Where did QE money go? There's been over $4 trillion of it created in the USA, which the Fed is now planning to unwind at a rate of £10 billion a month in what could, at that rate, see it take more than three decades for the programme to come to a close.

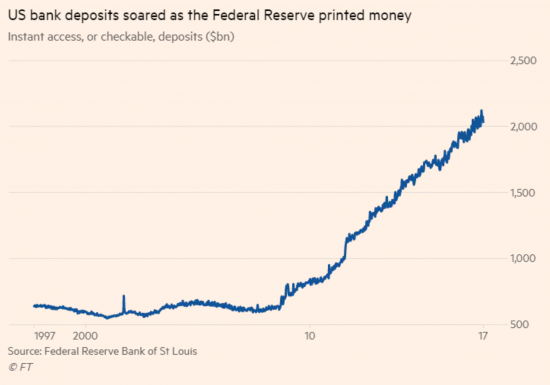

But the question the FT asks this morning is where all that QE money went. And the answer is pretty simple. It went into making new money. And large parts of that were not spent. This is the rise in the value of non-interest earning deposits in the USA over the last couple of decades:

That is $2 trillion on non-interest earning accounts right now because those with wealth have no idea what to do with their money. That's a pretty staggering statistic.

That is $2 trillion on non-interest earning accounts right now because those with wealth have no idea what to do with their money. That's a pretty staggering statistic.

And Trump wants to make rich America richer.

Whilst the Fed wants to use this money to reduce the scale of its balance sheet without actually adding anything to economic activity in the process.

And all the time what is needed is more state investment to build a better America, for which purpose $2 trillion could achieve quite a lot.

It really is time to put money to work.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Yes. Yes. And Yes.

I’m not sure why you equate non-interest earning deposits in the USA with QE. Those non-interest earning deposits are held by private customers in checking accounts that do not pay interest. Yes, some of them may have sold bonds to the Fed via brokers, and some may have sat on the cash, but wouldn’t that be rare? Didn’t most bond-owners simply buy other assets, i.e. participate in roll-over, hence QE had so little impact on spending? https://www.fool.com/investing/2016/12/13/the-hidden-cost-of-bank-of-americas-deposits.aspx

Because the Fed DO

Because look at that graph

I’m sorry but I don’t have a subscription to the FT so I can’t follow up on the graph. I see the correlation between QE and a huge increase in non-interest-paying checking deposits. But causality? Another explanation might be that with the sudden drop in interest rates huge numbers of accounts that were interest-bearing ceased to be. It is not that plausible, surely that private customers whose bonds were sold to the Fed, and now in receipt of QE, would happily have swapped an interest-bearing asset for a non-interest-bearing asset. Why would they do that? Surely they would re-invest? (If there is data on this please tell me, this is a genuine question.)

At the same time, why do you assume that non-interest-bearing deposits are doing any less work than interest-bearing deposits? As an accounting identity an increase in deposits for a bank must be equal to an increase in liabilities. The only non-interest bearing liabilities for a bank are cash.

OK, try offering another explanation

Where did $2 trillion come from?

Start from there

Given how much some shares plunged in 2008 I can hardly blame people that do have savings are reluctant/scared to risk losing x % if the said shares go down.

Richard, Firstly, Fed QE did very little to the long-term trend of the US private banks balance sheet, have a look at the graph at this link https://tradingeconomics.com/united-states/banks-balance-sheet and click on MAX for the 40-year trend. All that QE did was correct the stumble post-2008. So you anyway need an explanation for the growth of the balance sheet, regardless of QE. Secondly, I already did offer another explanation for the growth in non-interest paying checking account deposits, but I will repeat it. When interest rates crashed post-2008 it is possible that a huge swathe of accounts that used to pay interest ceased to do so.

Finally, you ignored my point about non-interest-bearing accounts v. interest-bearing accounts. Why do assume that the former do less “work” than the latter? As I pointed out, any increase in deposits is matched by an equal increase in liabilities, which, except for cash, are interest-bearing for the banks. To pay that interest somebody has borrowed at interest and must have a purpose for doing so, i.e. to spend it on something. Of course we may not approve of what they spent it on, that’s a different story.

We weren’t discussing the size of bank balance sheets

Total cash held has also gone up

And your last point rather proves what I say – no interest paid because nothing was done with the liquid funds

My understanding is that apart from “vault cash” as the Fed refers to it, everything on the asset side of a private bank balance sheet DOES have interest paid, however liquid or illiquid. Therefore your $2trn, except for the few percent held as vault cash by the banks, is all “at work”. (The $2trn on the deposit side must have a matching $2trn on the asset side.)

