The word decimate is rarely sued correctly: it stands for the culling of one in ten, usually as a punishment in a Roman legion. It will also be inappropriately used in this crisis if it is used to describe the consequence for smaller businesses. That is because the crisis has already resulted in one in ten small businesses being shut, dissolved or liquidated according to the Association of Chartered Certified Accountants. And they expect much worse to come. As they have put it:

And if the lockdown lasts another four weeks, respondents estimate that 38% of the businesses they advise will definitely not be able to access the additional cash they'll need to survive.

The lockdown is going to last.

In the FT not dissimilar stories are being related, with it being noted that:

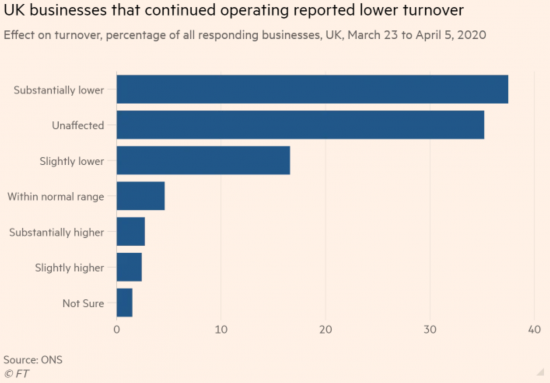

One quarter of companies in the UK have temporarily closed because of the coronavirus lockdown and the majority of those still operating have reported lower turnover, according to the Office for National Statistics.

They add:

Meanwhile, a study by Begbies Traynor, the insolvency firm, found that more than half a million companies were in “significant distress”. The analysis was based on county court judgments ordering companies to pay their debts.

It should be noted that this is up, but there is an underlying trend.

But as the FT notes, for a small number of businesses, activity is up at present. Convenience stores are amongst those doing very well, I gather. And then there is Amazon.

The data is, of course, patchy, but it would seem that the story is not. I strongly suspect that significantly more than 10% of smaller businesses will fail in this recession. That is almost inevitable.

It has, of course, to be said that some of those would have failed anyway. That is the way that these things go: significant numbers of small businesses fail at any time. So the question is about excess failures, as it is about excess deaths amongst people. There the telling chart is this from the FT:

The combined total of businesses with substantially and slightly lower turnovers is the majority of those in the survey. And that is the concern. Some of these may survive, but those with any significant overheads will find it very hard to do so for very long.

There is no doubt that the UK will be facing a significant change in its business landscape after this, and a radical difference in the number of small businesses in operation after it, whilst those that will arise from the ashes (because they will; of that I have no doubt) will be smaller and under-capitalised for some time and not pick up the slack.

There are tough times ahead. It is going to be a very long time before the fat lady sings on this occasion.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

This is the soft underbelly of Tory policy on Covid-19 and indicates their stupidity and short-sightedness with regard to preparedness despite being warned in about 2016.

HM Opposition needs (at the right time) to make sure voters know this and the business community in particular.

My response to this would be a national job creation policy – putting jobs back into services – well paid ones as well as offering more support to small businesses. There would be fewer telephones lines and numbers, web based contact and more real people to help you.

As you have said many a time Richard, the future to a better world is a caring society because such a society needs people (and therefore jobs) to make it work.

I look at the housing service I work for and the cutbacks in staff to check up on tenants for example. We just completed some new housing and they were allocated to mostly younger people. Within about 3 months these younger families had almost trashed the place – they seemed to have no idea how to live. Had we had the old system of housing visitors who would do just that – visit and check and advise – then I’d argue that any problems would have been nipped in the bud.

As things are all people see is that the scheme cost the public sector £1.3 million and all we get is a brand new, well designed, warm and high quality housing scheme being treated like a dump (the new residents thought it was OK not to use the bin store for their rubbish and stub out their cigarettes on the window frames of the double glazed windows for example). We are literally cutting our own throats as we go along – all because of constant cutting of budgets undermines our ability to manage what we have created. We only found out what was happening because a local Councillor wanted to visit the scheme – thank God we saw it first otherwise………? It just gives the public sector a bad name, creates resentment amongst hard pressed families not entitled to affordable housing and well, the cycle of underinvestment, reputational damage and economic division just keeps going around and around.

As a company owner I have a great working relationship with my bank relationship manager (so much so I don’t want to mention the bank name but its one thats supposed to be doing well with CBILS). A loan was “approved” 2 weeks ago and we were waiting a few days for paper work. Then we were waiting till the end of this week for paper work, now its being chased up and they will come back to me.

It should be said we are not a business in immediate danger as many are in this article but equally the comfort that would be provided from the loan means we don’t hold up payments to other businesses and thus it helps the whole cyclical business chain. Business preservation requires active cashflow management and so its easy to see how one businesses nervousness rapidly transmits problems to several others replicating much like the spread of Covid 19.

I can only assume the issue with our CBIL means that there is either too much workload, which is scary given the low volume of loans currently given compared to what is likely to be needed, or that we have been put to one side so the bank can concentrate on ‘fire fighting’ those businesses who are teatering on the brink. The latter is understandable although I would have expected to have been told that so at least expectations are managed.

A big problem in my humble opinion is even the pretty well capitalised firms in the SME arena are slowing the volume of payments as they put on the brakes in fear for their own cashflow and so this only exacerbates the problem for others. This of course supports the premise of pretty much all your articles on CBILS which is that the delay, whatever its cause, is going to have a catastrophic effect on small businesses…

Finally, you probably have covered it in another blog post but the ommission of company directors who are paid via dividends from any level of ‘wage support’ is likely to put massive pressure on smaller companies and potentially renders the benefit of the Job Retention Scheme (and other measures) redundant as a director has to remain solvent for a company to be solvent. CBILS may help as a bridge but essentially directors will be borrowing from the companies borrowing trying to keep both afloat.

Thanks

Interesting to note

Should we not be planning for a Roosevelt set of public spending works to build council homes, care homes, clean canals, open branch railways, write guides to counties, lay broadband, repurpose small hotels, plant trees, re-wild water courses?

Yes, if the Green New Deal is to be part of this

But that won’t happen on day one…

Meanwhile, it seems Big Business is getting largesse, in private, without accountability. https://positivemoney.org/2020/04/bank-of-england-provides-7-5-billion-in-big-business-bailouts-all-hidden-from-public-view/ (Peter May on PP highlighted this article)

Agreed – and Peter is doing a good job

Richard,

Could I ask you to post once a day with an open question to prompt your most excellent followers to scratch their heads and come up with a solution to a particular issue. In this way perhaps lateral exchanges will contribute to real-world solutions?

For example, to the question “How can small businesses regain their feet during the present COVID-19 crisis?” I would offer: try marginal pricing.

Turnover is comprised of direct costs, fixed costs and profit(loss). At the very least businesses could exclude the profit element from their prices to make a contribution. A widget sold for £100 (pre-covid19) with a direct cost of £30, fixed costs recovery of £30 and profit of £40, could be sold for £60 and the financial position of the company in the short-term would be unaffected?

Just a thought. About to disappear to the patio with a tin of draft Guinness. Not the real thing, but pretty damn close.

[…] Edwards is an accountant I met through this blog whose quietly offered opinions I value. He suggested yesterday […]