I noted the Bank of England's suddenly discovered concern about personal debt in the UK yesterday, and the threats that they are issuing to banks who have extended such loans. As I noted, I have been warning on this issue for some time. I have done so based on data available to the Bank of England at any time over the last few years. This data is that published by the Office for Budget Responsibility at the time of every budget and autumn statement over the last few years, of which there have been quite a lot.

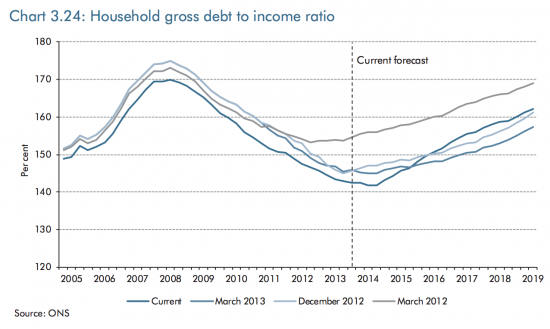

Take this forecast from the December 2013 OBR report, which usefully summarised a series of projections in the growth of household debt to household gross income:

It was clearly anticipated at that time that household debt would grow steadily.

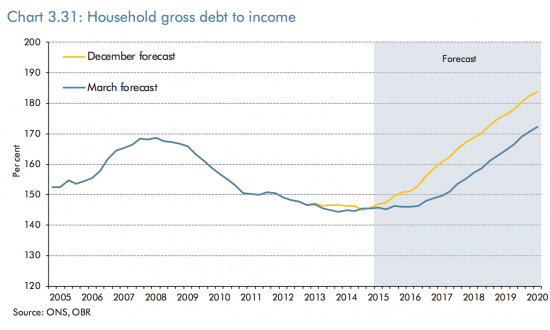

By March 2015 the forecast looked like this:

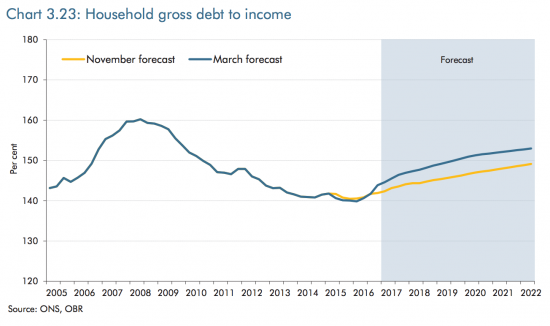

The projections were markedly higher. Record rates of borrowing wee forecast. In fairness, Carney sounded some alarm signals, but not enough. Admittedly by March 2017 the forecasts were down again:

Note the 2017 forecast is remarkably similar in all cases. And in every case the forecast is for a rise thereafter. So why is Carney surprised? This has been on the cards for a long time. And it is not by chance. The simple fact is that if the government tries to borrow less (and that remains its objective) then someone else has to save less or borrow more than at present. And since, given Brexit, it is not obvious that will be the overseas sector, consumers are the most likely to increase their borrowing.

Note the 2017 forecast is remarkably similar in all cases. And in every case the forecast is for a rise thereafter. So why is Carney surprised? This has been on the cards for a long time. And it is not by chance. The simple fact is that if the government tries to borrow less (and that remains its objective) then someone else has to save less or borrow more than at present. And since, given Brexit, it is not obvious that will be the overseas sector, consumers are the most likely to increase their borrowing.

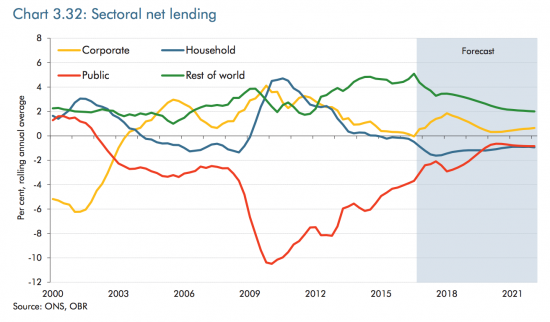

And I stress, this is not by chance. It is a necessary consequence of less government borrowing. That is because of what are called the sectoral balances, which I explained some time ago, here. In essence, in macro economics it is assumed that all transactions in sterling take place between four sectors. These are the household sector, business, government and the rest of the world. For once this is a good assumption: those do describe all the available options. And what national accounting, again entirely reasonably, assumes is that when considering transactions in sterling the economy (when the foreign sector is added into the equation) the transactions between these sectors must balance. Again, this is true: it's only a restatement of the accounting truth that for every debit there must be a credit.