But not for the depositor

It is free capital for the bank

And I get the horrible feeling you believe in fractional reserve banking from that comment

Any response to Martin Wheatcroft’s response to your response to his response to your Guardian letter?

https://www.theguardian.com/business/2017/oct/02/peoples-qe-risks-the-bank-of-england-going-bust

He shows he does not understand that tax does not constrain spending, nor the operation of money

Richard, the reason I provided the link in my first response is that it estimates that the cost of “interest-free” deposits to the bank actually amounts to something like 1.6%. In current times that is significant. So, sure the depositor sees no actual interest but receives it in kind. But you still miss my point: all deposits are equally “at work”, regardless of interest paid, no interest, or interest in kind. That is because, as an accounting identity, the assets side of the balance sheet has to match the liabilities side. So, if the liabilities side goes up $2trn, so does the assets side go up $2trn. And the only private bank assets that are not “at work”, i.e. receiving interest, is vault cash. (Prior to 2008 one would have to include “excess” reserves as non-interest bearing, but that has changed now as you know.)

Here is the link again if you want to check that 1.6% figure: https://www.fool.com/investing/2016/12/13/the-hidden-cost-of-bank-of-americas-deposits.aspx

I really think you might need to think hard about what banking is

Banks do not lend out depositors money

It really is time people realised that

So if all deposits were withdrawn (a ‘bank run’) presumably there can be no problem with the lending of the bank?

Of course there can be: deposits provide banks with capital

Remember depositor funds belong to the bank, not the depositor

Richard, you are not answering my point. If the private banking sector experiences a $2trn increase in liabilities, of whatever kind, then it must experience a $2trn increase in assets, of whatever kind. As an accountant are you going to deny that?

No

But you’re also saying that the asset is put to use

I am saying that need not in any way be the case

I am saying sums loaned are not deposits lent out

I think you need to read some modern monetary theory

I have read MMM. But we don’t need that to consider the question you pose: are there bank assets that are “not lent out”? We agree that vault cash and formerly excess reserves fall into that category. But please name any other form of financial asset held by a bank and recorded in its asset column that is not “lent out” and receiving interest. Indeed how could a financial asset be a financial asset if it did not earn its holder a return? Other than cash under the mattress?

Deposits are not lent

I think it’s unbelievable that so much freely available knowledge is ignored by the vast population of so called educated informed “experts”. I was always told follow the money, I guess it’s really “where did it come from and how did it end up there?”.

I guess I have to agree all that free money had to go somewhere and it went where money always goes, where it feels comfortable, in with a crowd of other money.

Richard, unless I’ve missed something, it has been quite a while since you blogged in any detail about the concept of universal basic income.

This seems to be gaining much traction around the world with pilots recently approved or initiated in Canada, Hawaii, Finland, and Scotland to name a few.

http://www.independent.co.uk/news/world/americas/canada-ontario-trialling-universal-basic-income-until-2020-free-money-4000-people-a7701431.html

http://www.independent.co.uk/news/world-0/hawaii-universal-basic-income-salary-wages-wealth-distribution-chris-lee-a7826931.html

https://www.theguardian.com/world/2017/jan/03/finland-trials-basic-income-for-unemployed

https://www.thersa.org/discover/publications-and-articles/rsa-blogs/2017/09/scottish-government-will-fund-basic-income-experiments

If you’re inclined, I’d very much welcome you revisiting this, with some of the enlightening analyses/number crunching you typically spoil us with.

I note an interesting analysis recently published by the Roosevelt Institute in the US which suggested that such a program would expand the US economy if funded by government debt, but not if funded through increases in taxation.

http://rooseveltinstitute.org/wp-content/uploads/2017/08/Modeling-the-Macroeconomic-Effects-Report-Brief.pdf

Time….just time…..

Erm…. Mike King,

“My understanding is that apart from “vault cash” as the Fed refers to it, everything on the asset side of a private bank balance sheet DOES have interest paid,…”

This is a bit technical for me, but surely ‘Vault cash’ and ‘everything……on a bank balance sheet..’

which ‘DOES have interest paid…’ is not the bank’s assets, but its liabilities.?

Even is money ‘deposited’ is non interest bearing it’s still a liability.

Bank assets as I understand it are the loans it generates.

Neat

But the analysis offered also assumes fractional reserve banking and it does not exist

Where did all the QE money go?

Rishard, if you are looking for one reason for the floating-about cash-with-nowhere-to-go question you will not find it. There are several. So it’s cumulative.

!) Mom and Pop retail investors think the Bull can’t keep running. They may well be wrong. They’ve been wrong for most of the second longest run in history. It’s safer in the bank. When they get over their fear resultant on the last hiding they took in the stock market they’ll get in just in time to get wiped out.

