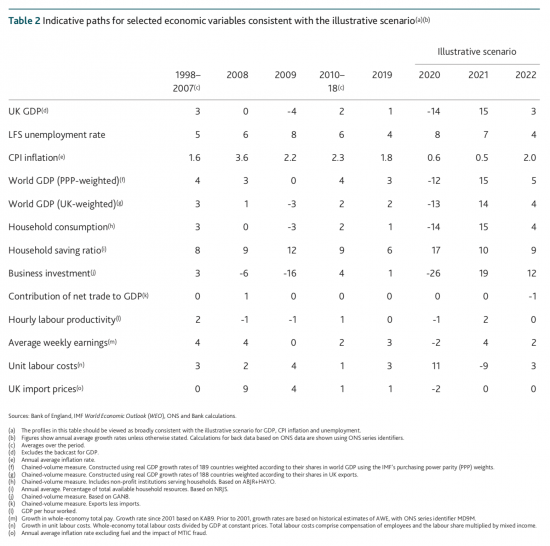

This is what they say is happening right now:

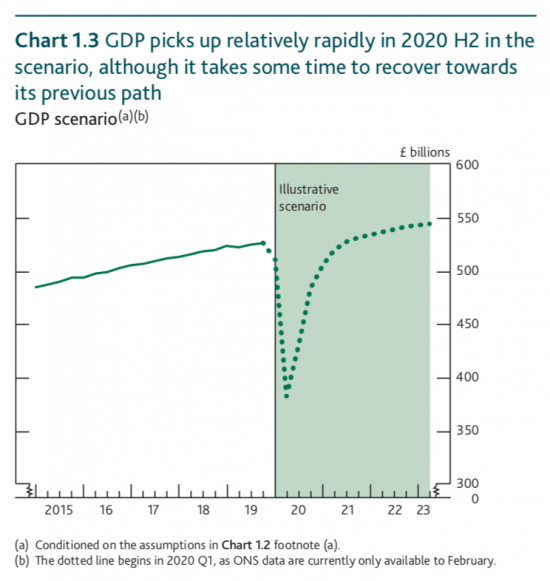

And this is their forecast based on what they call their 'scenario modelling':

Let's summarise that. First they say we fell off a cliff, along with everyone else.

Then they say that the consequence was a massive (unprecedented) fall in GDP: it's been suggested that it's bigger than anything since 1706, and data was not so good back then.

But third, we're going to be back on track by the end of 2021 as if nothing had happened. Voila!

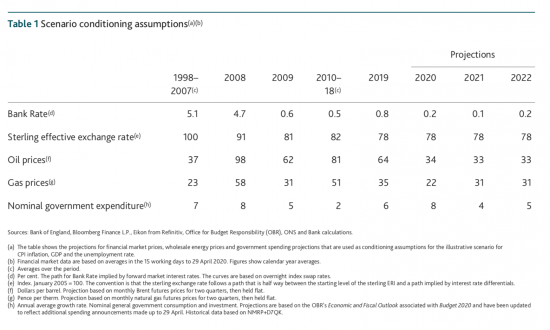

But that struck me as implausible, so I sought out their assumptions (which they do not make it that easy to find: why their smallest PDF of the day had to be hidden in a Zip file is hard to work out unless they wanted as few people as possible to get to it). These are the main assumptions behind that bounce back:

Frankly, these are ludicrous. I am afraid that I always presumed Andrew Bailey was hired to be a willing fool: now we know that is true.

Let me highlight just some of the conditions for the bounce-back that are not going to happen.

First, it is claimed that the exchange rate is not going to be impacted by hard Brexit, which is the only Brexit left on the table. But that is impossible, and not yet priced by markets, I would suggest.

Second, nor are import prices not going to be impacted in any way by Brexit, as is claimed. The whole point of Brexit is that this is not going to be true, and the impact will be adverse.

Third, it is claimed that unemployment will bounce back quickly. If anyone thinks that's true, they're whistling in the wind. Whole sectors of the economy are already wiped out.

Fourth, it is suggested that government spending is going to remain high even though we are bouncing back, which makes little sense and most definitely not what the government will want to do in that case.

Fifth, it is suggested that GDP will virtually recover in 2021 (and yes I know 15% increase after 14% fall is not complete recovery, but 3% in 2022, which is way above average, is the remainder of the recovery). I really do not see that happening.

