Let me put three suggestions before you. The first is that the UK is a massively divided society, with that trend having increased over time.

The second is that since 2008 the UK has suffered a savings glut, as Marin Wolf on the FT has called it. That is, we have vastly more savings than can be usefully invested in productive activity in the UK. These savings are, of course, largely owned by those on just one side of our divided society. The glut drives the government's deficit.

The third proposition, which has been pretty commonly held since Adam Smith first proposed it as a basic tenet of taxation in 1776, is that our tax system should be based on ability to pay, which most will interpret as meaning that it should be progressive, overall.

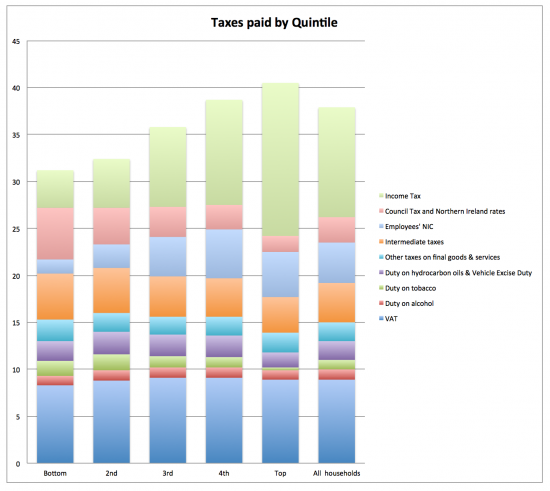

Now let me offer you three facts. The first is that the UK tax system is not very progressive, overall. It may only be flat at best. This chart indicates likely overall tax rates excluding the impact of those on capital (capital gains tax and inheritance tax) and the impact of income shifted to companies by quintile. Data is from the ONS. Flattening of the data to quintiles removes data on the very high rates paid by the bottom decile and the advantage of low corporate and capital tax rates to the top decile. Even so it is notable that I had to assemble this graph from ONS data: they did not publish these overall rates:

Note that excluding the impact of income tax the UK tax system is almost completely flat for the first four quintiles and then significantly benefits the top quintile. It is only the impact of income tax that changes this. Capital and corporate taxes significantly reverse this trend but are not in the ONS data.

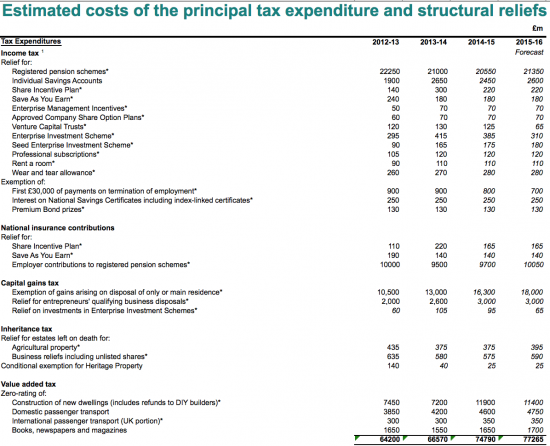

Second, the UK tax system massively subsidises the already well off under income tax rules. The following list us of what are likely, in the main, to be tax subsidies to those already well off in the UK, based on HMRC data here:

Why are those subsidies to the well off? For a start, the first group are very largely about subsidies to saving. And as a matter of fact, to save you must have money over at the end of the month. And you cannot beat about the bush, that means you are both better off than most people and have savings, of which we have a glut. You are also in a minority in the population as this chart based on ONS data of wealth distribution:

Other reliefs go to homeowners via capital gains, as does a VAT relief on new houses benefit them and landlords, who are, of course, In addition VAT subsidies to public transport go very largely to the better off commuter. Of course the numbers could be finessed, but by far the biggest, for pensions, is anyway understated because tax paid by pensioners is offset against the tax relief figure, meaning that the cost of pension relief is understated by more than £10 billion in the figures noted above.

