Some time ago I was invited to write on tax for the CBI's Great Business Debate and the resulting blog was published yesterday. I stress, it did take a very long time to come out: I wrote the blog sometime in November and I can only presume it took until late January for a sufficient response to be written, which seemed to be a pre-condition of its publication.

And what a response it is. Written by the CBI's chief economist, Rain Newton-Smith, most is pure PR waffle confirming the good news that the CBI believes in motherhood and apple pie. I am sure many people will be relieved.

What the CBI also does do is confirm its commitment to its tax principles, which suggest that companies explain their tax charges which sounds great until you realise they are opposed to public country-by-country reporting and the Fair Tax Mark, both of which seek to achieve this goal. So candidly, those principles can be dismissed as nonsense.

As can two more things be so dismissed, the first of which is the CBI's ‘golden rule' for economic management. They raised this issue because I argued in my piece that:

Tax is about raising money. But let's be clear: this exercise is reclamation of what the government has already spent into the economy through its commitment to fulfill a democratic mandate. Spending always comes first and tax comes second.

There are three points of explanation to note on this last issue. First, governments can, and always have, spent before they have tax revenues precisely because they can create new money. Second, that spending is not predicated on having tax revenues available. The quantitative easing programme, and the effective cancellation of government debt that it has given rise to proves that: deficit spending can be met without taxation. And third, this makes clear that there is a fundamental relationship between tax and monetary policy as well as tax and fiscal policy. In that case to treat tax as an administrative, technical or micro-economic issue, as the CBI very largely seems to do, is to fundamentally misunderstand its nature and significance. This is bound to lead to the promotion of policies that are politically and economically implausible, at best, which is why some of the CBI's contributions to tax debate are not only bound to be ignored but have to be ignored.

In response to this the CBI says:

The government does have a role to stabilise the economy through tax and public spending, particular when other levers to stabilise the economy, such as lowering interest rates, have already been pulled as far as they can go. However, sustainable public services are only possible through the government balancing its budget over the economic cycle.

Our ‘sustainable fiscal rule', as set out in our report Our Future Public Services — A Challenge for Us All, is consistent with this — that, once the Government has balanced the books, public spending should not exceed tax revenues over the economic cycle. This allows tax and spending to play a role in times of economic difficulty, so long as the Government support is then paid for once the economy recovers. The alternative is ever higher public debt and ever higher debt interest payments which leave less space in the government budget for spending on much more productive things like science, education and health.

Let me just consider that claim, because it is economically quite incredible. What the CBI are saying is that if there is government borrowing at any time then it is the duty of the government that incurred it, or any subsequent one, to then not only restore a balanced budget but actually run a surplus until such time as all the debt incurred has been repaid.

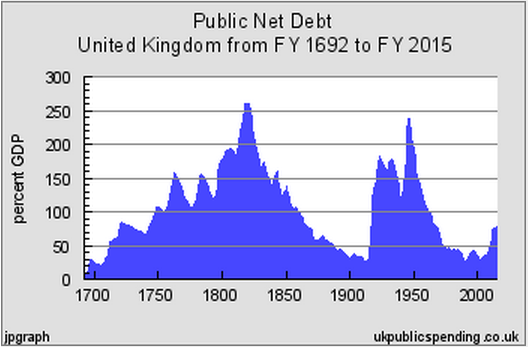

The logic is, of course, that of microeconomics and the corner shop in which situation if an overdraft has been incurred then it must, of course, be repaid. But there is an obvious problem with this logic, because whilst the corner shop cannot print its own money any government with a central bank can. The UK has been in that position since 1692.

The following graph shows the pattern of government borrowing as a proportion of GDP from 1692 until the present day:

You may note one curious fact about that graph and it is that not once, not ever, has the debt disappeared. Governments have, over a period of 323 years, never followed the CBI's advice. They have never felt the need to repay the sums they have borrowed, and there is good reason for that: they have not needed to do so.

One reason for that is that there has always been a strong demand for UK government debt (which is hardly surprising: it's one of the safest things anyone can invest in).

The second is that having realised it could always sell its debt no government has ever seen the reason why it should punish an economy by unnecessarily withdrawing government spending on the supply of goods and services that the government, and their varied electorates, have considered necessary, and affordable, partly, at least because of that ongoing demand for government debt that they were more than happy to meet.

But now the CBI says all that is of no consequence: 323 years of experience that balancing the books at the end of each economic cycle is not necessary should be ignored, they say, and we must do it in future. It's faintly ludicrous that they say that, but let me explain why. It's because, as is glaringly obvious, we have never had a debt crisis as a result of not doing so, and despite the fact that debt as a proportion of GDP has been vastly higher than it is now and that interest has formed a far larger part of the UK budget than it does at present as a consequence we have also not, again, ever had a government funding crisis as a result. To put it another way, the CBI's claim that failure to comply with its rule will lead to all sorts of problems is simply untrue; it has never happened, and candidly, won't happen. Which means the CBI is wrong.