And sixth, that is because you do not get that growth with 17%, 10%, and then 9% household savings ratios in successive years, which is what is assumed, meaning that exceptional levels of non-spending are to continue, which means growth must be crushed as a consequence, even though the model says otherwise.

Whilst, seventh, business is not going to do all-time record rates of investment as is claimed when it is going to be deeply vulnerable following this crisis and already burdened with debt: that is a claim from fantasy land.

And eighth, productivity is not going to be maintained, as is suggested, unless (and this is what I think the Bank must have been told) all social distancing ends: we know that otherwise that is just not possible.

And ninth, where is the pressure on wage rates to grow by an exceptional amount going to come from in the next couple of years? It just is not there. We have mass unemployment.

I could go on but I do not need to do so: this scenario plan is completely ludicrous and shows three things.

First, that we do not have an independent Bank of England. This is it playing to the government's tune.

Second, to put this forward as a plan indicates a level of either incompetence or outright willingness to misrepresent the truth at the Bank of England.

And third, we should not trust a word they say as a result.

I hate to say those three things, but what else is one meant to conclude?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Richard, this is the kind of ‘scenario modelling’ where the modeller works backwards from the ‘desired (or should that be required?) outcome’ in order to derive ‘appropriate’ assumptions and inputs. You’ve hit the nail on the head: You can only arrive at one reasonable conclusion about what has been happening to the BoE’s oft vaunted independence. It isn’t hard to imagine the impact this modelling ‘exercise’ is likely to have had on relations between the Governor and BoE staff.

Same as most BoE forecasts – start with the result you want and work back to a set of assumptions that might (im)plausibly get you there.

To be honest, nobody takes it seriously in the markets. Just take a look at the BTL comments in the FT to see that everyone knows they are nonsense. And to be fair, what can the BoE actually do? Monetary policy is ineffective at this point.

If you were hoping that the BoE would “speak truth to power” then that (sliver of) hope left with Mark Carney. Not saying he was great but as an independently wealthy foreigner with no career plans in Central Banking there might have been a chance he would say something. With Andrew Bailey there is no chance.

It seems inevitable to me that the corporate and personal sector will spend the next decade repairing their balance sheets (reducing investment, paying down debt, etc.). The policy response to this is NOT inevitable…. there is a choice…. but this government is hard wired to get it wrong.

Agree with all that

Good points. What clinched it for me is the contradictory assumptions between household consumption (aka spending) and increased household savings. So where is the money for spending coming from? Not from wages that is for sure. Are they expecting households to ramp up debt? I know that in the past forecasts on GDP from the OBR was based primarily on increased household debt. Is it possible to have a high savings ratio and a high debt ratio for households? I am not sure how the measures are calculated.

The savings ratio is a net ratio….so if households are net saving more it is hard to see how they are also spending more

Thank you. And also thank you for the post about the potential consequences of our government refusing to shift focus from rentiers and financiers, to workers and productive businessses. That was a bit of an eye opener, to say the least.

I think this is an excellent indication of the problems with /not/ using a stock-flow-consistent modelling paradigm (or an SFC /economic/ paradigm, for that matter) – the accounting literally doesn’t add up. Households can’t save more /and/ spend more /and/ earn the same, it just doesn’t add up, but this apparently doesn’t even register in the minds of these people.

If your economic model doesn’t even pass the most basic accounting rule-of-thumb tests then it doesn’t seem like it’s got the slightest hope of capturing real-world economic behaviour.

I think the BoE dropped a particularly bouncy dead cat.

The thing is that this is not written for the markets.

It has been written for the fellow bullshitters in the MSM as pseudo science as we gear up to get back to normal prematurely. Too many ordinary folk will buy it.

It has ‘disaster capitalism’ written all over it.

Agreed

It doesn’t take much brain-power to work out that if there is a second wave of infection as a consequence of trying to re-open the economy then all such BoE statistical modelling goes out of the window. That such a re-infection is likely cannot be easily ruled out given scientists still don’t know enough about how the coronavirus transmits, in particular whether the virus attaches to very small particles in the air and whether wearing face masks properly handled helps mitigate transmission. Given this incompetent government in the UK and the fact there is still no decision whether wearing face masks outside the home will be mandatory and what the penalties would be for not wearing them the situation is precarious. Any business that opens up needs to have clear direction on these matters. It’s no good say a small store with narrow aisles allowing customers to make their minds up whether to wear a mask or not because social distancing isn’t workable.