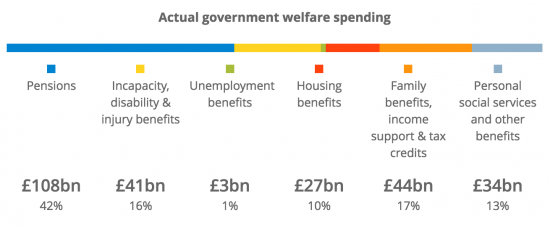

Third, let's compare that with the cost of benefits. This is the latest summary data from the ONS:

I am going to presume that most people think that we should care for the elderly and those with disability. Likewise I presume that most people think that support for those with real needs, whether for social services, or to let them stay in their homes, are vital. Personal social services are of this nature. So that leaves support for what might be thought of as more discretionary welfare payments amounts to about £74 billion a year. Except of this sum £27 billion is housing benefits and they go straight to landlords so they provide no benefit to claimants at all: they are actually a subsidy to savers who own rental properties which means this sum should be added to the total £77 billion subsidy to the better off noted above, bringing that sum to £104 billion, and leaving what most think of as benefits costing £47 billion.

Third, it is argued that because the UK continues to run a deficit benefits must be cut. Substantial cuts to benefits for those with disabilities as well as to broader universal credit and housing benefits are all scheduled for April 2017.

Let me offer three conclusions. The first is that when we have a glut of savings the last thing we need do is give tax subsidies to those with wealth. To achieve cuts in savings rates, cuts to the deficit which those savings drive, and to create growth rational economic policy would demand cuts to many of the tax reliefs I note, but most especially to the tax relief on pensions and ISAs. These subsidies are not only not needed - their recipients are already well off - they encourage behaviour completely contrary to our macroeconomic need.

Second, if these subsidies were cut and savings reduced as a result then the UK deficit would fall: the government has to act as borrower of last resort for the savings of UK depositors. That's a role it gets as creator of the money supply. Cutting saving by reducing subsidies that currently inflate their gross sum makes sense within the context of the deficit narrative as a result.

And third, if cuts are to be made then this analysis is so clear, even if some discussion on detail is glossed over by using relatively simple headings (albeit that they are all the ones the government uses), that it is obvious that it is not those on benefits who should face them. To impose the planned April 2017 cuts cannot be justified.

In summary, what is very obvious is that the wealthy are now by far the biggest recipients of state benefits and it is they, and they alone, who must face cuts as a result.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Interesting blog, as always.

Just one small query re. Housing Benefit: Is it not the case that the majority of HB is paid to Social Landlords (Housing Associations, Local Councis) with ‘only’ £9.3bn (£9.3bn too much IMHO) going to Private Landlords?

Maybe

As I made clear I have used general headings to explore an idea

The result is meant to be good enough to support my current thesis, not be definitive

It seems that since 2001, the private rented sector has grown by 69% according to Shelter. However, the social rented sector (council housing) is still the largest with 3.8 million households and the PRS bubbling under at 2.7 million. The social rented stock in the council sector has shrunk since the 1980’s because of right to buy and also Council’s not being able to build replacements until recently (now council landlords are allowed to keep their rent instead of sending it back to Government for it to be redistributed nationally).

So now, the HRA (housing revenue accounts) are stand alone income and expenditure pots for councils that stand or fall on how well they are managed locally.

The Tories enabled more local control of the HRA this way but just to show you what a nasty and mean swine George Osbourne was, he made all RSLs lower their rents by 1% for 3 years in 2015 which means that (for example) many landlords will build fewer affordable new homes because of the reduction in income.

I work in social (council) housing so I am biased I suppose but I think that the Government (and the tax payer through transfer payments which I think may help to pay for HB) get excellent value for money from my colleagues and I because social housing tends to be better maintained and managed than too many private landlords who let the other more responsible landlords down with poor housing (and I should know because we get referrals out of these dumps that people are renting in the private sector using benefits all of the time).

The city where I work has around 67% of tenants on some form of HB (full or partial) even though our rents are still lower and no more than 80% of market rents if they are higher than the social rent. It is true that we have more elderly people on fixed incomes but the HB bill is also helping the low waged too.