As they are also fundamentally wrong on the issue of what I call green quantitative easing. The CBI is apparently relaxed about £375 billion of funding being issued by the government to support banks. But it says of QE funding being used to create jobs, to create real investment and to boost the well being of its members who actually undertake useful economic activity:

Claims that the Bank of England's ‘quantitative easing' programme (printing money to buy Government bonds) provides a get-out-of-jail for unfunded public spending are misguided and risks ducking the tough but necessary decisions to reduce the deficit.

This is just misleading: such action is not ducking the tough decisions needed to reduce the deficit. It does instead create the necessary liquidity within the economy to create the economic activity that does in fact provide the only hope that the books might ever be balanced. In macroeconomics you can never cut your way to a balanced budget simply because putting people out of work does not mean you do not need to feed them anymore in the macro economy, but you do now have to feed them despite the fact you are asking them to do nothing in exchange. This is the simple error of logic that the CBI, fixated as it is with micro economics that assumes that people once sacked disappear from view, makes.

Or does it? Can the CBI really be so uninformed on economics, and so lacking in intellectual capacity that it really cannot see that its arguments make no sense at all? Or is it simply promoting nonsense to support its view that the state must be shrunk for purely dogmatic reasons that, I am sure they believe will increase the power of capital? I regret to say that I think the second of these two options is likely to be in play here, and that's worrying, to ay the least.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

At what point is a government/society big enough/respected enough to print its own money, rather than “balancing the books”? Serious question – I read somewhere that Devon’s economy is the same size as the DRC; both are considerably smaller than a large number of corporations. All three have (or ought to have) the best interests of human beings, aka society, at heart, and yet we propose radically different economic & governance models for each. Not sure where that train of thought will lead, but it’s one of the building blocks towards trying to rebalance a world economy that’s very different to everything that’s gone before.

When it has its own currency and central bank

And people are willing to trade in that currency

It is a fact that I acknowledge that too much printing destroys the credibility that permits it in the first place

Balance is key

We have printed for 323 years without a problem

Devon can’t

CBI =

Considerably

Bogus (Blinded?)

Institution

And to think that this was the same CBI who actually were against Thatcher’s Conservative Government and their high interest rate monetarism which destroyed a lot of our manufacturing base in the early 80’s.

Our differences of opinion with Richard Murphy are part of a much bigger debate on the role of economic and fiscal policy in times of stress.

The majority of our members feel that we need to reduce the fiscal deficit over time and lower the proportion of government spending taken up by debt interest payments. Our approach to fiscal rules therefore takes account of this important context, as set out in the CBI’s response to Richard Murphy [http://www.greatbusinessdebate.co.uk/opinion/cbi-response-to-richard-murphy/].

We recommend that once the public finances have returned to balance, the Government should continue to run a balance budget over the course of the economic cycle. That way, over the long-term, debt will be prevented from rising above already elevated levels and savings can be made on debt interest payments to allow more of the Government budget to be spent on schools, hospitals and the like.

Respectfully, and as I have shown, that is not the pattern of UK history, despite which, or perhaps because of which, we have propsoered

That’s because government spending is the backbone of GDP growth

And of almost all technological innovation

It also provides the safety net that lets people take the risk of working for private sector employers

And it also provides many businesses with by far its largest customer

But you wish to forego all that?

Why?

What on earth would make you wish to shrink the economy for all but a very few which is the inevitable consequence of your policy?

And why would you deny people the debt they want to buy?

Please explain, in full, because all you have offered is dogma, not argument

I can’t believe that a so-called serious institution like the CBI confuses micro economics with macro economics. You also seem to have had a mass memory loss as to the causes of the 2008 crash which was not because of a government budget problem but a collapse of the banking sector due to bad management by that sector and the public purse being asked to prop up a system that had effectively eaten itself alive.

This is a fundmental error of enormous proportions and gives the CBI as much credibilty as the ratings agencies got out of the 2008 crash. That is zilch credibility you understand as far as I am concerned. In fact as far as I am concerned you might as well wind yourselves up as an organisation as I believe that the CBI has dipped well below the competency levels required to be a representative body of this type. Sorry to be so direct but your stance is flagrant rhubarb.

I think it was Paul Krugman who once wrote that a household is not a country and that a company is not a country either; that the comparisons between country and household/business economic behaviours and objectives were too diffeent to be really comparable. As Steve Keen has also pointed out, treating macro economic issues as micro issues is just plain wrong.

This misrepresentation and confusing of serious issues to the public is also part of something that Adam Curtis explores in his new film ‘Bitter Lake’ and how politicians these days attempt to over simplify issues for the electorate – ‘balancing budgets’ is one such over-simplification. By over-simplifying this issue, you miss out the detail and the detail is HUMAN BEINGS.