Quite liked this by David Blanchflower on twitter yesterday:

‘Just to let all Fed presidents & Governors i have a forecast for US unempt rate in December of 11% – I obtained this estimate by writing numbers from 7% to 20% on bits of paper & picked one? If you make a forecast of what rate it will be please explain how your method is better?’

Seems appropriate here.

Nothing in there on property prices, domestic as well as commercial? Surely there will be an impact of some kind, even if you don’t believe the worst case, with knock-on consequences for the banks, and household propensity to save for starters

Just recieved this email from my favourite London eating place which looks like it is going bust. A good example of a good business desperately fighting to stay afloat.

Brasserie Zédel

Extraordinary Times

From Jeremy King

Extraordinary times can sometimes necessitate unusual actions — particularly when the situation becomes serious and unprecedented such as the situation we find ourselves in currently. I wouldn’t normally talk to you by video, but if you do have a couple of minutes, please watch the above as I am able to explain quickly and in more detail why we need your help.

In short, we in the catering industry have had a terrible shock, in that the Government furlough scheme we thought would look after our employees, does not include tronc, (or service charge,) in the calculation of wages, which ordinarily boosts earnings by 60% and is the staff’s chosen way of receiving remuneration. This a payment that is taxed, and they have come to rely on, meaning many will have insufficient to house and feed their families.

We have done all we can and topped up their wages in March and April but our money is running out quickly. And this is why I am writing to you now. What I am asking is that you buy Dining Vouchers in advance – for any amount that you wish – that can be redeemed in all restaurants across the group without any time limit. For every voucher we will give 50% directly to the staff as income replacement.

We would appreciate any help you can give. I hope you and your families are staying safe and we look forward to welcoming you when this is all over.

Best wishes,

Jeremy King

CEO & Founder

Buy A Gift Voucher

Copyright © 2020 Brasserie Zédel

Unsubscribe from further emails from Brasserie Zédel

A fine place which I know well and had to cancel a booking there during lockdown.

One might also mention Crazy Coqs, the attached nightclub which is a bit like an Art Nouveau Ronnie Scotts, They too will be hit terribly along with the artists who perform there, all of whom will be self employed and mostly on modest incomes.

[…] Cross-posted from Tax Research UK […]

For this sort of rapid bounce back to occur, the Covid 19 threat has to fade away to nothing very rapidly (no second wave after lifting restrictions) and Brexit has to be the roaring success that very few people except fantasists expect it to be.

On the basis of this BofE prediction I feel it safe to proceed with my plans for a Unicorn stud farm…….

[…] we are living in. I admit that I know how lucky I am to live where I do. But nothing, including the absurd economic forecasts we have seen this week and the incompetence of the political messaging changes the fact that we are […]

-It’s Peter Pan’s “Wendy you CAN fly …if only you wish hard enough.” …in graph format.

….. and then reality bites.

I glance at the headlines in the FT this Saturday morning……

(1) South Korea closes bars and clubs – ie. the battle against the virus is a marathon, not a sprint.

(2) UAL fails to borrow money at a sensible (single digit) rate – ie. even with all the Fed support, lenders will not lend to insolvent businesses (and old aircraft are poor collateral).

(3) Sweden’s “no lock down” policy may or may not be a health disaster….. but the economy still is. ie. even is lock down ends, our economy is still in real trouble.

(4)…..and I haven’t got to page 2 (well, not quite true as I am reading online but you get the picture).

Agreed the forecasts are unlikely but they are a gauge to measure subsequent government action.

If the Bank of England and the Government do whatever it takes to make these predictions come true then it is still possible that something close could happen.

Helicopter money can be dropped, taxes cut , credit lines can be further extended

and the bank of england underwrite the potential bad debts of the banks.

The game being played is to maintain confidence, maintain price levels and to get the economy moving again.

Its what the Japanese have been doing for years.

The economy can run on credit for a long time and as long as the rest of the world does the same and agrees its the sensible thing to do in the circumstances and doesn’t dump the currency and sell off Uk assets then it can work.

It might require more action than a conservative government would be happy with but that is their problem not a logical impossibility.

You assume people will bounce back

And you assume business still have capital

And that they will respond in ways they never do to crises

They won’t

The Bank of England model is complete nonsense