2) Savvy investors don’t try to time tops. Nobody rings a bell at the top, they say. So they get out with their targets in the bag and wait for a correction (crash if they’re lucky) and buy bargains. You can’t buy without a cash kitty. They know what is sound, but sound fundamentals don’t stop panic selling. So there will be bargains for the patient and they can actually afford to wait – they aren’t trying to make a living they are increasing wealth.

3) Well advised investors (with serious money and paying for the advice) are long gone. 12 months or more ago. They have their pile and their priority is safety – defensive strategies. Some in cash (interest level irrelevant) some in other markets.

4) Savers (as opposed to investors) are increasing cash holdings to offset diminishing interest returns. ‘Uncertainty’deters spending it.

5) Some people have more money than they know what to do with and are constitutionally risk averse. Their money is all in increments smaller than the deposit guarantee (or whatever it’s called). They believe in banks. They trust the government to bail the banks if it all goes TU.

6) Some who would/might buy bonds can’t see the point of the hassle because the returns are lousy at present. Better keep the cash on hand in case the Roller gets a puncture and they need to replace it.

7) Other reasons which may or may not be rational, but which I can’t think of.

8) irrational reasons I can’t be expected to think of.

9) Dodgy accounting figures for reasons best understood by bankers.

As to where the rest of it is.

Much of it is inflating equity prices to a level which, though currently sustainable, bear little relation to conventional measures of value. Unwind QE and the bubble will pop. External factors could also cause panic selling.

The bubble is inflated by spare cash wanting a return, borrowed money which is cheaper than established returns (past results are not a reliable guide to future performance, but what the hell?)

Big business buying back its own shares for personal boardroom bonus returns and shareholder value. (this is the one element which is ‘safe’ if the winnings are carefully squirreled outside the the vulnerable markets. Some of it will be some of it won’t. Some of it is in those bank figures in cash)

Passive investment funds which follow the trend but thereby keep the buying going.

Lots tied up in property. Some speculatively, and some earning rental income.

A very small proportion spent on high end goods and services.

When that graph you show above changes direction and starts dipping down it’s probably time to put the tin hat on. Because something major has changed; even if it’s ‘only’ market sentiment.

Agreed

But do you sleep?

Oh yes, I sleep. It’s what I’m really good at. I just don’t keep regular hours because I don’t need to.

I sometimes know that feeling

Mike King,

3 quick things in reverse order of importance:

1. Deposits are not lent out. Loans are deposited. This oft-cited BoE statement bears that out:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

Visionary theorists like Sweden’s Knut Wiscksell knew this 100 years ago:

http://www.econlib.org/library/Essays/wcksInt1.html

2. Richard Murphy’s main point relates to the liquidity preferences ( http://www.investopedia.com/terms/l/liquiditypreference.asp ) of wealth holders over the past 9 years and that point remains.

3. R. Murphy and the Financial Times have also made a point about a relationship between QE liquidity preference. You didn’t quite like it apparently, you were asked for an alternative explanation and didn’t provide one. Explanations, right or wrong, are conclusive. The words “it is possible that” do not preface an explanation they belong to a thought bubble that you apparently couldn’t be bothered trying to substantiate. Confusing “private banks balance sheets” with those of the Fed doesn’t help either and reveals a lack of attention. If you are going to be contrarian in a big way you need to do the homework.

Meanwhile..whilst on that topic, there seems to be evidence emerging that QE had a couple of effects in this respect. Giving this post another run might be timely:

http://www.ft.com/intl/cms/s/0/4d936278-4cd4-11e5-9b5d-89a026fda5c9.html?siteedition=intl#axzz3kJuPcxa8

http://www.taxresearch.org.uk/Blog/2015/08/28/qe-was-life-support-for-financial-markets-pqe-is-life-support-for-real-people/

The chart that goes with it is startling.

Thanks

Appreciated

So, cutting through the thicket of monetary theory and bank deposits, we come to a very simple point: QE created money which all went to banks, and to the very wealthy; and they do not deploy their wealth into productive investment.

It has, in short, created nothing except profit for the banks and hoarded cash.

Precisely

Nile,

The key is the pretence that the economy is the other way up. Defiant of gravity.

This model insists falsely that wealth ‘trickles down’ through the economy whereas in reality it flows upwards.

The peasants grow turnips and they end up in the king’s treasury.

If the King has enough turnips he can raise an army and go steal more turnips from the adjoining kingdom. These extra turnips keep the king in turnips until the peasants (whom he lost as cannon fodder) replace themselves and the cycle goes round again.

Stolen turnips trickle down no further than as payment to the barons as spoils of war. Peasants who steal turnips (even while at war) are looters and their lives are forfeit, (See ‘Slaughterhouse 5’ by Kurt Vonnegut. The fate of Edgar Derby – Dresden 1945) So it goes.