I’ve revised what CBI stands for and offer this instead:

Can’t

Be

Independent

It’s a funny kind of conservatism that proposes to tear up over three hundred years of economic policy. 1692, the year of the Salem witch trials in Massachusetts, incidentally. The good old days!…

Hello CBI, may I ask where you believe money comes from? I’m intrigued by your suggestion an economy needs to be ‘balanced’, a term reminiscent of Mr Micawber’s dictum, clearly specific to individuals or households but not sovereign nations. Further, why is it you think the government has to work to a budget at all when it can create currency, fiat currency, in any amount it wishes without it necessarily being devalued, unlike the bad old days when the amount in existence was supposed to be representative of the gold the country (allegedly) had in its vaults, and no more?

That Micawber reference is very apt

I have to question whether the CBI represents the majority of British businesses on these issues.

If we consider taxation, ask a High Street optician how they feel about their biggest competitor, buying-up or pushing out all the small businesses with the benefit of tax-free cash – obtained by declaring a venerable British corporation to be the unprofitable subsidiary of a brass plate in Switzerland.

The greengrocer next door isn’t exactly pleased with *his* most dangerous competitor, undercutting tax-compliant businesses by sending the cash on holiday to the Cayman Islands… And enjoying a taxpayer-funded supply of free labour under Workfare.

Both of those businesses are under pressure from Austerity – as are their behemoth competitors – because of the depressing effect on consumption. I find it difficult to believe that the CBI has succeeded in persuading a majority with an abstract economic argument, in the face of visible reductions in turnover; that they claim to have done so when that argument is flawed – or at best, has very persuasive counter-arguments – is surprising.

I would also like the CBI to reprise their position on Quantitative Easing, an economic rescue policy that acts as a money-pump into banks – surely there are CBI members who might argue that *their* business, or their business sector, is a better recipient of free money.

Alternatively, should I look forward to the CBI publicising all the feel-good stories, from what must surely be a majority of their member businesses, about the transformation in the economy powered by the ‘QE supercharger’ of proactive and plentiful business finance pumping out of the banks?

5th columnists are everywhere.

I have read these comments by CBI with astonishment. Do they not realise that 97% of all new money is introduced as debt?

They claim to represent corporate UK but most corporations are funded and financed by shareholders and/or bank borrowing. In their utopia perhaps they think that corporations should only be run by 100% shareholding directors.

They then seem to be extending this thinking to the macro-economics of running a sovereign nation. Thank you for challenging this, Richard.

I very much doubt they have a clue about money

Remember the BoE had to point out just a year ago that most economics text books on this issue are profoundly wrong

CBI =

Can’t

Be

Intelligent

I promise that this is the last one!

It’s a conundrum, isn’t it? How much right wing economic nonsense is the product of deceptive, underhanded and self-interested but at the same time knowing and self-aware skulduggery and how much is just straightforward ignorance? I suppose the two things are not mutually exclusive.

This blog hits the spot — it also reads as a history of wars and economic crashes in one graph, and ought to be taught in school as fundamental knowledge. A nice school exercise to fit wars and economics to the graph and learn about history e.g. the rise of the Rothschild dynasty and the Napoleonic wars, the maxima in the graph. Also, if only journalists had the courage to discuss: 1. Govt debt and 2. Macro/micro economics and the absurdity of the Con/Dem/[new Lab] presentation of these [facts]. Would TV economists readily present these as headlines to the public, I fear not – they would consider their individual future employment prospects. As to the CBI, again the desire to cheerlead and be employed overrides critical thinking, and the thought of being a whistleblower – well, that does not bear thinking about.

Over the weekend, Prof Richard Werner was interviewed on RT (not BBC, of course) and he explained how he had introduced the term Quantitative Easing, which was a Japanese translation, to describe the process of easing the monetary supply in Japan in the 1980s. His process involved their treasury directly investing into their economy for infrastructure, housing etc NOT through the banks. BoJ rejected this idea probably as a result of pressure from BIS.

BoE and The FED took his QE term and applied it to their process of buying treasury bonds from the banks but in reality his process much more accurately describes your Green QE.

Which is why, unsurprisingly, Richard is relaxed with my version of QE – which harks back to his

The slightly astonishing thing is that tax avoidance hurts the majority of the CBI’s members ie. the ones that do not tax avoid on a grand scale. Tax avoidance distorts ‘the market’ and shifts competitiveness towards larger multi national companies. So why don’t the CBI pick up on this?

Like I said, 5th columnists everywhere, easy to implement if you have enough money to spread about so if you’re backed by the banks who can create the stuff then I’d think it’s a doddle… don’t fight the unions or other organisations of influence, just get your own men in at the head of them.

How long is this ‘economic cycle’ that CBI wants to ‘balance the budget’ over? I always understood that this was a theoretical concept rather a real period, used only because economic models require it and, as such, has no meaning in the real world. Don’t they realise that, either?