So, in that case if the overseas, household and business sectors all saved the government has to borrow. As borrower of last resort it has to. This is shown by this chart, this version being from March 2017:

Government borrowing since 2009 has existed almost entirely because almost every other sector has chosen to save. But we now know consumer patterns are changing. Savings ratio are reaching all time lows and borrowing is rising, rapidly. It's the corollary of the government's desire to offload its obligation to borrow onto an economy unfit for any other sector to take over the task without major risk arising.

I repeat, Carney should have seen this coming. The government's plans to increase consumer debt and so put us in this position have existed for years. So three questions. Why didn't he say that this policy was wrong much earlier? And why didn't he put steps in place to prevent it earlier? And why didn't he say government retained the duty to borrow, which is a virtually risk free activity? Because he did none of those things the fault for this is Carney's. And George Osborne and Philip Hammond's, of course. None can duck responsibility for the crisis we're facing. They made it.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

What is driving this I feel is that there is still much in the public sector that needs to be exploited by the 1%.

Manufacturing crises (Kleins’ ‘Shock Doctrine’) is the best way to manufacture consent and make a killing on state assets.

Carney is after all ex-Goldman Sachs. Leopards do not change their spots – more’s the pity.

because people feel more confident about their future under a conservative government.

Really?

On the sector balance, what worries me is that only the corporate sector is in surplus, see graph

http://www.progressivepulse.org/economics/economics-101/follow-the-money/

All money creation flows to the corporates and they are not spending it. I cannot see how that is sustainable.

Neither do I

It’s why we need higher corporation taxes…

I feel a blog coming on..

[…] Credit card debt is not, of course, the whole of the personal debt market. But the following chart, from the FT, provides a remarkable insight into the growth of the personal debt problem: […]

As long as private banks stand to gain profits from the interest made on selling debt to households and individuals, this situation will continue. Carney has placed no restrictions on what the debt can be used for. In the absence of any guidance or control over what debt is used for and in the presence of low interest rates, the incentive for banks to lend for speculative purposes (including mortgages and car finance which are backed by assets), is still the same as it was prior to the crash. Nothing of any significance has changed and people still have to either rely on credit or choose to use it in order to maintain their lifestyles.

you do get more checks when buying things on credit now than before the last crash.

i know its a bad thing to say, but i think that sky should also be classed as a financial service and more checks made to see if people can afford it.

You graph of household debt to income conveniently starts at 2005.

Had you started at 1997 when Labour came into power you would have seen consumer debt level increase by over 250% in the run up to the financial crisis.

In the 10 years since then, actual personal debt was broadly the same level, falling slightly post crisis and increasing slightly to a small 10% increase.

That certainly suggests that the rise in consumer debt should be directed to the Blair Labour government, not the Coalition or the Tories!

Source: Bank of England (total personal debt)

Check my other post on debt today that has longer term data that shows what you are saying is nonsense

If you comment here you have to add value with you disagreement. It us not clear you are

Please see the link below.

Can you explain this graph which is from the Bank of England and looks at total debt, not just one component.

http://www.thisismoney.co.uk/money/cardsloans/article-3913560/Household-debt-hits-record-high-1-5-TRILLION-says-Money-Charity.html

This shows mortgages and other debt in one graph

The concern is not with mortgages right now but other debt

I agree with your analysis completely Richard and I think the answer to all three of your questions to Carney is the same and is simple : to do so would let the cat out of the bag – that is to say that in actual fact it is the responsibility of Government in conjunction with the Bank of England to strive on behalf of all ‘ the people of the United Kingdom ‘ ( as the B of E website says ) to ‘ maintain monetary and financial stability ‘ , but they – the Government and the Bank of England – have derogated from this responsibility in the ideologically driven belief that it will all be sorted out by the private sector . It’s the secular version of the Dualism of God and Mammon . How ironical is that ?

Deeply