Our biggest challenge now is that the under 35’s are to have their benefit capped at the lower private sector Local Housing Rate making even our council 1 bed flats too expensive for them to rent. This is the because the rate covers the cost of renting a room in a shared house in a private house – not a 1 bed flat!!

How nasty is that? We are now having to build smaller properties otherwise we are going to see a lot of younger people sleeping rough.

Housing Associations have their own problems of which I am no expert but I hope this helps.

and private landlords largely pay tax on the rent which is not the case with social landlords (so on corporation tax rates from benefit received would be about £3 billion) let alone the other subsidies. People reckon social is so generous being cheaper yet (according to a study I read( its only on average 16% cheaper which given a landlord could pay between 20-45% its not actually cheaper put in context)

Most landlords do not pay tax

They get tax relief on borrowings instead

Sam

The tax situation is very complicated. True, in our role as a manager of the publically owned housing stock we do not pay tax because the asset essentially belongs to the government and is a tool of government policy and of course as such Government does not tax itself.

However, my org is also an RSL (registered socially landlord) and we are charged vat when we are building for social rent but owned by us which is a cost to us – just like housing associations in fact and just like private landlords.

Most of our higher rents are 80% of market rates and we also have loads of tenants on social rents which are cheaper still making your 16% seem a bit dubious. It does vary from area to area so for example 80% of market rent in say Derby will be a whole lot cheaper than 80% of what market rents will be in an inner city London borough. It’s best not to generalise too much on such matters.

I bet that study didn’t take into account the quality of the housing though.

Housing benefit is not paid for privately rented accomodation.

That benefit is called “local housing allowance”

The £9 billion paid in lha is is about a third of the money private landlords get allocated by the state…

https://www.theguardian.com/money/2015/feb/09/private-landlords-gain-26-7-billion-uk-taxpayer-generation-rent

Accepted

It does not change my overall thesis

On my extensive travels around the country, I have often heard from people “those earning £10k more than me should pay more tax” or similar words.

In other words, those on £20k think those earning £30k should pay more, those on £30k etc…

VAT, income tax, IPT, council tax, National Insurance, capital gains, plus a myriad of others, the majority of people simply do not understand taxation.

I found this blog rather confusing Richard until I figured out that tax expenditure is what most of the world calls a tax break. It was still confusing though from where it said that UK taxation across incomes was flat at best, and when it said it significantly wasn’t.

Sorry, I presume tax spend is a known term

And I made clear the flat issue, I accept

But apologies: candidly, I wrote it between sessions in bed feeling pretty grotty

How have you arrived at us having a savings glut? I can see a certain section of the older population having it, but the statistics I’m aware of show consumer debt per adult in the UK at higher levels than before. I cannot find figures that exclude mortgages, but http://themoneycharity.org.uk/money-statistics/ and http://www.independent.co.uk/money/is-britain-facing-a-debt-disaster-a6808086.html point to savings being the last thing on most people’s minds.

Trillions of corporate savings

Savings of the ultra wealthy

The savings are deeply concentrated: the data I use shows that

Richard, why have you ignored the most regressive tax, Council Tax? Owner of £200m Westminster home pays £100 less pa than tenant of £345 pm flat in Weymouth. The fact is that landlords are getting the biggest subsidy of all.

It is in there

Sorry looked at wrong chart.

The current incredibly low level of mortgage interest is effectively a give-away to homeowners. But only people in comfortable, safe jobs can get a mortgage, consigning the poor to paying rent for life.

You state that the tax system massively subsidies the well off, which is true given the published figures. But is tax relief on registered pension schemes a subsidy, or just deferred taxation? Yes employees and employers do receive tax relief on their pension contributions, while at work but they pay tax on their pensions when in retirement. I recognize that there is some subsidy because many contributors may be higher rate taxpayers but only standard rate taxpayers at retirement. However to take the full relief as subsidy is inappropriate as it is deferred taxation not a subsidy because you will have counted the tax paid by pensioners in your total income tax figures.This appears a good reason to restrict tax relief on pensions to standard rate tax band.

I am not suggesting total abolition necessarily

As you say, basic rate would be a start and then the deferral argument may just make some sense

But you’d have to abolish the tax free lump sum then