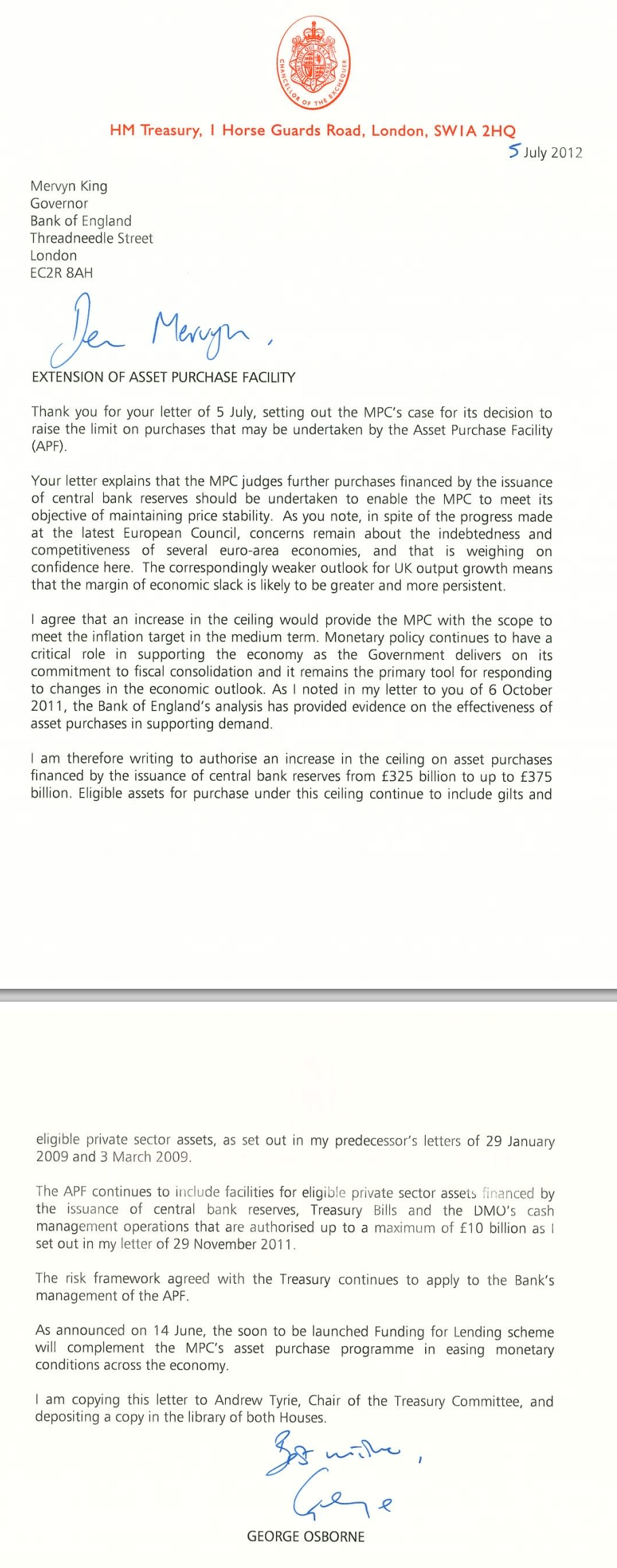

Here is another Treasury letter from 2012 authorising the purchase of assets other than gilts (and so, by default, People's Quantitative Easing), this time from George Osborne in 2012:

Rather boringly I have been told over the last few weeks that my ideas on Bank of England independence will ruin the UK's economy.

Rather boringly I have been told over the last few weeks that my ideas on Bank of England independence will ruin the UK's economy.

And as boringly I have been told that the Bank of England buying private sector and other assets would be a wholly impossible intrusion by it in the economy.

And that if something like I have proposed were to happen the confidence of foreign investors in the UK would collapse.

Now lets deal with the realities. First, such interventions have already been authorised, by both Labour and the Coalition and so the Conservatives and LibDems, by default. Second, in modest amount (£1 billion, in the early days of QE) they happened. Third, no one has fled from the UK economy as a result.

So what is all the hysteria about People's Quantitative Easing about? Would anyone like to explain?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Foreign investors are like bond market vigilantes and seven headed hydras. Terrifying fictional monsters designed to keep people in their place.

If ‘foreign investors’ don’t like Sterling priced assets, then they can sell those Sterling priced Assets to somebody more enlightened and take the appropriate loss. The assets continue to exist and continue to deliver a return regardless of what ‘foreign investors’ decide to do in the secondary market.

Foreign investment is only required if you think you haven’t got any money. We both know that can easily be replaced with Green Investment ex nihilo – for example via an Investment Bank set up for the purpose.

Indeed

My understanding is that UK pension funds are desperate to buy more gilt or gilt-like assets. Equities are just too volatile and don’t deliver the long term returns needed. Fixed income assets can be used to match assets with expected liabilities. Gilts are just too rich for schemes to commit right now. If foreign buyers exited UK pension schemes would be very happy. So too would their sponsors who’d have one less risk to worry about and might even be encouraged to invest more as a consequence!

Did the Fed not buy non Treasury assets in its asset buying programme? Agency MBS and other securitised assets?

I was at a talk by Roz Altmann last year. Roz, of course, is now the Tories’ pensions advisor, which is ironic because she was bemoaning the lack of imagination by the Bank in only buying gilts!

I do find this broad topic hard to fully understand though. That link (in a previous thread) to the Bank paper on money creation was really helpful.

However, I still can’t help but feel that it’s 4 years’ too late as economic stimulus is less needed (so far!) although infrastructure investment is. Unconventional asset purchases were required after the GFC but much less so now. That’s not to say I don’t agree with a National Investment Bank, I do and it’s hardly radical as Vince Cable rightly advocated that RBS remains in public ownership with such a remit. Osborne has been quoted this week as saying he wants to complete the sale of RBS and LBG because the Government has no role owning banks. That’s just crazed ideological stupidity.

The letter above highlights the importance of monetary policy during a time of fiscal tightening. It reminds me of JK Galbraith’s criticism of monetary policy in The Affluent Society. He said that it overwhelmingly benefits people in the finance business, the people closest to the money. The public don’t understand monetary policy as well as fiscal policy. That’s an understatement: try explaining the money creation process to the average voter!

I simply don’t agree we do not need stimulus now

We have the most fragile of recoveries with all the signs that we can rely on no export aid

Yes, I can see that but politically the case is weak. By this I mean that Osborne and CBI among others are heralding the recovery. It is both fragile and unbalanced but the public believes the economy is in good hands. What is commonly (mis)perceived as funny money being printed to finance projects and real loans to real things that employ real people will be seen as a left wing hobby horse damaging credibility. Politically the time for real QE (I don’t like the term People’s – again it just sounds like a Lefty thing, purely from a PR perspective) is when another bout of QE is to be considered.

More importantly, someone should ask Roz Altmann what she thinks. If the Tories’ own pensions tsar says the the Bank should buy real loans to real businesses – which I am certain she said at that talk, albeit at a time when QE was in full flow – it could both embarrass Osborne and Cridland et al, and give a qualified thumbs up to PQE protagonists.

The “recovery” to date has been exclusively based on internal demand & that has been largely achieved by Osborne’s clever trick of allowing everyone over 50 to access the money previously “locked up” in pension pots.

This wasn’t, by any stretch, a bright idea, but it is also a trick you can only pull once. Whilst I can, sadly, think of dozens more ways by which Mr Cameron can make all our lives collectively worse, & by which Mr Duncan-Smith can more effectively ruin the lives of the poorest people, I honestly can’t see where Gideon is hiding any more rabbits.

Peter,

The Fed did buy non-treasury assets in the form Agency-MBS as part of LSAP (Large Scale Asset Purchase) programs. The agencies being Fannie Mae and Freddie Mac were (officially at least) government-sponsored agencies. Those actions probably encouraged Darling and Osborne – with one notable difference perhaps being that the BofE was authorised to purchase a broader range of “eligible private assets”. In doing so they expanded the scope of unconventional monetary policy even further.

None of which detracts from the case that Richard is making, if anything the US example actually adds to the list of precedents which support his argument.

As for the ‘fragile’ UK. With 0.1% inflation, a persistent 0.5% rate of interest and unemployment trending back up again for the last 2 months I would have thought confident reports of a recovery are exaggerated and probably reliant on the assurances of those who persist in calling it a recovery. They seem to have created a perception but perceptions alone are never sufficient.

The problem they have Richard I imagine is that some idiots signed us up to the Washington Consensus and they don’t want to upset the big boys.

Andy,

Washington and the IMF are overtly critical of EU austerity. For the last 3 years they have been urging Germany, the UK and various others to ease their fiscal policies.

When those guys are telling you to loosen-up you know you’ve got a problem.

http://www.ft.com/intl/cms/s/0/1fd77e84-0920-11e5-b643-00144feabdc0.html?siteedition=intl#axzz3joWRbNzC

QE for the people would be best spent on a unconditional basic income in my opinion.

As QE is inflationary we can just jack up interest rates to what ever they need to be to offset any inflation created.

This way the economy will have more debt free money in it (base money/ M1) and less credit money.

This would be a much healthier ratio as an overall money supply in my opinion.